Global Label Free Detection Market

Market Size in USD Billion

USD

1.43 Billion

USD

2.68 Billion

2024

2032

USD

1.43 Billion

USD

2.68 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.43 Billion | |

| USD 2.68 Billion | |

| % | |

|

Label-Free Detection Market Size

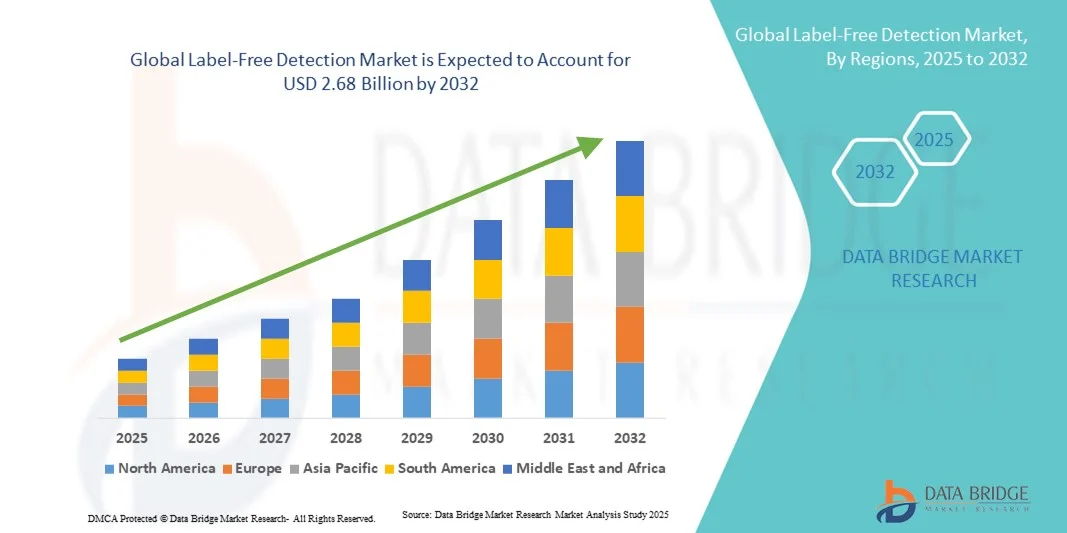

- The global label-free detection market size was valued at USD 1.43 billion in 2024 and is expected to reach USD 2.68 billion by 2032, at a CAGR of 8.20% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced analytical technologies and rising investments in life sciences research, diagnostics, and pharmaceutical development. With Label-Free Detection solutions offering real-time, high-throughput analysis without the need for fluorescent or radioactive tags, they are becoming essential tools in drug discovery, biomolecular interaction studies, and diagnostics applications

- Technological advancements in sensor platforms, such as surface plasmon resonance (SPR), biolayer interferometry (BLI), and optical waveguide-based systems, are further enhancing the sensitivity, accuracy, and scalability of Label-Free Detection methods. This progress is enabling researchers and laboratories to conduct more reliable experiments with lower operational costs, driving higher market adoption

Label-Free Detection Market Analysis

- Label-free detection technologies are increasingly vital components in modern biomedical research, offering real-time, label-free analysis of biomolecular interactions. These systems are integral to various applications, including drug discovery, biomarker development, and clinical diagnostics

- The escalating demand for label-free detection is primarily fueled by the need for high-throughput screening methods, advancements in biotechnology, and the growing emphasis on personalized medicine. The ability to perform real-time analysis without the use of labels enhances the efficiency and accuracy of research processes

- North America dominated the label-free detection market with the largest revenue share of 44.56% in 2024. This dominance is attributed to the region's robust healthcare infrastructure, significant investments in research and development, and the presence of leading pharmaceutical and biotechnology companies

- Asia-Pacific is expected to be the fastest-growing region in the label-free detection market during the forecast period, with a projected compound annual growth rate (CAGR) of 8.65%. Factors contributing to this growth include increasing healthcare expenditures, expanding research activities, and the rising adoption of advanced technologies in countries like China and India

- The Binding Kinetics segment dominated the label-free detection market with the largest revenue share of 50.7% in 2024, due to the critical need for accurate determination of molecular interaction rates and affinities. This segment is essential in drug discovery, antibody development, and protein characterization

