Global Multi Cancer Early Detection Tests Market

Market Size in USD Million

USD

979.50 Million

USD

3,300.88 Million

2025

2033

USD

979.50 Million

USD

3,300.88 Million

2025

2033

| 2026 - 2033 | |

| USD 979.50 Million | |

| USD 3,300.88 Million | |

| % | |

|

Multi-Cancer Early Detection Tests Market Size

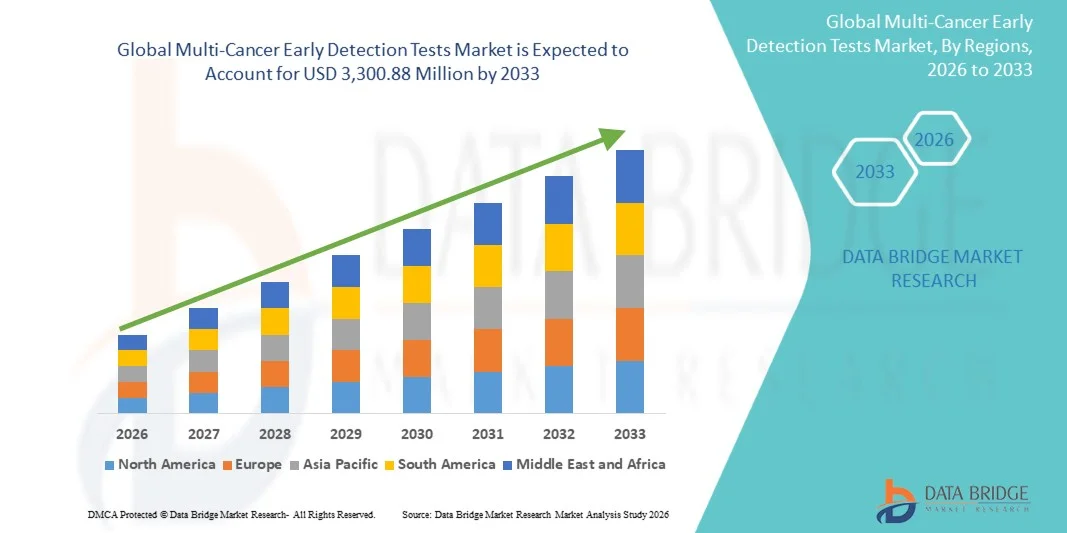

- The global multi-cancer early detection tests market size was valued at USD 979.50 million in 2025 and is expected to reach USD 3,300.88 million by 2033, at a CAGR of 16.40% during the forecast period

- The market growth is largely fueled by the expanding use of liquid biopsy technologies, advances in genomic and epigenomic profiling, and increasing adoption of precision oncology, all of which are accelerating the shift toward non-invasive cancer screening solution

- Furthermore, rising awareness of early cancer diagnosis, growing investment in multi-omics research, and the need for broad-coverage screening tools that detect multiple cancers from a single test are establishing MCED platforms as the next-generation diagnostic standard. These converging factors are rapidly boosting the uptake of MCED tests and significantly driving market expansion

Multi-Cancer Early Detection Tests Market Analysis

- Multi-cancer early detection tests, which utilize liquid biopsy and multi-omics profiling to identify multiple cancers through a single blood draw, are emerging as pivotal innovations in oncology due to their non-invasive nature, early-stage detection capabilities, and strong alignment with precision medicine across clinical and population health settings

- The rising demand for multi-cancer early detection tests is driven by the increasing global cancer burden, growing prioritization of early diagnosis, rapid advancements in genomic, epigenomic, and AI-enabled biomarker technologies, and a strong shift toward minimally invasive screening methods among patients and healthcare providers

- North America dominated the multi-cancer early detection tests market with the largest revenue share of 44.6% in 2025, supported by early adoption of liquid biopsy platforms, significant R&D investments, robust healthcare infrastructure, and the strong presence of leading diagnostic innovators, with the U.S. showing notable growth through pilot screening programs and expanding clinical partnerships focused on multi-cancer testing

- Asia-Pacific is expected to be the fastest growing region in the multi-cancer early detection tests market during the forecast period due to rising healthcare expenditure, increasing awareness of early cancer detection, rapid urbanization, and expanding availability of advanced diagnostic technologies across major countries

