Global Interventional Neurology Devices Market

Market Size in USD Billion

USD

3.23 Billion

USD

6.45 Billion

2024

2032

USD

3.23 Billion

USD

6.45 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.23 Billion | |

| USD 6.45 Billion | |

| % | |

|

Interventional Neurology Devices Market Size

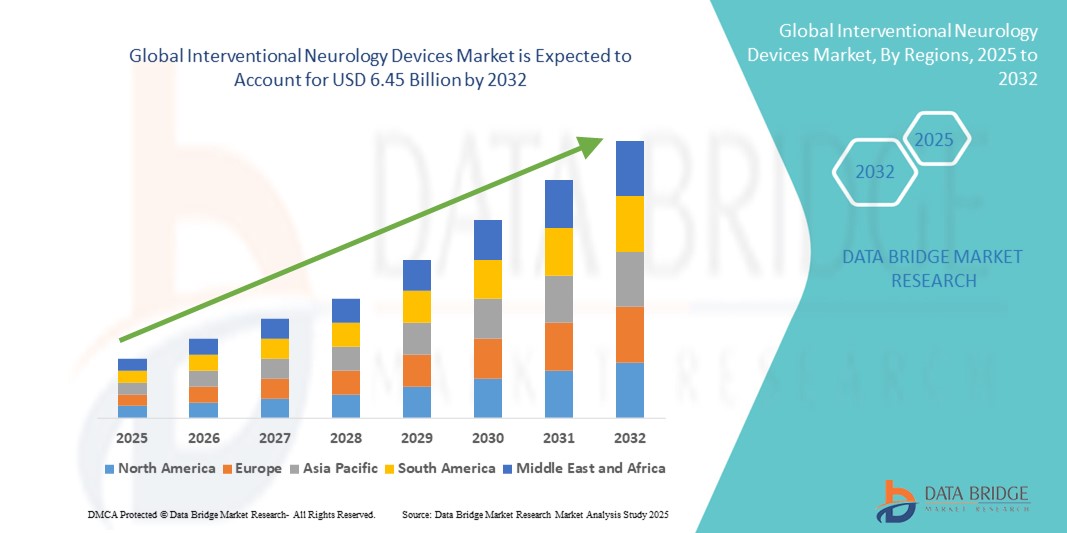

- The global interventional neurology devices market size was valued at USD 3.23 billion in 2024 and is expected to reach USD 6.45 billion by 2032, at a CAGR of 9.00% during the forecast period

- The market growth is primarily driven by increasing adoption and technological advancements in minimally invasive procedures, catheter-based interventions, and image-guided therapies, which are transforming patient care in neurology

- Furthermore, rising prevalence of neurovascular disorders, growing demand for efficient stroke management, and the need for precision in complex neurological procedures are fueling the adoption of Interventional Neurology Devices, significantly supporting the industry’s expansion

Interventional Neurology Devices Market Analysis

- Interventional neurology devices are increasingly vital components in modern neurovascular treatment and minimally invasive surgical procedures, used extensively in both clinical and research settings due to their precision, safety, and effectiveness in treating conditions such as strokes, aneurysms, and other neurovascular disorders

- The escalating demand for interventional neurology devices is primarily fueled by the growing prevalence of neurological disorders, rising adoption of minimally invasive procedures, and increasing investment in advanced healthcare infrastructure. Additionally, technological advancements in catheter systems, neurovascular stents, and imaging-guided devices are driving broader adoption across hospitals, specialized neurocenters, and research institutions

- North America dominated the interventional neurology devices market with the largest revenue share of 51.3% in 2024, driven by advanced healthcare infrastructure, high adoption of minimally invasive neurological procedures, and the strong presence of leading device manufacturers. The U.S. market witnessed substantial growth in interventional neurology device installations, supported by continuous technological innovations, increasing prevalence of neurological disorders, and strategic collaborations between hospitals and device providers