Report Scope and Label-Free Detection Market Segmentation

|

Attributes |

Label-Free Detection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Label-Free Detection Market Trends

Enhanced Convenience Through Real-Time, Label-Free Analysis

- A significant and accelerating trend in the global label-free detection market is the increasing adoption of real-time, label-free technologies for biomolecular interaction analysis, enabling researchers to monitor molecular binding without the need for fluorescent or radioactive labels. This approach improves efficiency, reduces experimental complexity, and accelerates drug discovery and biomarker research

- For instance, Cytiva’s Sartorius Octet BLI system allows real-time monitoring of protein interactions without any labeling, offering rapid and accurate results for high-throughput screening

- Label-free systems such as Surface Plasmon Resonance (SPR) platforms now integrate advanced software analytics, enabling researchers to detect interactions at low concentrations and analyze kinetic binding parameters more efficiently

- The seamless integration of these systems with laboratory automation platforms and data management tools facilitates centralized control over multiple experiments, improving productivity and experimental reproducibility

- This trend toward more intelligent, high-throughput, and automated label-free detection platforms is reshaping expectations for efficiency and precision in research laboratories. Consequently, companies such as Bio-Rad and Bruker are developing label-free detection instruments with enhanced automation, real-time monitoring, and improved data analytics capabilities

- The demand for label-free detection technologies that offer real-time monitoring, automation, and high accuracy is growing rapidly across pharmaceutical, biotechnology, and academic research sectors, as users increasingly prioritize speed, precision, and cost-effectiveness in experimental workflows

Label-Free Detection Market Dynamics

Driver

Growing Demand for Efficient Drug Discovery and Biomolecular Research

- The increasing focus on rapid drug discovery, biomolecular research, and diagnostic development is a significant driver for the heightened demand for label-free detection systems. These technologies provide precise and reproducible measurements, which are critical for identifying therapeutic targets and evaluating candidate molecules

- For instance, in March 2024, Cytiva announced the expansion of its Octet BLI portfolio, enabling faster screening of antibody–antigen interactions for novel therapeutic development. Such strategies by leading companies are expected to drive the label-free detection market growth during the forecast period

- As research institutions and pharmaceutical companies face mounting pressure to accelerate development timelines, label-free detection platforms offer advantages such as reduced assay complexity, minimal sample consumption, and faster experimental turnaround

- Furthermore, the growing prevalence of personalized medicine and biologics development has increased reliance on high-precision analytical tools, making label-free detection an integral part of modern R&D pipelines

- The ability to perform real-time, accurate, and reproducible experiments positions label-free detection as a key enabler of efficient and cost-effective drug discovery and biomolecular research

Restraint/Challenge

High Instrumentation Costs and Technical Complexity

- The high initial cost and technical complexity associated with label-free detection instruments pose a significant challenge to market expansion. Advanced platforms such as SPR and BLI require substantial investment and trained personnel to operate effectively

- For instance, the Cytiva Octet system can be cost-prohibitive for smaller research labs or early-stage biotech companies, limiting its accessibility

- Addressing these challenges requires developing more cost-effective solutions, providing comprehensive user training, and integrating user-friendly software interfaces to lower technical barriers

- In addition, the complexity of interpreting kinetic binding data can be a hurdle for laboratories with limited expertise, necessitating software tools and support services from instrument manufacturers.

- Overcoming these barriers through instrument miniaturization, cloud-based data analytics, and flexible financing options will be vital for expanding adoption and sustained growth in the label-free detection market

Label-Free Detection Market Scope

The market is segmented on the basis of product and service, technology, application, and end user.