- Liquid biopsy tests dominated the multi-cancer early detection tests market with a market share of 67.8% in 2025, driven by their widespread clinical acceptance, simple sample collection process, and strong performance in detecting a broad range of cancers, positioning them as the leading platform for multi-cancer screening

Report Scope and Multi-Cancer Early Detection Tests Market Segmentation

|

Attributes |

Multi-Cancer Early Detection Tests Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Multi-Cancer Early Detection Tests Market Trends

“Rapid Advancement Through Multi-Omics and AI-Integrated Screening”

- A significant and accelerating trend in the global multi-cancer early detection tests market is the deepening integration of multi-omics profiling with artificial intelligence (AI) and advanced bioinformatics platforms, enabling more accurate detection of multiple cancers at early or pre-symptomatic stages through a single blood draw

- For instance, leading MCED platforms now combine genomic, epigenomic, and fragmentomic biomarkers with machine-learning algorithms to identify cancer signals across numerous organ systems with improved sensitivity and specificity, strengthening their role within precision oncology frameworks

- AI integration in multi-cancer early detection tests enables capabilities such as pattern recognition in complex molecular signatures, enhanced classification of tissue-of-origin signals, and intelligent risk-stratification alerts for clinicians; for instance, several emerging tests utilize AI to refine methylation pattern analysis and deliver more precise cancer-signal predictions over time

- The seamless integration of MCED technologies with digital health platforms and oncology workflows facilitates centralized management of patient risk assessments, longitudinal monitoring, and downstream diagnostics, creating a unified ecosystem for early detection and cancer care coordination

- This trend toward more intelligent, automated, and clinically integrated cancer detection solutions is fundamentally reshaping expectations for preventive oncology; consequently, companies are advancing AI-enabled MCED assays with improved multi-cancer coverage, streamlined reporting interfaces, and expanded compatibility with clinical decision-support tools

- The demand for MCED solutions that offer enhanced AI-driven analytical accuracy and broad multi-omics integration is growing rapidly across both clinical and population-level screening programs, as healthcare systems increasingly prioritize early detection and minimally invasive diagnostics

Multi-Cancer Early Detection Tests Market Dynamics

Driver

“Growing Need Due to Rising Cancer Burden and Advancements in Liquid Biopsy”

- The increasing global cancer burden coupled with the accelerating adoption of liquid biopsy technologies is a significant driver fueling the rising demand for multi-cancer early detection tests

- For instance, in recent years several diagnostic companies have announced major advancements in liquid biopsy and multi-omics detection platforms, integrating high-resolution sequencing and enhanced biomarker panels to strengthen early-stage cancer identification and support market expansion

- As healthcare providers prioritize early diagnosis and better patient outcomes, MCED tests offer key advantages such as non-invasive sample collection, broad cancer coverage, and the ability to detect early molecular changes, providing a compelling alternative to traditional screening methods that often target only a single cancer

- Furthermore, the growing popularity of precision medicine initiatives and the shift toward personalized screening pathways are making MCED tests an essential component of modern oncology strategies, offering seamless integration with genomic programs and digital health platforms

- The convenience of blood-based testing, remote sample collection possibilities, and the ability to support risk-based screening approaches are key factors propelling the adoption of MCED solutions across clinical settings, with expanding clinical trials and supportive research ecosystems further contributing to market growth

Restraint/Challenge

“Clinical Validation Complexity and Regulatory Compliance Hurdle”

- Concerns surrounding the clinical validation requirements and regulatory complexities associated with introducing multi-cancer early detection tests pose significant challenges to broader market penetration, as MCED platforms must demonstrate high accuracy across numerous cancer types and stages

- For instance, publicized discussions around the difficulty of validating multi-cancer assays at scale have raised caution among regulators, clinicians, and payers, increasing scrutiny about clinical utility, appropriate use cases, and performance consistency

- Addressing these concerns through large-scale clinical trials, robust analytical validation, and transparent performance reporting is crucial for establishing trust; companies emphasize validated biomarker signatures, rigorous assay design, and high assay reproducibility to reassure healthcare stakeholders

- In addition, the relatively high cost of advanced MCED tests compared to traditional single-cancer screening modalities can be a barrier to adoption for cost-sensitive healthcare systems, particularly in regions where reimbursement frameworks are still evolving or limited

- While costs are gradually expected to decline as technology matures, the perceived price premium for multi-omics and AI-enabled diagnostics may hinder widespread adoption among early-stage screening programs, especially where budget constraints limit the uptake of emerging diagnostic technologies

- Overcoming these challenges through expanded evidence generation, clearer regulatory pathways, payer engagement strategies, and the development of more cost-efficient assay designs will be vital for sustained market growth

Multi-Cancer Early Detection Tests Market Scope

The market is segmented on the basis of test, technology, sample type, and end user.

