Global Karyotyping Market

Market Size in USD Million

USD

350.92 Million

USD

555.11 Million

2024

2032

USD

350.92 Million

USD

555.11 Million

2024

2032

| 2025 - 2032 | |

| USD 350.92 Million | |

| USD 555.11 Million | |

| % | |

|

Karyotyping Market Size

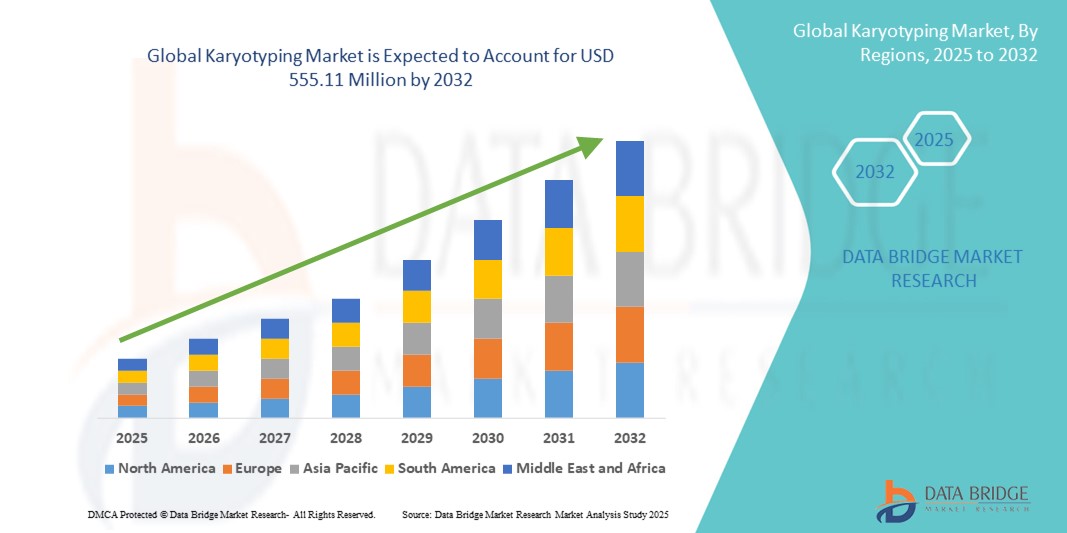

- The global karyotyping market size was valued at USD 350.92 million in 2024 and is expected to reach USD 555.11 million by 2032, at a CAGR of 5.9% during the forecast period

- The market growth is largely fueled by increasing prevalence of genetic disorders and rising demand for prenatal and cancer diagnostics, leading to higher adoption of advanced chromosomal analysis techniques

- Furthermore, technological advancements such as integration of AI and machine learning in karyotyping, along with rising awareness of non-invasive prenatal testing, are establishing karyotyping as a crucial tool in modern genetic diagnostics. These converging factors are accelerating the uptake of karyotyping solutions, thereby significantly boosting the industry's growth

Karyotyping Market Analysis

- Karyotyping, the laboratory technique used to examine chromosomes for abnormalities, is increasingly vital in modern genetic diagnostics across both clinical and research settings due to its ability to detect structural and numerical chromosomal variations associated with various genetic disorders and cancers

- The escalating demand for karyotyping is primarily fueled by the rising prevalence of genetic disorders, increasing adoption of personalized medicine, and a growing emphasis on early disease detection, particularly in prenatal and oncology diagnostics

- North America dominated the karyotyping market with the largest revenue share of 35.5% in 2024, characterized by advanced healthcare infrastructure, high adoption rates of genetic testing technologies, and substantial funding for genetic research. The U.S. experienced significant growth in karyotyping services, particularly in prenatal and cancer diagnostics, driven by innovations from both established tech companies and startups focusing on AI and machine learning applications in genetic analysis

- Asia-Pacific is expected to be the fastest-growing region in the karyotyping market, attributed to increasing healthcare investments, rising prevalence of genetic disorders, and growing awareness of advanced diagnostic techniques

- Consumables and accessories dominated the karyotyping market with a market share of 45.5% in 2024, driven by their essential role in routine karyotyping procedures and the increasing demand for high-quality reagents and kits in genetic testing

