Global Joint Disorders Market

Market Size in USD Billion

USD

12.15 Billion

USD

21.83 Billion

2025

2033

USD

12.15 Billion

USD

21.83 Billion

2025

2033

| 2026 - 2033 | |

| USD 12.15 Billion | |

| USD 21.83 Billion | |

| % | |

|

Joint Disorders Market Size

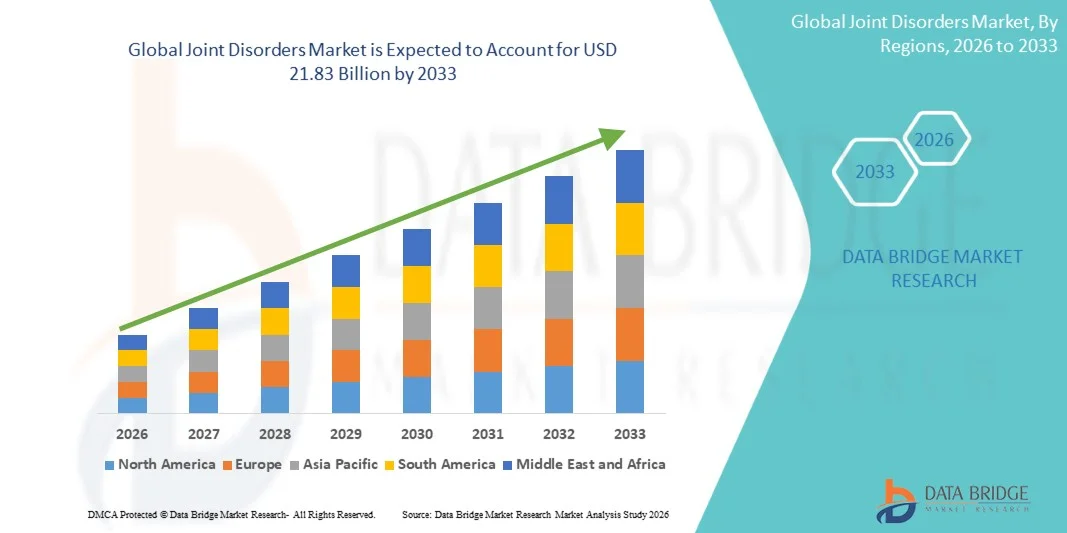

- The global joint disorders market size was valued at USD 12.15 billion in 2025 and is expected to reach USD 21.83 billion by 2033, at a CAGR of 7.6% during the forecast period

- The market growth is largely fueled by increasing incidence of joint‑related disorders worldwide, including degenerative conditions caused by aging, obesity, sedentary lifestyles, and sports injuries. Improved healthcare access and awareness about early treatment options are also expanding demand for both conservative and surgical interventions, contributing to sustained market expansion

- Furthermore, rising consumer and clinician demand for effective, less invasive, and personalized joint care solutions spanning medications, injections, supportive devices, and regenerative therapies is strengthening the joint disorders sector. These converging factors are accelerating the uptake of innovative treatments and management strategies, thereby significantly boosting overall industry growth

Joint Disorders Market Analysis

- Joint disorders, including conditions such as osteoarthritis, rheumatoid arthritis, spondylarthritis, juvenile idiopathic arthritis, lupus, gout, and bursitis, are increasingly driving demand for advanced diagnostics, therapeutic interventions, and surgical procedures in both residential and clinical healthcare settings due to their impact on mobility, quality of life, and long-term health outcomes

- The escalating demand for joint disorder management is primarily fueled by the rising prevalence of musculoskeletal conditions worldwide, an aging population, sedentary lifestyles, and growing awareness among patients and healthcare providers about early diagnosis and effective treatment options

- North America dominated the joint disorders market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high adoption of diagnostic tools such as MRI, X-ray, and DEXA scans, and a strong presence of key market players. The U.S. experienced substantial growth in medication, therapy, and surgical interventions, driven by innovations in biologics, minimally invasive procedures, and personalized treatment solutions

- Asia-Pacific is expected to be the fastest-growing region in the joint disorders market during the forecast period due to increasing healthcare access, rising geriatric population, growing prevalence of obesity and joint-related conditions, and expanding adoption of advanced diagnostics and treatment modalities

- The medication segment dominated the treatment market in 2025 with a market share of 45.3%, driven by its effectiveness in managing pain, inflammation, and disease progression, while physical examination, MRI, and X-ray remained the leading diagnostic methods due to their reliability in assessing joint damage and monitoring therapy outcomes