- By Test

On the basis of test, the multi-cancer early detection tests market is segmented into liquid biopsy tests, gene panels, proteomic biomarker tests, multi-omics assays, and laboratory-developed tests (LDTs). The liquid biopsy segment dominated the market in 2025 with the largest revenue share of 67.8%, driven by its strong clinical adoption and ability to detect multiple cancers from a simple blood draw. Healthcare providers increasingly prefer liquid biopsy–based MCED tests because they are non-invasive, reduce patient discomfort, and offer broad cancer coverage in a single test. Advancements in circulating tumor DNA (ctDNA), methylation signatures, and cell-free DNA analytics have strengthened the clinical performance of these tests, positioning them as the leading MCED platform. In addition, companies such as GRAIL and Exact Sciences have heavily commercialized liquid biopsy MCED solutions, reinforcing market dominance. The scalability of blood-based testing and growing integration into clinical workflows further accelerate adoption. Together, these factors make liquid biopsy the most widely utilized test type in the MCED market.

The multi-omics assays segment is anticipated to witness the fastest growth from 2026 to 2033, driven by the increasing need for highly accurate early detection using combined genomic, epigenomic, proteomic, and fragmentomic data. These assays leverage multiple biomarker layers to improve sensitivity and specificity across diverse cancer types, particularly early-stage cancers that are difficult to detect using single-modality methods. Multi-omics platforms are attractive for research institutions and commercial players aiming to broaden cancer coverage while reducing false positives. The growing integration of machine learning into multi-omics datasets further enhances detection accuracy. With rising investment from biotechnology companies and expanding clinical trials, multi-omics assays are positioned for rapid adoption. Their ability to offer comprehensive biological insights makes them the fastest-growing test category.

- By Technology

On the basis of technology, the market is segmented into DNA methylation analysis, targeted sequencing, fragmentomics, proteomics, and machine learning–based analysis. DNA methylation analysis dominated the market in 2025, supported by its proven effectiveness in detecting multiple cancer types using blood-based biomarkers. Methylation signatures provide highly stable and reproducible markers, making them ideal for MCED applications where early-stage accuracy is critical. Leading MCED products utilize methylation analysis because it enables broad biological coverage and strong tissue-of-origin prediction. The scalability of methylation sequencing technology and its successful clinical validation has further increased its adoption among diagnostic laboratories. In addition, growing research investment in epigenetic profiling continues to expand the applications of methylation-based MCED tests. As a result, DNA methylation analysis remains the most widely utilized and clinically validated technology in this market.

Machine learning–based analysis is expected to witness the fastest CAGR from 2026 to 2033, driven by its essential role in interpreting complex biomarker patterns and enhancing detection accuracy. ML algorithms enable integration of large datasets across genomic, epigenomic, fragmentomic, and proteomic inputs, allowing more precise identification of cancer-specific signals. As MCED tests become more data-intensive, AI and machine learning provide superior predictive modeling and tissue-of-origin classification. Investments from diagnostic innovators increasingly focus on AI-enabled platforms to reduce false positives and improve sensitivity. Furthermore, regulatory agencies are supporting AI-assisted diagnostic pathways, accelerating adoption. This makes machine learning–based analysis the fastest-growing technological category in the MCED landscape.

- By Sample Type

On the basis of sample type, the market is segmented into blood, urine, saliva, and stool. The blood sample segment dominated the market in 2025, driven by its non-invasive nature, ease of collection, and compatibility with liquid biopsy technologies widely used in MCED tests. Blood samples provide reliable access to circulating tumor DNA, epigenetic markers, and proteomic signatures, making them highly effective for multi-cancer detection. Clinical workflows across hospitals and diagnostic laboratories already support blood-based testing, facilitating rapid integration of MCED solutions. In addition, blood-based MCED platforms have received the most clinical validation, reinforcing physician confidence and widespread adoption. Commercial availability of blood-based MCED products from leading companies further supports scale. These advantages collectively make blood the most widely used sample type in the MCED market.

