Global Medical Dressing Market

Market Size in USD Billion

USD

9.65 Billion

USD

15.04 Billion

2024

2032

USD

9.65 Billion

USD

15.04 Billion

2024

2032

| 2025 - 2032 | |

| USD 9.65 Billion | |

| USD 15.04 Billion | |

| % | |

|

Medical Dressing Market Size

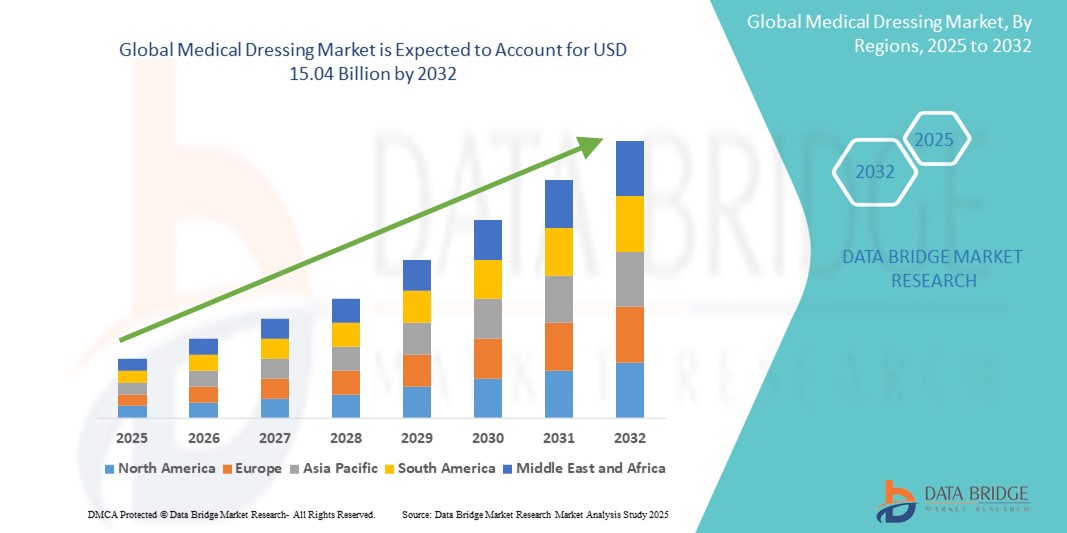

- The global medical dressing market size was valued at USD 9.65 billion in 2024 and is expected to reach USD 15.04 billion by 2032, at a CAGR of 5.71% during the forecast period

- The market growth is primarily driven by the increasing prevalence of chronic wounds, rising surgical procedures, and a growing aging population, all of which necessitate advanced wound care solutions

- In addition, technological advancements in dressing materials such as hydrocolloids, alginates, and foam dressings combined with rising awareness of infection prevention, are enhancing the demand for effective and patient-friendly dressing options. These trends are propelling the expansion of the medical dressing market globally

Medical Dressing Market Analysis

- Medical dressings, essential for wound protection, healing, and infection prevention, are critical components in both acute and chronic care settings, with applications spanning hospitals, home healthcare, and outpatient clinics due to their versatility and clinical effectiveness

- The rising demand for medical dressings is primarily driven by the increasing incidence of chronic wounds, diabetic ulcers, and surgical interventions, coupled with a growing focus on patient-centered care and advanced wound management solutions

- North America dominated the medical dressing market with the largest revenue share of 38.80% in 2024, supported by a well-established healthcare infrastructure, high healthcare expenditure, and the rapid adoption of technologically advanced wound care products across the U.S. and Canada

- Asia-Pacific is projected to be the fastest growing region in the medical dressing market during the forecast period, attributed to expanding healthcare access, rising geriatric population, and increased government focus on healthcare modernization

- The advanced wound dressing segment dominated the market with a share of 47.4% in 2024, driven by its superior healing capabilities, moisture retention properties, and growing preference among clinicians for managing complex wounds

Report Scope and Medical Dressing Market Segmentation

|

Attributes |

Medical Dressing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical Dressing Market Trends

“Technological Advancements in Advanced Wound Care Dressings”

- A key and rapidly evolving trend in the global medical dressing market is the development and adoption of advanced wound care dressings, which include hydrocolloid, hydrogel, foam, alginate, and antimicrobial dressings designed for enhanced healing and patient comfort