Report Scope and Joint Disorders Market Segmentation

|

Attributes |

Joint Disorders Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Joint Disorders Market Trends

“Advancements in Regenerative and Biologic Therapies”

- A significant and accelerating trend in the global joint disorders market is the increasing adoption of regenerative medicine and biologic therapies, including stem cell treatments and platelet-rich plasma (PRP) injections, which aim to repair damaged joint tissue and slow disease progression

- For instance, Regenexx’s PRP therapy is increasingly used for osteoarthritis patients to reduce inflammation and promote cartilage repair, offering an alternative to conventional surgical interventions

- These therapies provide targeted treatment options that can improve mobility, reduce pain, and minimize recovery time, while offering patients a more personalized and less invasive approach to joint care

- Integration of biologics with conventional treatment plans allows clinicians to optimize patient outcomes, combining medication, physical therapy, and regenerative procedures in a holistic care model

- This trend towards biologic and regenerative therapies is reshaping patient and clinician expectations, with companies such as Orthofix developing cell-based therapies and delivery systems that enhance efficacy and convenience

- The demand for regenerative and biologic solutions is growing rapidly across both developed and emerging markets, driven by patient preference for minimally invasive procedures and long-term joint health benefits

- Artificial intelligence and predictive analytics are increasingly applied in treatment planning to forecast disease progression and personalize patient care, further enhancing market adoption

Joint Disorders Market Dynamics

Driver

“Rising Prevalence of Musculoskeletal Disorders and Aging Population”

- The increasing incidence of osteoarthritis, rheumatoid arthritis, and other musculoskeletal conditions, combined with a growing aging population, is a key driver for the heightened demand for joint disorder treatments

- For instance, in 2024, Zimmer Biomet reported increased uptake of joint replacement procedures among elderly patients, reflecting the growing demand for effective interventions in aging populations

- As patients seek relief from chronic pain and improved mobility, advanced medications, therapies, and surgical procedures are becoming essential for managing joint disorders effectively

- Furthermore, rising awareness among patients and healthcare providers regarding early diagnosis and preventive care is encouraging timely interventions, reducing disease progression and long-term complications

- The convenience of combining medical, therapeutic, and surgical treatments, alongside improved access to healthcare services, is propelling adoption across both urban and rural patient populations

- The trend towards integrated joint care models and personalized treatment solutions is strengthening the market, with clinics and hospitals offering multidisciplinary approaches for optimal patient outcomes

- Government initiatives and insurance coverage expansions in developed regions are supporting increased patient access to costly treatments, further driving market growth

- Technological advancements in minimally invasive surgery and robotic-assisted procedures are improving treatment outcomes and reducing recovery time, increasing patient acceptance of surgical interventions

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Regions”

- The high cost of advanced medications, biologics, and surgical procedures poses a significant challenge to widespread market adoption, particularly in developing countries and price-sensitive populations

- For instance, the cost of total knee replacement surgery in emerging markets can be several times higher than the average annual income, limiting patient access to essential care

- Limited availability of specialized healthcare professionals and advanced diagnostic equipment in some regions further restricts timely and effective treatment for joint disorders

- Patients in rural or underserved areas may face delays in receiving proper care due to lack of infrastructure, which can worsen disease progression and reduce treatment efficacy

- While some lower-cost medications and therapy options are available, the gap in access to high-quality, advanced treatments continues to restrain market growth

- Addressing these challenges through healthcare policy support, patient education, and expansion of affordable treatment options will be crucial for sustained market development

- Regulatory hurdles and stringent approval processes for biologics and novel therapies can delay product launches, limiting the availability of advanced treatment solutions

- Patient adherence challenges, including long-term therapy regimens and lifestyle modifications, may affect treatment effectiveness and overall market adoption

Joint Disorders Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the joint disorders market is segmented into osteoarthritis, rheumatoid arthritis, spondylarthritis, juvenile idiopathic arthritis, lupus, gout, bursitis, and others. The osteoarthritis segment dominated the market with the largest revenue share of 32% in 2025, driven by its high prevalence among aging populations and increasing incidence due to obesity and sedentary lifestyles. Patients often prioritize early intervention through medications, therapy, and surgical procedures, making osteoarthritis the largest contributor to overall market revenue. Advanced treatment options, including joint replacement and regenerative therapies, are widely adopted in this segment, further supporting market dominance. The segment also benefits from awareness programs and healthcare campaigns focused on osteoarthritis management. In addition, the growing number of clinical trials targeting osteoarthritis therapeutics is enhancing treatment adoption and patient outcomes. The segment’s high incidence across both developed and emerging regions contributes significantly to market growth.