- By Product and Service

On the basis of product and service, the Label-Free Detection market is segmented into Instruments, Consumables, Software, and Services. The Instruments segment dominated the market with the largest revenue share of 48.6% in 2024. This dominance is driven by the increasing adoption of high-precision analytical platforms in pharmaceutical, biotechnology, and academic research. Instruments such as SPR, BLI, and ITC are widely used for binding kinetics, thermodynamics studies, and drug discovery applications. The segment benefits from continuous technological advancements, including enhanced automation, integration with software solutions, and compatibility with multiple biomolecular assays. Laboratories prefer advanced instruments to improve experimental accuracy, reproducibility, and throughput. Rising R&D investments by global pharmaceutical companies further boost demand. The need for high-throughput and sensitive detection methods in biopharmaceutical research sustains growth. Instrument-based platforms enable real-time monitoring of biomolecular interactions without additional labeling. In addition, strong support from academic and contract research organizations enhances market adoption. The instruments segment also drives innovation in label-free detection by enabling novel assay formats and multi-parameter measurements. Increasing emphasis on early-stage drug discovery and biologics development strengthens market demand.

The Software segment is expected to witness the fastest CAGR of 10.9% from 2025 to 2032. The growth is fueled by the increasing need for automated data analysis, AI-assisted interpretation, and visualization tools that simplify complex biomolecular studies. Software platforms enable seamless integration with instruments, cloud storage, and remote monitoring, improving operational efficiency. Researchers benefit from real-time analytics, reducing human error and accelerating decision-making. The adoption of advanced software supports high-throughput screening and kinetic modeling. Academic institutions and contract research organizations increasingly rely on software solutions to optimize workflows. Software facilitates standardized reporting, regulatory compliance, and reproducibility in experiments. The rising focus on personalized medicine and biologics development further drives software adoption. Compatibility with multiple label-free detection technologies enhances software versatility. Integration with machine learning and AI allows predictive modeling for drug discovery. The convenience of remote access and cloud-based platforms increases usability for global research teams. Software also supports cost reduction by minimizing experimental repeats and optimizing resource usage.

- By Technology

On the basis of technology, the market is segmented into Surface Plasmon Resonance (SPR), Bio-Layer Interferometry (BLI), Isothermal Titration Calorimetry (ITC), Differential Scanning Calorimetry (DSC), and Others. The Surface Plasmon Resonance (SPR) segment dominated the market with the largest revenue share of 45.3% in 2024. Its dominance is due to high sensitivity, real-time detection, and label-free operation. SPR is widely applied in drug discovery, antibody characterization, and protein–protein interaction studies. The segment benefits from reproducibility, flexibility, and compatibility with various biomolecules. Pharmaceutical and biotech companies heavily invest in SPR platforms for early-stage research. Academic and government research labs adopt SPR for precise kinetic and affinity measurements. Integration with advanced software and high-throughput formats enhances workflow efficiency. SPR enables multiplexed analysis and minimal sample consumption. Its reliability in regulatory-compliant experiments supports continued adoption. Rising biologics development fuels demand. Continuous technological innovation, such as miniaturized and automated SPR instruments, supports market growth. The segment also benefits from collaborations between instrument manufacturers and end users for tailored solutions. Increasing requirement for label-free, non-destructive detection strengthens SPR’s leading position.

The Bio-Layer Interferometry (BLI) segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2032. BLI’s growth is driven by high-throughput capabilities, simplicity, and suitability for large-scale screenings. It is increasingly adopted in antibody screening, protein–protein interaction studies, and kinetic analyses. BLI platforms reduce sample consumption and experimental time. Contract research organizations and academic institutions leverage BLI for rapid, reliable, and reproducible measurements. Its compatibility with multi-well plates enables simultaneous analysis of multiple interactions. The platform supports automation and integration with data analysis software. BLI adoption is rising in emerging markets due to affordability and ease of use. Flexibility in experimental design allows researchers to study diverse biomolecular interactions. Real-time, label-free detection minimizes interference and preserves sample integrity. The ability to provide kinetic and affinity data in high-throughput format accelerates drug discovery. Continuous innovation in BLI sensor technology further enhances accuracy and robustness. Increasing adoption by CROs and biotech startups contributes to rapid CAGR growth.

