Global Medical Laser Systems Market

Market Size in USD Billion

USD

5.08 Billion

USD

7.64 Billion

2025

2033

USD

5.08 Billion

USD

7.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.08 Billion | |

| USD 7.64 Billion | |

| % | |

|

Medical Laser Systems Market Overview

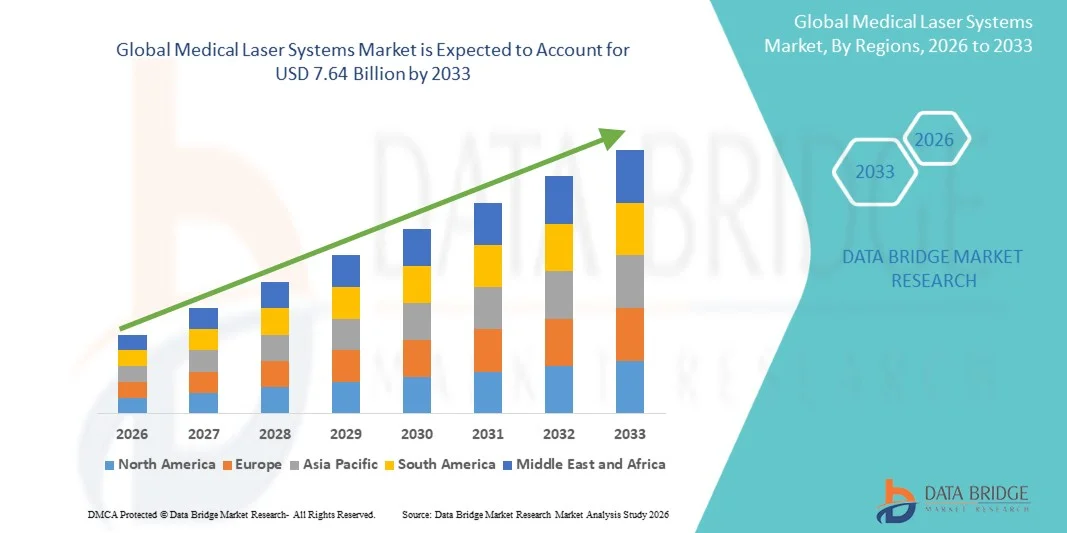

The Medical Laser Systems Market was valued at USD 5.08 billion in 2025 and is projected to reach USD 7.64 billion by 2033, growing at a CAGR of 5.25% from 2026 to 2033. The Medical Laser Systems Market is experiencing steady growth driven by rising demand for minimally invasive surgical procedures, increasing preference for precision-based treatment technologies, and continuous advancements in laser device performance across dermatology, ophthalmology, oncology, and cosmetic surgery applications. Growing adoption of laser-based systems in both therapeutic and aesthetic procedures is further accelerating market expansion, supported by improved patient outcomes, reduced recovery time, and lower risk of complications compared to traditional surgical methods.

The increasing prevalence of chronic diseases, including cancer, cardiovascular disorders, and ophthalmic conditions such as cataracts and diabetic retinopathy, is significantly boosting demand for medical laser systems across hospitals, specialty clinics, and ambulatory surgical centers. In addition, rising aesthetic consciousness and growing demand for cosmetic procedures such as skin resurfacing, hair removal, tattoo removal, and anti-aging treatments are further strengthening market penetration. Expanding healthcare infrastructure in emerging economies, along with growing investments in advanced surgical technologies and outpatient care facilities, is also encouraging wider adoption of laser-based medical devices globally.

Key Market Trends & Insights

- North America dominated the Medical Laser Systems Market with the largest revenue share of 36% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong investment in medical technology innovation.

- The Diode Lasers segment dominated the market with a share of 42.18% in 2025, owing to their compact design, cost-effectiveness, high energy efficiency, and wide clinical applicability across dermatology, dentistry, ophthalmology, and minor surgical procedures.

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, fueled by expanding healthcare infrastructure, rising patient awareness, and increasing adoption of advanced laser-based medical treatments in countries such as China and India.

- The Dermatology segment led the market by application, owing to rising demand for aesthetic procedures such as skin resurfacing, hair removal, and treatment of vascular and pigmented lesions using laser-based therapies.

- The Ophthalmology segment also held a significant share, supported by increasing prevalence of vision disorders and growing adoption of laser-assisted refractive and retinal procedures.

- The Gynecology application segment is witnessing strong growth, driven by increasing use of laser systems for minimally invasive treatments such as endometriosis management and cervical lesion procedures.

- Gas and solid-state lasers continue to play a key supporting role in specialized procedures, while technological advancements in precision targeting and safety systems are expanding their use across complex surgical applications.

