Global Non Hodgkins Lymphoma And Chronic Lymphoma Treatment Market

Market Size in USD Billion

USD

9.97 Billion

USD

18.11 Billion

2025

2033

USD

9.97 Billion

USD

18.11 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.97 Billion | |

| USD 18.11 Billion | |

| % | |

|

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Size

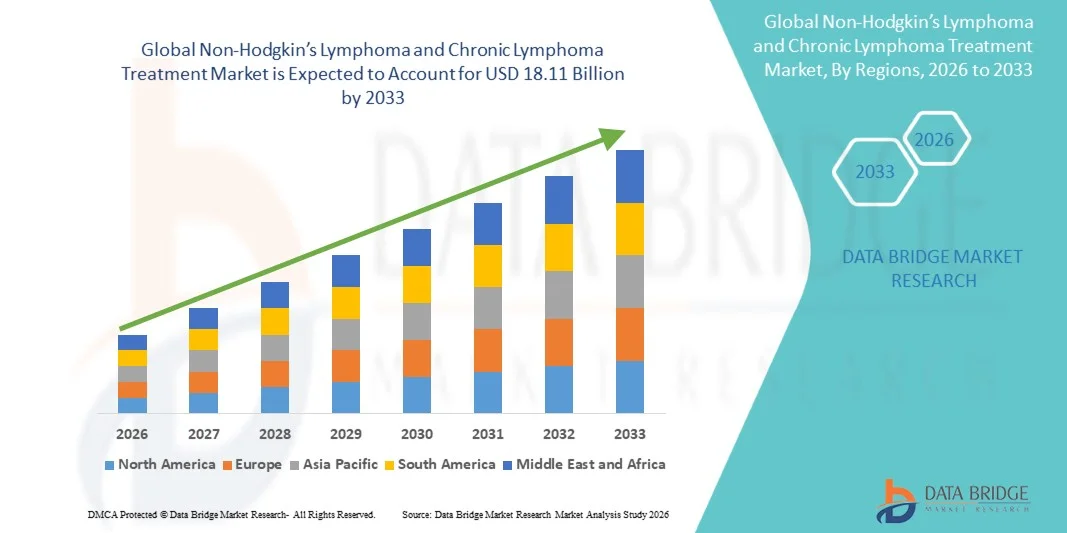

- The global Non-Hodgkin’s lymphoma and chronic lymphoma treatment market size was valued at USD 9.97 billion in 2025 and is expected to reach USD 18.11 billion by 2033, at a CAGR of 7.75% during the forecast period

- The market growth is largely driven by the increasing prevalence of lymphatic cancers, advances in targeted therapies and immunotherapies, and growing adoption of precision medicine approaches in oncology

- Furthermore, rising patient awareness, enhanced healthcare infrastructure, and supportive government initiatives for cancer care are expanding access to novel treatment options, establishing innovative therapies as the preferred choice for clinicians and patients. These converging factors are accelerating the adoption of advanced treatment modalities, thereby significantly boosting the industry's growth

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Analysis

- Non-Hodgkin’s lymphoma and chronic lymphoma treatments, including targeted therapies, immunotherapies, and combination regimens, are increasingly vital components of modern oncology care in both hospital and outpatient settings due to their improved efficacy, personalized approach, and better safety profiles

- The escalating demand for these treatments is primarily fueled by the rising prevalence of lymphatic cancers, growing awareness of advanced therapies among patients and clinicians, and a preference for precision medicine approaches over traditional chemotherapy

- North America dominated the Non-Hodgkin’s lymphoma and chronic lymphoma treatment market with the largest revenue share of 40.6% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of key pharmaceutical and biotech players, with the U.S. witnessing substantial adoption of novel therapies such as CAR-T and monoclonal antibodies, driven by continuous R&D and regulatory support for innovative cancer treatments

- Asia-Pacific is expected to be the fastest growing region in the Non-Hodgkin’s lymphoma and chronic lymphoma treatment market during the forecast period due to increasing healthcare access, government initiatives for oncology care, and rising patient awareness