The urine segment is expected to witness the fastest growth from 2026 to 2033, supported by expanding research on urinary biomarkers for early cancer detection and patient preference for highly non-invasive sampling. Urine contains tumor-derived metabolites, DNA fragments, and proteins that can be analyzed using emerging multi-omics and epigenetic technologies. As urinary biomarker accuracy improves, developers are increasingly exploring urine-based MCED tests for cancers such as bladder, prostate, and kidney. The convenience of self-collection also positions urine as a practical option for population screening programs. Moreover, advancements in sample stabilization and molecular concentration technologies are enhancing clinical reliability. These factors make urine the fastest-growing sample type in the MCED market.

- By End User

On the basis of end user, the market is segmented into diagnostic laboratories, hospitals & health systems, physician offices, direct-to-consumer channels, and research institutes. Diagnostic laboratories dominated the market in 2025 because they serve as the primary hubs for processing MCED test samples and implementing advanced sequencing technologies. These labs possess the necessary infrastructure, such as NGS platforms and AI-enabled analytics, required for complex multi-cancer testing. Growing partnerships between MCED companies and national laboratory networks have expanded access to testing across clinical settings. Diagnostic labs also play a major role in supporting large-scale cancer screening initiatives, increasing test volumes significantly. The availability of reimbursement frameworks and established sample logistics systems further strengthens their dominance. As a result, diagnostic laboratories remain the leading end-user segment for MCED tests.

The direct-to-consumer segment is anticipated to witness the fastest growth from 2026 to 2033, driven by rising consumer awareness of early cancer detection and increasing interest in at-home health testing solutions. DTC MCED offerings allow individuals to access screening without clinical appointments, appealing to patients seeking convenience and proactive health management. Companies are increasingly exploring DTC pathways to expand market reach and reduce healthcare system bottlenecks. Advancements in telehealth and digital platforms also support seamless ordering, result delivery, and physician consultation. Growing consumer willingness to pay for preventive testing further accelerates this trend. Consequently, DTC channels represent the fastest-expanding end-user category.

Multi-Cancer Early Detection Tests Market Regional Analysis

- North America dominated the multi-cancer early detection tests market with the largest revenue share of 44.6% in 2025, supported by early adoption of liquid biopsy platforms, significant R&D investments, robust healthcare infrastructure, and the strong presence of leading diagnostic innovators

- Healthcare consumers in the region place high value on non-invasive, accurate, and comprehensive cancer screening tools that integrate seamlessly with precision medicine platforms and existing clinical workflows

- This accelerated adoption is further supported by robust healthcare investment, strong presence of leading MCED innovators, and growing demand for proactive health monitoring, establishing multi-cancer early detection tests as a preferred solution across both clinical and preventive care settings

U.S. Multi-Cancer Early Detection Tests Market Insight

The U.S. multi-cancer early detection tests market captured the largest revenue share within North America in 2025, fueled by strong adoption of liquid biopsy technologies and expanding investment in precision oncology initiatives. Healthcare providers are increasingly prioritizing early cancer detection through blood-based screening platforms capable of identifying multiple cancer types. The rising acceptance of non-invasive testing, combined with growing payor interest in preventive screening, further propels the MCED market. Moreover, increasing integration of genomic profiling, AI-driven analytics, and multi-omics workflows into routine clinical practice is significantly contributing to market expansion.

Europe Multi-Cancer Early Detection Tests Market Insight

The Europe multi-cancer early detection tests market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strict cancer screening guidelines and the region’s accelerating shift toward early diagnostic programs. Increasing urbanization and the growing demand for advanced diagnostic technologies are fostering MCED adoption. European healthcare systems are also emphasizing early detection to reduce long-term treatment costs and improve patient outcomes. The region is experiencing strong growth in both public and private healthcare settings, with MCED tests being incorporated into pilot screening studies and precision medicine initiatives.

U.K. Multi-Cancer Early Detection Tests Market Insight

The U.K. multi-cancer early detection tests market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the growing trend toward personalized medicine and the need for improved cancer screening efficiency. Rising concerns regarding late-stage cancer diagnosis are encouraging healthcare providers to adopt innovative blood-based screening solutions. The U.K.’s strong digital health infrastructure, along with robust clinical research collaborations, is expected to continue stimulating market growth.

Germany Multi-Cancer Early Detection Tests Market Insight

The Germany multi-cancer early detection tests market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cancer prevention and demand for advanced, data-driven diagnostic solutions. Germany’s well-developed healthcare infrastructure and strong emphasis on clinical innovation support the widespread adoption of MCED technologies. The integration of liquid biopsy platforms with hospital information systems is becoming increasingly prevalent, with a strong preference for accurate, privacy-focused diagnostic solutions aligned with local healthcare standards.