- Asia-Pacific is expected to be the fastest-growing region in the interventional neurology devices market during the forecast period, fueled by expanding healthcare infrastructure, increasing awareness of neurological disorders, rising disposable incomes, and growing adoption of minimally invasive neurointerventional procedures in countries such as China, India, and Japan

- The Ischemic Strokes segment dominated the interventional neurology devices market with a revenue share of 45.3% in 2024, owing to the high prevalence of stroke cases and the critical need for immediate intervention. Interventional devices for this pathology enable effective restoration of blood flow, reducing brain tissue damage and improving patient survival

Report Scope and Interventional Neurology Devices Market Segmentation

|

Attributes |

Interventional Neurology Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Interventional Neurology Devices Market Trends

Advancements in Precision and Minimally Invasive Neurovascular Procedures

- A significant and accelerating trend in the global interventional neurology devices market is the adoption of precision-guided and minimally invasive neurovascular treatment technologies. These innovations are enhancing procedural accuracy, reducing patient recovery time, and improving overall clinical outcome

- For instance, the development of advanced microcatheters, neurovascular stents, and embolic coils allows physicians to treat complex cerebral aneurysms, ischemic strokes, and arteriovenous malformations with greater safety and efficacy

- Imaging-guided systems, including high-resolution angiography and intraoperative navigation, are being increasingly integrated with interventional devices, enabling real-time monitoring of vascular structures and optimized device placement during procedures

- The trend toward minimally invasive approaches is fostering shorter hospital stays, reduced procedural risks, and enhanced patient comfort, which is driving adoption in both established hospitals and specialized neurovascular centers

- Key players in the market are focusing on continuous innovation in device design, material biocompatibility, and procedural workflow efficiency, ensuring that physicians have reliable and versatile tools for complex neurological interventions

- The increasing prevalence of neurovascular disorders, combined with rising awareness of advanced treatment options and improvements i healthcare infrastructure, is driving substantial growth in device adoption across both developed and emerging markets

- As interventional neurology procedures become more standardized and widely accepted, the market is witnessing robust demand from hospitals, outpatient neurocenters, and research institutions for devices that offer precision, safety, and procedural efficiency

Interventional Neurology Devices Market Dynamics

Driver

Growing Need Due to Increasing Neurovascular Disorders and Advanced Treatment Adoption

- The rising prevalence of neurovascular disorders such as ischemic stroke, cerebral aneurysms, and arteriovenous malformations, coupled with increasing awareness of minimally invasive treatment options, is a significant driver for the growing demand for Interventional Neurology Devices

- For instance, in April 2024, leading medical device companies announced innovations in next-generation microcatheters and neurovascular stents, enabling safer and more precise interventions in complex brain and spinal procedures. Such advancements are expected to fuel market growth in the forecast period

- Hospitals and specialized neurocenters are increasingly prioritizing devices that allow real-time monitoring, improved procedural accuracy, and optimized treatment outcomes, replacing older, more invasive techniques with safer, image-guided interventions

- The growing investment in preclinical research, hospital infrastructure, and training for interventional procedures is enhancing the adoption of advanced neurology devices. Institutions are seeking equipment that supports high-resolution imaging, automated navigation, and integrated workflow solutions to improve patient safety and clinical efficacy

- The trend toward minimally invasive procedures, combined with increasing demand for faster recovery times and reduced hospitalization, is boosting the uptake of precision-guided interventional devices across both established and emerging markets

Restraint/Challenge

Concerns Regarding High Initial Costs and Training Requirements

- The relatively high initial investment required for advanced interventional neurology devices can pose a significant barrier, particularly for smaller hospitals, regional clinics, and emerging-market healthcare providers. These high costs often include not only the devices themselves but also associated imaging systems, software, and maintenance contracts, which can strain limited budgets