Report Scope and Karyotyping Market Segmentation

|

Attributes |

Karyotyping Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Karyotyping Market Trends

Advancements in AI and Automation for Enhanced Chromosomal Analysis

- A significant and accelerating trend in the global karyotyping market is the integration of artificial intelligence (AI) and automation technologies to enhance the accuracy and efficiency of chromosomal analysis. This fusion of technologies is significantly improving diagnostic capabilities and reducing turnaround times

- For instance, AI-powered models, such as Topological Vision Transformers (TopViTs), have demonstrated over 99% accuracy in detecting chromosomal aberrations, even in "few-shot" learning scenarios. These advancements enable high-quality performance in identifying structural and numerical chromosomal variations associated with various genetic disorders and cancers

- Automation in karyotyping processes allows for faster and more reproducible results, facilitating large-scale screenings and reducing human error. This trend towards more intelligent, intuitive, and interconnected diagnostic systems is fundamentally reshaping expectations for genetic diagnostics

- Consequently, companies are developing AI-enabled karyotyping solutions with features such as automated chromosomal analysis, integration with electronic health records (EHR), and decision support systems, aiming to streamline workflows and enhance diagnostic accuracy

- The demand for karyotyping services that offer seamless AI and automation integration is growing rapidly across both clinical and research settings, as healthcare providers increasingly prioritize efficiency and comprehensive diagnostic capabilities

Karyotyping Market Dynamics

Driver

Rising Demand for Genetic Testing in Prenatal and Cancer Diagnostics

- The increasing prevalence of genetic disorders and cancers, coupled with the growing emphasis on early disease detection, is a significant driver for the heightened demand for karyotyping services

- For instance, in 2024, hospitals and genetic testing laboratories expanded their karyotyping programs to improve prenatal screening outcomes, particularly for chromosomal abnormalities such as Down syndrome and Turner syndrome

- As healthcare providers become more aware of the benefits of genetic testing, karyotyping offers advanced features such as chromosomal analysis, structural variation detection, and numerical variation identification, providing a compelling upgrade over traditional diagnostic methods

- Furthermore, the growing popularity of personalized medicine and the desire for accurate and early diagnosis are making karyotyping an integral component of these systems, offering detailed insights into genetic health

- The convenience of comprehensive chromosomal analysis, early detection of genetic disorders, and the ability to inform treatment decisions are key factors propelling the adoption of karyotyping services in both clinical and research sectors

Restraint/Challenge

High Costs and Limited Accessibility in Emerging Markets

- The relatively high cost of karyotyping services, compared to traditional diagnostic methods, poses a significant challenge to broader market penetration, especially in emerging markets with limited healthcare budgets

- For instance, several clinics in developing countries have delayed implementing advanced karyotyping due to infrastructure costs and the need for trained specialists

- Addressing these cost concerns through the development of affordable karyotyping solutions and offering scalable testing options is crucial for expanding access to genetic diagnostics in underserved regions

- Additionally, the complexity of karyotyping procedures requires specialized training and expertise, which may not be readily available in all healthcare settings, further limiting accessibility

- Overcoming these challenges through cost-effective solutions, training programs, and infrastructure development will be vital for sustained growth and equitable access to karyotyping services

Karyotyping Market Scope

The market is segmented on the basis of product, type, application, end user, and distribution channel.

- By Product

On the basis of product, the karyotyping market is segmented into instruments, software & services, and consumables & accessories. Consumables & Accessories segment dominated the market with the largest revenue share of 45.5% in 2024, driven by the essential role of reagents, staining kits, and slides in routine karyotyping procedures. Laboratories and diagnostic centers prioritize high-quality consumables to ensure accurate chromosomal analysis, particularly in prenatal and cancer diagnostics. The consistent demand for consumables is reinforced by recurring usage in testing, making this segment a stable revenue contributor. Consumables also benefit from increasing automation in karyotyping workflows, which requires standardized kits for consistent results. Additionally, the growing number of research and clinical laboratories globally supports strong demand for consumables and accessories. Availability of ready-to-use kits and enhanced accuracy of reagents further boosts adoption in both clinical and academic settings.