- Targeted therapy segment dominated the market with a share of 42.9% in 2025, driven by its ability to selectively attack cancer cells while minimizing damage to healthy tissue, making it a preferred choice among oncologists and patients alike

Report Scope and Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Segmentation

|

Attributes |

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Trends

“Advancements in Targeted and Immunotherapies”

- A significant and accelerating trend in the global Non-Hodgkin’s lymphoma and chronic lymphoma treatment market is the increasing adoption of targeted therapies and immunotherapies, including CAR-T cell therapy, monoclonal antibodies, and bispecific antibodies, which are transforming treatment paradigms and improving patient outcomes

- For instance, CAR-T therapies such as Kymriah and Yescarta have demonstrated high response rates in relapsed or refractory lymphoma patients, establishing immunotherapy as a key treatment option alongside traditional chemotherapy

- The integration of biomarker-driven precision medicine enables therapies to be tailored to specific genetic and molecular profiles of tumors, optimizing efficacy while minimizing adverse effects. For instance, patients with CD20-positive B-cell lymphomas benefit from rituximab-based targeted regimens

- Enhanced treatment monitoring through advanced diagnostics, including liquid biopsies and minimal residual disease (MRD) assessment, allows clinicians to adapt therapies in real time, improving survival outcomes and reducing unnecessary toxicity

- This trend towards more personalized, precise, and biologically targeted treatment approaches is reshaping clinician and patient expectations, leading pharmaceutical companies such as Gilead Sciences and Roche to focus on expanding their immunotherapy pipelines

- The demand for therapies offering higher efficacy, fewer side effects, and targeted mechanisms of action is growing rapidly across both hospital and outpatient oncology care settings, as patients and providers prioritize innovative and effective treatment options

- Digital health platforms and real-world evidence collection are being leveraged to optimize treatment protocols and monitor patient outcomes, further driving innovation and adoption in the market

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Dynamics

Driver

“Increasing Prevalence of Lymphatic Cancers and Patient Awareness”

- The rising incidence of Non-Hodgkin’s and chronic lymphomas, coupled with growing patient awareness and demand for advanced therapies, is a significant driver for the expansion of the treatment market

- For instance, recent epidemiological data indicates an upward trend in lymphoma cases in North America and Europe, fueling the adoption of novel therapies such as CAR-T and antibody-drug conjugates

- As patients and clinicians increasingly seek more effective, targeted, and less toxic treatment options, therapies offering improved survival and quality of life are gaining preference over conventional chemotherapy

- Furthermore, enhanced access to healthcare infrastructure and oncology centers in emerging markets is increasing the availability and adoption of advanced lymphoma treatments

- The growing emphasis on early diagnosis, patient education programs, and government support for cancer care is further accelerating the uptake of innovative therapies across both hospital and outpatient oncology settings

- Rising investment in oncology R&D by both public and private sectors is facilitating faster development of next-generation therapies, expanding treatment options for lymphoma patients

- Increasing awareness campaigns and screening initiatives are leading to earlier diagnosis, which allows timely initiation of advanced treatments and better patient outcomes

Restraint/Challenge

“High Cost of Therapies and Limited Accessibility”

- The relatively high cost of advanced treatments, including CAR-T therapies and novel immunotherapies, poses a significant challenge to broader market adoption, particularly in low- and middle-income countries

- For instance, the list price of CAR-T therapies can exceed several hundred thousand dollars per patient, making them inaccessible for many despite their clinical benefits

- Limited treatment infrastructure, including specialized infusion centers and trained healthcare personnel, restricts access to these therapies in certain regions, delaying market penetration

- Regulatory hurdles, complex approval processes, and reimbursement constraints further impede the rapid adoption of innovative treatment options in multiple markets

- Overcoming these challenges through cost reduction strategies, expanded manufacturing capabilities, patient assistance programs, and streamlined regulatory pathways will be critical for sustained growth and accessibility in the non-Hodgkin’s and chronic lymphoma treatment market

- Side effects associated with advanced therapies, including cytokine release syndrome in CAR-T treatments, require careful monitoring and management, limiting their use in some patient populations

- Variability in healthcare policies and insurance coverage across regions creates inconsistency in treatment availability, impacting equitable access and adoption globally

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Scope

The market is segmented on the basis of treatment type, cell type, route of administration, and end user.

