Global Inverted Pouches Market

Market Size in USD Billion

USD

14.16 Billion

USD

26.40 Billion

2024

2032

USD

14.16 Billion

USD

26.40 Billion

2024

2032

| 2025 - 2032 | |

| USD 14.16 Billion | |

| USD 26.40 Billion | |

| % | |

|

Inverted Pouches Market Size

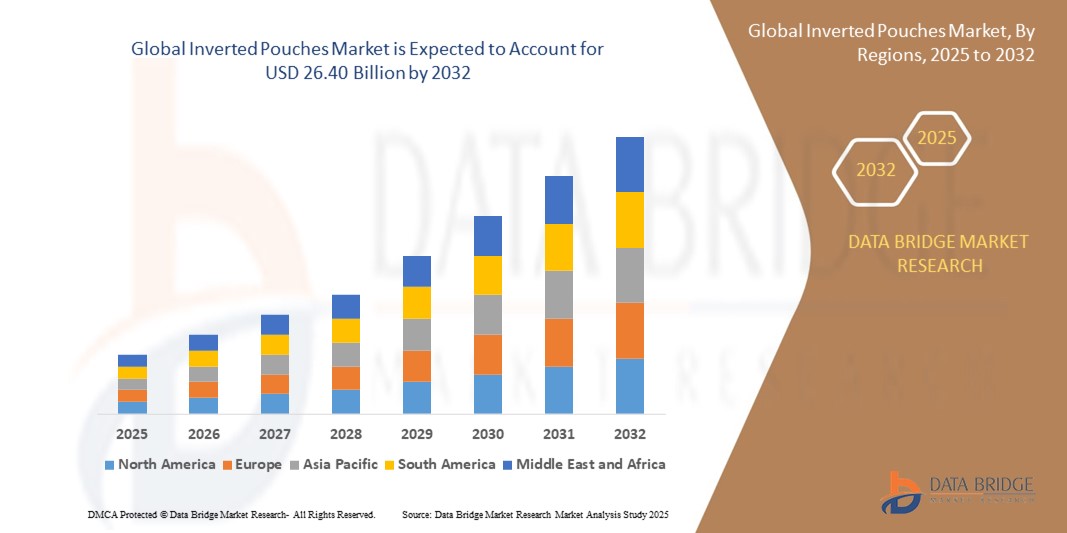

- The global inverted pouches market size was valued at USD 14.16 billion in 2024 and is expected to reach USD 26.40 billion by 2032, at a CAGR of 8.1% during the forecast period

- The market growth is largely fueled by the increasing demand for convenient, easy-to-use, and mess-free packaging solutions across food, personal care, and household product segments, leading to widespread adoption of inverted pouch formats by both global and regional brands

- Furthermore, rising consumer expectations for sustainable, resealable, and aesthetically appealing packaging, coupled with advancements in material science and filling technology, are driving manufacturers to adopt inverted pouches as a modern packaging alternative, thereby significantly boosting the industry's growth

Inverted Pouches Market Analysis

- Inverted pouches are flexible, self-standing packaging formats designed for easy dispensing of viscous or semi-liquid products such as sauces, shampoos, lotions, and cleaning gels. These pouches are engineered to reduce product waste, enhance shelf visibility, and improve user experience through one-handed operation and complete product evacuation

- The growing adoption of inverted pouches is primarily fueled by rising demand for lightweight, recyclable, and consumer-friendly packaging in fast-moving consumer goods (FMCG), expanding e-commerce penetration, and increasing brand focus on product differentiation and sustainability

- North America dominated the inverted pouches market with a share of 29.3% in 2024, due to the widespread demand for convenient, mess-free packaging solutions in food and personal care segments

- Asia-Pacific is expected to be the fastest growing region in the inverted pouches market during the forecast period due to increasing consumption of packaged food, personal care products, and rapid development of flexible packaging infrastructure

- Premade segment dominated the market with a market share of 58.9% in 2024, due to its convenience, reduced downtime in production, and consistent quality control during manufacturing. Premade pouches are especially favored by small and medium-sized brands that prioritize rapid product launches without investing heavily in automated filling lines. Their aesthetic appeal, print-friendly surfaces, and ability to support high-barrier laminates also make them a preferred choice for premium product packaging

