Global Medical Grade Silicone Implant Curing Oven Systems Market

Market Size in USD Million

USD

65.00 Million

USD

183.73 Million

2024

2032

USD

65.00 Million

USD

183.73 Million

2024

2032

| 2025 - 2032 | |

| USD 65.00 Million | |

| USD 183.73 Million | |

| % | |

|

Medical-Grade Silicone Implant Curing Oven Systems Market Size

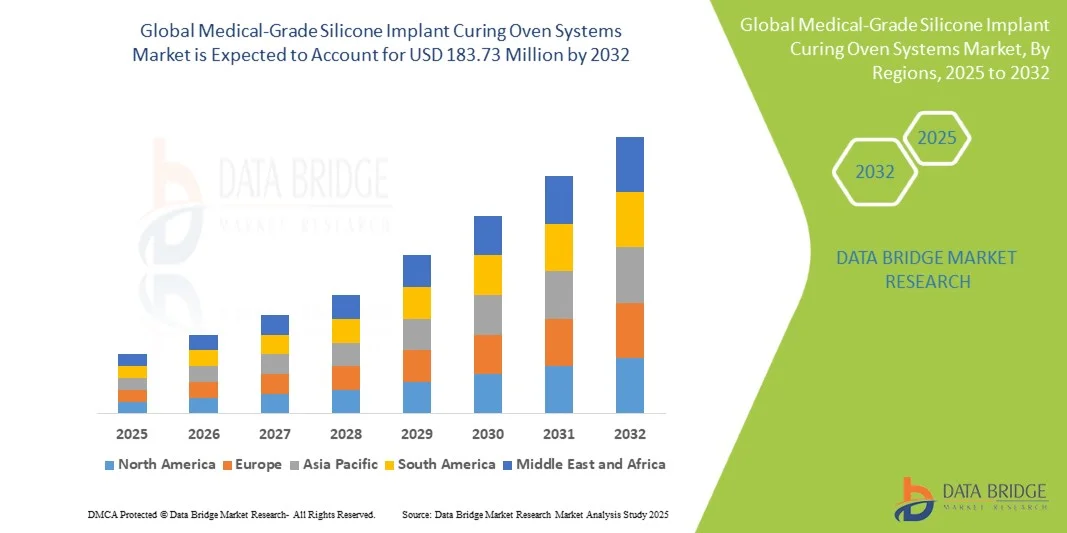

- The global medical-grade silicone implant curing oven systems market size was valued at USD 65.00 million in 2024 and is expected to reach USD 183.73 million by 2032, at a CAGR of 13.87% during the forecast period

- The market growth is largely fueled by the increasing adoption and technological advancements in medical device manufacturing, particularly in implant production, where precision curing processes are critical for ensuring safety and performance

- Furthermore, rising demand for secure, efficient, and reliable curing systems in both healthcare and medical device industries is positioning Medical-Grade Silicone Implant Curing Oven Systems as the preferred choice for implant manufacturing. These converging factors are accelerating the uptake of Medical-Grade Silicone Implant Curing Oven Systems solutions, thereby significantly boosting the industry’s growth

Medical-Grade Silicone Implant Curing Oven Systems Market Analysis

- Medical-Grade Silicone Implant Curing Oven Systems, designed to ensure precise temperature control and uniform curing of silicone implants, are becoming increasingly vital in healthcare and medical device manufacturing due to their enhanced reliability, efficiency, and compliance with stringent regulatory standards. Their integration into modern production processes supports consistent quality, reduces errors, and improves patient safety outcomes

- The escalating demand for medical-grade silicone implant curing oven systems is primarily fueled by the rising number of cosmetic and reconstructive surgeries, increasing awareness of medical-grade implants, and the growing emphasis on manufacturing precision in the healthcare sector. Advancements in automation, AI-based monitoring, and energy-efficient oven technologies are further driving adoption among manufacturers

