Global Mhealth Market

Market Size in USD Billion

CAGR :

%

USD

117.40 Billion

USD

1,309.08 Billion

2025

2033

USD

117.40 Billion

USD

1,309.08 Billion

2025

2033

| 2026 –2033 | |

| USD 117.40 Billion | |

| USD 1,309.08 Billion | |

| % | |

|

Mobile Health (mhealth) Market Size

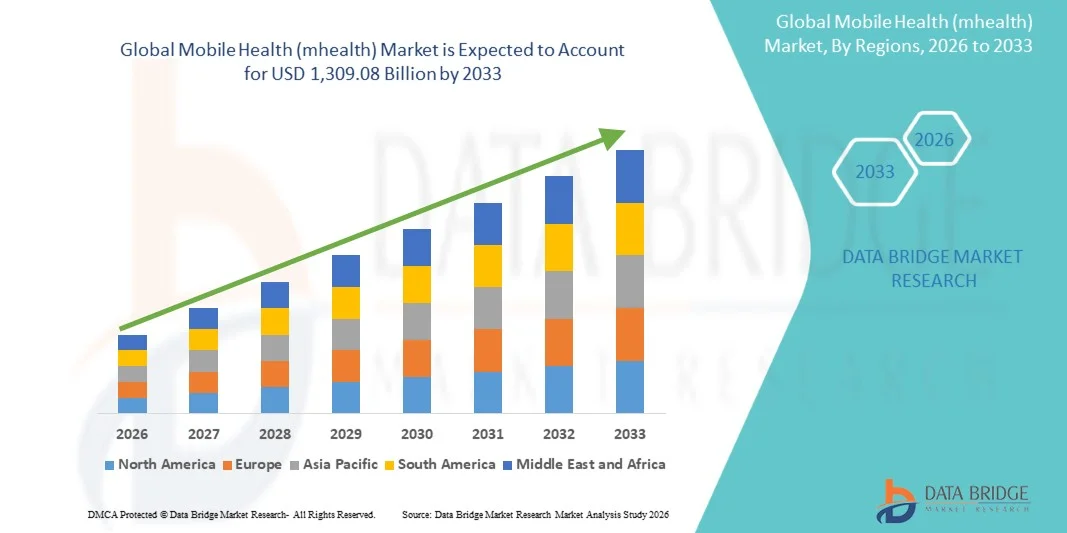

- The global mobile health (mhealth) market size was valued at USD 117.40 billion in 2025 and is expected to reach USD 1,309.08 billion by 2033, at a CAGR of 35.18% during the forecast period

- The market growth is largely fueled by the increasing adoption of digital health solutions, mobile apps, and telemedicine platforms, alongside the rapid advancement of healthcare technologies that enable real-time monitoring, diagnostics, and patient management

- Furthermore, rising patient awareness, demand for personalized healthcare, and the need for remote health monitoring solutions are driving the integration of mobile health applications in both clinical and consumer settings. These converging factors are accelerating the adoption of mHealth solutions, thereby significantly boosting the industry's growth

Mobile Health (mhealth) Market Analysis

- Mobile health (mHealth) solutions, encompassing mobile apps, wearable devices, and telemedicine platforms, are becoming essential components of modern healthcare delivery in both clinical and consumer settings due to their ability to enable real-time monitoring, remote consultations, and seamless integration with digital health ecosystems

- The escalating demand for mHealth solutions is primarily driven by the widespread adoption of smartphones and connected devices, increasing patient awareness of digital health tools, and a growing preference for convenient, personalized, and remote healthcare services

- North America dominated the mHealth market with the largest revenue share of 38.7% in 2025, supported by early adoption of digital health technologies, advanced healthcare infrastructure, high smartphone penetration, and a strong presence of leading app developers and telehealth providers, with the U.S. experiencing significant uptake of remote monitoring and telemedicine services, driven by innovations in AI, wearable integration, and real-time analytics

- Asia-Pacific is expected to be the fastest-growing region in the mHealth market during the forecast period due to rising smartphone adoption, increasing internet penetration, and government initiatives promoting digital healthcare solutions

- Remote Monitoring Services segment dominated the mHealth market with a market share of 41.5% in 2025, driven by its proven effectiveness in chronic disease management, patient engagement, and integration with wearable devices for continuous health tracking