- By Treatment Type

On the basis of treatment type, the market is segmented into chemotherapy, immunotherapy, targeted therapy, radiation therapy, and stem cell transplant. The targeted therapy segment dominated the market with the largest revenue share of 42.9% in 2025, driven by its ability to selectively attack cancer cells while minimizing damage to healthy tissues. Targeted therapies, including monoclonal antibodies and small molecule inhibitors, are increasingly preferred by oncologists due to higher efficacy, fewer side effects, and compatibility with combination regimens. The growing number of FDA-approved targeted drugs and continuous R&D in precision oncology further strengthen its leadership in the market. Patients often favor targeted therapy for its personalized approach, improving both survival outcomes and quality of life. Pharmaceutical companies are expanding pipelines for B-cell and T-cell lymphomas, further supporting market dominance. The integration of biomarker-based patient selection enhances treatment success, driving broader adoption globally.

The immunotherapy segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by the rising adoption of CAR-T cell therapies, immune checkpoint inhibitors, and bispecific antibodies. Immunotherapy offers durable responses in relapsed or refractory lymphoma patients and has demonstrated significant clinical success in B-cell lymphomas. Ongoing clinical trials and new product approvals are expanding treatment options, especially in markets with advanced healthcare infrastructure. Increasing awareness among patients and oncologists regarding immunotherapy benefits is accelerating uptake. Government initiatives and funding for advanced oncology treatments further support rapid adoption. In addition, improvements in safety management, such as mitigating cytokine release syndrome, are making these therapies more accessible and acceptable to a broader patient population.

- By Cell Type

On the basis of cell type, the market is segmented into B-cell and T-cell lymphomas. The B-cell lymphoma segment dominated the market with the largest revenue share in 2025, due to the higher prevalence of B-cell subtypes such as diffuse large B-cell lymphoma (DLBCL) and follicular lymphoma globally. A wide range of targeted therapies, immunotherapies, and combination regimens are available for B-cell lymphomas, making them a major focus for treatment development. Clinicians often prefer established treatment protocols with proven efficacy, driving higher market penetration. In addition, robust clinical research and ongoing approval of novel agents for B-cell malignancies contribute to sustained growth. Patient awareness and early diagnosis of B-cell lymphoma also support its market dominance. Pharmaceutical companies continue to invest heavily in B-cell therapy pipelines, further consolidating their market share.

The T-cell lymphoma segment is expected to witness the fastest CAGR during the forecast period due to the rising focus on rare and aggressive T-cell subtypes, which historically had limited treatment options. Novel targeted therapies, CAR-T approaches, and clinical trials specific to T-cell malignancies are creating new opportunities. Increasing incidence of peripheral T-cell lymphomas in certain regions is driving awareness and demand for specialized treatments. Market growth is further supported by the development of combination therapies aimed at improving response rates. Adoption is particularly strong in North America and Europe, where advanced healthcare infrastructure allows access to cutting-edge therapies.

- By Route of Administration

On the basis of route of administration, the market is segmented into intravenous (IV), subcutaneous, intrathecal, intramuscular, and oral. The intravenous segment dominated the market in 2025 due to its suitability for delivering a wide range of chemotherapy, immunotherapy, and targeted therapies. IV administration allows precise dosing, controlled infusion rates, and real-time monitoring of adverse reactions. Hospitals and specialized oncology centers widely prefer IV therapies for both inpatient and outpatient treatments. Continuous innovation in infusion protocols and supportive care reduces complications and enhances patient adherence. Many novel therapies, including CAR-T and monoclonal antibodies, rely on IV administration, further consolidating market dominance. Advanced IV delivery systems also improve treatment efficiency and safety.