- North America dominated the medical-grade silicone implant curing oven systems market with the largest revenue share of 38.7% in 2024, characterized by the presence of advanced healthcare infrastructure, high demand for silicone-based implants, and strong regulatory frameworks that emphasize product quality and safety. The U.S. contributed the most significant portion of this growth, driven by increasing adoption of technologically advanced curing ovens by medical device companies and innovations introduced by both established manufacturers and emerging players

- Asia-Pacific is expected to be the fastest growing region in the medical-grade silicone implant curing oven systems market during the forecast period, projected to expand at a CAGR of 10.8%, owing to rapid urbanization, improving healthcare infrastructure, rising disposable incomes, and increasing investments by global medical device companies in countries such as China, India, and South Korea

- The Electric Heating segment dominated the medical-grade silicone implant curing oven systems market with a market share of 45.1% in 2024, driven by precise temperature control, energy efficiency, and compatibility with batch and pilot-scale ovens

Report Scope and Medical-Grade Silicone Implant Curing Oven Systems Market Segmentation

|

Attributes |

Medical-Grade Silicone Implant Curing Oven Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Medical-Grade Silicone Implant Curing Oven Systems Market Trends

“AI-Driven Automation and Precision in Medical-Grade Silicone Implant Curing Oven Systems”

- A significant and accelerating trend in the global medical-grade silicone implant curing oven systems market is the integration of artificial intelligence (AI) and advanced automation controls to enhance precision, efficiency, and usability. These technologies allow manufacturers and healthcare facilities to achieve better process consistency, reduced human error, and optimized curing cycles for implants

- For instance, next-generation curing oven systems now incorporate AI-driven temperature monitoring and adaptive cycle adjustments, which automatically calibrate based on implant material properties. This ensures consistent curing quality while reducing operator intervention

- AI integration also allows predictive maintenance by analyzing operational data and detecting potential issues before breakdowns occur, thereby reducing downtime and operational costs. Furthermore, hands-free and touchless interfaces are being developed to enhance user convenience, especially in sterile environments where manual handling needs to be minimized

- The seamless integration of these ovens with broader digital health manufacturing ecosystems enables centralized monitoring of curing processes, production workflows, and compliance reporting. Through a single interface, operators can manage oven systems alongside other equipment, fostering efficiency and quality assurance

- This trend toward more intelligent and intuitive oven systems is fundamentally transforming manufacturing processes in the medical device sector. Consequently, companies are investing in R&D to develop AI-enabled curing ovens with automated control cycles, energy optimization, and real-time analytics

- The demand for advanced Medical-Grade Silicone Implant Curing Oven Systems that combine AI-driven intelligence and user-friendly interfaces is rapidly increasing across hospitals, specialty clinics, and implant manufacturers, as stakeholders prioritize efficiency, precision, and regulatory compliance

Medical-Grade Silicone Implant Curing Oven Systems Market Dynamics

Driver

“Rising Demand for Precision and Compliance in Implant Manufacturing”

- The increasing demand for medical-grade silicone implants across applications such as reconstructive surgery, orthopedics, and aesthetics is driving the adoption of advanced curing oven systems. The need for consistent quality, sterility, and precision in implant manufacturing makes these systems indispensable

- For instance, in March 2024, a leading medical device manufacturer launched an AI-powered curing oven designed to optimize energy consumption while ensuring uniform curing of silicone implants, marking a step forward in process automation

- As regulatory bodies impose stricter requirements on device safety and performance, manufacturers are relying on advanced oven systems to meet compliance standards while ensuring product reliability

- In addition, the rising demand for minimally invasive procedures and the surge in elective surgeries are pushing manufacturers to scale up production capacities, further fueling the need for efficient curing solutions

- The integration of digital controls, remote monitoring capabilities, and automated cycle adjustments further positions these ovens as vital equipment for next-generation medical device manufacturing

Restraint/Challenge

“High Capital Investment and Technical Complexity Hindering Adoption”