Report Scope and Mobile Health (mhealth) Market Segmentation

|

Attributes |

Mobile Health (mhealth) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Mobile Health (mhealth) Market Trends

“AI-Driven Personalized Healthcare and Remote Monitoring”

- A significant and accelerating trend in the global mHealth market is the growing integration of artificial intelligence (AI) and machine learning into mobile health apps and wearable devices, enhancing personalized care and predictive analytics

- For instance, the HealthTap AI platform analyzes patient inputs to provide tailored health recommendations and triage guidance, while Fitbit and Apple Watch integrate AI for continuous health monitoring and predictive alerts

- AI in mHealth enables features such as predictive risk assessment for chronic diseases, automated health coaching, and intelligent notifications for medication adherence. For instance, Cardiogram uses AI to detect early signs of atrial fibrillation and other cardiac conditions from wearable data

- The seamless integration of mHealth apps with electronic health records (EHRs) and telemedicine platforms allows healthcare providers to monitor patient health remotely and intervene proactively, improving outcomes and reducing hospital visits

- This trend toward smarter, data-driven, and interconnected healthcare solutions is redefining patient expectations for mobile health services. Consequently, companies such as Ada Health are developing AI-enabled diagnostic apps that provide symptom checking and health insights based on real-time patient data

- The demand for mobile health solutions offering predictive AI and personalized monitoring is growing rapidly across both clinical and consumer sectors, as patients increasingly prioritize convenience, engagement, and continuous access to health insights

- Expansion of multilingual and culturally adaptive mHealth apps is helping reach broader patient populations, supporting global adoption and accessibility

Mobile Health (mhealth) Market Dynamics

Driver

“Increasing Adoption of Digital Health and Telemedicine Platforms”

- The rising adoption of smartphones, wearable devices, and telemedicine platforms is a significant driver for the accelerated growth of mHealth solutions

- For instance, in March 2025, Teladoc Health expanded its virtual care offerings to integrate AI-driven remote monitoring and chronic care management, enhancing patient engagement and care continuity

- As patients and providers increasingly seek accessible, cost-effective, and personalized healthcare services, mHealth apps provide real-time consultations, remote monitoring, and data-driven health insights, offering a compelling alternative to traditional care

- Furthermore, growing awareness of preventive healthcare, chronic disease management, and patient-centric care is fueling the integration of mobile health tools into daily life, supporting continuous health tracking and timely interventions

- The convenience of remote monitoring, teleconsultations, and AI-driven personalized care, along with rising healthcare digitization initiatives, is propelling mHealth adoption in both developed and emerging markets

- Rising partnerships between healthcare providers, tech companies, and insurance firms are enabling integrated care delivery through mHealth platforms, strengthening market growth

- Increasing government initiatives and digital health policies supporting telemedicine reimbursement and remote monitoring adoption are further accelerating mHealth uptake

Restraint/Challenge

“Data Privacy Concerns and Regulatory Compliance”

- Concerns surrounding data privacy, cybersecurity, and regulatory compliance pose a significant challenge to broader mHealth adoption, as apps collect sensitive health information

- For instance, high-profile breaches in mobile health apps have heightened consumer awareness and hesitancy regarding storing personal health data digitally

- Addressing these concerns through HIPAA-compliant platforms, secure encryption, and transparent privacy policies is essential for building user trust. Companies such as MyChart and Babylon Health emphasize strong data protection protocols to reassure users

- In addition, variations in healthcare regulations across countries, along with the high cost of advanced AI-enabled health apps and devices, can hinder adoption among price-sensitive users, particularly in emerging markets

- While app affordability is gradually improving, premium features such as AI diagnostics, wearable integration, and teleconsultation services often come at a higher cost, limiting accessibility

- Overcoming these challenges via enhanced cybersecurity, regulatory alignment, and cost-effective mobile health solutions will be crucial for sustained market growth

- Limited digital literacy among older adults and rural populations can restrict mHealth adoption despite available technology

- Fragmented healthcare ecosystems and lack of standardization in mobile health platforms can impede seamless integration and data interoperability across providers

Mobile Health (mhealth) Market Scope

The market is segmented on the basis of product and service, mHealth apps, medical apps, and mHealth services.