- In addition, the adoption of these devices demands specialized training and skilled personnel to ensure safe and effective use. Hospitals or clinics lacking experienced interventional neurologists or trained technical staff may face difficulties in integrating these technologies into routine procedures, which can slow down adoption rates

- The complexity of certain procedures, combined with the need for continuous professional development, can further discourage smaller institutions from investing in high-end devices, limiting accessibility for patients in underserved regions

- To overcome these barriers, manufacturers and healthcare providers are exploring options such as structured training programs, simulation-based learning, flexible leasing or financing schemes, and simplified device models tailored for smaller setups

- Despite these challenges, the growing demand for minimally invasive neurovascular interventions, the push toward improved patient safety, and the expansion of healthcare infrastructure globally are expected to mitigate some of these restraints and continue driving the adoption of Interventional Neurology Devices over the forecast period

Interventional Neurology Devices Market Scope

The market is segmented on the basis of product type, disease pathology, procedure, and end user.

- By Product Type

On the basis of product type, the interventional neurology devices market is segmented into aneurysm coiling and embolization devices, cerebral balloon angioplasty and stenting systems, support devices, and neurothrombectomy devices. The aneurysm coiling and embolization devices segment dominated the market with a revenue share of 42.5% in 2024, due to the high prevalence of cerebral aneurysms and the growing preference for minimally invasive treatments. These devices provide precise aneurysm occlusion, reducing rupture risks and improving patient outcomes. Advancements in coil design and materials enhance treatment efficiency, while training programs and awareness campaigns drive adoption in hospitals and specialized neurology centers. The segment benefits from strong reimbursement policies and increasing patient awareness, reinforcing its leadership in the market.

The neurothrombectomy devices segment is expected to witness the fastest CAGR of 22.1% from 2025 to 2032, driven by the rising incidence of ischemic strokes worldwide. These devices enable mechanical clot removal, restoring cerebral blood flow and minimizing neurological damage. Innovations in catheter flexibility, aspiration systems, and real-time imaging guidance improve procedural success rates. Rapid hospital adoption, combined with increasing stroke awareness and early intervention protocols, supports the strong growth trajectory of this segment.

- By Disease Pathology

On the basis of disease pathology, the market is segmented into ischemic strokes, cerebral aneurysms, and arteriovenous malformation (AVM) and fistulas. The ischemic strokes segment dominated with a revenue share of 45.3% in 2024, owing to the high prevalence of stroke cases and the critical need for immediate intervention. Interventional devices for this pathology enable effective restoration of blood flow, reducing brain tissue damage and improving patient survival. The segment’s dominance is supported by increasing investment in stroke care infrastructure, advanced imaging for early detection, and government initiatives promoting rapid intervention programs. Hospitals and specialized stroke centers widely adopt these devices, further reinforcing their market leadership.

The cerebral aneurysms segment is expected to witness the fastest CAGR of 21.8% from 2025 to 2032, fueled by rising aneurysm detection rates due to improved neuroimaging techniques. Minimally invasive coiling and embolization procedures are preferred for safety and efficacy, driving device adoption. Continuous technological advancements, along with increasing awareness and screening programs, enhance treatment outcomes and encourage early intervention, contributing to rapid market growth.

- By Procedure

On the basis of procedure, the market is segmented into embolization, angioplasty, and neurothrombectomy. The embolization segment dominated with a revenue share of 43.7% in 2024, owing to its widespread application in treating aneurysms and AVMs. Embolization offers a minimally invasive approach, precise vessel occlusion, and lower complication rates compared with traditional surgical procedures. Hospitals and neurology centers prefer embolization for its efficiency and patient safety. Technological improvements in embolic materials and microcatheter designs further enhance treatment success, making it the leading procedural segment in the market.

The neurothrombectomy segment is expected to witness the fastest CAGR of 22.3% from 2025 to 2032, driven by increasing ischemic stroke cases and global recognition of mechanical clot retrieval as standard care. These procedures allow rapid reperfusion, reduce long-term disability, and improve patient outcomes. Device innovations, including aspiration catheters and stent retrievers, support higher procedural efficiency and safety. Growing awareness campaigns, hospital adoption, and reimbursement policies further contribute to the fast growth of this segment.