- By Application

On the basis of application, the market is segmented into Binding Kinetics, Binding Thermodynamics, Endogenous Receptor Detection, Hit Confirmation, Lead Generation, and Others. The Binding Kinetics segment dominated the market with the largest revenue share of 50.7% in 2024, due to the critical need for accurate determination of molecular interaction rates and affinities. This segment is essential in drug discovery, antibody development, and protein characterization. High adoption in pharmaceutical R&D is supported by regulatory and quality requirements. Binding kinetics analysis enables selection of optimal candidates and reduces clinical failure risks. Label-free technologies allow real-time, non-destructive measurement. Adoption is also driven by research in biologics, vaccines, and biosimilars. Contract research organizations and academic labs rely on binding kinetics for mechanistic studies. Advanced instruments and software integration improve data accuracy and reproducibility. Multi-parameter analysis enhances understanding of biomolecular interactions. Rising investments in early-stage drug discovery strengthen segment dominance. Market growth is supported by increasing pipeline development for complex biologics.

The Hit Confirmation segment is expected to witness the fastest CAGR of 10.8% from 2025 to 2032. The growth is fueled by the need for rapid validation of potential drug targets and early-stage screening of compounds. Label-free detection platforms enable fast, cost-effective, and reliable hit confirmation. High-throughput capabilities reduce experimental time while maintaining accuracy. CROs and biotech companies increasingly rely on hit confirmation for compound prioritization. Integration with automated instruments and software accelerates workflow efficiency. Emerging markets are adopting label-free methods to expand research capabilities. Non-destructive detection preserves sample integrity and allows repeated measurements. Compatibility with multiple molecular assays increases utility. Growing focus on antibody development and personalized medicine drives adoption. The segment benefits from technological innovations in sensor design and assay formats. Strong demand from academic and industrial research institutions further supports CAGR growth.

- By End User

On the basis of end user, the market is segmented into Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Contract Research Organizations (CROs), and Others. The Pharmaceutical and Biotechnology Companies segment dominated with the largest revenue share of 53.4% in 2024, driven by the growing focus on biologics, monoclonal antibodies, and precision medicine. Companies require accurate biomolecular characterization for preclinical studies, candidate optimization, and regulatory compliance. Adoption of label-free detection accelerates research timelines, improves reproducibility, and reduces experimental costs. High R&D investments and pipeline expansion in biologics development support segment dominance. Integration with automated instruments and software increases efficiency. Demand for label-free platforms spans early-stage discovery to process development. The segment also benefits from collaborations with instrument and software providers. Strong regulatory emphasis on robust data in drug approval processes enhances adoption. Advanced detection methods enable real-time monitoring and high-throughput analysis. Pharmaceutical companies prioritize platforms with multi-application compatibility. Market growth is further supported by ongoing innovation in analytical technologies.

The Contract Research Organizations (CROs) segment is expected to witness the fastest CAGR of 11.5% from 2025 to 2032. The growth is driven by outsourcing of R&D activities, increasing clinical trial volume, and the need for scalable, cost-efficient analytical solutions. CROs adopt label-free detection platforms for high-throughput screening, binding studies, and kinetic analysis. Platforms enable rapid, reproducible, and non-destructive experiments. Integration with software and automation enhances operational efficiency. Growing demand for biologics and personalized medicine fuels adoption. Emerging markets offer additional growth opportunities for CROs. BLI and SPR technologies are increasingly utilized by CROs for flexibility and speed. Label-free detection reduces experimental errors and optimizes workflows. Adoption in contract research supports faster time-to-market for clients. The segment benefits from collaborations with pharmaceutical and biotech companies. Technological innovations and affordability improvements further accelerate CAGR growth.

Label-Free Detection Market Regional Analysis

- North America dominated the label-free detection market with the largest revenue share of 44.56% in 2024

- This dominance is attributed to the region's robust healthcare infrastructure, significant investments in research and development, and the presence of leading pharmaceutical and biotechnology companies

- The market growth is further supported by increasing adoption of advanced analytical platforms in drug discovery, biologics development, and clinical research applications. The presence of well-established laboratories, advanced research facilities, and a high concentration of key market players enhances adoption

U.S. Label-Free Detection Market Insight

The U.S. label-free detection market captured the largest revenue share of 81% in 2024 within North America, driven by the swift adoption of advanced analytical systems, high-throughput platforms, and integration of AI-assisted data analytics in research workflows. Pharmaceutical and biotechnology companies are increasingly prioritizing label-free detection technologies for drug discovery, antibody characterization, and biomolecular interaction studies. The market benefits from the presence of top research institutions, clinical laboratories, and robust funding programs. Continuous advancements in sensor technology and automation are accelerating adoption across multiple research applications.