- By Product and Service

On the basis of product and service, the mHealth market is segmented into connected medical devices, mHealth apps, medical apps, and mHealth services. The connected medical devices segment dominated the market with the largest revenue share in 2025, driven by the adoption of wearable devices, smart glucometers, and remote monitoring tools for chronic disease management. Hospitals and clinics increasingly integrate these devices with telehealth platforms, enabling real-time data collection and analytics for physicians and care teams. Patients benefit from continuous monitoring, early detection of anomalies, and personalized care recommendations. The dominance is further strengthened by regulatory approvals for medical-grade devices and partnerships between device manufacturers and healthcare providers. Rising demand for home-based care and telemonitoring services also supports this segment’s growth. Continuous innovations in miniaturization, battery efficiency, and AI-driven analytics enhance usability and adoption.

The other connected medical devices segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by expanding applications in home care, fitness tracking, and preventive healthcare. Devices such as smart thermometers, portable ECG monitors, and pulse oximeters are increasingly integrated with smartphones and apps for real-time feedback. Growing consumer awareness of personal health management and self-monitoring drives adoption. Advancements in IoT connectivity, cloud-based analytics, and interoperability enhance attractiveness. Ease of use, affordability, and compatibility with Android and iOS platforms accelerate adoption further. Innovations in non-invasive monitoring and AI-assisted health insights expand application potential and market penetration.

- By mHealth Apps

On the basis of mHealth app, the mHealth market is divided into healthcare apps and medication management apps. Healthcare apps dominated the market in 2025 with the largest revenue share due to multifunctional capabilities including teleconsultation, appointment scheduling, fitness tracking, and integration with wearable devices. Consumers increasingly rely on these apps for preventive care, lifestyle management, and continuous engagement with healthcare providers. Dominance is reinforced by app store penetration, smartphone accessibility, and AI-enabled health analytics features. Partnerships between hospitals, clinics, and app developers enhance adoption for patient monitoring. Rising adoption of digital wellness programs and remote health management further strengthens the segment. Consumer demand for personalized insights and visualized health data drives preference for healthcare apps.

The medication management apps segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising awareness about medication adherence, polypharmacy, and chronic disease management. These apps provide reminders, dosage tracking, refill notifications, and interaction warnings to prevent medication errors. Integration with telehealth platforms and pharmacy services enhances utility. The increasing elderly population and patients with chronic conditions contribute to sustained demand. Regulatory encouragement for digital adherence tools and insurance support further accelerate growth. AI-driven features that optimize dosage schedules and improve adherence patterns also fuel adoption.

- Medical Apps

On the basis of medical apps, the market is segmented into medical reference apps, continuing medical education apps, patient management and monitoring apps, and communication and consulting apps. Patient management and monitoring apps dominated the market in 2025, driven by real-time health tracking, remote consultations, and integration with electronic health records (EHRs). Hospitals and clinics leverage these apps to improve workflow efficiency, care coordination, and patient outcomes. Dominance is supported by telemedicine adoption, AI-enabled analytics, and IoT integration. Providers benefit from enhanced engagement and data-driven decision-making. Innovations in usability, interface design, and secure data exchange further strengthen this segment. Consumer preference for apps providing longitudinal health monitoring also contributes to its leadership.

The communication and consulting apps segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the rising need for virtual consultations, secure provider-patient messaging, and remote collaboration among medical teams. These apps facilitate telemedicine, specialist referrals, and patient education, improving accessibility and reducing geographic barriers. High-speed internet penetration and supportive government policies enhance adoption. Integration with AI triage systems, video conferencing, and voice assistants further increases utility. Multilingual and culturally adaptive platforms expand global reach. Awareness of digital healthcare communication solutions in emerging markets further accelerates growth.

- mHealth Services

On the basis of mHealth services, the market is segmented into remote monitoring services, diagnosis and consultation services, treatment services, healthcare system strengthening services, fitness and wellness services, and prevention services. Remote monitoring services dominated the market in 2025 with a market share of 41.5%, driven by healthcare providers adopting connected devices and telehealth platforms to monitor patients remotely. Continuous data collection, real-time alerts, and AI-driven analytics improve patient safety and reduce hospitalizations. Mobile apps allow seamless communication between patients and providers, enabling timely intervention. Government support and insurance incentives for telemonitoring further boost adoption. Innovations in wearable sensor technologies and cloud-based analytics strengthen the segment. Increasing preventive healthcare awareness and patient-centric care management also contribute to demand.

