Global Medication Delivery Systems Market

Market Size in USD Billion

USD

47.72 Billion

USD

77.21 Billion

2025

2033

USD

47.72 Billion

USD

77.21 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 47.72 Billion |

Market Size (Forecast Year) |

USD 77.21 Billion |

CAGR |

% |

Major Markets Players |

|

Medication Delivery Systems Market Size

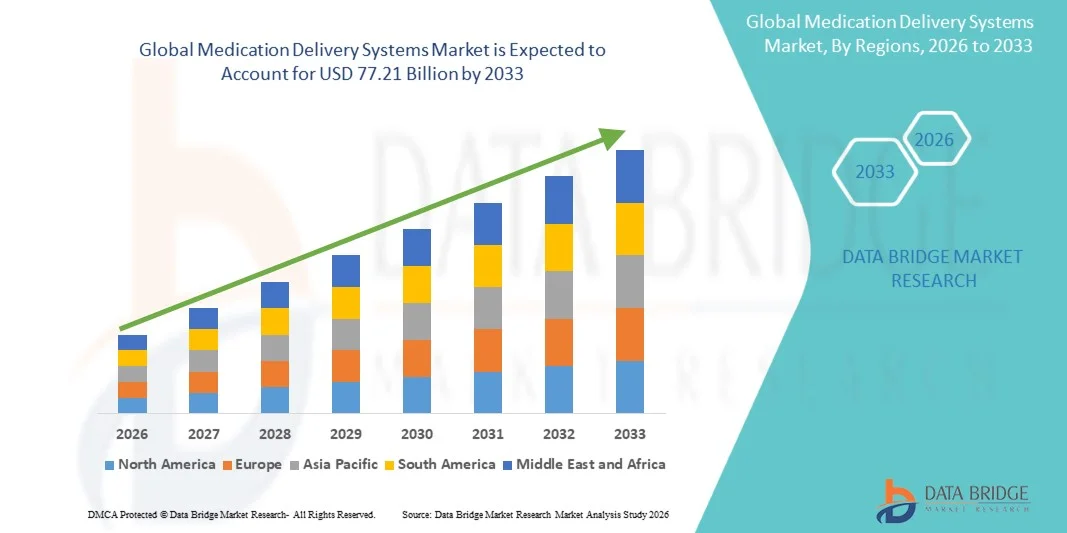

- The global medication delivery systems market size was valued at USD 47.72 billion in 2025 and is expected to reach USD 77.21 billion by 2033, at a CAGR of 6.2% during the forecast period

- The market growth is primarily driven by the rising prevalence of chronic diseases, increasing demand for advanced drug delivery methods, and continuous innovation in biotechnology and pharmaceutical formulations aimed at improving therapeutic efficacy and patient compliance

- In addition, the growing adoption of self-administration and home-based healthcare devices, coupled with technological advancements such as smart injectors and controlled-release systems, is transforming drug delivery practices. These factors collectively enhance treatment precision and convenience, thereby accelerating the global market expansion

Medication Delivery Systems Market Analysis

- Medication delivery systems, encompassing technologies such as injectors, inhalers, transdermal patches, and infusion devices, are becoming increasingly essential in modern healthcare for ensuring precise, safe, and efficient administration of pharmaceuticals across hospital and homecare settings

- The growing demand for advanced medication delivery systems is primarily driven by the rising prevalence of chronic and lifestyle-related diseases, increasing need for self-administration solutions, and ongoing innovation in targeted and sustained-release drug delivery technologies

- North America dominated the global medication delivery systems market with the largest revenue share of 40.3% in 2025, attributed to a well-established healthcare infrastructure, high healthcare expenditure, and strong presence of leading biopharmaceutical and medical device manufacturers driving innovation in drug delivery technologies

- Asia-Pacific is projected to be the fastest-growing region during the forecast period due to expanding healthcare access, rising awareness of advanced treatment options, and increasing pharmaceutical R&D investments across emerging economies

- The Injection- Based Drug Delivery System segment dominated the market with largest market share of 46.7% in 2025, driven by its critical role in chronic disease management, improved bioavailability, and growing use of prefilled syringes, autoinjectors, and wearable injectors for self-administration

Report Scope and Medication Delivery Systems Market Segmentation

|

Attributes |

Medication Delivery Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Medication Delivery Systems Market Trends

Integration of Smart and Connected Drug Delivery Technologies

- A significant and accelerating trend in the global medication delivery systems market is the integration of smart technologies and connectivity features such as IoT and AI within drug delivery devices, enabling real-time monitoring, precise dosing, and improved patient adherence