- By End User

On the basis of end user, the market is segmented into hospitals, neurology clinics, and ambulatory care centers. The Hospitals segment dominated the market with a revenue share of 49.1% in 2024, owing to advanced stroke care infrastructure, high patient volume, and availability of skilled interventional teams. Hospitals integrate imaging and procedural technologies for comprehensive treatment, enabling widespread use of interventional neurology devices. The segment’s dominance is reinforced by multi-specialty care coordination, increasing incidence of cerebrovascular diseases, and adoption of minimally invasive procedures. Funding, training programs, and technological advancements also contribute to strong hospital-based demand.

The neurology clinics segment is expected to witness the fastest CAGR of 20.7% from 2025 to 2032, due to the expansion of outpatient procedures and specialized cerebrovascular care. Clinics adopt compact, versatile devices for cost-effective treatments, allowing early intervention without hospitalization. Growing patient preference for outpatient care, technological advancements, and integration with imaging systems support rapid adoption. Clinics also benefit from high patient throughput and operational efficiency, driving the segment’s strong growth trajectory.

Interventional Neurology Devices Market Regional Analysis

- North America dominated the interventional neurology devices market with the largest revenue share of 51.3% in 2024, characterized by advanced healthcare and pharmaceutical R&D infrastructure, high disposable incomes, and a strong presence of key industry players

- The region benefits from cutting-edge neurointerventional research facilities, widespread adoption of innovative diagnostic and therapeutic technologies, and growing investments in minimally invasive procedures

- Hospitals, specialty clinics, and academic research centers in North America are increasingly deploying advanced devices for neurovascular interventions, contributing to substantial market growth

U.S. Interventional Neurology Devices Market Insight

The U.S. interventional neurology devices market captured the largest revenue share of 71% in 2024 within North America, fueled by the rapid adoption of high-resolution imaging systems, robotic-assisted interventions, and AI-enabled neurodiagnostic platforms. The country’s focus on improving patient outcomes, reducing procedural risks, and accelerating minimally invasive treatments has reinforced its leading position. Integration of multi-modal imaging, navigation systems, and automated monitoring platforms is further driving market expansion. These innovations allow clinicians to perform complex neurovascular procedures with higher precision, efficiency, and safety, making the U.S. a dominant player in the global market.

Europe Interventional Neurology Devices Market Insight

The Europe interventional neurology devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing investments in healthcare infrastructure, the rising prevalence of neurological disorders, and the adoption of minimally invasive neurointerventional procedures. Stringent regulatory frameworks in Europe, coupled with collaborations between academic research institutions and industry players, are facilitating the introduction of advanced interventional devices for the treatment of stroke, aneurysm, and other neurovascular conditions. Growing awareness among patients and healthcare providers regarding precision neurovascular care is further fueling market growth across the region.

U.K. Interventional Neurology Devices Market Insight

The U.K. interventional neurology devices market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing government initiatives aimed at improving neurological healthcare, rising investments in hospitals, and the adoption of advanced diagnostic and interventional devices. Rising prevalence of cerebrovascular diseases, coupled with growing demand for precise and minimally invasive neurovascular procedures, is driving market expansion. The U.K.’s robust healthcare infrastructure and focus on translational research in neurology further reinforce adoption of interventional neurology technologies.

Germany Interventional Neurology Devices Market Insight

The Germany interventional neurology devices market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare system, focus on clinical innovation, and growing awareness of advanced neurointerventional procedures. Integration of high-resolution imaging systems, robotic-assisted interventions, and real-time monitoring platforms is driving adoption in both academic hospitals and private clinics. Germany’s emphasis on precision, safety, and technological advancement ensures steady growth in the interventional neurology devices sector.