The fitness and wellness services segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising consumer interest in preventive healthcare, lifestyle management, and digital fitness programs. These services include activity tracking, nutrition management, mental wellness apps, and wellness coaching delivered via mobile apps and wearable devices. Smartphone penetration, increasing health consciousness, and gamification features contribute to rapid adoption. Integration with corporate wellness programs, insurance incentives, and AI-based personalized recommendations further accelerates growth. Health awareness campaigns and social media influence drive global adoption. Continuous innovations in fitness wearables and AI-guided wellness tracking expand this segment’s application and market penetration.

Mobile Health (mhealth) Market Regional Analysis

- North America dominated the mHealth market with the largest revenue share of 38.7% in 2025, supported by early adoption of digital health technologies, advanced healthcare infrastructure, high smartphone penetration, and a strong presence of leading app developers and telehealth providers

- Consumers in the region increasingly rely on mobile health apps, connected medical devices, and remote monitoring services for chronic disease management, fitness tracking, and preventive care

- This dominance is further supported by high disposable incomes, technologically inclined populations, supportive healthcare policies, and growing integration of mHealth solutions with telemedicine platforms, establishing mobile health as a preferred solution for both individual consumers and healthcare providers in hospitals, clinics, and home care settings

U.S. Mobile Health (mhealth) Market Insight

The U.S. mHealth market captured the largest revenue share of 78% in 2025 within North America, fueled by the rapid adoption of smartphones, wearable devices, and telehealth platforms. Consumers increasingly prioritize digital health solutions for chronic disease management, fitness tracking, and preventive care. The growing preference for mobile apps, connected medical devices, and remote monitoring services further propels the mHealth industry. Moreover, integration with AI-enabled platforms, electronic health records (EHRs), and popular health apps enhances the overall user experience and clinical efficiency. Rising government support for telemedicine and remote care initiatives also contributes to market expansion. The U.S. continues to lead due to high disposable incomes, strong healthcare infrastructure, and technologically inclined consumers.

Europe Mobile Health (mHealth) Market Insight

The Europe mHealth market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by supportive healthcare policies and the increasing need for remote and digital healthcare solutions. Rising urbanization and adoption of connected medical devices are fostering growth across both residential and clinical settings. European consumers are also drawn to the convenience, real-time monitoring, and personalized health insights offered by mHealth solutions. The market is witnessing strong demand in both hospitals and home care services, with mobile health apps and remote monitoring services becoming integral to preventive and chronic care management. Innovations in secure data exchange, interoperability, and AI-based analytics further accelerate adoption. Cross-border healthcare collaborations and rising telemedicine initiatives strengthen the region’s market outlook.

U.K. Mobile Health (mHealth) Market Insight

The U.K. mHealth market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of digital health solutions and the rising adoption of mobile health apps among patients and healthcare providers. The growing focus on preventive care, chronic disease management, and teleconsultations is propelling demand. In addition, the U.K.’s robust healthcare infrastructure and regulatory support for mobile health platforms encourage adoption. Integration with wearable devices, patient monitoring apps, and AI-based analytics tools is enhancing convenience, accessibility, and clinical outcomes. The country’s thriving e-health ecosystem and growing telemedicine initiatives continue to stimulate market growth.

Germany Mobile Health (mHealth) Market Insight

The Germany mHealth market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digital health solutions and strong demand for technologically advanced healthcare services. Hospitals, clinics, and home care providers are increasingly adopting remote monitoring and telehealth services. Germany’s focus on innovation, sustainability, and privacy aligns with the adoption of secure mHealth platforms. Integration with electronic health records, AI-based diagnostics, and mobile apps enhances patient engagement and clinical efficiency. The availability of government incentives and reimbursement policies for digital healthcare solutions also supports market expansion. Consumer preference for convenience, personalized care, and preventive healthcare further drives growth.