Europe Label-Free Detection Market Insight

The Europe Label-Free Detection market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory requirements for drug development and the rising demand for advanced analytical technologies in research. Key countries, including Germany, France, and the U.K., are witnessing strong adoption due to well-established healthcare and research infrastructures. Academic institutions and pharmaceutical R&D centers are major contributors to growth, focusing on precision medicine and biologics development. The market also benefits from government initiatives promoting biotechnology and advanced research programs.

U.K. Label-Free Detection Market Insight

The U.K. label-free detection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing research activities in the pharmaceutical and biotechnology sectors. Rising investments in biologics development and personalized medicine are enhancing demand for label-free detection platforms. The presence of advanced research facilities and active collaboration between academic institutions and industry players supports market expansion.

Germany Label-Free Detection Market Insight

The Germany label-free detection market is expected to expand at a considerable CAGR during the forecast period, fueled by rising research expenditures, strong healthcare infrastructure, and the presence of major pharmaceutical and biotechnology companies. Germany’s emphasis on innovation, high-quality research, and regulatory compliance supports the adoption of advanced label-free detection instruments and software.

Asia-Pacific Label-Free Detection Market Insight

The Asia-Pacific label-free detection market is poised to grow at the fastest CAGR of 8.65% during the forecast period, driven by increasing healthcare expenditures, expanding research activities, and the rising adoption of advanced analytical technologies in countries such as China, India, and Japan. Growing investments in pharmaceutical R&D, biologics development, and academic research initiatives are key factors propelling market growth. The expansion of biotechnology and life sciences industries, coupled with government support for research infrastructure, is facilitating adoption of label-free detection platforms.

Japan Label-Free Detection Market Insight

The Japan label-free detection market is gaining momentum due to the country’s high-tech research environment, increasing healthcare investments, and rising focus on biologics and precision medicine. The market is supported by strong government initiatives promoting innovation in life sciences and advanced analytical technologies. Adoption is driven by pharmaceutical companies, contract research organizations, and academic research institutes seeking real-time, high-throughput biomolecular analysis solutions.

China Label-Free Detection Market Insight

The China label-free detection market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid technological adoption, expanding industrial applications, and growing research infrastructure. China’s increasing focus on pharmaceutical R&D, government funding for life sciences research, and growing biotechnology ecosystem are key factors driving market growth. The rising number of research laboratories, universities, and contract research organizations further supports the demand for label-free detection platforms.

Label-Free Detection Market Share

The label-free detection industry is primarily led by well-established companies, including:

- Cytiva (U.S.)

- GE Healthcare (U.S.)

- Sartorius AG (Germany)

- Bio-Rad Laboratories, Inc. (U.S.)

- Agilent Technologies, Inc. (U.S.)

- Bruker (U.S.)

- Malvern Panalytical Ltd. (U.K.)

- Sartorius AG (Germany)

- IBIS Technologies B.V. (Netherlands)

- NanoTemper Technologies (Germany)

- Molecular Devices, LLC. (U.S.)

- XanTec bioanalytics GmbH (Germany)

- Bioinformatics Solutions Inc. (Canada)

- Biosensing Instrument (U.S.)

Latest Developments in Global Label-Free Detection Market

- In April 2022, Sartorius AG introduced the Octet® SF3, a next-generation Surface Plasmon Resonance (SPR) system. This launch marked Sartorius as the only brand to offer both Bio-Layer Interferometry (BLI) and SPR technologies, enhancing its position in advanced label-free bioanalytics. The Octet SF3 provides robust, high-throughput, low-maintenance characterization of biomolecular interactions, featuring OneStep Injection Technology to eliminate the need for multiple dilution series

- In February 2022, Bruker Corporation unveiled the timsTOF MALDI PharmaPulse (MPP) system at the SLAS2022 International Conference and Exhibition. This high-end solution offers unbiased, deep high-throughput screening (HTS) and ultra HTS based on label-free mass spectrometry. The system integrates advanced mass spectrometry techniques with label-free detection, enabling rapid and accurate analysis of biomolecular interactions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.