- For instance, the BD Libertas Wearable Injector and Ypsomed’s SmartPilot system use integrated sensors and connectivity to transmit dosing data, allowing healthcare professionals and patients to track treatment progress remotely through digital platforms

- AI-enabled delivery systems can analyze patient data to personalize drug administration schedules, detect anomalies in usage, and provide predictive maintenance alerts for reusable injectors or infusion pumps. This data-driven approach is improving treatment outcomes and compliance rates

- The growing emphasis on digital health ecosystems is facilitating the seamless integration of connected delivery devices with mobile health apps and telemedicine platforms, allowing synchronized management of medication, vitals, and treatment plans through unified dashboards

- This trend toward intelligent, data-driven, and patient-centric delivery systems is reshaping the future of therapeutics, driving the development of advanced platforms for chronic disease management and precision medicine. Consequently, companies such as West Pharmaceutical Services and Phillips-Medisize are focusing on smart injectors with wireless connectivity and adherence tracking

- The demand for connected and automated delivery devices is increasing rapidly across hospital, homecare, and self-administration settings as patients and healthcare providers prioritize convenience, accuracy, and remote monitoring capabilities

Medication Delivery Systems Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Shift Toward Self-Administration Devices

- The growing global burden of chronic diseases such as diabetes, cancer, and cardiovascular disorders, coupled with a rising preference for home-based care, is a key driver of the medication delivery systems market

- For instance, in March 2025, Novo Nordisk launched a next-generation insulin delivery pen with enhanced dose memory and Bluetooth connectivity to support real-time data sharing with healthcare providers, reflecting the shift toward smart self-administration solutions

- As patients seek greater independence and convenience, drug delivery systems such as autoinjectors, prefilled syringes, and wearable injectors are enabling self-management of complex therapies, reducing hospital dependency and improving quality of life

- Furthermore, technological advancements in formulation science and device design are enhancing drug stability, bioavailability, and precision in dosing, supporting the adoption of advanced systems across therapeutic areas

- The growing emphasis on personalized medicine, where treatment is tailored to individual patient needs, is further fueling demand for delivery systems capable of controlled and targeted administration, especially for biologics and biosimilars. The expansion of home healthcare services and digital monitoring further amplifies market growth

Restraint/Challenge

Regulatory Complexity and Device Safety Concerns

- Complex and evolving regulatory requirements surrounding combination products, where drugs and devices are integrated, pose a major challenge to the commercialization and approval of new medication delivery systems

- For instance, stringent guidelines from agencies such as the FDA and EMA regarding device validation, sterility assurance, and human factors testing can significantly prolong development timelines and increase compliance costs for manufacturers

- Concerns related to device malfunction, dosing errors, and material biocompatibility also raise patient safety challenges, requiring continuous innovation in device design and testing protocols

- Furthermore, the integration of electronics and connectivity features introduces cybersecurity risks and necessitates robust data protection measures to safeguard patient information and ensure device reliability

- The high cost of advanced delivery systems compared to traditional methods can also restrict access in cost-sensitive markets, particularly in developing economies with limited reimbursement structures. However, ongoing efforts to streamline regulatory pathways and encourage digital health innovation are expected to ease these barriers over time

- Overcoming these challenges through early regulatory engagement, cross-disciplinary R&D collaboration, and adherence to international safety standards will be critical to maintaining market competitiveness and ensuring patient trust

Medication Delivery Systems Market Scope

The market is segmented on the basis of type, technology, carrier type, application, and end-users.

- By Type

On the basis of type, the global medication delivery systems market is segmented into oral drug delivery system, injection-based drug delivery system, inhalation/pulmonary drug delivery system, transdermal drug delivery system, transmucosal drug delivery system, carrier-based drug delivery system, and others. The injection-based drug delivery system segment dominated the market with the largest revenue share of 46.7% in 2025, primarily due to its widespread application in chronic disease management, vaccines, and biologic therapies. The segment benefits from the increasing demand for prefilled syringes, autoinjectors, and wearable injectors that promote self-administration and dosage accuracy. Injectables remain the preferred choice for delivering large-molecule drugs that cannot be effectively administered orally. Furthermore, continuous innovations in needle-free injectors and smart injection devices are improving safety and convenience. The strong presence of global players focusing on user-friendly and connected injection systems further supports the dominance of this segment.