The oral segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing patient preference for home-based treatments and convenience of self-administration. Oral targeted therapies, such as BTK inhibitors, enable long-term treatment without frequent hospital visits. Growing awareness among patients and caregivers regarding oral treatment benefits is accelerating adoption. Pharmaceutical companies are actively developing more potent and safer oral formulations. The oral route also reduces healthcare system burden and associated costs, making it appealing in emerging markets. In addition, adherence-monitoring technologies and patient education programs support the growth of oral therapy adoption globally.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers, cancer institutes, research and academic institutes, and others. The hospitals segment dominated the market with the largest revenue share in 2025, due to well-established oncology departments, advanced treatment infrastructure, and availability of specialized healthcare professionals. Hospitals offer comprehensive care for lymphoma patients, including access to chemotherapy, targeted therapy, immunotherapy, and stem cell transplantation under a single facility. High patient volumes and advanced diagnostic capabilities support market dominance. Hospitals also benefit from collaborations with pharmaceutical companies for clinical trials and early access programs. Government funding and insurance reimbursement policies further enhance hospital-based treatment adoption.

The cancer institutes segment is expected to witness the fastest growth during the forecast period due to increasing specialization in lymphoma care and rising investment in dedicated oncology centers. Cancer institutes focus on advanced therapies, clinical trials, and precision medicine, attracting patients seeking cutting-edge treatments. The adoption of CAR-T therapies and novel immunotherapies is particularly high in these centers. Expansion of cancer institutes in emerging regions is improving access to specialized care. Strategic collaborations with biotech and pharma companies accelerate the introduction of new treatment options. Patient-centric care models and research-driven protocols drive rapid growth of this segment globally.

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Regional Analysis

- North America dominated the Non-Hodgkin’s lymphoma and chronic lymphoma treatment market with the largest revenue share of 40.6% in 2025, characterized by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of key pharmaceutical and biotech players

- Patients and clinicians in the region benefit from early access to innovative therapies, such as CAR-T cell therapy, monoclonal antibodies, and targeted small molecule inhibitors, improving treatment outcomes and survival rates

- This widespread adoption is further supported by well-established oncology centers, skilled healthcare professionals, and robust clinical research, establishing advanced lymphoma treatments as the preferred choice for both hospital and outpatient settings

U.S. Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The U.S. Non-Hodgkin’s lymphoma and chronic lymphoma treatment market captured the largest revenue share of 42% in 2025 within North America, fueled by early adoption of advanced therapies such as CAR-T, monoclonal antibodies, and targeted small molecule inhibitors. Patients and clinicians increasingly prioritize personalized and precision medicine approaches to improve survival outcomes and reduce adverse effects. The strong presence of leading pharmaceutical and biotech companies, alongside well-established oncology centers, further drives market growth. Moreover, government support, favorable reimbursement policies, and clinical trial activity contribute to the rapid introduction of innovative therapies. The growing awareness of lymphoma treatment options and early diagnosis programs is also expanding patient access to advanced care.

Europe Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The Europe market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare infrastructure, rising incidence of lymphoma, and increasing patient awareness. Government initiatives supporting oncology care, coupled with growing investment in advanced therapies, are fostering the adoption of novel treatment options. European healthcare providers emphasize combination regimens and precision therapies to improve outcomes, further driving demand. The region is witnessing significant growth across hospital and specialized cancer institute settings, with new therapies being incorporated into both first-line and relapsed treatment protocols.

U.K. Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The U.K. market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing adoption of targeted therapies and immunotherapies, alongside the rising need for patient-centric and precision oncology care. High awareness of cancer treatment advancements and supportive reimbursement frameworks encourage uptake of novel therapies. In addition, early diagnosis programs, active clinical trials, and strong research collaborations with biotech companies are enhancing patient access to innovative treatment options. The U.K.’s integrated healthcare system facilitates adoption of complex therapies such as CAR-T in both public and private hospital settings.

