Global Metastatic Castrate Resistant Prostate Cancer Treatment Market

Market Size in USD Billion

USD

11.99 Billion

USD

22.37 Billion

2024

2032

USD

11.99 Billion

USD

22.37 Billion

2024

2032

| 2025 - 2032 | |

| USD 11.99 Billion | |

| USD 22.37 Billion | |

| % | |

|

Metastatic Castrate Resistant Prostate Cancer Treatment Market Size

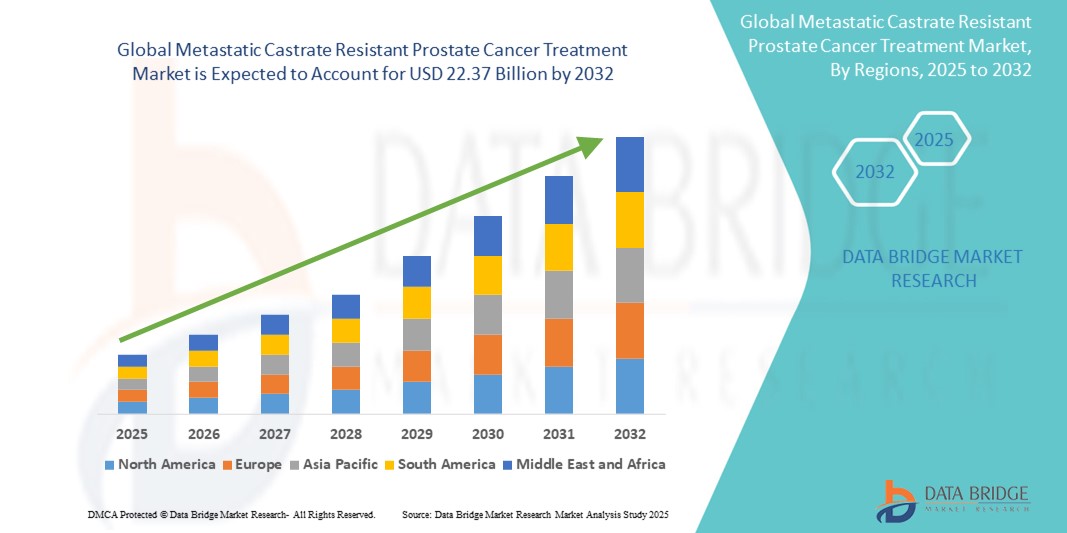

- The global metastatic castrate resistant prostate cancer treatment market size was valued at USD 11.99 billion in 2024 and is expected to reach USD 22.37 billion by 2032, at a CAGR of 8.10% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced oncology therapies and technological advancements in precision medicine, leading to enhanced diagnostic and treatment capabilities for metastatic castrate resistant prostate cancer (mCRPC) across healthcare settings

- Furthermore, rising patient awareness, increasing prevalence of prostate cancer, and the demand for more effective, targeted, and personalized treatment options are establishing mCRPC therapies—such as androgen receptor inhibitors, radioligand therapy, and immunotherapy—as essential components in modern cancer care. These converging factors are accelerating the uptake of Metastatic Castrate Resistant Prostate Cancer Treatment solutions, thereby significantly boosting the industry's growth

Metastatic Castrate Resistant Prostate Cancer Treatment Market Analysis

- Metastatic castrate resistant prostate cancer (mCRPC) treatments, including advanced hormone therapies, chemotherapy, radiopharmaceuticals, and immunotherapy, are becoming increasingly vital components of modern oncology care due to their effectiveness in managing advanced-stage prostate cancer and improving patient survival outcomes

- The escalating demand for mCRPC treatment is primarily fueled by the rising global incidence of prostate cancer, growing geriatric population, and increasing availability of next-generation targeted therapies and diagnostic tools

