Global Low Differential Pressure Sensor Market

Market Size in USD Billion

USD

12.66 Billion

USD

23.62 Billion

2024

2032

USD

12.66 Billion

USD

23.62 Billion

2024

2032

| 2025 - 2032 | |

| USD 12.66 Billion | |

| USD 23.62 Billion | |

| % | |

|

What is the Global Low Differential Pressure Sensor Market Size and Growth Rate?

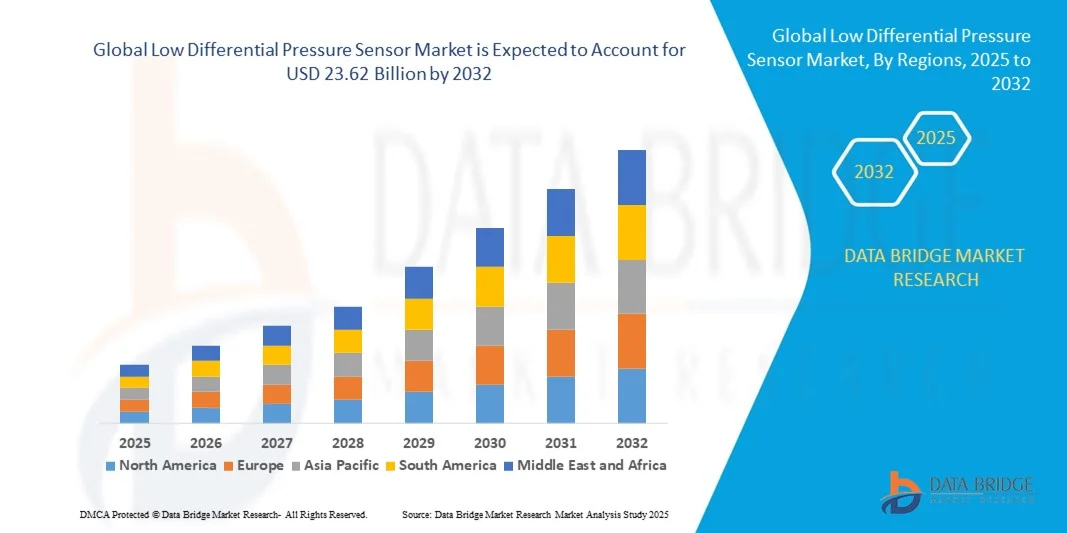

- The global low differential pressure sensor market size was valued at USD 12.66 billion in 2024 and is expected to reach USD 23.62 billion by 2032, at a CAGR of 8.10% during the forecast period

- Rising industrialization and growth in the production of automobiles will emerge as the major low differential pressure sensor market growth driving factor

- Growing technological advancements in the low differential pressure sensors, surging adoption of internet of things technology and rising globalization and urbanization of economies will further aggravate the low differential pressure sensor market value

What are the Major Takeaways of Low Differential Pressure Sensor Market?

- Growing expenditure to undertake research and development proficiencies and growing demand for miniaturized consumer devices will further carve the way for the growth of the low differential pressure sensor market

- However, lack of awareness in the underdeveloped economies and maturity of end user segment will act as a growth restraint for the low differential pressure sensor market. High costs involved and low profit margin will further dampen the growth rate of the low differential pressure sensor market. Dearth of technological expertise will further challenge the low differential pressure sensor market growth rate

- Asia-Pacific dominated the low differential pressure sensor market with the largest revenue share of 39.91% in 2024, driven by rapid urbanization, government initiatives promoting smart homes, and strong adoption of connected devices across residential, commercial, and industrial sectors

- North America is expected to grow at the fastest CAGR of 8.25% from 2025 to 2032, driven by the increasing adoption of connected devices, home automation, and smart building solutions

- The digital segment dominated the market with a revenue share of 62% in 2024, owing to its advanced capabilities such as real-time data transmission, enhanced signal processing, and seamless integration with building management and industrial automation systems

Report Scope and Low Differential Pressure Sensor Market Segmentation

|

Attributes |

Low Differential Pressure Sensor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Low Differential Pressure Sensor Market?