Asia-Pacific Multi-Cancer Early Detection Tests Market Insight

The Asia-Pacific multi-cancer early detection tests market is poised to grow at the fastest CAGR during the forecast period, driven by increasing urbanization, rising healthcare expenditure, and technological advancements in countries such as China, Japan, and India. The region’s expanding focus on early cancer detection, supported by government-led screening programs and precision medicine initiatives, is driving MCED adoption. Furthermore, as APAC strengthens its role in genomic research and diagnostic manufacturing, the affordability and accessibility of MCED tests are rapidly expanding to a broader patient population.

Japan Multi-Cancer Early Detection Tests Market Insight

The Japan multi-cancer early detection tests market is gaining momentum due to the country’s strong biomedical innovation ecosystem, rapid urbanization, and rising need for early detection solutions. The Japanese market places significant emphasis on accuracy and preventive healthcare, leading to growing adoption of liquid biopsy-based multi-cancer tests. The integration of MCED platforms with AI-powered diagnostic tools and imaging systems is fueling growth. Moreover, Japan’s aging population is likely to spur demand for early and non-invasive cancer screening solutions across both clinical and community health settings.

India Multi-Cancer Early Detection Tests Market Insight

The India multi-cancer early detection tests market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, and rising awareness of early cancer diagnosis. India stands as one of the fastest-growing markets for advanced diagnostic solutions, and MCED tests are becoming increasingly relevant across hospitals, diagnostic chains, and preventive health programs. The push toward digital healthcare, increasing accessibility of liquid biopsy technologies, and growing involvement of domestic research organizations are key factors propelling the MCED market in India.

Multi-Cancer Early Detection Tests Market Share

The Multi-Cancer Early Detection Tests industry is primarily led by well-established companies, including:

- GRAIL, Inc., (U.S.)

- Exact Sciences Corporation (U.S.)

- Guardant Health, Inc. (U.S.)

- Freenome Holdings, Inc., (U.S.)

- Burning Rock Dx (China)

- Singlera Genomics Inc., (U.S.)

- Foundation Medicine, Inc. (U.S.)

- Elypta (Sweden)

- VolitionRx (Belgium)

- CellMax Life (China)

- StageZero Life Sciences, (U.S.)

- C2i Genomics (Israel)

- ArcherDX (U.S.)

- 1drop Inc., (U.S.)

- Laboratory for Advanced Medicine, Inc., (U.S.)

- GENECAST (China)

- Prenetics Global Limited (Hong Kong)

- Quibim (Spain)

- Harbinger Health (U.S.)

- Myriad Genetics, Inc., (U.S.)

What are the Recent Developments in Global Multi-Cancer Early Detection Tests Market?

- In September 2025, Exact Sciences launched Cancerguard a new multi-cancer early detection blood test offered as a laboratory-developed test (LDT) in the U.S. The test analyses multiple biomarker classes and can detect signals from over 50 cancer types, including many cancers that often go undiagnosed until late stages

- In May 2025, Geneseeq announced results from a large-scale MCED study published in Nature Medicine for its blood-based test CanScan. The study demonstrated that CanScan® can accurately detect early-stage cancers from a simple blood draw by integrating genomic, fragmentomic and epigenomic cfDNA features

- In November 2024, DETECT-A study data shared by Exact Sciences showed that a multi-biomarker class MCED approach (combining DNA methylation, protein markers, and mutation reflex) significantly improved sensitivity for early-stage and overall cancer detection compared to prior methods. This supports combining multiple biomarker types for better MCED performance

- In January 2024, Geneseeq’s CanScan was granted a U.S. Food and Drug Administration (FDA) Breakthrough Device Designation a regulatory milestone recognizing its potential as a next-generation multi-cancer early detection solution. The test uses low-depth whole-genome sequencing of circulating cfDNA to detect cancer signals and predict tissue of origin, covering cancers for which no standard-of-care screening exists

- In April 2023, researchers presented at the American Association for Cancer Research (AACR) meeting that a liquid biopsy-based MCED test using methylation of cell-free DNA was able to detect 12 types of cancers including early-stage and low DNA-shedding cancers showing the feasibility of non-invasive early detection across a broad cancer spectrum

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.