Report Scope and Inverted Pouches Market Segmentation

|

Attributes |

Inverted Pouches Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Inverted Pouches Market Trends

“Growing Demand for user-Friendly Packaging”

- The inverted pouches market is gaining traction as consumers increasingly prefer packaging solutions that offer convenience, ease of use, and minimal product waste—especially for products that are viscous or difficult to dispense

- For instance, companies such as Glenroy Inc. and Liqui-Box have developed innovative inverted pouch solutions for condiments, nut butters, and honey, ensuring near-complete product evacuation and providing easy grip functionality for older adults and children

- The rise of on-the-go lifestyles and smaller households is fueling the demand for packaging that combines portability with efficient dispensing, making inverted pouches an attractive option in multiple consumer goods categories

- Sustainability is another growing trend, with inverted pouches using less plastic than rigid bottles or jars, helping brands lower their carbon footprint while maintaining premium functionality

- Brand differentiation is a key driver, as inverted pouches offer excellent shelf impact and allow for high-quality graphics and customization, enabling FMCG companies to enhance visibility and consumer engagement

- The surge in e-commerce has also contributed to the adoption of flexible, durable packaging such as inverted pouches, which provide spill resistance and reduced breakage during shipping compared to rigid packaging

Inverted Pouches Market Dynamics

Driver

“Increased Demand in Food and Beverage Sector”

- The food and beverage industry accounts for a significant share of inverted pouch adoption, driven by consumer preferences for clean, efficient dispensing of products such as sauces, spreads, yogurts, and beverages

- For instance, Kraft Heinz has introduced several product lines such as ketchup and mayonnaise in inverted pouch formats to improve product shelf life, minimize mess, and offer a premium consumer experience

- Health-conscious and environmentally aware consumers are driving food brands to adopt packaging that enhances hygiene, supports portion control, and offers better resealability—capabilities well-supported by inverted pouch design

- The growing trend of ready-to-use and premium food products has led manufacturers to choose inverted pouches to reinforce their product positioning while ensuring product freshness

- Expansion of private-label food brands across global retail channels is boosting demand for cost-efficient, high-impact packaging formats—creating opportunities for inverted pouch manufacturers to scale production

Restraint/Challenge

“High Production Costs of Inverted Pouches”

- Despite demand growth, the higher manufacturing and material costs associated with inverted pouches—due to multi-layer films, specialized closures, and custom filling lines—pose challenges for widespread adoption

- For instance, smaller brands and regional players struggle to adopt inverted pouches as leading companies such as AptarGroup and Glenroy benefit from economies of scale, leaving cost-sensitive businesses reliant on traditional packaging formats

- Upfront investment in new filling and sealing technology, staff training, and compatibility testing can be significant, especially for manufacturers transitioning from rigid or standard flexible packaging

- Raw material fluctuations and the need for strong barrier properties and recyclable laminates add to the cost burden, impacting overall price competitiveness in mass markets

- Cost constraints often limit the adoption of inverted pouches to premium product segments, potentially slowing market penetration in price-sensitive regions or among value brands

Inverted Pouches Market Scope

The market is segmented on the basis of pouch type, material type, capacity, and end use.

- By Pouch Type

On the basis of pouch type, the inverted pouches market is segmented into premade and form-fill-seal (FFS). The premade segment accounted for the largest market revenue share of 58.9% in 2024, owing to its convenience, reduced downtime in production, and consistent quality control during manufacturing. Premade pouches are especially favored by small and medium-sized brands that prioritize rapid product launches without investing heavily in automated filling lines. Their aesthetic appeal, print-friendly surfaces, and ability to support high-barrier laminates also make them a preferred choice for premium product packaging.

