Global Medical Automation Market

Market Size in USD Billion

USD

53.34 Billion

USD

110.73 Billion

2024

2032

USD

53.34 Billion

USD

110.73 Billion

2024

2032

| 2025 - 2032 | |

| USD 53.34 Billion | |

| USD 110.73 Billion | |

| % | |

|

Medical Automation Market Size

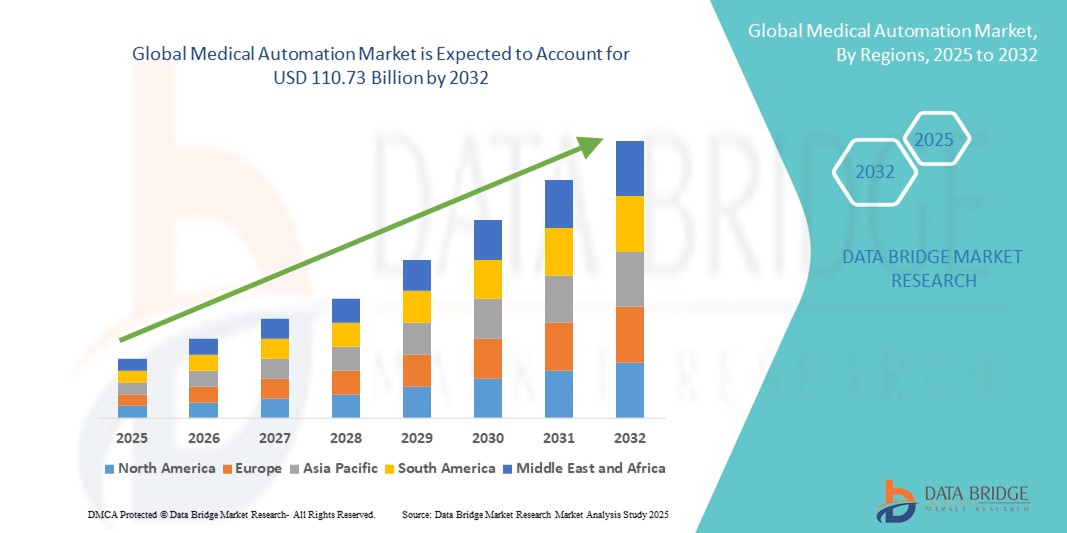

- The global medical automation market size was valued at USD 53.34 billion in 2024 and is expected to reach USD 110.73 billion by 2032, at a CAGR of 9.56% during the forecast period

- The market growth is primarily driven by the increasing need for operational efficiency, accuracy, and cost reduction in healthcare facilities, coupled with technological advancements in robotics, AI, and automated laboratory systems

- Moreover, the rising demand for faster diagnostics, improved patient outcomes, and streamlined hospital workflows is positioning medical automation as an essential component of modern healthcare infrastructure. These factors are collectively accelerating the adoption of medical automation solutions, thereby significantly propelling the market’s growth

Medical Automation Market Analysis

- Medical automation, including robotics, automated laboratory systems, and AI-driven diagnostic tools, is increasingly becoming a cornerstone of modern healthcare facilities due to its ability to enhance operational efficiency, accuracy, and patient safety across clinical and administrative workflows

- The growing demand for medical automation is primarily driven by the need for faster diagnostics, reduced human error, optimized hospital operations, and the integration of advanced technologies such as AI, machine learning, and IoT in healthcare processes

- North America dominated the medical automation market with the largest revenue share of 39.5% in 2024, supported by advanced healthcare infrastructure, high adoption of cutting-edge technologies, and the presence of major market players, with the U.S. witnessing significant growth in robotic surgeries, automated lab testing, and AI-enabled clinical decision support systems

- Asia-Pacific is expected to be the fastest-growing region in the medical automation market during the forecast period due to rising healthcare investments, expanding hospital networks, and increasing demand for efficient, scalable, and cost-effective medical solutions in emerging economies