Software & services segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising adoption of AI-driven analysis, digital imaging, and automated chromosomal interpretation tools. Software solutions help laboratories streamline workflow, improve accuracy, and reduce manual error in karyotype analysis. Services such as outsourced chromosomal analysis and consulting are gaining traction in research institutes and hospitals with limited in-house expertise. Cloud-based solutions allow for remote analysis, collaboration, and integration with electronic health records, expanding the market reach. The rising focus on personalized medicine and genetic diagnostics drives demand for advanced software and service solutions. Enhanced software capabilities such as pattern recognition, anomaly detection, and reporting automation contribute to the fast growth trajectory.

- By Type

On the basis of type, the karyotyping market is segmented into spectral karyotyping and virtual karyotyping. Spectral Karyotyping dominated the market with the largest share in 2024, owing to its ability to provide detailed visualization of chromosomal abnormalities using multicolor probes. This type is widely used in cancer diagnostics and research laboratories for identifying structural variations and translocations. The robustness, precision, and reproducibility of spectral karyotyping make it the preferred choice in high-end clinical and research applications. Laboratories rely on spectral karyotyping for accurate detection of complex chromosomal rearrangements. Its established presence in clinical workflows and the availability of comprehensive kits and protocols reinforce its dominance. Ongoing R&D and familiarity among cytogeneticists further support its leading market position.

Virtual Karyotyping is expected to witness the fastest growth during the forecast period, driven by increasing adoption of high-throughput genomic and bioinformatics approaches. Virtual karyotyping enables in silico analysis using DNA microarrays and next-generation sequencing, reducing the need for labor-intensive microscopy. The technique offers rapid and cost-effective detection of chromosomal imbalances, making it attractive for large-scale screening programs. Academic and research institutes prefer virtual karyotyping for studies requiring genome-wide analysis. Its integration with AI and machine learning platforms enhances predictive analysis, boosting its adoption. The growing demand for non-invasive and high-resolution diagnostics contributes to the accelerated growth of virtual karyotyping.

- By Application

On the basis of application, the karyotyping market is segmented into diagnosis, personalized medicines, research, and others. Diagnosis dominated the market with the largest revenue share in 2024, driven by its critical role in identifying chromosomal abnormalities in prenatal, oncology, and rare genetic disorder testing. Diagnostic applications ensure early detection and intervention, improving patient outcomes. Clinical laboratories and hospitals rely on karyotyping for accurate diagnosis of aneuploidy and structural chromosomal defects. The increasing prevalence of genetic disorders globally reinforces consistent demand in diagnostic settings. Standardization of protocols and availability of advanced diagnostic kits further strengthen this segment. Collaboration between hospitals and specialized diagnostic labs ensures wide accessibility of karyotyping services.

Research is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by increasing investments in genomics, cancer research, and personalized medicine initiatives. Research applications leverage karyotyping for understanding disease mechanisms, identifying novel targets, and validating therapeutic approaches. The integration of virtual karyotyping and AI-assisted tools accelerates research productivity and data analysis. Academic and pharmaceutical research institutes are expanding their cytogenetics capabilities to explore genetic variation and chromosomal instability. Funding support from government and private agencies drives new research projects requiring karyotyping. Growing collaborations between biotech firms and academic centers create additional demand for research-focused karyotyping services.

- By End User

On the basis of end user, the karyotyping market is segmented into clinical & research laboratories, hospitals, pathology laboratories, pharmaceutical & biotechnology companies, academic research institutes, and others. Clinical & Research Laboratories dominated the market with the largest share in 2024, attributed to their core focus on chromosomal testing, prenatal screening, and oncology diagnostics. These labs are equipped with state-of-the-art instruments, consumables, and software, enabling high-volume testing and consistent quality. Frequent demand from hospitals and research projects sustains market leadership. Laboratory personnel rely on both spectral and virtual karyotyping techniques to meet diverse diagnostic and research needs. The presence of skilled cytogeneticists and trained staff ensures accurate interpretation of results. Ongoing expansion of lab networks globally further solidifies the dominance of this end-user segment.

Hospitals are expected to witness the fastest growth during the forecast period, driven by increasing adoption of in-house genetic testing for prenatal, oncology, and personalized medicine applications. Hospitals aim to provide comprehensive care, reducing the need to outsource karyotyping tests. Integration of karyotyping results into patient records supports clinical decision-making and personalized treatment plans. Rising awareness among clinicians about the utility of genetic testing drives adoption. Advanced hospital laboratories are increasingly incorporating AI-assisted karyotyping for faster turnaround. Expansion of hospital networks in emerging markets further accelerates this segment's growth.