- North America dominated the metastatic castrate resistant prostate cancer treatment market with the largest revenue share of 41.7% in 2024, characterized by early adoption of innovative cancer therapies, robust healthcare infrastructure, favorable reimbursement policies, and the strong presence of key biopharmaceutical companies

- Asia-Pacific is expected to be the fastest-growing region in the metastatic castrate resistant prostate cancer treatment market, projected to grow at a CAGR of 24.7% during the forecast period (2025–2032). This growth is supported by increasing awareness of prostate cancer, improvements in healthcare infrastructure, growing healthcare expenditure, and rising access to modern oncology treatments across countries such as China, Japan, and India

- The hormone therapies segment dominated the metastatic castrate resistant prostate cancer treatment market with a market share of 44.6% in 2024, driven by their established role as the first-line treatment in managing advanced prostate cancer. These therapies, particularly androgen receptor inhibitors, have demonstrated significant efficacy in delaying disease progression and improving patient survival, making them a cornerstone in clinical practice

Report Scope and Metastatic Castrate Resistant Prostate Cancer Treatment Market Segmentation

|

Attributes |

Metastatic Castrate Resistant Prostate Cancer Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Metastatic Castrate Resistant Prostate Cancer Treatment Market Trends

“Evolving Treatment Landscape Driven by Targeted and Radioligand Therapies”

- A significant and accelerating trend in the global metastatic castrate resistant prostate cancer (mcrpc) treatment market is the shift towards advanced targeted therapies and radioligand treatments, offering enhanced efficacy and improved patient outcomes compared to traditional chemotherapy options. This evolution is fundamentally changing the clinical approach to managing advanced-stage prostate cancer

- For instance, Pluvicto (lutetium Lu 177 vipivotide tetraxetan), a recently approved radioligand therapy by Novartis, has demonstrated promising results in improving progression-free and overall survival in patients with mCRPC who have already undergone androgen receptor pathway inhibition and chemotherapy

- Targeted therapies, such as PARP inhibitors (such as, olaparib and rucaparib), are also gaining traction, particularly for patients with homologous recombination repair (HRR) gene mutations, offering personalized treatment options based on genetic profiling

- The integration of companion diagnostics with these therapies is enabling more precise identification of eligible patients, ensuring better treatment outcomes and minimizing unnecessary exposure to ineffective drugs

- This trend toward more personalized and biologically targeted treatment modalities is redefining the treatment landscape, encouraging pharmaceutical companies to invest in research and development of novel therapeutic agents and combination regimens

- The demand for these next-generation therapies is growing rapidly across major markets, as oncologists and healthcare providers increasingly prioritize efficacy, tolerability, and survival benefits for patients with advanced prostate cancer

Metastatic Castrate Resistant Prostate Cancer Treatment Market Dynamics

Driver

“Growing Need Due to Rising Disease Burden and Evolving Treatment Expectations”

- The increasing global burden of prostate cancer, especially in aging male populations, coupled with the transition of many patients to metastatic castrate-resistant stages, is significantly driving demand for advanced treatment options in the mCRPC market

- For instance, in April 2024, Novartis AG announced the expansion of its radioligand therapy manufacturing capabilities in Europe to support rising demand for Pluvicto, highlighting the pharmaceutical industry’s commitment to addressing the unmet needs of the mCRPC patient population

- As patients and healthcare providers seek more effective, life-prolonging therapies, the market is seeing growing preference for targeted treatments such as androgen receptor inhibitors, radioligand therapies, and PARP inhibitors, which offer improved survival benefits over traditional chemotherapy

- Furthermore, advancements in genetic testing and companion diagnostics are enabling the personalization of treatment strategies, increasing the effectiveness of mCRPC therapy while minimizing side effects

- The convenience of oral therapies, ongoing development of less invasive administration routes, and the emergence of combination treatment regimens are key factors accelerating therapy adoption across both developed and developing regions. In addition, the increasing number of clinical trials and accelerated regulatory approvals are expected to further propel market growth