The FFS segment is projected to register the fastest growth rate from 2025 to 2032, driven by increased adoption among large-scale manufacturers aiming to reduce packaging costs through in-house filling operations. FFS systems offer greater flexibility in pouch customization and significantly higher throughput, making them ideal for high-volume product categories such as condiments and personal care items. The growing trend of automation and integrated production lines in the packaging industry is further propelling the adoption of FFS inverted pouches.

- By Material Type

On the basis of material type, the market is segmented into polyolefin, metalized aluminum, ethylene vinyl alcohol (EVOH), and others. Polyolefin dominated the market with the largest revenue share in 2024 due to its cost-effectiveness, high heat-seal strength, and recyclability. This material’s excellent moisture barrier and flexibility make it suitable for a wide range of food and non-food applications. Its compatibility with modern filling systems and ease of customization in pouch design have made polyolefin-based inverted pouches a market standard.

The EVOH segment is expected to grow at the highest CAGR from 2025 to 2032, fueled by rising demand for high-barrier materials that protect contents from oxygen and moisture. EVOH films are particularly critical for extending shelf life in food and personal care products, where product integrity is essential. As clean-label and preservative-free products gain traction, EVOH’s superior barrier properties are becoming increasingly valuable to manufacturers seeking to maintain product freshness without additives.

- By Capacity

On the basis of capacity, the market is segmented into below 150 ml, 150–500 ml, 500 ml–1 liter, and above 1 liter. The 150–500 ml segment captured the largest share of market revenue in 2024 due to its versatility across both food and personal care applications. This size range is highly favored for condiments, baby food, shampoos, and lotions, offering an optimal balance between portability and sufficient volume. Brands often choose this capacity to meet consumer preferences for single-use or short-term use products while maintaining attractive shelf presence.

The below 150 ml segment is expected to grow at the fastest rate from 2025 to 2032, driven by the rising popularity of trial-sized packaging and travel-friendly products. These smaller pouches are increasingly used in promotional kits, e-commerce sample distributions, and on-the-go consumption products. Their lightweight nature and reduced material use also appeal to sustainability-conscious consumers and brands aiming to lower their packaging footprint.

- By End Use

On the basis of end use, the market is segmented into food, personal care, and others. The food segment dominated the largest revenue share in 2024, propelled by the growing demand for convenient, squeezable, and spill-proof packaging formats. Inverted pouches have become increasingly popular for sauces, spreads, and baby foods, where easy dispensing and shelf stability are critical. Their extended shelf life, tamper-evidence, and user-friendly design make them ideal for modern consumers seeking convenience and hygiene in food packaging.

The personal care segment is anticipated to witness the fastest growth from 2025 to 2032, supported by the increasing adoption of inverted pouches for shampoos, body washes, creams, and other viscous formulations. Personal care brands are shifting toward flexible packaging to enhance product usability, minimize product waste, and improve sustainability. The ability to stand inverted and dispense contents completely has made these pouches a strategic solution for both consumer satisfaction and product differentiation in a competitive market.

Inverted Pouches Market Regional Analysis

- North America dominated the inverted pouches market with the largest revenue share of 29.3% in 2024, driven by the widespread demand for convenient, mess-free packaging solutions in food and personal care segments

- Manufacturers and consumers across the region prioritize user-friendly dispensing formats and extended shelf life, both of which are effectively addressed by inverted pouches

- High levels of packaged food consumption, established FMCG brands, and increasing emphasis on packaging innovation continue to drive adoption in both the U.S. and Canada

U.S. Inverted Pouches Market Insight

The U.S. inverted pouches market captured the largest revenue share in 2024 within North America, owing to strong demand from sauces, condiments, and baby food categories. The preference for easy-to-use, portable packaging that ensures product evacuation and reduces waste is a major factor contributing to adoption. The country’s advanced packaging industry, along with brand efforts toward premium and sustainable solutions, is accelerating the market. In addition, consumer expectations for convenience, coupled with a surge in e-commerce packaging innovations, is propelling growth.

Europe Inverted Pouches Market Insight

The Europe inverted pouches market is expected to grow at a significant CAGR during the forecast period, supported by rising environmental awareness and shifting consumer preferences toward sustainable, flexible packaging. The demand for hygienic, resealable, and easy-dispense formats is fueling interest across food, cosmetics, and household segments. Regulatory pressure on single-use plastics and emphasis on lightweight, recyclable alternatives are encouraging both brands and manufacturers to adopt inverted pouch solutions.