- By Distribution Channel

On the basis of distribution channel, the karyotyping market is segmented into direct tender, retail sales, and others. Direct Tender dominated the market with the largest share in 2024, driven by institutional procurement by hospitals, government laboratories, and large diagnostic centers. Bulk purchases of instruments, consumables, and software through tenders ensure cost efficiency and reliable supply. Direct tender agreements often include long-term maintenance and training services, enhancing adoption. Healthcare institutions prefer direct sourcing to ensure quality and authenticity of karyotyping products. Established vendors maintain strong relationships with end users to secure recurring contracts. Centralized procurement systems in major healthcare facilities further support dominance of this channel.

Retail Sales is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing availability of karyotyping kits and instruments through distributors and e-commerce platforms for smaller labs and academic research institutes. Retail channels provide flexibility, faster delivery, and accessibility to a wider customer base. Rising demand from emerging markets, where direct tenders may be limited, drives retail growth. Companies are expanding their distribution networks to cater to localized labs and institutions. The convenience of online procurement, bundled kits, and smaller volume packages enhances adoption through retail channels.

Karyotyping Market Regional Analysis

- North America dominated the karyotyping market with the largest revenue share of 35.5% in 2024, characterized by advanced healthcare infrastructure, high adoption rates of genetic testing technologies, and substantial funding for genetic research

- Healthcare providers and research institutions in the region highly value the accuracy, reproducibility, and comprehensive chromosomal analysis offered by karyotyping solutions for prenatal, oncology, and genetic disorder diagnostics

- This widespread adoption is further supported by the presence of well-established clinical and research laboratories, a skilled workforce of cytogeneticists, and the availability of advanced instruments and AI-enabled software, establishing karyotyping as a critical tool in modern genetic diagnostics

U.S. Karyotyping Market Insight

The U.S. karyotyping market captured the largest revenue share of 82% in 2024 within North America, fueled by the advanced healthcare infrastructure and the widespread adoption of genetic testing technologies. Clinical laboratories and hospitals are increasingly prioritizing accurate chromosomal analysis for prenatal screening, oncology diagnostics, and rare genetic disorders. The growing demand for AI-assisted and automated karyotyping solutions further propels market growth. Additionally, the integration of karyotyping with electronic health records (EHR) and personalized medicine initiatives is significantly contributing to the market’s expansion. The presence of skilled cytogeneticists, well-equipped research facilities, and strong government support for genetic diagnostics reinforces the U.S. market leadership.

Europe Karyotyping Market Insight

The Europe karyotyping market is projected to expand at a substantial rate throughout the forecast period, primarily driven by stringent healthcare regulations and the increasing emphasis on early detection of genetic disorders and cancers. The rise in prenatal and oncology testing, combined with the demand for precision medicine, is fostering adoption of karyotyping solutions. European research and clinical laboratories also benefit from robust infrastructure and technological expertise. Growing awareness among clinicians and patients about the advantages of advanced chromosomal testing is further encouraging uptake. The region is witnessing considerable growth across hospitals, academic research institutes, and biotechnology companies.

U.K. Karyotyping Market Insight

The U.K. karyotyping market is anticipated to grow at a noteworthy pace during the forecast period, driven by the increasing focus on genetic diagnostics, personalized medicine, and early disease detection. Rising concerns about hereditary disorders and cancer prevalence are motivating hospitals and laboratories to adopt comprehensive chromosomal analysis. The U.K.’s strong healthcare infrastructure, advanced research institutions, and adoption of digital solutions facilitate market growth. The expansion of public and private genetic testing initiatives is expected to continue stimulating market demand.

Germany Karyotyping Market Insight

The Germany karyotyping market is expected to expand at a considerable rate during the forecast period, fueled by increasing awareness of genetic disorders and demand for technologically advanced diagnostic solutions. Germany’s well-established healthcare and research infrastructure, along with emphasis on innovation and quality, promotes the adoption of karyotyping in clinical and research settings. Hospitals and diagnostic laboratories are increasingly integrating automated and AI-assisted karyotyping technologies. Government support for genetic research and personalized medicine initiatives also enhances market growth.