- For instance, companies such as Smith & Nephew and Mölnlycke Health Care are introducing dressings that incorporate silver ions or honey to reduce infection risk and accelerate tissue regeneration. Products such as Biatain Silicone with 3DFit Technology exemplify innovations aimed at better exudate management and conformability

- These advanced dressings not only help maintain a moist wound environment but also offer superior absorbency, reduced pain during dressing changes, and decreased healing time, especially beneficial in treating chronic wounds such as diabetic foot ulcers and pressure sores

- The use of smart dressings that integrate sensors to monitor wound conditions in real-time is also gaining traction. Some emerging dressings can detect infection by analyzing pH levels or temperature and can transmit data to healthcare providers, enabling timely interventions

- The increasing integration of evidence-based practices, nanotechnology, and biomaterials into dressing formulations is significantly raising clinician preference and patient outcomes. This shift is also contributing to reduced hospital stays and lower long-term healthcare costs

- As healthcare systems worldwide focus more on outpatient and home-based care, the demand for easy-to-use, comfortable, and high-performance dressings is rising. This trend is reshaping wound care strategies and driving substantial innovation in the medical dressing market

Medical Dressing Market Dynamics

Driver

“Rising Chronic Wounds and Surgical Interventions Fueling Demand”

- The growing global burden of chronic wounds, including diabetic foot ulcers, pressure ulcers, and venous leg ulcers driven by an aging population and rising diabetes prevalence—is a major factor boosting the demand for medical dressings

- For instance, the increasing number of surgical procedures worldwide, including post-operative wound management needs, is elevating the requirement for high-quality dressings that promote faster recovery and minimize complications

- In March 2024, 3M Health Care expanded its line of advanced wound care dressings, focusing on antimicrobial variants with improved moisture control, highlighting the industry's focus on innovation in response to clinical needs

- Furthermore, the shift toward home healthcare and outpatient treatment due to healthcare cost pressures and patient preferences is creating demand for easy-to-apply and longer-wear dressings that reduce the frequency of changes and hospital visits

- Improved patient awareness, coupled with rising healthcare spending and government initiatives in wound care management, particularly in aging populations and diabetic patients, are significantly propelling the growth of the medical dressing market

Restraint/Challenge

“Allergic Reactions and High Cost of Advanced Dressings”

- One of the key challenges hindering the wider adoption of certain advanced medical dressings is the potential for allergic reactions or skin irritation, particularly with dressings containing adhesives, latex, or antimicrobial agents such as iodine or silver

- For instance, patients with sensitive skin may experience contact dermatitis or delayed wound healing when exposed to some synthetic dressing components, leading to reluctance in their use and a preference for more basic alternatives

- In addition, the higher cost associated with advanced wound care dressings compared to traditional gauze or basic dressings poses a barrier, especially in cost-sensitive healthcare environments and developing markets

- While these products offer significant clinical benefits, their premium pricing can deter usage in public hospitals and by uninsured or underinsured patients. Reimbursement limitations in some regions further compound the accessibility issue

- Overcoming these challenges will require continued product innovations to reduce allergenic potential, increased availability of affordable advanced options, and broader insurance coverage or government support to improve adoption in economically constrained settings

Medical Dressing Market Scope

The market is segmented on the basis of type, application, and end user.

- By Type

On the basis of type, the global medical dressing market is segmented into advanced wound dressings and traditional wound dressings. The advanced wound dressings segment dominated the market with the largest revenue share of 47.4% in 2024, driven by increasing demand for moisture-retentive, antimicrobial, and tissue-regenerating dressings that enhance healing outcomes for chronic and acute wounds. These dressings are preferred in clinical settings due to their superior effectiveness in treating complex wounds such as diabetic ulcers, surgical incisions, and pressure injuries. Growing R&D activities and new product innovations from companies such as Smith & Nephew and 3M are further fueling the dominance of this segment.

The traditional wound dressings segment is expected to witness fastest growth during forecast period, including gauze and cotton-based products, continues to hold a significant share in developing regions due to cost-effectiveness and accessibility. However, its growth rate is comparatively slower due to the increasing shift toward evidence-based advanced wound care solutions globally.