- One of the major challenges in the medical-grade silicone implant curing oven systems market is the high upfront cost associated with advanced AI-integrated systems. Smaller manufacturers or budget-constrained healthcare facilities may find it difficult to justify the investment compared to traditional curing methods

- For instance, premium systems with built-in analytics, automated quality checks, and predictive maintenance features often require substantial capital expenditure, limiting adoption among mid-tier manufacturers

- Furthermore, the complexity of installation, calibration, and operator training for these systems can act as a barrier, particularly in regions with limited access to skilled technical staff

- Concerns regarding integration with existing manufacturing systems and compliance documentation further add to the hesitancy in adoption

- While the long-term benefits such as reduced operational costs, improved implant safety, and regulatory compliance outweigh initial barriers, the perceived complexity and cost continue to restrict widespread adoption

- Overcoming these challenges through cost-optimized models, simplified user interfaces, and awareness programs highlighting the benefits of advanced curing ovens will be crucial for market penetration, especially in emerging markets

Medical-Grade Silicone Implant Curing Oven Systems Market Scope

The market is segmented on the basis of type, capacity, heating method, application, and end-user.

• By Type

On the basis of type, the medical-grade silicone implant curing oven systems market is segmented into batch curing ovens, continuous/conveyor curing ovens, vacuum curing ovens, high-temperature/pressure curing ovens, and others. The batch curing ovens segment dominated the largest market revenue share of 42.5% in 2024, driven by its versatility in handling small-to-medium implant production batches and precise temperature control. These ovens are widely adopted in research laboratories, pilot production, and specialty implant manufacturing due to their ability to maintain consistent product quality. Batch ovens allow for process flexibility, modularity, and easy integration into existing production lines. Their compatibility with multiple implant types, including breast and orthopedic implants, strengthens their market position. The segment benefits from established operational familiarity among technicians and low maintenance requirements. Batch ovens also support high reproducibility and compliance with medical manufacturing standards. Their use in both small-scale production and clinical research enhances their applicability. Demand from regions with high cosmetic and reconstructive surgery volumes further consolidates market dominance. Strong adoption by implant manufacturers ensures steady revenue generation and growth stability.

The Continuous/Conveyor Curing Ovens segment is expected to witness the fastest CAGR of 20.8% from 2025 to 2032, driven by the rising need for high-throughput industrial-scale implant production. Continuous ovens offer automated handling, reduced labor, and uniform heating, ideal for large-volume manufacturing. Technological advancements in conveyor design, energy efficiency, and process monitoring boost adoption. Manufacturers investing in continuous ovens benefit from faster production cycles and lower operational costs. The segment is increasingly preferred for standardized breast, orthopedic, and dental implants. Continuous curing ensures uniformity, minimizes errors, and meets strict regulatory standards. Its ability to integrate with automated production lines makes it attractive for OEMs and contract manufacturers. Rising global demand for implants drives adoption in emerging markets. Large manufacturers are implementing continuous ovens to optimize productivity and reduce manual interventions. Overall, the segment represents rapid growth potential across industrial implant manufacturing.

• By Capacity

On the basis of capacity, the medical-grade silicone implant curing oven systems market is segmented into small scale/lab-scale, medium scale/pilot manufacturing, and high volume/industrial Scale. The Medium Scale/Pilot Manufacturing segment held the largest market revenue share of 39.6% in 2024, favored for bridging research-scale and industrial-scale operations. This capacity enables process optimization, quality validation, and flexibility for custom implant production. Medium-scale systems are widely adopted for pilot studies, clinical trial materials, and specialty implants. Manufacturers benefit from modular design and adaptability to multiple implant types. These systems reduce material wastage while ensuring compliance with medical standards. Their versatility allows use in both research labs and small production facilities. Process reproducibility and consistent curing quality strengthen market leadership. The segment supports early-stage commercialization and product testing. Moderate investment requirements and manageable operational complexity enhance adoption. Medium-scale ovens provide a balance between throughput, flexibility, and quality control, making them a preferred choice for implant producers.