Asia-Pacific Karyotyping Market Insight

The Asia-Pacific karyotyping market is poised to grow at the fastest pace during the forecast period, driven by rising healthcare investments, urbanization, and technological advancements in countries such as China, Japan, and India. Growing awareness of genetic disorders and the expansion of hospitals and diagnostic laboratories are key factors driving adoption. The increasing emphasis on prenatal screening, cancer diagnostics, and research applications is supporting market growth. Additionally, emerging economies in the region are expanding their infrastructure for genetic testing, making karyotyping services more accessible and affordable.

Japan Karyotyping Market Insight

The Japan karyotyping market is gaining momentum due to the country’s advanced healthcare system, high focus on research, and growing demand for accurate genetic diagnostics. Adoption is fueled by an increasing number of hospitals and diagnostic laboratories offering prenatal, oncology, and rare disease testing. Integration of AI-assisted karyotyping and digital analysis tools enhances efficiency and diagnostic accuracy. Moreover, Japan’s aging population is driving demand for easier, precise chromosomal testing in both residential and clinical healthcare settings.

India Karyotyping Market Insight

The India karyotyping market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, expanding healthcare infrastructure, and rising awareness of genetic disorders. India is emerging as a key market for genetic testing, including prenatal and oncology diagnostics, with both private and public laboratories expanding their karyotyping capabilities. Government initiatives promoting genetic research, the rise of personalized medicine, and availability of cost-effective karyotyping solutions are major factors propelling market growth. The presence of skilled cytogeneticists and domestic manufacturers further strengthens the market landscape.

Karyotyping Market Share

The Karyotyping industry is primarily led by well-established companies, including:

- MetaSystems (Germany)

- Applied Spectral Imaging. (U.S.)

- PerkinElmer (U.S.)

- Oxford Gene Technology IP Limited (U.K.)

- Bio-Rad Laboratories, Inc. (U.S.)

- QIAGEN (Germany)

- Bionano Genomics, Inc. (U.S.)

- KONICA MINOLTA, INC. (Japan)

- Leica Biosystems (Germany)

- Sysmex Corporation (Japan)

- Cytosure, Inc. (U.S.)

- Creative Bioarray (U.S.)

- Laboratory Imaging s.r.o. (Czech Republic)

- West Medica Produktions- und Handels- GmbH (Austria)

- SciGene Corporation (U.S.)

- CytoTest Inc. (U.S.)

- Empire Genomics a Biocare Medical Company (U.S.)

- Applied Spectral Imaging (U.S.)

What are the Recent Developments in Global Karyotyping Market?

- In April 2025, Clean Cells, a French biologics services firm, acquired Karyologic, a karyotyping service provider, to establish a presence in the U.S. market. This acquisition enhances Clean Cells' capabilities in cell line analysis and expands its service offerings in the United States

- In May 2024, Dartmouth Health introduced Optical Genome Mapping (OGM), a pioneering digital karyotyping technology aimed at enhancing the diagnosis of hematologic cancers such as leukemias and lymphomas. OGM offers high-resolution detection of chromosomal aberrations, facilitating more precise and timely cancer diagnostics

- In May 2024, KromaTiD announced the expansion of their gene therapy analytic assay suite with the addition of Good Laboratory Practice (GLP) Genomic Integrity Karyotyping services. This expansion aims to support the growing need for comprehensive genomic analysis in gene and cell therapy applications

- In June 2023, Applied Spectral Imaging (ASI) and CytoCell announced a collaboration. ASI, a provider of cytogenetic and pathology imaging solutions, partnered with CytoCell, a division of OGT (a Sysmex Group company) specializing in diagnostic genomic solutions. This partnership aimed to expand the global reach of their products and enhance value for customers in cytogenetics laboratories worldwide

- In April 2021, MetaSystems received a U.S. patent for AI-based chromosome analysis. The patent recognizes the company's innovative use of artificial intelligence to assist in the classification of chromosomes. This development underscores the growing importance of AI and automation in streamlining the karyotyping workflow, reducing analysis time, and increasing the accuracy of chromosome analysis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.