- By Application

On the basis of application, the global medical dressing market is categorized into surgical wounds, ulcers, burns, and others. The surgical wounds segment led the market in 2024, supported by the rising volume of surgical procedures and post-operative care needs across hospitals and outpatient facilities. Medical dressings designed to manage exudate, protect against infections, and promote faster healing are in high demand for post-surgical applications.

The ulcers segment is anticipated to witness the fastest growth rate from 2025 to 2032, largely driven by the increasing prevalence of diabetes and the associated rise in diabetic foot ulcers and pressure ulcers. These chronic wounds require advanced dressings with extended wear times and antimicrobial features. The burns segment also shows steady growth, especially in emergency and trauma care units, where dressings that maintain a moist environment and offer pain relief are crucial.

- By End User

On the basis of end user, the global medical dressing market is divided into inpatient facilities and outpatient facilities. Inpatient facilities, including hospitals and long-term care centers, held the largest revenue share in 2024 due to the high volume of complex wound cases treated in these settings, necessitating frequent dressing changes and advanced wound care management.

Outpatient facilities are projected to grow at the fastest rate through 2032, driven by the global trend toward home-based care, cost containment, and the availability of user-friendly, ready-to-use dressing solutions. The rising geriatric population and increasing emphasis on decentralized healthcare delivery further support the growth of this segment.

Medical Dressing Market Regional Analysis

- North America dominated the medical dressing market with the largest revenue share of 38.80% in 2024, supported by a well-established healthcare infrastructure, high healthcare expenditure, and the rapid adoption of technologically advanced wound care products across the U.S. and Canada

- The region benefits from a well-developed healthcare infrastructure, high healthcare expenditure, and the presence of major industry players offering innovative dressing technologies

- Moreover, increasing awareness about wound management, favorable reimbursement policies, and a growing geriatric population contribute significantly to market growth. The widespread adoption of advanced wound dressings in both inpatient and outpatient settings has positioned North America as a key region in driving global market expansion

U.S. Medical Dressing Market Insight

The U.S. medical dressing market captured the largest revenue share of 79% in 2024 within North America, driven by a high incidence of chronic wounds, surgical procedures, and increasing demand for advanced wound care solutions. The presence of leading healthcare providers and strong reimbursement frameworks supports widespread adoption of both traditional and advanced dressings. Technological advancements in wound care materials, combined with a growing preference for outpatient and home-based treatment, are further propelling market growth. The aging population and rising diabetes rates continue to drive the need for high-performance wound dressings across diverse care settings.

Europe Medical Dressing Market Insight

The Europe medical dressing market is projected to grow at a substantial CAGR throughout the forecast period, supported by increasing surgical volumes, chronic wound cases, and healthcare modernization efforts across the region. The region’s stringent quality standards, coupled with a strong demand for evidence-based, patient-centric wound care, are boosting the adoption of advanced dressings. In addition, rising healthcare expenditures and greater awareness of infection prevention are promoting innovation and adoption in both public and private healthcare sectors. Countries such as Germany, France, and the U.K. are leading in product uptake.

U.K. Medical Dressing Market Insight

The U.K. medical dressing market is expected to grow at a noteworthy CAGR during the forecast period, fueled by an aging population and rising chronic disease burden, particularly diabetes and vascular conditions. National Health Service (NHS) initiatives focused on pressure ulcer prevention and home healthcare expansion are driving the demand for advanced wound dressings. The U.K.'s strong emphasis on clinical effectiveness and cost-efficiency is encouraging the adoption of high-quality, long-wear dressing solutions across hospitals and community care facilities.

Germany Medical Dressing Market Insight

The Germany medical dressing market is anticipated to expand at a considerable CAGR during the forecast period, supported by robust healthcare infrastructure, high healthcare expenditure, and increased investment in advanced wound care. German consumers and healthcare providers show strong preferences for clinically proven, innovative dressings that reduce hospital stays and improve patient outcomes. The market is also supported by a proactive stance on elderly care and post-surgical recovery solutions, where advanced dressings are widely implemented across both public and private facilities.

Asia-Pacific Medical Dressing Market Insight

The Asia-Pacific medical dressing market is projected to grow at the fastest CAGR of 23.5% during 2025 to 2032, driven by rising chronic disease prevalence, expanding healthcare access, and growing demand for modern wound care solutions. Rapid urbanization, aging demographics, and increasing awareness of wound management best practices are fostering greater adoption of both traditional and advanced dressings. The region's growth is further boosted by government-led healthcare initiatives, local manufacturing, and the affordability of innovative wound care products, especially in populous nations such as India and China.