Restraint/Challenge

“High Treatment Costs and Limited Access in Low-Income Regions”

- One of the primary challenges in the mCRPC treatment market is the high cost associated with next-generation therapies such as radioligand treatments and targeted oral therapies. These advanced options often come with premium pricing, limiting access for patients in low- and middle-income countries

- For instance, the cost of Pluvicto or combination therapy involving enzalutamide and olaparib can exceed tens of thousands of dollars annually, creating affordability barriers despite their clinical efficacy

- Limited insurance coverage or reimbursement in many healthcare systems further restricts treatment availability, especially in regions where public health budgets are constrained

Addressing these affordability and access issues through tiered pricing strategies, partnerships with health organizations, and government subsidies is essential to ensure equitable access to life-saving treatments - In addition, patient reluctance toward newer therapies due to lack of awareness or trust in genetic-based treatments can slow market uptake. Enhancing provider and patient education on the benefits and safety of innovative treatment modalities will be critical for long-term market growth and penetration

Metastatic Castrate Resistant Prostate Cancer Treatment Market Scope

The market is segmented on the basis of treatment, route of administration, form, end-users, and distribution channel.

• By Treatment

On the basis of treatment, the metastatic castrate resistant prostate cancer treatment market is segmented into hormone therapies, Xofigo, Sipuleucel-T, cabazitaxel, docetaxel, and others. The hormone therapies segment dominated the market with the largest revenue share of 44.6% in 2024, driven by the long-standing use of androgen deprivation therapy (ADT) and newer androgen receptor signaling inhibitors (such as, enzalutamide and abiraterone). These therapies continue to be first-line and backbone treatments due to their proven survival benefits.

The xofigo segment is expected to witness the fastest CAGR of 10.3% from 2025 to 2032, supported by increasing clinical adoption of radiopharmaceuticals for bone metastases management and favorable clinical trial data validating its efficacy and safety.

• By Route of Administration

On the basis of route of administration, the metastatic castrate resistant prostate cancer treatment market is segmented into oral, parenteral, and others. The oral segment held the largest market revenue share of 56.7% in 2024, driven by patient preference for convenience and the wide adoption of orally administered therapies such as abiraterone and enzalutamide. The rise in home-based treatment models and telehealth services also supports this growth.

The parenteral segment is anticipated to grow at the fastest CAGR of 9.2% from 2025 to 2032, due to the increasing use of intravenous chemotherapy (such as docetaxel and cabazitaxel) and immunotherapy agents that require clinical supervision for administration.

• By Form

On the basis of form, the metastatic castrate resistant prostate cancer treatment market is segmented into Solid Dosage Form and Liquid Dosage Form. The solid dosage form segment accounted for the largest market share of 62.4% in 2024, attributed to the dominance of oral drugs in the treatment landscape and their stability, ease of storage, and transportability.

The liquid dosage form segment is expected to register a CAGR of 8.7% during the forecast period, fueled by the increasing use of injectable therapeutics and novel radiopharmaceuticals, especially for patients with bone-dominant metastases.

• By End-Users

On the basis of end-users, the metastatic castrate resistant prostate cancer treatment market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment led the market with the highest revenue share of 44.3% in 2024, driven by the availability of multidisciplinary care, access to advanced diagnostics, and preferred settings for chemotherapy and radiopharmaceutical administrations.

The homecare segment is expected to experience the fastest CAGR of 10.9% from 2025 to 2032, due to growing preference for oral therapies and the shift toward remote care and self-administration of medications, particularly in developed regions.

• By Distribution Channel

On the basis of distribution channel, the metastatic castrate resistant prostate cancer treatment market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment captured the largest share of 48.2% in 2024, supported by the institutional sales of high-cost injectable and specialty medicines administered in inpatient or outpatient oncology units.

The online pharmacy segment is projected to grow at the fastest CAGR of 11.5% over the forecast period, driven by increased digital health adoption, medication delivery convenience, and rising patient comfort with telemedicine and digital prescriptions.