- Lab and Pharmacy Automation segment dominated the medical automation market with a market share of 42.2% in 2024, driven by increasing demand for high-throughput, accurate, and reproducible testing, as well as integration with digital healthcare management systems

Report Scope and Medical Automation Market Segmentation

|

Attributes |

Medical Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Automation Market Trends

Intelligent Healthcare Operations Through AI and Robotics

- A significant and accelerating trend in the global medical automation market is the deepening integration of artificial intelligence (AI), machine learning (ML), and robotic systems across diagnostics, therapeutics, and laboratory operations. This convergence is enhancing operational efficiency, accuracy, and patient care outcomes

- For instance, robotic-assisted surgical systems such as the da Vinci Surgical System allow surgeons to perform minimally invasive procedures with greater precision, while AI-enabled diagnostic platforms such as PathAI improve pathology slide analysis accuracy. Similarly, automated pharmacy dispensing systems streamline medication management, reducing errors and improving patient safety

- AI integration in medical automation enables predictive analytics for patient monitoring, workflow optimization in hospitals, and intelligent decision support in diagnostics. For example, some automated laboratory platforms utilize AI to optimize test sequencing and flag anomalies in real time. Robotics in hospitals further enhance operational efficiency, performing repetitive tasks such as sample handling, sterilization, or logistics with minimal human intervention

- The seamless integration of automation platforms with electronic health records (EHR) and hospital management systems facilitates centralized monitoring and control over multiple aspects of healthcare delivery. Through a single interface, medical staff can manage diagnostics, therapeutics, inventory, and patient data, creating a unified, efficient, and error-minimized environment

- This trend towards more intelligent, interconnected, and data-driven healthcare systems is fundamentally reshaping expectations for clinical operations. Consequently, companies such as Intuitive Surgical, Siemens Healthineers, and Philips are developing AI-enabled and robotic solutions that integrate predictive analytics, workflow automation, and interoperability with hospital IT infrastructure

- The demand for medical automation solutions offering AI-driven decision support, robotics integration, and interoperability with digital healthcare platforms is growing rapidly across hospitals, diagnostic centers, and research institutes, as healthcare providers prioritize efficiency, safety, and quality of care

Medical Automation Market Dynamics

Driver

Rising Need for Efficiency, Accuracy, and Patient Safety in Healthcare Delivery

- The increasing demand for faster diagnostics, reduced human error, and optimized hospital operations is a significant driver for the heightened adoption of medical automation

- For instance, in March 2024, Siemens Healthineers launched an AI-powered imaging platform that accelerates radiology workflows and enhances diagnostic precision. Such innovations by key companies are expected to propel the medical automation market during the forecast period

- As healthcare providers face mounting pressure to improve patient outcomes and reduce operational costs, medical automation systems offer advanced functionalities such as automated sample handling, predictive analytics, and real-time patient monitoring, providing compelling advantages over manual processes

- Furthermore, the growing trend of smart hospitals, adoption of EHR systems, and integration of IoT-enabled medical devices are making automation an essential component of healthcare infrastructure

- The ability to automate repetitive tasks, optimize staff allocation, and enable remote monitoring of patients contributes significantly to market growth. The trend towards AI-enabled decision support and the increasing availability of user-friendly automation solutions further accelerate adoption in both developed and emerging markets

Restraint/Challenge

High Implementation Costs and Regulatory Compliance Hurdles

- The relatively high cost of implementing advanced medical automation systems, combined with complex regulatory compliance requirements, poses a challenge for widespread adoption, particularly among smaller healthcare facilities

- For instance, sophisticated robotic surgery platforms and fully automated laboratory systems require substantial upfront investment and ongoing maintenance costs, limiting accessibility for budget-constrained hospitals or clinics

- In addition, stringent regulations around patient data privacy, medical device safety, and interoperability standards can slow the deployment of automation solutions. Companies must navigate compliance with FDA, CE, and HIPAA regulations, among others

- Addressing these challenges through scalable, cost-effective solutions, training programs for healthcare personnel, and adherence to regulatory frameworks is crucial for building trust and encouraging broader adoption. Moreover, increasing awareness about long-term cost savings, efficiency gains, and improved patient outcomes can mitigate perceived barriers associated with high initial investments

- Continuous innovation to offer modular, flexible, and affordable automation solutions will be vital to overcoming these challenges and sustaining market growth

Medical Automation Market Scope

The market is segmented on the basis of component, type, application, connectivity, distribution channel, and end user.