Smart Monitoring and Predictive Insights

- A major trend in the global low differential pressure sensor market is the integration of advanced analytics, AI, and IoT connectivity to enable real-time monitoring, predictive maintenance, and automated alerts. This trend is helping industries optimize system performance, reduce downtime, and enhance operational safety

- For instance, modern low differential pressure sensors now integrate with cloud platforms and analytics software, providing actionable insights into airflow, filter clogging, and system efficiency, enabling proactive maintenance

- AI-enabled sensors can learn system patterns, detect anomalies, and alert facility managers to unusual pressure changes, improving safety and reducing maintenance costs

- Integration with IoT platforms allows centralized monitoring across multiple sites, giving users full visibility and control over HVAC systems, clean rooms, and industrial processes from a single interface

- This shift toward intelligent, predictive, and interconnected sensor systems is reshaping industrial and commercial expectations. Companies such as Honeywell and TE Connectivity are developing solutions that combine AI and cloud connectivity to maximize performance and energy efficiency

- The adoption of Low Differential Pressure Sensors with predictive and AI-driven capabilities is growing rapidly across industrial, commercial, and healthcare sectors, as organizations seek efficiency, reliability, and cost savings

What are the Key Drivers of Low Differential Pressure Sensor Market?

- Increasing awareness of energy efficiency and operational reliability across industrial and commercial sectors is driving the demand for Low Differential Pressure Sensors

- For instance, in March 2024, TE Connectivity launched an AI-enabled sensor line for HVAC and filtration systems, enabling predictive maintenance and energy optimization. Such initiatives are expected to fuel market growth

- The need to comply with stringent regulatory standards for clean rooms, hospitals, and industrial processes encourages the adoption of precise low differential pressure monitoring

- Growing industrial automation and smart building implementations make these sensors an integral component of interconnected systems, allowing seamless integration with building management or process control systems

- The convenience of remote monitoring, automated alerts, and predictive maintenance reduces operational costs, minimizes downtime, and enhances safety, thereby accelerating adoption across manufacturing, healthcare, and commercial sectors

Which Factor is Challenging the Growth of the Low Differential Pressure Sensor Market?

- High initial investment and integration complexity pose a barrier to adoption, especially for small-scale industries or budget-conscious facilities. Advanced sensors with AI and IoT integration are costlier than traditional mechanical or analog devices

- Concerns regarding data security and network vulnerabilities in connected sensor systems can make industries cautious about deploying IoT-enabled solutions

- For instance, reported breaches in industrial IoT systems have highlighted potential risks in connected sensors, leading to adoption hesitancy

- Addressing these challenges requires robust encryption, secure data protocols, and user-friendly deployment. Companies such as Honeywell and Schneider Electric emphasize security and seamless integration in their sensor solutions to build trust

- Although costs are gradually decreasing, the perceived premium for smart, connected sensor technology may still hinder widespread adoption, particularly in developing regions

- Overcoming these barriers through affordable, secure, and scalable sensor solutions and educating end-users about energy and operational efficiency benefits will be vital for sustained market growth

How is the Low Differential Pressure Sensor Market Segmented?

The market is segmented on the basis of interface, accuracy, and end user.

- By Interface

On the basis of interface, the low differential pressure sensor market is segmented into analogue and digital. The digital segment dominated the market with a revenue share of 62% in 2024, owing to its advanced capabilities such as real-time data transmission, enhanced signal processing, and seamless integration with building management and industrial automation systems. Digital sensors are widely preferred in modern HVAC systems, clean rooms, and industrial applications due to their precision, ease of calibration, and compatibility with IoT platforms. They allow centralized monitoring and predictive maintenance through analytics software, reducing operational downtime and improving energy efficiency.

Conversely, the analogue segment is still used in simpler applications for cost-sensitive setups but is gradually losing market share due to the growing preference for automation and smart monitoring solutions. The digital interface segment is also expected to witness the fastest CAGR of 20.5% during 2025–2032, driven by rising demand for smart, connected, and high-performance sensor systems across industrial and commercial sectors.