Market Size & Forecast

- Global Market Value (2025): USD 5.08 Billion

- Expected Market Value (2033): USD 7.64 Billion

- Forecast CAGR (2026–2033): 5.25%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Medical Laser Systems Market Segmentation

|

Attributes |

Medical Laser Systems Key Market Insights |

|

Segments Covered |

· By Product: Diode Lasers, Solid State (Crystal) Lasers, Gas Lasers, and Dye Lasers · By Application: Dermatology, Ophthalmology, Gynecology, Urology, Dentistry, Cardiology, Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Lumenis Ltd. (Israel) |

|

Market Opportunities |

· Rising demand for minimally invasive aesthetic and dermatology procedures · Expansion of ophthalmic laser applications in aging populations · Technological advancements in AI-integrated and portable laser systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Medical Laser Systems Market Trends

Trend: Growth in Minimally Invasive Aesthetic & Surgical Procedures

The rising global preference for minimally invasive treatments is significantly accelerating the adoption of medical laser systems across dermatology, ophthalmology, and cosmetic surgery. Patients are increasingly opting for laser-based procedures such as skin resurfacing, tattoo removal, hair reduction, LASIK vision correction, and vascular lesion treatment due to reduced recovery time, lower risk of complications, and improved clinical outcomes. Clinics and hospitals are rapidly expanding their laser treatment portfolios, with diode and solid-state laser systems gaining strong traction due to their precision, efficiency, and adaptability across multiple indications. For instance, according to clinical adoption trends reported in dermatology practices across North America and Europe, laser-based aesthetic procedures have grown consistently over the past few years, supported by rising disposable income and medical tourism in cosmetic treatments.

Medical Laser Systems Market Dynamics

Key Market Driver: Rising Prevalence of Chronic Diseases and Ophthalmic Disorders

The increasing global burden of chronic diseases such as diabetes, cardiovascular conditions, and age-related vision disorders is driving strong demand for medical laser systems, particularly in ophthalmology and surgical applications. Conditions like diabetic retinopathy, glaucoma, and cataracts are becoming more prevalent with aging populations; for instance, the International Diabetes Federation (IDF) estimates that over 530 million adults globally are living with diabetes, a key risk factor for laser-treated retinal diseases. As a result, hospitals and specialty eye care centers are increasingly deploying laser-assisted procedures such as photocoagulation, LASIK, and selective laser trabeculoplasty. Medical laser systems are also being integrated into cardiology and urology applications, where minimally invasive laser-based interventions help reduce hospital stay duration and improve procedural accuracy, further strengthening market expansion.

Key Restraint/Challenge: High Capital Cost and Regulatory Compliance Burden

Despite strong clinical advantages, the high cost of advanced medical laser systems remains a major barrier to widespread adoption, particularly in small clinics and developing healthcare systems. Premium laser platforms integrated with imaging guidance, robotic precision systems, and multi-wavelength capabilities can require significant upfront investment along with recurring costs for maintenance, consumables, and operator training. In addition, stringent regulatory approvals from bodies such as the U.S. FDA and European CE authorities add complexity and time to product commercialization. For instance, high-end surgical laser systems used in oncology and ophthalmology often undergo multi-phase clinical validation before approval, extending time-to-market and increasing R&D costs. This limits accessibility for mid-tier healthcare providers, especially in cost-sensitive regions such as parts of Asia-Pacific, Africa, and Latin America.

Key Market Opportunity: Expansion of AI-Integrated and Image-Guided Laser Systems

The integration of artificial intelligence, robotics, and advanced imaging technologies into medical laser systems presents a major growth opportunity for the market. AI-enabled platforms are increasingly being used to enhance treatment precision, automate parameter settings, and provide real-time tissue recognition during surgical procedures. For instance, ophthalmic laser systems are now incorporating AI-based diagnostic imaging to improve accuracy in retinal disease treatment planning, while dermatology platforms use machine learning algorithms to customize energy delivery based on skin type and condition. In addition, the development of smart operating rooms and digitally connected healthcare ecosystems is enabling seamless integration of laser devices with hospital information systems. Growing adoption of cloud-based surgical analytics and remote treatment planning in technologically advanced healthcare centers across North America and Europe is further expected to drive next-generation innovation and market expansion.

Medical Laser Systems Market Scope

The Medical Laser Systems market is segmented on the basis of product and application.

- By Product

On the basis of product, the Medical Laser Systems Market is segmented into diode lasers, solid state (crystal) lasers, gas lasers, and dye lasers. The Diode Lasers segment dominated the market with a share of 42.18% in 2025, owing to their compact design, cost-effectiveness, high energy efficiency, and wide clinical applicability across dermatology, dentistry, ophthalmology, and minor surgical procedures. Their ease of integration into portable and outpatient systems has further strengthened adoption across hospitals and specialty clinics. In addition, continuous technological advancements in wavelength precision and cooling efficiency are enhancing treatment accuracy and patient safety, further reinforcing segment dominance across global healthcare settings.