- By Component

On the basis of component, the medical automation market is segmented into equipment, software, and services. Equipment leads the market due to the increasing adoption of advanced medical devices such as robotic surgical systems, diagnostic imaging machines, and automated laboratory instruments. These devices enhance precision, reduce human error, and improve patient outcomes, making them integral to modern healthcare facilities. Hospitals and diagnostic centers prioritize equipment that supports efficient workflows and reliable performance. Continuous technological innovations, along with strong capital investments from healthcare providers, reinforce the dominance of this segment. In addition, the high demand for automated imaging and laboratory systems across developed and emerging markets sustains equipment’s significant market share.

Services are growing rapidly during forecast period, driven by the rising need for maintenance, training, and support for complex medical automation systems. As healthcare providers adopt more automated solutions, comprehensive service packages ensure optimal performance, minimize downtime, and comply with regulatory standards. Outsourced biomedical engineering services, technical support, and installation assistance further boost demand. Growth is particularly strong in regions with increasing hospital automation and emerging telemedicine services. The segment benefits from a shift toward subscription-based service models, offering continuous updates and training to healthcare staff.

- By Type

On the basis of type, the medical automation market is segmented into automated prescription formulation and dispensing, automated health assessment and monitoring, automated imaging, automated healthcare logistics, resource and personnel tracking, medical robotics and computer-assisted surgical devices, therapeutic automation, procedures, and automated laboratory testing and analysis. Therapeutic automation has a strong market presence due to robotic-assisted surgeries, automated drug delivery systems, and treatment technologies that improve clinical outcomes. Hospitals and specialty clinics adopt these solutions for reduced complications, enhanced precision, and accelerated patient recovery. Technological advancements in robotics and minimally invasive procedures drive adoption, supported by increasing clinical acceptance. This segment benefits from growing investments in high-end surgical and therapeutic equipment in developed healthcare systems. Its integration with hospital IT systems allows better workflow management and monitoring, reinforcing its critical role in modern healthcare.

Automated prescription formulation and dispensing is growing rapidly during forecast period, driven by the need to reduce medication errors, enhance pharmacy workflow efficiency, and improve patient safety. Automation streamlines the process from prescription to dispensing, ensuring accuracy, faster delivery, and better inventory management. Hospitals, pharmacies, and homecare providers increasingly implement these solutions to optimize operational efficiency. Regulatory requirements and patient safety initiatives further encourage adoption. The integration of these systems with electronic health records (EHR) improves medication tracking and adherence, enhancing overall healthcare quality.

- By Application

On the basis of application, the medical automation market is segmented into diagnostics and monitoring, therapeutics, lab and pharmacy automation, medical logistics and training, and others. Lab and pharmacy automation dominates the market with a market share of 42.2%, due to its ability to increase throughput, reduce human errors, and ensure consistent quality in laboratory and pharmacy operations. Automated systems streamline sample analysis, medication dispensing, and inventory management, improving operational efficiency and patient safety. Hospitals, diagnostic centers, and research labs increasingly adopt these systems to optimize workflows. Integration with EHRs and digital healthcare platforms enhances process control and allows real-time monitoring. The segment benefits from the growing demand for rapid diagnostics, regulatory compliance, and the need for high-quality standards in laboratory and pharmacy environments. Automation also enables faster turnaround times and reduces manual labor, strengthening its market dominance.