The inhalation/pulmonary drug delivery system segment is projected to witness the fastest growth rate of 21.3% from 2026 to 2033, driven by the increasing prevalence of respiratory conditions such as asthma and COPD. Growing awareness of localized pulmonary drug delivery and the development of smart inhalers that track usage patterns are enhancing treatment adherence. Pharmaceutical companies are investing heavily in digital inhalation devices integrated with mobile applications to optimize dosage and compliance. In addition, expanding research into inhaled formulations for systemic diseases beyond respiratory disorders, such as diabetes and CNS conditions, is expected to boost this segment’s growth.

- By Technology

On the basis of technology, the market is segmented into prodrug, implants and intrauterine devices, targeted drug delivery, polymeric drug delivery, and other technologies. The targeted drug delivery segment dominated the market with a revenue share of 38.2% in 2025, owing to its precision in delivering drugs directly to the site of action, thereby improving efficacy and minimizing systemic side effects. This technology has gained significant traction in oncology and autoimmune disease treatments. Pharmaceutical companies are increasingly leveraging nanocarriers, antibody conjugates, and ligand-targeting methods to improve site specificity and therapeutic outcomes. For instance, targeted polymeric nanoparticles and liposomes are being widely used for controlled cancer therapy. Ongoing advances in molecular targeting and bioengineering continue to strengthen the position of this segment.

The polymeric drug delivery segment is expected to record the fastest CAGR of 20.8% from 2026 to 2033, driven by the growing adoption of biocompatible and biodegradable polymers in sustained-release drug formulations. Polymeric materials enable controlled and predictable drug release, improving compliance for chronic therapies. Their adaptability in forming micelles, implants, and nanoparticles enhances versatility in multiple applications. Moreover, increasing R&D in stimuli-responsive and bioresorbable polymers is creating new possibilities in controlled-release and implantable delivery systems.

- By Carrier Type

On the basis of carrier type, the market is divided into liposomes, nanoparticles, microspheres, monoclonal antibodies, and others. The nanoparticles segment dominated the market with a revenue share of 41.5% in 2025, due to their superior ability to enhance drug solubility, protect active ingredients, and provide controlled release. Nanoparticles play a critical role in oncology and CNS applications by enabling targeted and efficient drug delivery across biological barriers. Their compatibility with diverse drug molecules—including peptides, nucleic acids, and small molecules—makes them integral to next-generation therapeutics. Ongoing advancements in lipid-based and polymeric nanoparticle formulations are expanding their adoption in mRNA vaccines and gene therapy. The growing collaboration between nanotech developers and pharmaceutical firms continues to sustain the dominance of this segment.

The monoclonal antibodies segment is projected to witness the fastest growth rate of 22.1% from 2026 to 2033, driven by the expanding use of antibody-drug conjugates (ADCs) and targeted biologic therapies. Monoclonal antibodies offer high specificity and reduced toxicity, making them a cornerstone of modern drug delivery strategies. Increasing FDA approvals of mAb-based therapeutics for oncology, immunology, and infectious diseases are boosting market adoption. Furthermore, innovations in bispecific and humanized antibodies are enhancing delivery efficiency and expanding treatment potential across diverse therapeutic areas.

- By Application

On the basis of application, the market is segmented into cardiovascular diseases, oncology, urology, diabetes, CNS, ophthalmology, inflammatory diseases & infections, and other applications. The oncology segment dominated the market with a revenue share of 33.4% in 2025, primarily due to the increasing global cancer incidence and demand for precision-based drug delivery technologies. Advanced systems such as nanocarrier-based chemotherapy and implantable release devices are revolutionizing cancer treatment by improving targeted efficacy and reducing systemic toxicity. Pharmaceutical companies are focusing on developing personalized and controlled-release formulations for various cancer types. The rising use of antibody-drug conjugates and liposomal formulations further reinforces oncology’s dominance in this market. Continuous R&D investments and regulatory approvals of innovative cancer therapies are expected to sustain this growth trajectory.

The diabetes segment is anticipated to record the fastest growth rate of 20.2% from 2026 to 2033, fueled by the growing global diabetic population and rising demand for advanced insulin delivery systems. Wearable insulin pumps, smart pens, and continuous glucose monitors integrated with mobile apps are transforming diabetes management. The increasing availability of user-friendly and minimally invasive devices is improving patient compliance. Furthermore, advancements in closed-loop insulin delivery and artificial pancreas technologies are expected to further accelerate growth in this segment during the forecast period.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, specialized clinics, and clinical research & development centers. The hospitals segment dominated the market with a revenue share of 47.9% in 2025, owing to their role as the primary centers for chronic and acute disease treatment requiring advanced delivery systems. Hospitals utilize cutting-edge injectables, infusions, and implantable devices for inpatient and outpatient care. The segment also benefits from skilled medical personnel, advanced monitoring infrastructure, and established procurement networks. Hospitals serve as major users of targeted delivery systems in oncology, cardiology, and pain management. The integration of connected drug delivery devices into hospital information systems further enhances treatment accuracy and safety.