- By Accuracy

On the basis of accuracy, the low differential pressure sensor market is segmented into 0.1–0.2%, 0.2–0.5%, and above 0.55%. The 0.2–0.5% segment dominated the market with a revenue share of 55% in 2024, as it provides a balance between precision, cost, and ease of implementation, making it ideal for HVAC systems, hospitals, and industrial monitoring. Sensors in this range offer sufficient reliability for maintaining airflow, pressure differentials, and safety compliance without the higher costs associated with ultra-precise models.

The 0.1–0.2% segment is expected to witness the fastest growth during 2025–2032, fueled by rising adoption in critical environments such as cleanrooms, laboratories, and healthcare facilities where minute pressure variations must be accurately measured. Increasing regulatory requirements and technological advancements are supporting the shift toward highly accurate sensors that can provide actionable data for preventive maintenance and energy optimization.

- By End User

On the basis of end user, the low differential pressure sensor market is segmented into HVAC, hospitals, laboratories, and others. The HVAC segment dominated the market with a 50% revenue share in 2024, driven by the widespread adoption of smart building systems, energy efficiency regulations, and demand for optimized airflow and pressure management in residential and commercial properties. HVAC applications require continuous monitoring to maintain system performance, reduce energy consumption, and prevent equipment failure, making these sensors indispensable.

The laboratories segment is projected to witness the fastest CAGR of 21% during 2025–2032, as precision control of environmental conditions is critical for research, pharmaceuticals, and semiconductor fabrication. Hospitals are also increasingly adopting low differential pressure sensors for cleanroom environments, operating theaters, and infection control, emphasizing safety and regulatory compliance. Overall, the growth of end-user applications is being driven by digital integration, energy-saving initiatives, and a shift toward smart facilities.

Which Region Holds the Largest Share of the Low Differential Pressure Sensor Market?

- Asia-Pacific dominated the low differential pressure sensor market with the largest revenue share of 39.91% in 2024, driven by rapid urbanization, government initiatives promoting smart homes, and strong adoption of connected devices across residential, commercial, and industrial sectors

- Consumers in the region increasingly value the convenience, energy efficiency, and integration offered by low differential pressure sensors with other smart devices such as HVAC systems, lighting, and industrial automation platforms

- The widespread adoption is further supported by a growing middle class, rising disposable incomes, and the expansion of smart city projects, establishing Low Differential Pressure Sensors as a preferred solution for both home and business environments

China Low Differential Pressure Sensor Market Insight

In China, the low differential pressure sensor market accounted for the largest revenue share in Asia-Pacific in 2024. Rapid urbanization, an expanding middle class, and strong adoption of smart homes and commercial buildings drive growth. Government-backed smart city initiatives, coupled with affordable sensor solutions and domestic manufacturing capabilities, make China a key market. Sensors are widely integrated into residential, commercial, and rental properties, enhancing energy efficiency and system automation. Technological advancements and IoT adoption are accelerating deployment across HVAC, industrial, and healthcare sectors, further consolidating China’s leadership in the global Low Differential Pressure Sensor market.

Japan Low Differential Pressure Sensor Market Insight

In Japan, the low differential pressure sensor market is growing steadily due to the country’s high-tech culture and increasing number of connected homes and commercial buildings. Consumers value seamless integration with IoT devices such as lighting, HVAC, and security systems, driving adoption. The aging population also supports demand for easy-to-use, secure, and reliable sensors. Japan’s emphasis on energy efficiency, industrial automation, and smart building solutions further fuels market expansion. Residential, commercial, and institutional applications benefit from precise pressure monitoring, enhancing convenience, safety, and operational efficiency. Continuous technological innovations are expected to sustain strong growth in Japan over the forecast period.

Which Region is the Fastest Growing Region in the Low Differential Pressure Sensor Market?

North America is expected to grow at the fastest CAGR of 8.25% from 2025 to 2032, driven by the increasing adoption of connected devices, home automation, and smart building solutions. Consumers in the U.S. and Canada are prioritizing intelligent, energy-efficient, and easy-to-use Low Differential Pressure Sensors for residential and commercial applications. The growing trend of DIY smart home installations, combined with demand for voice-controlled systems and mobile app integration, is further propelling market growth.