The High Volume/Industrial Scale segment is expected to register the fastest CAGR of 22.3% from 2025 to 2032, fueled by increasing global implant demand and large-scale production requirements. High-volume ovens provide fully automated, high-throughput processing and reduce cycle times. Adoption is driven by large implant manufacturers and OEMs focusing on efficiency and cost optimization. These systems integrate with continuous or conveyor ovens for industrial-scale output. Industrial-scale ovens ensure consistent curing for mass production of breast, orthopedic, and dental implants. Advanced monitoring and process control improve quality assurance. The segment benefits from rising outsourcing trends and contract manufacturing collaborations. Energy-efficient designs reduce operational costs, enhancing profitability. Growing demand in North America, Europe, and Asia-Pacific supports rapid adoption. The segment represents high growth potential in emerging markets and industrial implant manufacturing facilities.

• By Heating Method

On the basis of heating method, the medical-grade silicone implant curing oven systems market is segmented into electric heating, infrared heating, steam heating, gas heating, and others. The Electric Heating segment dominated with a market share of 45.1% in 2024, driven by precise temperature control, energy efficiency, and compatibility with batch and pilot-scale ovens. Electric heating ensures uniform curing and reduces material defects. Adoption is supported by its reliability, safety, and regulatory compliance. It is widely preferred in both research laboratories and manufacturing plants. Electric ovens facilitate automation and digital control, improving productivity and repeatability. Manufacturers benefit from lower maintenance costs and enhanced energy management. The segment supports diverse implant types, including breast, orthopedic, and dental implants. Integration with monitoring systems enables real-time process control. The established familiarity among technicians and regulatory acceptance further reinforces its market dominance.

The Infrared Heating segment is expected to witness the fastest CAGR of 21.5% from 2025 to 2032, driven by rapid heating cycles, energy savings, and uniform curing results. Infrared ovens are particularly useful for sensitive silicone materials and complex implant geometries. Adoption is increasing in pilot-scale and high-volume production facilities. Enhanced process control and precision reduce defects and improve product quality. Manufacturers favor infrared heating for its speed and reduced thermal gradients. Integration with conveyor or continuous systems accelerates industrial adoption. The segment also benefits from growing demand for custom and high-value implants. Infrared technology is increasingly used in orthopedic and facial implant production. Lower energy consumption and shorter curing times support cost efficiency. Overall, this segment represents rapid adoption potential in both research and manufacturing environments.

• By Application

On the basis of application, the medical-grade silicone implant curing oven systems market is segmented into breast implants, facial implants, dental implants, orthopedic implants, and others. The Breast Implants segment held the largest market revenue share of 40.8% in 2024, driven by high global demand for reconstructive and cosmetic surgeries. Batch curing ovens are widely used to ensure precise, consistent, and safe curing of medical-grade silicone. Breast implants require strict quality standards, regulatory compliance, and reproducibility, supporting the segment’s dominance. Manufacturers prioritize consistent temperature control and process reliability. Adoption is fueled by increasing cosmetic surgery rates in North America, Europe, and Asia-Pacific. Market growth is supported by well-established implant manufacturers and OEMs. Breast implants often use medium-scale and batch ovens to balance flexibility and production efficiency. The segment benefits from technological advancements in curing ovens and enhanced process monitoring. Manufacturers are investing in capacity expansion to meet rising demand. Stringent regulatory standards and quality assurance requirements reinforce the segment’s leadership.

The Orthopedic Implants segment is expected to register the fastest CAGR of 19.9% from 2025 to 2032, driven by increasing orthopedic procedures, rising prevalence of musculoskeletal disorders, and demand for precision implants. Industrial-scale curing ovens are being adopted for high-throughput orthopedic implant production. Automated and infrared ovens support uniform silicone curing for complex implant shapes. Growth is also supported by expansion of implant OEMs and contract manufacturing partnerships. Orthopedic implants require stringent process monitoring to ensure patient safety. The segment benefits from technological innovations in curing systems. Adoption is increasing across emerging markets with rising healthcare expenditure. Manufacturers focus on reducing defects and enhancing operational efficiency. Overall, this segment represents rapid growth potential in global medical-grade silicone implant production.