The Solid State (Crystal) Lasers segment is expected to witness the fastest CAGR of 6.7% from 2026 to 2033, driven by increasing demand for high-power surgical applications and precision-based treatments in oncology and ophthalmology. These lasers offer superior beam quality and deeper tissue penetration, making them suitable for complex procedures requiring high accuracy. Rising investments in advanced surgical infrastructure across developed economies, along with expanding use in minimally invasive surgeries, are accelerating segment growth. Moreover, ongoing innovation in crystal materials and energy efficiency is improving clinical outcomes, supporting wider adoption in hospitals and specialty surgical centers.

- By Application

On the basis of application, the Medical Laser Systems Market is segmented into dermatology, ophthalmology, gynecology, urology, dentistry, cardiology, and others. The Dermatology segment dominated the market with a share of 34.92% in 2025, driven by increasing demand for aesthetic procedures such as skin resurfacing, acne scar removal, tattoo removal, pigmentation correction, and hair reduction treatments. Growing consumer preference for non-invasive cosmetic procedures, along with rising disposable income and medical tourism in aesthetic dermatology, is significantly boosting adoption. In addition, the widespread availability of advanced diode and CO₂ laser systems in dermatology clinics and aesthetic centers is further supporting segment dominance globally.

The Ophthalmology segment is projected to register the fastest CAGR of 7.1% from 2026 to 2033, fueled by the rising global prevalence of vision disorders such as cataracts, glaucoma, diabetic retinopathy, and refractive errors. Increasing adoption of laser-assisted surgeries like LASIK, photocoagulation, and retinal therapy is driving strong growth in this segment. Aging populations, particularly in North America, Europe, and parts of Asia-Pacific, are further increasing demand for advanced ophthalmic laser treatments. Moreover, continuous innovation in precision laser systems and image-guided surgical technologies is improving clinical outcomes, making ophthalmology one of the fastest-expanding application areas in the global market.

Medical Laser Systems Market Regional Analysis

North America dominated the Medical Laser Systems Market and accounted for the largest revenue share of 36% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive laser-based procedures, strong investments in medical technology innovation, and the presence of established hospitals, specialty clinics, and research institutions. The region also benefits from stringent regulatory standards, high procedural volumes across dermatology, ophthalmology, dentistry, and cosmetic surgery, and growing adoption of AI- and image-guided laser systems. Increasing focus on precision treatment outcomes and advanced surgical technologies continues to strengthen North America’s leadership position in the global market.

U.S. Medical Laser Systems Market Insight

The U.S. Medical Laser Systems market is witnessing strong growth due to rising investments in advanced medical treatment technologies, increasing prevalence of chronic diseases, and expanding adoption of laser-based minimally invasive procedures across healthcare facilities. The country’s mature healthcare ecosystem, along with strong penetration of AI-powered diagnostic and surgical laser systems, is driving demand across dermatology, ophthalmology, oncology, and dental applications. In addition, growing emphasis on patient safety, reduced recovery time, and outpatient surgical procedures is accelerating the adoption of medical laser systems across hospitals and specialty clinics.

Europe Medical Laser Systems Market Insight

The Europe Medical Laser Systems market remains a major contributor to global revenue, driven by strong government healthcare support, advanced medical research infrastructure, and high demand for precision-based surgical treatments. The widespread use of laser systems in dermatology, ophthalmology, gynecology, urology, and dental applications is supporting market expansion across the region. Increasing investments in minimally invasive surgical technologies, coupled with strict healthcare quality standards and a highly skilled medical workforce, continue to enhance adoption of Medical Laser Systems throughout Europe.

U.K. Medical Laser Systems Market Insight

The U.K. Medical Laser Systems market is experiencing steady growth, supported by rising adoption of advanced laser technologies in hospitals, private clinics, and cosmetic surgery centers. Increasing demand for aesthetic procedures, along with growing utilization of laser systems in ophthalmic and dental treatments, is contributing to market expansion. Furthermore, integration of AI-assisted imaging, robotic precision systems, and advanced diagnostic tools is improving treatment accuracy and efficiency, positioning the U.K. as a key innovation hub in the Medical Laser Systems industry.

Germany Medical Laser Systems Market Insight

The Germany Medical Laser Systems market is expanding steadily due to the country’s strong medical device manufacturing base, advanced clinical research capabilities, and increasing adoption of high-precision laser technologies. Hospitals, specialty clinics, and research institutes are increasingly utilizing laser systems for surgical procedures, dermatological treatments, and ophthalmic applications. Continuous advancements in medical laser engineering, along with strong healthcare funding and innovation-driven policies, are further driving market growth in Germany.