Diagnostics and monitoring is growing steadily during forecast period, driven by the need for accurate, real-time patient data to guide treatment decisions. Automated imaging systems, patient monitoring devices, and laboratory diagnostic platforms enhance clinical precision. AI and machine learning integration in diagnostics enables predictive insights and early detection of diseases. Hospitals and specialty clinics are increasingly adopting automated diagnostics to improve patient outcomes. Remote monitoring capabilities allow healthcare providers to track patient health continuously, supporting proactive interventions. The expansion of telemedicine services further accelerates adoption of automated diagnostics and monitoring systems.

- By Connectivity

On the basis of connectivity, the medical automation market is segmented into wired and wireless. Wireless connectivity dominates due to its flexibility, real-time data transmission, and ease of integration with IoT-enabled devices. Wireless-enabled systems support remote monitoring, telemedicine, and seamless communication between healthcare providers and patients. Hospitals increasingly implement wireless solutions for automated monitoring, imaging, and robotic procedures. Integration with cloud platforms allows data analytics, predictive maintenance, and improved operational efficiency. Wireless adoption is accelerated by the growing trend of smart healthcare ecosystems and connected devices across clinical and homecare settings.

Wireless systems are also growing rapidly during forecast period, due to the proliferation of IoT-based medical devices and smart healthcare platforms. Remote patient monitoring, wearable health devices, and mobile-enabled automation benefit from wireless connectivity. The need for flexible and scalable healthcare solutions drives adoption, particularly in telehealth, homecare, and outpatient settings. Wireless connectivity reduces infrastructure costs and enables seamless software updates and device interoperability. Growth is further fueled by increasing demand for real-time patient data collection and integration into hospital management systems.

- By Distribution Channel

On the basis of distribution channel, the medical automation market is segmented into direct tender, retail sales, online sales, and others. Direct tender dominates as large hospitals, healthcare networks, and public health systems procure automation solutions in bulk for standardization, regulatory compliance, and long-term service agreements. High-value equipment such as robotic surgery systems and automated lab instruments are typically purchased through tenders. This channel ensures reliable delivery, installation, and support. Bulk procurement facilitates cost savings and compliance with hospital procurement policies. Direct tender adoption is higher in regions with centralized healthcare systems and government-backed hospitals.

Online sales are growing rapidly during forecast period, driven by the increasing digitalization of healthcare procurement. Online platforms provide a broad product range, competitive pricing, and faster delivery, making them attractive for smaller hospitals, clinics, and homecare providers. The rise of telemedicine and remote patient monitoring solutions has further increased online adoption. Digital catalogs, e-commerce portals, and direct-to-consumer sales models simplify procurement and reduce lead times. Online sales enable easier access to low- and medium-value automation products, particularly in emerging markets.

- By End User

On the basis of end user, the medical automation market is segmented into hospitals, diagnostic centers, pharmacies, research labs and institutes, homecare, specialty clinics, ambulatory surgical centers (ASCs), and others. Hospitals dominate due to their extensive need for advanced diagnostic, therapeutic, and monitoring equipment. High patient volumes, complex workflows, and the requirement for efficiency and patient safety drive adoption. Hospitals utilize automation in surgery, pharmacy, laboratories, and patient monitoring, supported by significant capital investments. Integration with hospital IT systems and EHR platforms enhances workflow management. Continuous adoption of AI-driven diagnostic and robotic therapeutic systems reinforces hospitals’ position as the largest end user segment.

Homecare is growing rapidly during forecast period, driven by an aging population, increasing prevalence of chronic diseases, and patient preference for receiving care at home. Automation in homecare, including remote monitoring devices and telehealth platforms, enables continuous care, improves patient compliance, and reduces hospital readmissions. Adoption is supported by wearable health devices, IoT-based monitoring systems, and connected care platforms. Cost efficiency and convenience for patients also encourage homecare automation growth. Digital solutions allow healthcare providers to track patient progress in real time, enhancing care quality outside traditional hospital settings.