• By End-User

On the basis of end-user, the medical-grade silicone implant curing oven systems market is segmented into Implant Manufacturers/OEMs, Medical Device Contract Manufacturers, Research Laboratories, and Academic & Research Institutes. The Implant Manufacturers/OEMs segment dominated with a 44.7% share in 2024, owing to high production volumes, stringent quality standards, and regulatory compliance. These end-users require reliable curing systems for consistent implant manufacturing. They benefit from batch and medium-scale ovens that balance throughput with flexibility. Adoption is driven by high demand for breast, orthopedic, and facial implants. Established relationships with equipment suppliers ensure timely upgrades and maintenance. The segment supports both pilot and industrial-scale production. Manufacturers prioritize energy efficiency, automation, and process reliability. OEMs leverage advanced curing systems to enhance operational efficiency and reduce costs. High adoption rates in North America, Europe, and Asia-Pacific reinforce market leadership.

The Medical Device Contract Manufacturers segment is expected to witness the fastest CAGR of 21.0% from 2025 to 2032, driven by increasing outsourcing of implant production, diverse client requirements, and demand for flexible curing solutions. Contract manufacturers leverage continuous and high-volume ovens to meet multiple client specifications. The segment benefits from advanced monitoring and automation systems that improve quality control. Rising global demand for implants encourages contract manufacturers to invest in scalable, energy-efficient curing ovens. Adoption is increasing in both emerging and developed markets. The segment is critical for OEMs seeking cost-effective, high-quality production. Focus on precision and compliance with medical standards supports rapid growth. Overall, this segment represents strong potential in the global market.

Medical-Grade Silicone Implant Curing Oven Systems Market Regional Analysis

- North America dominated the medical-grade silicone implant curing oven systems market with the largest revenue share of 38.7% in 2024, driven by advanced healthcare infrastructure, stringent regulatory frameworks, and a strong presence of key industry players

- The region’s medical device manufacturers are increasingly adopting technologically advanced curing ovens to ensure precision, consistency, and compliance in implant production. The market captured the majority of this growth, fueled by investments in innovative oven technologies, automation, and process optimization

- The focus on maintaining high-quality standards and enhancing operational efficiency continues to drive market expansion across hospitals, specialty clinics, and implant manufacturers

U.S. Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The U.S. medical-grade silicone implant curing oven systems market captured the largest revenue share within North America, accounting the regional market in 2024. This growth is driven by the country’s advanced healthcare infrastructure, high demand for silicone-based implants, and the adoption of technologically advanced curing oven systems by medical device manufacturers. Companies are increasingly investing in AI-enabled and automated ovens to improve precision, consistency, and operational efficiency in implant production. The rising number of elective and reconstructive surgeries, coupled with stringent regulatory standards for quality and safety, further supports market expansion. In addition, U.S.-based manufacturers are introducing innovative features such as predictive maintenance, digital monitoring, and energy-efficient operations, which are accelerating the adoption of curing oven systems across hospitals, specialty clinics, and medical device production facilities.

Europe Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The Europe medical-grade silicone implant curing oven systems market is projected to expand at a substantial CAGR throughout the forecast period, supported by the growing demand for precision, quality assurance, and compliance in medical-grade implant manufacturing. Countries such as Germany, France, and the U.K. are witnessing significant adoption of advanced curing ovens in both established medical device facilities and new manufacturing setups. Europe’s well-developed infrastructure, emphasis on regulatory compliance, and focus on technological innovation are driving the integration of automated curing solutions across hospitals and production units. The increasing prevalence of elective and reconstructive surgeries further fuels demand in residential and commercial medical manufacturing applications.