The rheumatoid arthritis segment is anticipated to witness the fastest growth at a CAGR of 8% from 2026 to 2033, fueled by increasing awareness of autoimmune disorders and rising adoption of biologics and targeted therapies. Rheumatoid arthritis requires long-term management and multidisciplinary care, which drives demand for innovative treatments and monitoring solutions. Early diagnosis using imaging and biomarker testing enhances treatment efficacy, supporting growth in this segment. The segment also benefits from rising insurance coverage and government initiatives promoting access to specialty care. Patients’ growing preference for minimally invasive interventions and therapy combinations contributes to the expanding market. Advances in personalized medicine and AI-assisted disease monitoring further accelerate adoption in this segment.

- By Diagnosis

On the basis of diagnosis, the market is segmented into physical examination, X-ray, MRI, ultrasound, blood test, DEXA scan, and others. The MRI segment dominated the market with the largest share of 22% in 2025, owing to its superior ability to visualize soft tissue, cartilage, and joint inflammation. MRI is considered the gold standard for diagnosing complex joint conditions, allowing clinicians to assess disease progression accurately. Patients and healthcare providers rely on MRI to guide treatment decisions, from conservative therapy to surgical intervention. The segment’s dominance is supported by increasing availability of advanced MRI machines and rising awareness among orthopedic specialists. MRI diagnostics also facilitate early detection of joint disorders, which improves outcomes and reduces long-term costs. High adoption in hospitals and specialty clinics further strengthens the segment’s market position.

The ultrasound segment is expected to witness the fastest growth from 2026 to 2033, due to its cost-effectiveness, portability, and ability to provide real-time imaging for joint assessment. Ultrasound is increasingly used in point-of-care settings for detecting synovial inflammation and guiding injections. Its non-invasive nature and safety profile support frequent monitoring, appealing to both patients and physicians. The segment benefits from technological innovations such as high-resolution probes and AI-assisted image analysis. Growing adoption in specialty clinics and smaller healthcare facilities also fuels growth. Ultrasound allows dynamic assessment of joint movement, providing additional clinical insights. Rising preference for bedside diagnostics in emerging regions further supports its expanding market share.

- By Treatment

On the basis of treatment, the market is segmented into medication, therapy, surgery, and others. The medication segment dominated the market with a 45.3% share in 2025, driven by widespread use of NSAIDs, DMARDs, biologics, and corticosteroids for managing pain and inflammation. Medications provide non-invasive and cost-effective solutions for patients, often as first-line therapy. High prevalence of chronic joint disorders such as osteoarthritis and rheumatoid arthritis ensures steady demand. The segment also benefits from continuous development of targeted therapies and biologics, enhancing efficacy and safety profiles. Increasing awareness and accessibility of pharmaceutical treatments in hospitals and retail pharmacies support market dominance. Patients’ preference for oral medications contributes to widespread adoption across demographics.

The surgery segment is anticipated to witness the fastest growth from 2026 to 2033, due to rising adoption of joint replacement procedures and minimally invasive surgical techniques. Technological innovations such as robotic-assisted surgeries and enhanced recovery protocols are improving patient outcomes and reducing hospital stays. Surgery is often required when conservative treatments fail, driving demand for advanced interventions. Increasing geriatric population and higher incidence of severe joint degeneration further propel growth. Governments and private insurers expanding coverage for surgical procedures support segment adoption. Rising awareness about post-operative physiotherapy and rehabilitation enhances long-term treatment efficacy.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, topical, and others. The oral segment dominated the market with a share of 55% in 2025, largely due to the convenience, cost-effectiveness, and patient preference for tablets, capsules, and oral supplements. Oral medications are widely used for pain management, disease-modifying therapy, and anti-inflammatory treatment. Patients can self-administer medications at home, reducing hospital visits and healthcare costs. High prescription rates and availability across hospital and retail pharmacies contribute to market dominance. The segment also benefits from continuous development of sustained-release and combination formulations. Oral administration remains a primary choice across chronic joint disorders.