Asia-Pacific Interventional Neurology Devices Market Insight

The Asia-Pacific interventional neurology devices market is poised to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. Expansion of healthcare infrastructure, increasing number of specialized neurocenters, and government initiatives promoting accessibility to neurointerventional care are key growth factors. Furthermore, emerging economies in the region are increasingly investing in advanced devices and training programs for clinicians, boosting the adoption of interventional neurology solutions.

Japan Interventional Neurology Devices Market Insight

The Japan interventional neurology devices market is gaining momentum due to the country’s highly developed healthcare infrastructure, emphasis on precision neurovascular interventions, and high adoption of advanced imaging and robotic-assisted technologies. The aging population and rising prevalence of cerebrovascular diseases are fueling demand for minimally invasive and safer treatment options. Clinicians increasingly rely on high-throughput diagnostic platforms and automated monitoring systems, facilitating faster, more accurate neurointerventional procedures across hospitals and specialized neurocenters.

China Interventional Neurology Devices Market Insight

The China interventional neurology devices market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding middle class, rapid urbanization, and growing incidence of neurological disorders. Strong domestic manufacturing capabilities, government initiatives supporting neurovascular research, and establishment of state-of-the-art neurointerventional centers are driving adoption. Increasing healthcare expenditure, combined with enhanced access to advanced imaging and therapeutic platforms, is significantly propelling market growth in hospitals, specialty clinics, and research institutions across China.

Interventional Neurology Devices Market Share

The interventional neurology devices industry is primarily led by well-established companies, including:

- Johnson & Johnson and its affiliates (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Terumo Corporation (Japan)

- Penumbra, Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- Kaneka Corporation (Japan)

- Integer Holdings Corporation (France)

- Perflow Medical (U.S.)

- Phenox GmbH (Germany)

- Sensome (France)

- Evasc Medical Systems Corp. (Canada)

- Rapid Medical (Israel)

- ASAHI INTECC CO. LTD (Japan)

- Acandis GmbH (Germany)

- Medikit Co. Ltd (Japan)

- Imperative Care (U.S.)

- Lepu Medical Technology(Beijing)Co.,Ltd. (China)

- Stryker (U.S.)

Latest Developments in Global Interventional Neurology Devices Market

- In July 2025, Imperative Care, Inc. announced the FDA 510(k) clearance of its Zoom 7X catheter for aspiration thrombectomy. This device is designed to enhance the efficiency and safety of clot removal procedures in patients experiencing acute ischemic stroke. The Zoom 7X catheter's advanced aspiration capabilities aim to improve patient outcomes by enabling faster and more effective thrombectomy procedures

- In June 2025, Stryker unveiled its AXS Lift Intracranial Base Catheter, a novel device developed to simplify neurovascular access and enhance the delivery of interventional therapies. This catheter is designed to provide improved support and stability during procedures, potentially reducing complications and enhancing procedural success rates

- In May 2025, Route 92 Medical announced FDA 510(k) clearance for its HiPoint 88 reperfusion system, which includes the Tenzing 8 delivery catheter featuring the Monopoint approach. This system is intended for use in neurovascular procedures, offering a streamlined approach to clot retrieval and potentially improving patient outcomes in acute ischemic stroke cases

- In April 2025, Brainomix received FDA clearance for its Brainomix 360 Core Volume feature, enabling physicians to assess ischemic core volume from universally available noncontrast CT (NCCT) images. This AI-powered tool aims to enhance stroke imaging capabilities, allowing for more accurate assessments and informed decision-making in acute ischemic stroke management

- In March 2025, Inari Medical, now part of Stryker, launched its Artix thrombectomy system, purpose-built for the distinct needs of peripheral arterial procedures. This system is designed to provide effective clot retrieval in peripheral arteries, expanding the range of interventional neurology devices available for treating vascular occlusions outside the brain

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.