Germany Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The Germany market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong oncology research, and emphasis on precision medicine. German clinicians increasingly utilize targeted therapies and immunotherapies to optimize treatment outcomes, supported by well-equipped cancer centers. The country’s emphasis on innovation and clinical research drives rapid adoption of novel therapies, while patients benefit from broad access to clinical trials and personalized treatment regimens. Integration of real-world evidence and biomarker-based therapies is becoming increasingly prevalent, aligning with local expectations for effective and safe lymphoma care.

Asia-Pacific Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR of 25% during the forecast period of 2026 to 2033, driven by rising healthcare access, increasing patient awareness, and growing prevalence of lymphoma in countries such as China, Japan, and India. Government initiatives promoting oncology infrastructure and the expansion of specialized cancer institutes are accelerating adoption of advanced therapies. Furthermore, improvements in diagnostic capabilities and availability of cost-effective targeted and immunotherapy options are enhancing patient reach. The region is also witnessing increased participation in global clinical trials, supporting the introduction of novel treatment modalities.

Japan Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The Japan market is gaining momentum due to high healthcare standards, advanced research in oncology, and growing demand for innovative therapies. Patients and clinicians prioritize immunotherapies and targeted treatments to improve survival outcomes and quality of life. The country’s strong focus on precision medicine and well-developed hospital infrastructure supports adoption of complex therapies such as CAR-T and monoclonal antibodies. In addition, government reimbursement policies, active clinical trial participation, and an aging population further drive market growth. Integration of advanced diagnostics and personalized treatment plans is fueling adoption in both hospital and outpatient settings.

India Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Insight

The India market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising healthcare awareness, increasing oncology infrastructure, and growing patient population. India is witnessing expanding access to targeted therapies, immunotherapies, and combination regimens in hospitals and cancer institutes. Government initiatives promoting oncology care, coupled with the presence of cost-effective treatment options and participation in global clinical trials, are key factors propelling market growth. Increasing adoption of early diagnosis programs and patient support services further improves access to advanced lymphoma treatments. Rapid urbanization and expanding private healthcare facilities are enhancing treatment availability across residential and urban centers.

Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market Share

The Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Gilead Sciences, Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- GSK plc (U.K.)

- Seagen Inc. (U.S.)

- Incyte Corporation (U.S.)

- Eli Lilly and Company (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Spectrum Pharmaceuticals, Inc. (U.S.)

- Kyowa Kirin Co., Ltd. (Japan)

What are the Recent Developments in Global Non-Hodgkin’s Lymphoma and Chronic Lymphoma Treatment Market?

- In December 2025, the U.S. FDA approved the first CAR‑T cell therapy for marginal zone lymphoma (Breyanzi / lisocabtagene maraleucel), offering a new engineered immune‑cell option for patients with relapsed or refractory marginal zone lymphoma after prior therapies, marking a significant expansion of CAR‑T options beyond common B‑cell lymphomas

- In June 2025, the U.S. FDA approved tafasitamab (Monjuvi) in combination with lenalidomide and rituximab for relapsed or refractory follicular lymphoma, expanding its use beyond diffuse large B‑cell lymphoma and providing a new immunotherapeutic option for a common indolent NHL subtype

- In February 2025, the U.K.’s National Institute for Health and Care Excellence (NICE) recommended CAR‑T therapy lisocabtagene maraleucel (Breyanzi) for relapsed/refractory large B‑cell lymphoma, influencing treatment access across the U.K. and signaling broader acceptance of CAR‑T in public health systems

- In August 2024, the European Commission approved odronextamab (Ordspono) as a treatment for adults with relapsed/refractory follicular lymphoma and diffuse large B‑cell lymphoma (DLBCL) after at least two prior lines of systemic therapy, expanding bispecific antibody treatment options in the EU

- In April 2021, the FDA approved the antibody‑drug conjugate loncastuximab tesirine (Zynlonta) for relapsed or refractory large B‑cell lymphoma and high‑grade B‑cell lymphoma, adding another targeted therapy option for NHL patients with difficult‑to‑treat disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.