U.K. Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The U.K. medical-grade silicone implant curing oven systems market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by rising investments in healthcare technology and precision manufacturing solutions. The demand is driven by hospitals and medical device companies seeking high-quality, reproducible curing processes for silicone implants. In addition, regulatory compliance requirements, increasing adoption of automated production systems, and the need for operational efficiency are contributing to growth. The U.K.’s robust healthcare infrastructure and strong focus on research and innovation further bolster the market.

Germany Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The Germany medical-grade silicone implant curing oven systems market is expected to expand at a considerable CAGR during the forecast period, fueled by a combination of strong industrial infrastructure, emphasis on technological innovation, and sustainability-focused production practices. Advanced curing ovens are increasingly adopted in medical device manufacturing for their precision, energy efficiency, and ability to maintain consistent product quality. The country’s regulatory environment, coupled with a focus on process automation and high-quality standards, supports continued adoption of these systems in both commercial and specialty manufacturing units.

Asia-Pacific Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The Asia-Pacific medical-grade silicone implant curing oven systems market is projected to be the fastest-growing region, with a CAGR of 10.8% from 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and ongoing expansion of healthcare infrastructure. Countries such as China, India, and South Korea are seeing increasing investments from global medical device manufacturers and local companies to meet growing demand for silicone implants. The rise in elective and reconstructive surgeries, coupled with improvements in manufacturing technology and regulatory standards, is propelling market growth. Asia-Pacific is also emerging as a manufacturing hub for curing oven systems, facilitating wider availability and adoption across the region.

Japan Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The Japan medical-grade silicone implant curing oven systems market is gaining momentum due to its high-tech manufacturing environment, emphasis on quality, and growing demand for medical-grade silicone implants. Advanced curing ovens are widely adopted in hospitals and implant production facilities to ensure precision, reproducibility, and regulatory compliance. Increasing surgical procedures, coupled with technological advancements in production equipment, are contributing to market expansion.

China Medical-Grade Silicone Implant Curing Oven Systems Market Insight

The China medical-grade silicone implant curing oven systems market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to its expanding healthcare sector, growing middle class, and increasing adoption of advanced medical technologies. The demand for silicone implants is rising, driving investments in precise curing oven systems to maintain quality and consistency. Strong domestic manufacturing capabilities, coupled with government initiatives supporting medical device innovation, are key factors fueling the country’s market growth.

Medical-Grade Silicone Implant Curing Oven Systems Market Share

The medical-grade silicone implant curing oven systems industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Carbolite Gero Ltd. (U.K.)

- Nabertherm GmbH (Germany)

- Despatch Industries (U.S.)

- Thermal Product Solutions (U.S.)

- Wisconsin Oven Corporation (U.S.)

- Blue M (U.S.)

- Sheffield Hi-Tech Refractories (Germany)

- Memmert GmbH + Co.KG (Germany)

- LEWCO, Inc. (U.S.)

- BINDER GmbH (Germany)

Latest Developments in Global Medical-Grade Silicone Implant Curing Oven Systems Market

- In March 2025, Extreme Molding, a U.S.-based manufacturer specializing in medical-grade silicone molding, highlighted the integration of automation, predictive maintenance, and sustainability in its operations. This approach aims to enhance the efficiency and environmental responsibility of silicone molding processes, aligning with industry trends toward smarter and more sustainable manufacturing practices

- In February 2025, Thermal Product Solutions (TPS) shipped a custom Gruenberg oven to a medical device manufacturer. The oven was designed to cure and sterilize silicone breast implants in various sizes and shapes, maximizing the customer's production efficiency

- In September 2025, SiliconePlus.net published expert predictions on the future of medical-grade silicone, emphasizing the material's role in driving safer devices and efficient healthcare growth beyond 2025. The article discusses how technological innovations and regulatory advancements are shaping the use of medical-grade silicone in healthcare applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.