The parenteral segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing use of biologics, corticosteroids, and injectable regenerative therapies. Parenteral administration allows targeted delivery of medications directly into joints, enhancing efficacy and reducing systemic side effects. The segment benefits from technological advancements in injection devices and precision delivery systems. Adoption in specialty clinics and hospitals is rising, especially for rheumatoid arthritis and advanced osteoarthritis cases. Patients’ growing trust in injectable therapies due to improved safety and outcomes fuels growth. Expansion of biologic therapy approvals and reimbursement policies further supports market adoption.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialty clinics, and others. The hospitals segment dominated with a 50% share in 2025, driven by advanced diagnostic facilities, surgical infrastructure, and comprehensive treatment capabilities. Hospitals provide multidisciplinary care combining medication, therapy, and surgery, meeting diverse patient needs. High patient inflow and established referral systems enhance hospital dominance. Availability of specialized orthopedic departments and trained healthcare professionals supports treatment delivery. Hospitals also drive adoption of advanced imaging and regenerative therapies. Government and private hospital expansion initiatives contribute to sustained market growth.

The specialty clinics segment is anticipated to witness the fastest growth from 2026 to 2033, due to rising outpatient care services, focused physiotherapy, and personalized joint care programs. Specialty clinics offer tailored treatments for rheumatoid arthritis, osteoarthritis, and other joint disorders. Patients prefer clinics for convenience, reduced waiting times, and specialized attention. Technological adoption, including telemedicine and AI-assisted diagnostics, accelerates growth in this segment. Clinics also provide targeted therapy plans combining medications and physiotherapy. Expansion of clinics in urban and semi-urban areas is further propelling adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated with a 48% share in 2025, supported by direct access to prescribed medications and integration with inpatient and outpatient care. Hospital pharmacies facilitate timely dispensing of advanced biologics, corticosteroids, and post-operative medications. Integration with hospital systems ensures proper treatment adherence and monitoring. Strong linkages with healthcare providers enhance reliability and patient trust. Availability of high-value medications through hospital pharmacies drives market dominance. Hospitals’ role in post-surgical care further reinforces this segment.

The retail pharmacy segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing self-medication, OTC drug availability, and ease of access to pain relief and joint health supplements. Retail pharmacies cater to patients preferring home-based therapy and regular monitoring. Expansion of pharmacy chains and online delivery services is accelerating adoption. Rising consumer awareness and availability of prescription refill services further drive growth. Retail channels also provide convenient access to supplements, topical treatments, and oral medications. Technological integration, including e-prescriptions and app-based delivery, enhances convenience for end-users.

Joint Disorders Market Regional Analysis

- North America dominated the joint disorders market with the largest revenue share of 39.8% in 2025, characterized by advanced healthcare infrastructure, high adoption of diagnostic tools such as MRI, X-ray, and DEXA scans, and a strong presence of key market players

- Patients and healthcare providers in the region highly value the availability of comprehensive joint care, including medications, biologics, physical therapy, and advanced surgical procedures such as minimally invasive and robotic-assisted joint replacements

- This widespread adoption is further supported by high healthcare spending, strong insurance coverage, and a technologically advanced medical ecosystem, establishing North America as a key region for both chronic joint disorder management and innovative treatment adoption

U.S. Joint Disorders Market Insight

The U.S. joint disorders market captured the largest revenue share of 42% in 2025 within North America, fueled by the high prevalence of osteoarthritis and rheumatoid arthritis, combined with advanced healthcare infrastructure. Patients are increasingly prioritizing access to innovative treatments, including biologics, regenerative therapies, and minimally invasive surgeries. The growing preference for outpatient care, home-based physiotherapy, and early intervention programs further propels the market. Moreover, rising awareness about preventive care and the integration of digital health platforms for monitoring joint health is significantly contributing to market expansion.

Europe Joint Disorders Market Insight

The Europe joint disorders market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by an aging population, rising prevalence of chronic joint diseases, and increasing adoption of advanced diagnostics and therapies. The growth of specialty clinics and physiotherapy centers, combined with strict healthcare regulations promoting early intervention, is fostering market adoption. European patients are also drawn to personalized treatment plans and multidisciplinary care. The region is experiencing significant growth across hospitals, specialty clinics, and outpatient care facilities, with advanced joint care solutions being incorporated into both preventive programs and surgical interventions.

U.K. Joint Disorders Market Insight

The U.K. joint disorders market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of musculoskeletal disorders and demand for high-quality treatment options. In addition, rising awareness of early diagnosis, preventive care, and therapy adherence is encouraging patients and healthcare providers to adopt comprehensive joint care solutions. The U.K.’s strong healthcare infrastructure and widespread access to advanced medications, imaging modalities, and surgical procedures are expected to continue stimulating market growth. Public campaigns on arthritis management and expanding insurance coverage further support adoption in both residential and clinical settings.