Medical Automation Market Regional Analysis

- North America dominated the medical automation market with the largest revenue share of 39.5% in 2024, supported by advanced healthcare infrastructure, high adoption of cutting-edge technologies, and the presence of major market players, with the U.S. witnessing significant growth in robotic surgeries, automated lab testing, and AI-enabled clinical decision support systems

- Healthcare providers in North America increasingly deploy automated diagnostic tools, robotic surgical systems, and laboratory automation solutions to reduce human error and improve workflow efficiency. Hospitals and specialty clinics prioritize automation to handle high patient volumes and complex procedures

- The widespread adoption is further supported by significant R&D investments, high healthcare expenditure, and a skilled workforce capable of managing sophisticated medical automation equipment. Increasing integration of AI, IoT, and connected healthcare platforms also enhances operational efficiency and clinical outcomes

U.S. Medical Automation Market Insight

The U.S. medical automation market captured the largest revenue share in North America in 2024, driven by advanced healthcare infrastructure, high adoption of cutting-edge medical technologies, and strong investments in hospital automation. Healthcare providers are increasingly deploying automated diagnostic tools, robotic surgical systems, and laboratory automation solutions to reduce human error and enhance workflow efficiency. The growing integration of AI, IoT, and connected healthcare platforms is further boosting the adoption of automation across hospitals, specialty clinics, and research institutes. In addition, government initiatives supporting digital health and telemedicine, along with strong R&D investments by private companies, are accelerating market growth. Patient safety, operational efficiency, and the need to handle high patient volumes remain key drivers of demand.

Europe Medical Automation Market Insight

The Europe medical automation market is projected to expand at a substantial CAGR during the forecast period, driven by well-established healthcare infrastructure, increasing demand for operational efficiency, and stringent regulatory standards. Hospitals and diagnostic centers are adopting automation to streamline workflows, reduce errors, and ensure compliance with EU medical device regulations. The growing trend of smart hospitals and the integration of AI-driven diagnostic and therapeutic systems further support market expansion. Urbanization, technological awareness, and investments in digital health initiatives are fostering the adoption of automation across both public and private healthcare facilities. In addition, energy-efficient and eco-friendly medical devices are gaining traction in Europe, enhancing the appeal of automated solutions.

U.K. Medical Automation Market Insight

The U.K. medical automation market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the rising adoption of advanced hospital automation systems, digital health technologies, and robotics-assisted surgeries. Concerns regarding patient safety, efficiency, and the reduction of human error are driving the implementation of automated solutions in hospitals, diagnostic centers, and laboratories. The U.K.’s strong healthcare IT infrastructure, along with widespread adoption of connected devices and digital health platforms, continues to support market growth. In addition, government-backed initiatives promoting telehealth, AI-assisted diagnostics, and smart hospital projects are expected to further accelerate adoption. The emphasis on quality patient care and operational efficiency reinforces the growing reliance on medical automation technologies.

Germany Medical Automation Market Insight

The Germany medical automation market is expected to expand at a considerable CAGR during the forecast period, supported by the country’s focus on technological innovation, advanced healthcare infrastructure, and high-quality standards. Hospitals and research centers are increasingly adopting robotic surgical systems, automated laboratory testing, and pharmacy automation solutions to enhance efficiency and reduce clinical errors. The demand for eco-friendly and energy-efficient medical devices also contributes to the market growth. Integration of medical automation with hospital information systems and AI-enabled analytics platforms is becoming more common, enabling better workflow management. Germany’s emphasis on patient safety, precision diagnostics, and operational optimization drives the adoption of advanced automated solutions.

Asia-Pacific Medical Automation Market Insight

The Asia-Pacific medical automation market is poised to grow at the fastest CAGR during the forecast period, driven by increasing urbanization, rising healthcare expenditure, and the adoption of advanced medical technologies in countries such as China, Japan, and India. Hospitals, diagnostic centers, and specialty clinics are rapidly implementing automated diagnostic, therapeutic, and laboratory systems to improve efficiency and patient care. Government initiatives promoting digital healthcare and smart hospital infrastructure are further encouraging adoption. The growing presence of domestic manufacturers and cost-effective medical automation solutions enhances accessibility in emerging markets. Increasing awareness of patient safety, precision diagnostics, and operational efficiency are key factors propelling market growth in the region.