U.K. Inverted Pouches Market Insight

The U.K. inverted pouches market is projected to expand at a notable CAGR, driven by the rising popularity of eco-friendly packaging and growing consumer interest in on-the-go convenience products. Demand is surging across sauces, personal care products, and children’s food items. The country’s strong private label presence, retail innovations, and heightened focus on product shelf presence and consumer usability are key growth enablers.

Germany Inverted Pouches Market Insight

The Germany inverted pouches market is anticipated to grow steadily due to increasing demand for packaging formats that reduce product waste and enhance user experience. German consumers’ strong focus on hygiene, recycling, and product freshness is contributing to higher uptake in food and homecare applications. Moreover, the country’s advanced automation capabilities support high-volume adoption among both domestic and international brands.

Asia-Pacific Inverted Pouches Market Insight

The Asia-Pacific inverted pouches market is poised to grow at the fastest CAGR from 2025 to 2032, driven by increasing consumption of packaged food, personal care products, and rapid development of flexible packaging infrastructure. Countries such as China, India, and Japan are witnessing rising demand for convenient packaging formats due to urbanization, expanding middle-class population, and changing lifestyles. Cost-effective production and growing exports are also influencing market expansion.

Japan Inverted Pouches Market Insight

The Japan inverted pouches market is growing steadily, supported by the country's reputation for high packaging standards and demand for space-saving, functional formats. Consumers in Japan value packaging that enables full product use, preserves freshness, and fits well in compact storage spaces. The popularity of refillable packaging in personal care and home cleaning products is further enhancing the use of inverted pouch solutions.

China Inverted Pouches Market Insight

The China inverted pouches market held the largest revenue share within Asia-Pacific in 2024, driven by its massive packaged food industry, demand for modern retail packaging, and rapid adoption by domestic FMCG players. Inverted pouches are gaining traction across sauces, skincare, and detergent segments due to their affordability and ease of use. The push toward sustainable and value-added packaging by local manufacturers is strengthening the market's position across both urban and rural consumption channels.

Inverted Pouches Market Share

The inverted pouches industry is primarily led by well-established companies, including:

- Glenroy, Inc. (U.S.)

- VOLPAK S.A.U. (Spain)

- Perfect Packaging (India)

- Sonoco Products Company (U.S.)

- AptarGroup, Inc. (U.S.)

- Cheer Pack North America (U.S.)

- Viking Masek Global Packaging (U.S.)

- THIMONNIER (France)

- ProAmpac (U.S.)

- Polymer Packaging Inc. (U.S.)

Latest Developments in Global Inverted Pouches Market

- In November 2024, Mespack, a leading packaging machine supplier, and Amor, a packaging company, collaborated to develop a recyclable 2L stand-up bag specifically designed for household products such as laundry detergents, soaps, and cleansers. This innovation is expected to accelerate sustainable packaging adoption in the homecare segment, reinforcing the role of inverted pouches in reducing plastic waste while maintaining performance and user convenience

- In February 2024, Amcor, in partnership with Cheer Pack North America and Stonyfield Organic, introduced the first all-polyethylene (PE) spouted pouch. This first-to-market innovation marks a significant advancement in sustainable packaging, setting a benchmark for recyclability without compromising functionality. The collaboration demonstrates growing industry commitment to eco-friendly solutions, expected to influence broader adoption of recyclable inverted pouch formats across food and beverage sectors

- In January 2024, the API Group and Accredo Packaging, in collaboration with Fresh-Lock by Presto, announced efforts to launch a flexible stand-up pouch that integrates recycled content. This initiative highlights the importance of cross-industry partnerships in driving circular economy goals. By focusing on scalability across all consumer packaged goods categories, this development is poised to enhance the viability and appeal of inverted pouches made with post-consumer recycled materials

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Inverted Pouches Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Inverted Pouches Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Inverted Pouches Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.