Metastatic Castrate Resistant Prostate Cancer Treatment Market Regional Analysis

- North America dominated the metastatic castrate resistant prostate cancer treatment market with the largest revenue share of 41.7% in 2024, driven by the early adoption of advanced oncology therapies, strong healthcare infrastructure, and extensive reimbursement coverage for cancer treatments

- The U.S., in particular, has witnessed robust growth in mCRPC treatment adoption, supported by a high prevalence of prostate cancer, increasing awareness among patients and physicians, and the availability of cutting-edge treatment options such as enzalutamide, abiraterone, and radiopharmaceuticals such as Xofigo

- Furthermore, ongoing clinical trials, increased investment in precision medicine, and strategic collaborations between biotech firms and academic institutions are reinforcing the region’s leadership in mCRPC innovation and treatment accessibility

U.S. Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The U.S. metastatic castrate resistant prostate cancer treatment market captured the largest revenue share of 81.2% in 2024 within North America, driven by the widespread availability of advanced therapeutics and high prostate cancer prevalence. The U.S. healthcare system facilitates rapid uptake of novel treatments such as androgen receptor signaling inhibitors (enzalutamide, abiraterone), chemotherapy (docetaxel, cabazitaxel), and targeted radiopharmaceuticals (Xofigo). In addition, strong R&D investments, robust clinical trial networks, and FDA approvals of new mCRPC therapies continue to bolster the market. Patient access is further supported by reimbursement policies and the presence of key pharmaceutical companies with extensive oncology portfolios.

Europe Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The Europe metastatic castrate resistant prostate cancer treatment market is projected to register a CAGR of 12.9% from 2025 to 2032, driven by increased diagnosis rates, growing awareness about prostate cancer treatment options, and the adoption of advanced therapeutics across major countries including Germany, the U.K., France, and Italy. Stringent healthcare regulations supporting evidence-based treatments and expanded use of hormone therapies and immunotherapy agents such as sipuleucel-T are key growth contributors. In addition, collaborations between EU-based research institutions and biotech firms are supporting the development of next-generation treatments for late-stage prostate cancer.

U.K. Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The U.K. metastatic castrate resistant prostate cancer treatment market is expected to grow at a CAGR of 13.4% during the forecast period, driven by an increase in the geriatric population and national cancer care initiatives. The National Health Service (NHS) supports early screening and reimbursement of novel therapeutics, while research programs funded by Cancer Research UK and private partners encourage faster clinical development. The country’s streamlined regulatory environment under NICE further facilitates access to innovative mCRPC treatments.

Germany Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The Germany metastatic castrate resistant prostate cancer treatment market is projected to expand at a CAGR of 12.2% through 2032, attributed to its strong pharmaceutical manufacturing base, high healthcare spending, and emphasis on precision medicine. Adoption of combination therapies, including hormonal agents and chemotherapy, along with participation in pan-European clinical trials, supports market growth. German healthcare providers are increasingly utilizing biomarker-based treatment decisions to personalize therapy for mCRPC patients.

Asia-Pacific Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The Asia-Pacific metastatic castrate resistant prostate cancer treatment market is expected to grow at the fastest CAGR of 24.7% from 2025 to 2032, propelled by rising cancer burden, healthcare infrastructure improvement, and increased access to innovative therapies. Countries such as China, Japan, and India are seeing substantial growth due to favorable government policies, international collaborations in cancer research, and greater availability of branded and generic treatments. The growing focus on telemedicine and precision diagnostics also supports market expansion in the region.

Japan Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The Japan metastatic castrate resistant prostate cancer treatment market is gaining traction due to its rapid adoption of advanced oncology drugs and early diagnosis protocols. Japan’s aging male population, along with national health coverage and strong pharmaceutical innovation, supports the widespread availability of enzalutamide, abiraterone, and radiotherapy options. The country’s focus on clinical efficiency and integration of real-world data into treatment evaluation also enhances therapeutic outcomes.