Japan Medical Automation Market Insight

The Japan medical automation market is gaining momentum due to the country’s high-tech healthcare ecosystem, aging population, and increasing focus on patient convenience and safety. Adoption of robotic-assisted surgeries, automated diagnostics, and telehealth solutions is driven by hospitals and clinics aiming to improve efficiency and reduce errors. Integration of automated systems with IoT-enabled devices, AI-driven analytics, and electronic health records enhances workflow optimization. Japan’s focus on smart hospital initiatives, technological innovation, and precision healthcare contributes to the growth of medical automation. The need for easier-to-use solutions for elderly patients further fuels demand in both residential care and clinical environments.

India Medical Automation Market Insight

The India medical automation market accounted for the largest market revenue share in Asia-Pacific in 2024, supported by rapid urbanization, growing middle-class population, and increasing technological adoption in healthcare facilities. Hospitals, diagnostic centers, and pharmacies are implementing automated solutions to enhance operational efficiency, improve patient care, and reduce manual errors. Government initiatives promoting digital health, telemedicine, and smart hospital infrastructure are accelerating adoption. The availability of cost-effective automation solutions from domestic manufacturers, coupled with rising awareness of patient safety and workflow optimization, is driving market growth. In addition, the expansion of private healthcare and multi-specialty hospitals contributes to the increasing deployment of medical automation systems across India.

Medical Automation Market Share

The medical automation industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Siemens Healthineers AG (Germany)

- Abbott (U.S.)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- BIOTRONIK SE & Co. KG (Germany)

- Terumo Corporation (Japan)

- Stryker (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Boston Scientific Corporation (U.S.)

- Zimmer Biomet (U.S.)

- Smith + Nephew (U.K.)

- AbbVie Inc. (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Beckman Coulter, Inc. (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- Canon Medical Systems Corporation (Japan)

- Mitsubishi Electric Corporation (Japan)

- Hitachi, Ltd. (Japan)

What are the Recent Developments in Global Medical Automation Market?

- In July 2025, THINK Surgical, an innovator in orthopedic surgical robots, announced the successful first use of a b-ONE Ortho Corporation's implant with its TMINI® Miniature Robotic System. This collaboration and milestone highlight the increasing trend of "open platforms" in surgical robotics, where the robotic system can be used with implants from multiple manufacturers, giving surgeons greater choice

- In June 2025, Johnson & Johnson MedTech announced the launch of a new fund to accelerate the development of artificial intelligence solutions in surgery. This initiative, in collaboration with companies such as NVIDIA and AWS, is designed to support promising AI innovations that address challenges in the operating room. This is a major corporate action that directly impacts the development of new medical automation technologies

- In December 2024, Canon Medical Systems USA introduced an AI-powered automation platform designed to streamline clinical workflows. This zero-click solution leverages deep learning technology to provide fast, actionable results, integrating seamlessly from scanner to clinical decision-making. The platform aims to enhance patient triage and treatment planning, empowering healthcare providers with precise tools to improve patient outcomes

- In March 2024, Capsa Healthcare, a leader in healthcare workflow solutions, officially announced the launch of its new NexPak Automated Packaging System. This system is designed to provide pharmacies with a flexible and scalable solution for automated medication packaging. The NexPak aims to improve medication adherence and streamline workflows in both institutional and retail pharmacies, a crucial development in the pharmacy automation sector

- In May 2021, Ricoh USA, Inc. received the 2021 MedTech Breakthrough Award for "Clinical Efficiency Innovation" for its eFax Referrals Solution. This solution revolutionizes the digital health and medical technology markets by expediting the referrals process, safeguarding sensitive patient information, and lowering administrative costs for medical providers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.