Germany Joint Disorders Market Insight

The Germany joint disorders market is expected to expand at a considerable CAGR during the forecast period, fueled by high healthcare expenditure, technological advancements in surgical and diagnostic tools, and patient awareness regarding chronic joint conditions. Germany’s well-developed hospital network, emphasis on innovation, and availability of advanced therapies promote adoption of joint disorder treatments. The integration of digital health monitoring and minimally invasive procedures is becoming increasingly prevalent, with patients seeking effective, privacy-focused, and long-term solutions. Government initiatives supporting geriatric care and musculoskeletal health further contribute to growth.

Asia-Pacific Joint Disorders Market Insight

The Asia-Pacific joint disorders market is poised to grow at the fastest CAGR of 9.5% from 2026 to 2033, driven by rising geriatric populations, increasing incidence of obesity-related joint conditions, and growing healthcare infrastructure in countries such as China, Japan, and India. The region’s increasing awareness of early diagnosis and preventive care, supported by government initiatives, is driving the adoption of joint disorder treatments. Furthermore, the expansion of specialty clinics, affordable therapeutic options, and greater access to surgical procedures are enabling more patients to seek care, increasing the overall market reach.

Japan Joint Disorders Market Insight

The Japan joint disorders market is gaining momentum due to the country’s rapidly aging population, high prevalence of osteoarthritis, and strong healthcare system. Adoption is driven by advanced surgical procedures, regenerative therapies, and widespread access to imaging and diagnostics. Integration of digital health platforms and telemedicine solutions for monitoring joint conditions is further fueling growth. Patients are increasingly seeking minimally invasive and personalized care options, boosting demand across hospitals, clinics, and outpatient centers. Public awareness campaigns and insurance coverage for advanced therapies support the market’s expansion.

India Joint Disorders Market Insight

The India joint disorders market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising geriatric population, and increasing awareness of musculoskeletal health. India has witnessed significant growth in specialty clinics, physiotherapy centers, and hospital-based joint care services. Affordable treatment options, availability of generic medications, and growing adoption of minimally invasive procedures are key factors driving market growth. Furthermore, government initiatives promoting preventive care, combined with increasing private sector healthcare investments, are expanding access to joint disorder treatments in both urban and semi-urban regions.

Joint Disorders Market Share

The Joint Disorders industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Novartis AG (Switzerland)

- Amgen Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Ferring B.V. (Netherlands)

- Zimmer Biomet (U.S.)

- Stryker (U.S.)

- Anika Therapeutics, Inc. (U.S.)

- Bioventus LLC (U.S.)

- Flexion Therapeutics, Inc. (U.S.)

- Seikagaku Corporation (Japan)

- Smith & Nephew (U.K.)

- Fidia Farmaceutici S.p.A. (Italy)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

What are the Recent Developments in Global Joint Disorders Market?

- In October 2025, AbbVie announced that its newer arthritis drug Rinvoq (upadacitinib) demonstrated superior efficacy compared with Humira (adalimumab) in a head‑to‑head study involving rheumatoid arthritis patients who had failed prior TNF inhibitor therapy, with significantly higher remission and disease‑activity reduction rates, strengthening evidence for Rinvoq’s clinical advantage

- In September 2025 (published research), scientists highlighted key molecular and inflammatory pathways (NF‑κB signaling, MMPs and ADAMTS) involved in cartilage degradation and angiogenesis in osteoarthritis, providing insights into future disease‑modifying drug targets that could shift the therapeutic landscape beyond symptomatic relief

- In August 2025, the U.S. Food and Drug Administration approved the first‑ever vagus nerve stimulation implant (Setpoint System) for adults with moderate‑to‑severe rheumatoid arthritis, offering a novel neuroimmune approach that significantly reduced joint swelling and tenderness in clinical study participants, representing a landmark non‑drug treatment option

- In June 2024, Sanofi announced that the interleukin‑6 receptor blocker Kevzara received FDA approval for the treatment of active polyarticular juvenile idiopathic arthritis (pJIA) and is already approved in multiple countries for rheumatoid arthritis, expanding therapeutic options for chronic autoimmune joint inflammation in both adults and children

- In December 2021, major research reviews documented significant advancements in biologic DMARDs and targeted small‑molecule therapies that improved remission rates and significantly reduced joint damage and disability in rheumatoid arthritis, laying the foundation for next‑generation treatment strategies still evolving in current pipelines

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.