The clinical research & development centers segment is projected to witness the fastest CAGR of 18.7% from 2026 to 2033, driven by increasing R&D investment in biologics, gene therapy, and nanomedicine. Research centers play a critical role in testing and validating new delivery technologies such as micro-needles, polymeric implants, and nanoformulations. The rise of contract research organizations (CROs) and collaborations between pharmaceutical firms and technology developers is accelerating innovation. In addition, growing adoption of preclinical and clinical evaluation of smart delivery systems to enhance therapeutic outcomes is further supporting this segment’s growth.

Medication Delivery Systems Market Regional Analysis

- North America dominated the global medication delivery systems market with the largest revenue share of 40.3% in 2025, attributed to a well-established healthcare infrastructure, high healthcare expenditure, and strong presence of leading biopharmaceutical and medical device manufacturers driving innovation in drug delivery technologies

- Healthcare providers and patients in the region highly value advanced drug delivery technologies that offer precise dosing, enhanced safety, and improved treatment adherence, particularly for chronic diseases and biologic therapies

- The widespread adoption of connected and smart drug delivery devices, combined with supportive regulatory frameworks and reimbursement policies, is further encouraging market growth. High R&D investment in innovative delivery platforms, such as autoinjectors, wearable injectors, and targeted delivery systems, is strengthening North America’s leading position

U.S. Medication Delivery Systems Market Insight

The U.S. medication delivery systems market captured the largest revenue share of 78% in 2025 within North America, driven by high adoption of advanced drug delivery technologies and strong healthcare infrastructure. Patients and healthcare providers increasingly prefer connected and smart delivery devices such as autoinjectors, wearable injectors, and prefilled syringes that enable precise dosing and improved adherence. The rising prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders is fueling demand for innovative delivery solutions. Furthermore, the integration of devices with mobile health applications and remote monitoring platforms is supporting personalized therapy management. Robust R&D investments by major pharmaceutical and medical device companies further stimulate market expansion. These factors collectively establish the U.S. as the dominant market for cutting-edge medication delivery systems.

Europe Medication Delivery Systems Market Insight

The Europe medication delivery systems market is projected to expand at a substantial CAGR during the forecast period, primarily driven by the rising prevalence of chronic diseases and increasing demand for self-administration solutions. Regulatory frameworks supporting innovative drug delivery technologies encourage the adoption of devices such as smart pens, inhalers, and implantable systems. Growing urbanization and the preference for home-based healthcare are fostering market growth across residential and clinical settings. Consumers and healthcare providers are also drawn to advanced systems that improve treatment compliance, safety, and convenience. The adoption of connected and automated devices across hospitals and clinics is accelerating the market’s growth in Western and Northern Europe.

U.K. Medication Delivery Systems Market Insight

The U.K. medication delivery systems market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of chronic disease management and demand for improved treatment adherence. The trend toward home-based care and patient-centric delivery solutions, such as wearable injectors and smart insulin pens, is boosting adoption. Rising government initiatives to promote digital health and telemedicine further support the integration of connected delivery devices. In addition, the country’s advanced healthcare infrastructure and well-established pharmaceutical industry are enabling faster deployment of novel drug delivery technologies. These factors make the U.K. a key growth market within Europe.

Germany Medication Delivery Systems Market Insight

The Germany medication delivery systems market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s focus on healthcare innovation and technological adoption. Increasing awareness of chronic disease management and precision therapy is driving the adoption of advanced injectable, transdermal, and implantable systems. Germany’s well-developed healthcare infrastructure and strong presence of medical device manufacturers support the integration of connected and smart delivery devices. Demand for eco-friendly, safe, and patient-friendly delivery technologies is also rising. The integration of devices with digital health platforms and hospital monitoring systems is further enhancing market growth. Consumer preference for technologically advanced and reliable drug delivery solutions aligns with local healthcare expectations.