Asia-Pacific Medical Laser Systems Market Insight

The Asia-Pacific Medical Laser Systems market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising medical tourism, increasing patient awareness, and growing demand for advanced laser-based treatments across emerging economies such as China, India, and Japan. The region is experiencing strong adoption of medical laser systems in dermatology, ophthalmology, and cosmetic procedures, supported by government initiatives to modernize healthcare systems and improve access to advanced medical technologies. In addition, increasing investments in private healthcare facilities and hospital modernization are further accelerating market expansion across Asia-Pacific.

Japan Medical Laser Systems Market Insight

The Japan Medical Laser Systems market is witnessing consistent growth due to rising demand for advanced surgical precision technologies, increasing prevalence of age-related eye and skin disorders, and strong focus on medical innovation. Hospitals and specialty clinics are increasingly adopting laser systems for ophthalmic surgeries, dermatology procedures, and minimally invasive treatments. Moreover, integration of robotic-assisted systems and high-precision laser platforms is further enhancing clinical efficiency and supporting market growth in Japan.

China Medical Laser Systems Market Insight

The China Medical Laser Systems market is growing rapidly, driven by expanding healthcare infrastructure, rising burden of chronic diseases, increasing aesthetic treatment demand, and strong government support for medical technology advancement. Growing adoption of laser systems in dermatology, ophthalmology, dentistry, and surgical applications is significantly boosting market demand. In addition, rapid urbanization, rising disposable income, and increasing investments in hospital modernization and medical R&D are positioning China as one of the fastest-growing markets for Medical Laser Systems globally.

Medical Laser Systems Market Share

The Medical Laser Systems industry is primarily led by well-established companies, including:

- Lumenis Ltd. (Israel)

- Boston Scientific Corporation (U.S.)

- Olympus Corporation (Japan)

- Bausch + Lomb Corporation (U.S.)

- Alcon Inc. (Switzerland)

- Candela Corporation (U.S.)

- Cutera Inc. (U.S.)

- Fotona d.o.o. (Slovenia)

- IPG Photonics Corporation (U.S.)

- Biolase Inc. (U.S.)

- Lynton Lasers Ltd. (U.K.)

- El.En. S.p.A. (Italy)

- Syneron Medical Ltd. (Israel)

- Alma Lasers (Sisram Medical Ltd.) (Israel)

- Dornier MedTech GmbH (Germany)

- Quanta System S.p.A. (Italy)

- Excelitas Technologies Corp. (U.S.)

- Spectranetics Corporation (U.S.)

- Sharplan Lasers (Israel)

- Heraeus Holding GmbH (Germany)

- Topcon Corporation (Japan)

- NIDEK Co., Ltd. (Japan)

- Shanghai Wonderful Opto-Electrics Co., Ltd. (China)

- Shenzhen New Industries Biomedical Engineering Co., Ltd. (China)

- Beijing Qianjing Medical Co., Ltd. (China)

- Allengers Medical Systems Ltd. (India)

- PolyPhotonix Ltd. (U.K.)

- Trimedyne Inc. (U.S.)

- IRIDEX Corporation (U.S.)

- A.R.C. Laser GmbH (Germany)

- LightScalpel LLC (U.S.)

Latest Developments in Medical Laser Systems Market

- In March 2021, Boston Scientific Corporation announced a definitive agreement to acquire the surgical business of Lumenis for approximately USD 1.07 billion, strengthening its position in urology and surgical laser technologies. The acquisition expanded Boston Scientific’s laser portfolio used in minimally invasive procedures such as kidney stone and prostate treatments, reinforcing its leadership in advanced energy-based medical devices and broadening its global surgical laser offerings

- In January 2024, Bausch + Lomb Corporation received U.S. FDA approval for the TENEO Excimer Laser Platform for LASIK vision correction procedures, including treatment of myopia and myopic astigmatism. The launch enhanced the company’s ophthalmic laser portfolio, enabling faster and more precise refractive surgery procedures and strengthening its presence in the rapidly growing vision correction segment of the medical laser systems market

- In September 2021, ZEISS Medical Technology introduced the VISUMAX 800 femtosecond laser system, designed for next-generation refractive eye surgery. The system improved workflow efficiency, reduced laser treatment time, and enhanced precision in procedures such as SMILE eye surgery, marking a significant advancement in ophthalmic laser technology and reinforcing ZEISS’s leadership in vision correction solutions

- In April 2022, Alcon Inc. expanded its femtosecond laser-assisted cataract surgery (FLACS) ecosystem through continued upgrades to its LenSx and related laser platforms, focusing on improving surgical precision, imaging integration, and procedural efficiency. These enhancements supported wider adoption of laser-assisted cataract procedures across hospitals and eye care centers globally, reinforcing Alcon’s strong position in ophthalmic laser systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.