China Metastatic Castrate Resistant Prostate Cancer Treatment Market Insight

The China metastatic castrate resistant prostate cancer treatment market accounted for the largest revenue share in Asia-Pacific in 2024, due to a growing number of prostate cancer cases, rapid healthcare digitalization, and aggressive expansion by domestic pharma companies. With increasing access to imported and local generic drugs, government initiatives supporting cancer care reforms, and rising awareness about late-stage treatment options, China is becoming a key mCRPC market in the region. Investment in local clinical trials and biosimilar development is also contributing to its growth trajectory.

Metastatic Castrate Resistant Prostate Cancer Treatment Market Share

The metastatic castrate resistant prostate cancer treatment industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd. (Switzerland

- Teva Pharmaceutical Industries Ltd. (Ireland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- Lilly (U.S.)

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- Cipla (U.S.)

- Amneal Pharmaceuticals LLC (U.S.)

- Bausch Health Companies Inc. (Canada)

- Takeda Pharmaceutical Company Limited (Japan)

- AbbVie Inc. (U.S.)

- Merck KGaA (Germany

Latest Developments in Global Metastatic Castrate Resistant Prostate Cancer Treatment Market

- In May 2024, Bayer AG announced updated clinical trial results for Xofigo (radium Ra 223 dichloride), which demonstrated a 14% improvement in overall survival among patients with symptomatic bone-predominant mCRPC. This development underscores Bayer’s ongoing commitment to expanding therapeutic benefits for patients through radiopharmaceutical innovations. The data positions Xofigo as a key component of combination treatment regimens and is expected to significantly boost Bayer’s share in the radiotherapy segment, which accounted for 11.8% of the global market revenue in 2024

- In April 2024, Pfizer Inc. received FDA approval for the expanded indication of Talzenna (talazoparib) in combination with enzalutamide for patients with mCRPC harboring homologous recombination repair (HRR) gene mutations. This approval marks a pivotal advancement in precision oncology, offering targeted treatment options to a broader patient population. The HRR-targeted therapy segment is projected to grow at a CAGR of 19.6% from 2025 to 2032

- In March 2024, Janssen Pharmaceutical Companies of Johnson & Johnson launched A Study of Niraparib and Abiraterone Acetate (MAGNITUDE Trial) in Europe, aiming to evaluate the efficacy of the combination therapy in newly diagnosed mCRPC patients with and without HRR mutations. This strategic move is expected to enhance Janssen’s market penetration in Europe, where the company held a 16.2% market share in 2024, by addressing both biomarker-positive and biomarker-negative populations

- In February 2024, Astellas Pharma Inc. and Pfizer announced new long-term efficacy data for Xtandi (enzalutamide) from the PROSPER and PREVAIL trials. The combined findings revealed a 21% improvement in radiographic progression-free survival (rPFS) over standard of care. Xtandi continues to dominate the androgen receptor signaling inhibitor segment, which represented 34.5% of the global treatment market share in 2024, and is forecasted to retain leadership through 2032

- In January 2024, Sanofi initiated a Phase 1/2 clinical trial evaluating a first-in-class bispecific T-cell engager (BiTE) immunotherapy for metastatic prostate cancer. This move signals Sanofi’s entry into the immunotherapy domain for mCRPC, a segment currently in its early stages but projected to grow at an exponential CAGR of 25.3% due to increasing demand for durable, targeted immunologic responses

- In December 2023, Myovant Sciences and Sumitomo Pharma reported promising real-world evidence supporting Orgovyx (relugolix), a once-daily oral GnRH receptor antagonist. The data showed faster testosterone suppression compared to injectable therapies, bolstering patient adherence and reducing cardiovascular risk profiles. The oral hormone therapy segment accounted for 29.4% of the total treatment market share in 2024, and the demand for convenient dosing formats is expected to drive its growth

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.