Japan Medical Dressing Market Insight

The Japan medical dressing market is gaining momentum due to its aging population, rising surgical volume, and strong emphasis on infection control and post-acute care. Technological innovation in wound dressings, including hydrogel and antimicrobial variants, aligns well with Japan’s healthcare standards. The adoption of dressings integrated with smart monitoring capabilities is also gaining traction, driven by demand for improved home healthcare solutions. Japan’s established healthcare system and clinical precision further promote growth in advanced wound care adoption.

India Medical Dressing Market Insight

The India medical dressing market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by increasing diabetes cases, government investment in healthcare infrastructure, and a growing middle-class population. The push toward universal health coverage and smart city healthcare initiatives is enhancing access to modern wound care. Domestic manufacturers are expanding product availability, particularly of cost-effective advanced dressings, to meet rising demand across both urban and rural healthcare facilities. The growing home care sector and awareness campaigns around wound hygiene further contribute to India’s strong market performance.

Medical Dressing Market Share

The medical dressing industry is primarily led by well-established companies, including:

- 3M (U.S.)

- Smith+Nephew (U.K.)

- Mölnlycke AB (Sweden)

- ConvaTec Group Plc (U.K.)

- Coloplast A/S (Denmark)

- Paul Hartmann AG (Germany)

- Medline Industries, LP (U.S.)

- B. Braun SE (Germany)

- Johnson & Johnson Services, Inc. (U.S.)

- Derma Sciences, Inc. (U.S.)

- Lohmann & Rauscher GmbH & Co. KG (Germany)

- Nitto Denko Corporation (Japan)

- Hollister Incorporated (U.S.)

- Winner Medical Co., Ltd. (China)

- Advancis Medical (U.K.)

- BSN medical GmbH (Germany)

- Cardinal Health, Inc. (U.S.)

- DeRoyal Industries, Inc. (U.S.)

- AMERX Health Care Corporation (U.S.)

- Medtronic (Ireland)

What are the Recent Developments in Global Medical Dressing Market?

- In April 2023, 3M Health Care announced the launch of its 3M Tegaderm Antimicrobial Film Dressing with CHG, aimed at improving infection prevention in catheter-related procedures. This next-generation dressing combines transparent film with chlorhexidine gluconate (CHG), offering extended antimicrobial protection while allowing visibility of the insertion site. The launch reflects 3M's focus on developing innovative wound care solutions that enhance patient safety and clinical outcomes in both inpatient and outpatient settings

- In March 2023, Mölnlycke Health Care expanded its Mepilex range by introducing Mepilex Border Comfort, a dressing designed for enhanced absorbency and patient comfort. This product incorporates Mölnlycke’s proprietary Flex Technology, enabling it to conform better to challenging body contours while maintaining secure adhesion. The development supports the company's commitment to providing advanced dressings tailored for complex wounds, especially in post-operative and chronic care settings

- In February 2023, Smith+Nephew launched the PICO 7Y Single Use Negative Pressure Wound Therapy System with AIRLOCK Technology, addressing the growing demand for portable wound care solutions. Designed for high-risk surgical incisions and chronic wounds, the system enhances fluid management and minimizes the risk of surgical site complications. This innovation signifies Smith+Nephew’s ongoing efforts to integrate advanced technology into wound healing, particularly in ambulatory and home care market

- In February 2023, Coloplast A/S announced a strategic collaboration with the Danish Wound Healing Society to support clinical research and education on modern wound care. This initiative includes funding clinical trials, hosting workshops, and developing evidence-based guidelines on the use of advanced medical dressings. The partnership reflects Coloplast’s commitment to advancing wound care through clinician education and product innovation, reinforcing its position in the European market

- In January 2023, ConvaTec Group Plc introduced AQUACEL Ag+ Extra, an advanced antimicrobial dressing designed to combat biofilm and support faster healing in infected wounds. This next-gen dressing builds on ConvaTec’s Hydrofiber Technology and is particularly suited for treating pressure ulcers, diabetic foot ulcers, and venous leg ulcers. The launch underscores ConvaTec’s emphasis on clinically effective, infection-fighting solutions in the growing chronic wound segment

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.