Asia-Pacific Mobile Health (mHealth) Market Insight

The Asia-Pacific mHealth market is poised to grow at the fastest CAGR of 26% during the forecast period of 2026 to 2033, driven by increasing smartphone penetration, rising healthcare awareness, and growing adoption of wearable devices and mobile health apps. The region’s inclination towards telemedicine, remote monitoring, and preventive care is accelerating mHealth adoption. Government initiatives supporting digital health infrastructure and smart healthcare solutions are driving growth in countries such as China, Japan, and India. Moreover, APAC’s large population base, expanding middle class, and increasing urbanization are boosting market potential. Innovations in affordable mobile health platforms and AI-powered health analytics are expanding accessibility to a wider consumer base.

Japan Mobile Health (mHealth) Market Insight

The Japan mHealth market is gaining momentum due to high smartphone penetration, rapid urbanization, and increasing adoption of connected medical devices. The market places a strong emphasis on preventive care, convenience, and real-time health monitoring. Integration of mHealth apps with wearable devices, AI diagnostics, and teleconsultation platforms is driving adoption. Moreover, Japan’s aging population is likely to spur demand for easy-to-use, secure, and reliable remote health solutions. Hospitals, clinics, and home care providers are increasingly leveraging mobile health platforms to improve patient outcomes. Consumer awareness of digital health tools and government incentives further strengthen the market.

India Mobile Health (mHealth) Market Insight

The India mHealth market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rising smartphone adoption, expanding healthcare access, and increasing awareness of preventive care. Mobile health apps, remote monitoring services, and connected medical devices are increasingly being used across residential, clinical, and rural healthcare settings. Government initiatives supporting telemedicine and digital healthcare platforms are accelerating adoption. The growing middle class, rising disposable incomes, and affordability of mobile health solutions further contribute to market growth. Domestic startups and technology companies are actively innovating in AI-enabled apps and wearable health devices. India’s focus on digital health, smart cities, and accessible healthcare solutions is propelling the overall mHealth market.

Mobile Health (mhealth) Market Share

The Mobile Health (mhealth) industry is primarily led by well-established companies, including:

- Apple Inc. (U.S.)

- Samsung (South Korea)

- Teladoc Health, Inc. (U.S.)

- Medtronic (Ireland)

- Dexcom, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Omron Corporation (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Garmin Ltd. (Switzerland)

- Withings (France)

- Huawei Technologies Co., Ltd. (China)

- Xiaomi Corporation (China)

- Veradigm LLC (U.S.)

- AirStrip Technologies, Inc. (U.S.)

- AliveCor, Inc. (U.S.)

- iHealth Labs, Inc. (U.S.)

- BioTelemetry, Inc. (U.S.)

- Pear Therapeutics, Inc. (U.S.)

- Omada Health, Inc. (U.S.)

What are the Recent Developments in Global Mobile Health (mhealth) Market?

- In March 2026, Samsung and b.well Connected Health unveiled a smartphone‑based health record access feature at HIMSS26, enabling Samsung Health users to store and share their medical data via QR codes with participating healthcare providers, streamlining clinical visits and reducing administrative burden. The capability extends mobile health functionality by integrating wearable data and longitudinal patient records into one platform, aimed at replacing traditional paper intake

- In March 2025, the New Zealand government announced a national 24/7 telehealth service that provides online appointments with general practitioners and nurse practitioners, expanding mobile health accessibility and virtual care delivery across the country. This initiative reflects the growing role of national policy in expanding mHealth services beyond pilot programs into broad public healthcare access

- In February 2025, Amazon launched telehealth medical services for its Prime members, offering fixed‑price telehealth visits, treatment plans, and medication delivery, thereby leveraging its existing consumer base to expand digital health access at scale. This move signals major tech platform entry into mainstream mHealth service provision

- In January 2025, Samsung introduced a new Personal Health Records feature on its Samsung Health mobile app in India, allowing users to securely create and access their Ayushman Bharat Health Account (ABHA) and manage medical history and health data digitally. This launch enhances mHealth utility by integrating personal health records with mobile health tracking, reducing reliance on physical paperwork and improving access to comprehensive health information

- In June 2024, Dexcom announced that its G7 Continuous Glucose Monitoring (CGM) System is now directly compatible with the Apple Watch in the U.S., making it the first CGM to display real‑time glucose readings on the wrist without requiring a smartphone device. This development enhances convenience for users managing diabetes and represents a significant integration of mHealth device data with wearable technology

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.