Asia-Pacific Medication Delivery Systems Market Insight

The Asia-Pacific medication delivery systems market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing prevalence of chronic and lifestyle diseases, rising disposable incomes, and expanding healthcare infrastructure in countries such as China, Japan, and India. The growing awareness of self-administration and home-based care is supporting demand for wearable injectors, smart pens, and inhalers. Government initiatives promoting digital health adoption are further encouraging market expansion. Furthermore, the region is becoming a hub for manufacturing advanced drug delivery devices, improving affordability and accessibility for a wider patient base. These factors collectively position APAC as the fastest-growing market globally.

Japan Medication Delivery Systems Market Insight

The Japan medication delivery systems market is gaining momentum due to rapid urbanization, an aging population, and a high level of technological adoption. The demand for convenient and precise drug administration is driving the adoption of connected delivery devices such as smart injectors, infusion pumps, and inhalers. Integration of these devices with mobile applications and remote monitoring platforms supports patient adherence and clinical outcomes. Japan’s emphasis on digital health, coupled with strong healthcare infrastructure and R&D investment in advanced therapies, is further stimulating market growth. Rising awareness of chronic disease management and self-care solutions also contributes to market expansion.

India Medication Delivery Systems Market Insight

The India medication delivery systems market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, increasing healthcare access, and high adoption of advanced technologies. Rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions is boosting demand for smart drug delivery devices. Government initiatives promoting digital health, telemedicine, and smart hospital infrastructure are further accelerating adoption. Affordable and locally manufactured delivery systems, such as wearable injectors and prefilled syringes, are expanding accessibility to a broader population. Increasing awareness of self-administration and patient-centric therapies is supporting market growth across residential, clinical, and hospital settings.

Medication Delivery Systems Market Share

The Medication Delivery Systems industry is primarily led by well-established companies, including:

- BD (U.S.)

- West Pharmaceutical Services, Inc. (U.S.)

- AptarGroup, Inc. (U.S.)

- ENABLE INJECTIONS (U.S.)

- YPSOMED (Switzerland)

- Nemera (France)

- Owen Mumford (U.K.)

- ARx, LLC. (U.S.)

- Camurus AB (Sweden)

- Catalent, Inc. (U.S.)

- Gerresheimer AG (Germany)

- Phillips Medisize (U.S.)

- SHL Medical (Switzerland)

- Consort Medical plc (U.K.)

- Recipharm AB (Sweden)

- Samyang Holdings Corporation. (South Korea)

- WestRock Company (U.S.)

- Unilife Corporation (U.S.)

- Geratherm Medical AG (Germany)

What are the Recent Developments in Global Medication Delivery Systems Market?

- In August 2025, Enable Injections announced that Brazil’s regulatory agency (ANVISA) approved the enFuse system for subcutaneous administration and the UK’s MHRA registered it for use. This signifies global regulatory expansion of wearable/large‑volume injectors into emerging markets, demonstrating that advanced delivery systems are moving beyond developed markets and opening broader commercial opportunities for patient‑centric drug‑device solutions

- In July 2025, BD announced the launch of its first pharma‑sponsored combination‑product clinical trial using the BD Libertas Wearable Injector technology for subcutaneous delivery of complex biologics. This development is significant because it moves wearable large‑volume injectors out of purely internal development into pharma‑sponsored trials, pointing to increasing viability of self‑administered biologics and the maturation of the delivery‑system segment

- In March 2025, Enable Injections, Inc. received CE‑Mark (EU MDR) approval for its enFuse® On‑Body Injector System (syringe and vial‑transfer system) in Europe, enabling the device to be used by healthcare professionals in clinic settings. Achieving CE‑Mark under EU Medical Device Regulation for a large‑volume on‑body injector is a key milestone highlighting the movement toward wearable, patient‑friendly systems capable of delivering biologics at home or in‑clinic, reducing burden on infusion centres

- In January 2025, Becton Dickinson and Company (BD) announced that it would showcase an extensive range of drug‑delivery innovations at the Pharmapack 2025 event in Paris, emphasising biologics (GLP‑1s, vaccines, acute care) and partnering with pharma/biotech to support combinations and self‑care devices. This move highlights the industry’s shift toward self‑administration and home‑based care devices, particularly for large‑volume injectable biologics, and BD’s strategy to strengthen its drug‑device platform portfolio and ecosystem partnerships

- In February 2023, BD and its subsidiary ZebraSci announced strategic investments to support the development of drug‑device combination products, including wearable and on‑body injectors such as the Libertas platform. This earlier development sets the stage for the later trial launch and regulatory approvals by showing how companies are building upstream capabilities to meet the rising demand for advanced delivery systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.