U.S. Low Differential Pressure Sensor Market Insight

In the U.S., the low differential pressure sensor market captured the largest revenue share of 71% within North America in 2024. The market growth is fueled by increasing smart home adoption, DIY installations, and integration with voice-controlled platforms such as Alexa, Google Assistant, and Apple HomeKit. Consumers increasingly prefer energy-efficient and remotely controllable solutions for residential and commercial applications. Strong demand exists across HVAC systems, industrial automation, and healthcare facilities. Advanced features such as digital monitoring, automated alerts, and smartphone-based control are driving adoption. The U.S. market continues to expand rapidly due to consumer preference for convenience, safety, and connected smart building solutions.

Canada Low Differential Pressure Sensor Market Insight

In Canada, the low differential pressure sensor market is growing steadily, driven by rising awareness of smart homes, industrial automation, and energy-efficient building solutions. The government encourages adoption through incentives for green construction and smart infrastructure projects. Canadian consumers and businesses are adopting sensors for HVAC systems, hospitals, laboratories, and commercial buildings to improve operational efficiency, safety, and monitoring. Integration with IoT platforms allows centralized control and data analytics. The demand for precise, reliable, and user-friendly pressure sensors is increasing, supporting growth across residential, commercial, and industrial sectors. Continuous technological improvements are expected to sustain market momentum in Canada.

Which are the Top Companies in Low Differential Pressure Sensor Market?

The low differential pressure sensor industry is primarily led by well-established companies, including:

- Honeywell International Inc. (U.S.)

- TE Connectivity (Switzerland)

- Robert Bosch GmbH (Germany)

- ABB (Switzerland)

- NXP Semiconductors (Netherlands)

- Infineon Technologies AG (Germany)

- GENERAL ELECTRIC COMPANY (U.S.)

- Schneider Electric (France)

- Emerson Electric Co. (U.S.)

- DENSO CORPORATION (Japan)

- OMRON Corporation (Japan)

- Rockwell Automation, Inc. (U.S.)

- Texas Instruments Incorporated (U.S.)

- Bestech Australia (Australia)

- Servoflo Corporation (U.S.)

- SensorsONE Ltd (U.K.)

- DWYER Instruments, Inc. (U.S.)

- Sensirion AG Switzerland (Switzerland)

- SEMI (U.S.)

- OMEGA Engineering (U.S.)

What are the Recent Developments in Global Low Differential Pressure Sensor Market?

- In February 2025, Honeywell International Inc. (U.S.) announced a strategic partnership with ForwardEdge ASIC (U.S.), a subsidiary of Lockheed Martin, to develop radiation-hardened microelectronics for space applications, leveraging Honeywell’s foundry expertise and ForwardEdge’s design capabilities, aiming to provide highly reliable ASICs and memory solutions for satellites and defense systems, marking a significant step in aerospace-grade sensor technology

- In November 2024, ABB (Switzerland) launched its new P-Series pressure transmitter portfolio at CIIE, including the P-100, P-300, and high-precision P-500 series, integrating digital technologies such as Bluetooth, RFID, and advanced HMI to enhance process control and energy efficiency across industries, demonstrating the company’s commitment to industrial digital transformation

- In April 2024, TE Connectivity (Switzerland) expanded its wireless IoT pressure sensor lineup with the 65xxN (BLE-based) for short-range and 69xxN (LoRaWAN-based) for long-range applications, providing ultra-compact, low-power solutions for real-time condition monitoring in industrial environments, supporting predictive maintenance and advancing smart factory initiatives, reinforcing its leadership in industrial IoT

- In March 2024, Amphenol Corporation (U.S.) introduced the AABP Series, a leadless miniature package pressure sensor designed for diverse design requirements, ensuring supply chain stability and serving as a drop-in replacement for existing designs or competitors’ products, emphasizing reliability and quality across various pressure sensing applications, strengthening its market position

- In January 2024, Sensata Technologies, Inc. (U.S.) unveiled the 129CP Series Digital Water Pressure Sensor, aimed at water utilities for intelligent pressure monitoring and water conservation, integrating with water meter PCBs for reliable readings from 0-232 psi in high-moisture environments, offering digital I2C output and low power consumption, enabling utilities to detect leaks efficiently and optimize water distribution

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Low Differential Pressure Sensor Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Low Differential Pressure Sensor Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Low Differential Pressure Sensor Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.