Global Ocular Migraine Market

Market Size in USD Million

USD

90.04 Million

USD

171.53 Million

2024

2032

USD

90.04 Million

USD

171.53 Million

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 90.04 Million |

Market Size (Forecast Year) |

USD 171.53 Million |

CAGR |

% |

Major Markets Players |

|

Ocular Migraine Market Size

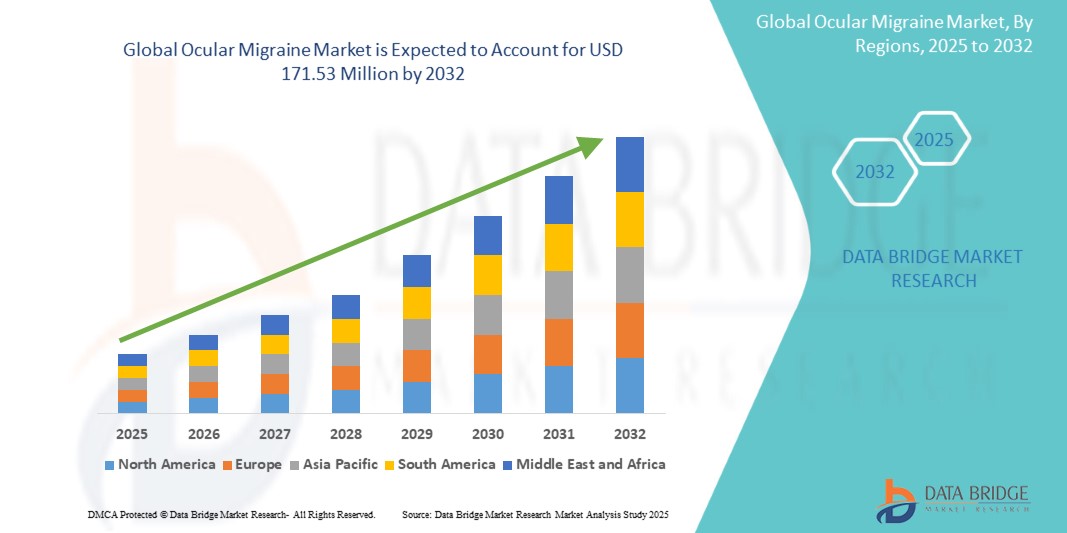

- The global ocular migraine market size was valued at USD 90.04 million in 2024 and is expected to reach USD 171.53 million by 2032, at a CAGR of 8.39% during the forecast period

- The market growth is largely fueled by the rising prevalence of migraine disorders, increased awareness of vision-related complications, and advancements in diagnostic and therapeutic approaches for ocular migraine management

- Furthermore, growing demand for effective preventive and acute treatment options, along with the availability of novel drug classes and digital health solutions, is establishing ocular migraine therapies as a crucial part of modern neurological and ophthalmic care. These converging factors are accelerating the uptake of ocular migraine treatments, thereby significantly boosting the industry’s growth

Ocular Migraine Market Analysis

- Ocular migraine, characterized by temporary visual disturbances often linked with neurological and vascular factors, is increasingly recognized within migraine management for its impact on vision and quality of life, driving demand for improved diagnostic and therapeutic approaches

- The escalating demand for ocular migraine therapies is primarily fueled by rising awareness among patients and physicians, growing incidence of migraine with visual symptoms, and the availability of advanced preventive and acute treatment modalities

- North America dominated the ocular migraine market with the largest revenue share of 45.94% in 2024, supported by advanced healthcare infrastructure, higher diagnosis rates, and strong presence of pharmaceutical innovators in neurology and ophthalmology

- Asia-Pacific is expected to be the fastest-growing region in the ocular migraine market during the forecast period, driven by expanding healthcare access, rising awareness of migraine-related vision disorders, and increasing investments in neurology and ophthalmology services

- The preventive treatment segment dominated the ocular migraine market with a market share of 62.08% in 2024, reflecting the strong demand for long-term management options that reduce attack frequency and severity

Report Scope and Ocular Migraine Market Segmentation

|

Attributes |

Ocular Migraine Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Ocular Migraine Market Trends

Advancement in Biologic Therapies and Digital Health Integration

- A significant and accelerating trend in the global ocular migraine market is the growing adoption of advanced biologic therapies, particularly CGRP inhibitors and monoclonal antibodies, alongside the integration of digital health technologies such as telemedicine platforms, mobile apps, and wearable devices for migraine tracking

- For instance, several CGRP-targeting drugs launched in recent years are demonstrating strong efficacy in reducing both frequency and severity of ocular migraine episodes, while smartphone-based applications now allow patients to log visual aura patterns, monitor triggers, and share real-time data with healthcare providers

- The combination of biologics with digital health tools enhances treatment personalization by enabling physicians to tailor therapy plans based on patient-reported data, improving adherence and long-term outcomes. Wearable devices with biosensors are also being explored to predict and alert patients ahead of migraine onset

- Digital integration also facilitates remote monitoring and teleconsultations, which are becoming increasingly important in regions with limited neurology or ophthalmology specialists, thus broadening access to advanced care

- This convergence of innovative pharmacological solutions and connected digital platforms is reshaping patient expectations, pushing the market towards more proactive, personalized, and accessible migraine care models. Companies are investing in R&D pipelines and partnerships with digital health firms to expand these capabilities

- The demand for biologic-driven prevention and digital monitoring solutions is growing rapidly across developed and emerging regions asuch as, as patients and providers prioritize convenience, early intervention, and effective long-term management of ocular migraine

Ocular Migraine Market Dynamics

Driver

Rising Prevalence of Migraine Disorders and Growing Awareness

- The increasing global burden of migraine disorders, with a significant subset presenting ocular manifestations, is a key driver fueling demand for effective diagnostic and therapeutic solutions. Rising patient awareness of vision-related migraine risks further supports market expansion

- For instance, pharmaceutical advancements in targeted therapies, combined with global awareness campaigns by neurological associations, are encouraging patients to seek earlier intervention, thereby accelerating treatment adoption

- As healthcare systems emphasize early diagnosis and integrated migraine management, ocular migraine solutions are gaining attention due to their potential to prevent progression to more severe complications

- Furthermore, the rising focus on preventive care and improved accessibility through telehealth platforms is propelling adoption of both drug-based and digital monitoring solutions across hospital, specialty clinic, and homecare settings

- Growing investments in neurology and ophthalmology research, along with the availability of advanced biologics and patient-centric treatment models, further strengthen this driver, positioning ocular migraine therapies as a crucial component of modern neurological care

Restraint/Challenge

High Treatment Costs and Underdiagnosis

- The relatively high cost of advanced biologics and targeted therapies, compared with conventional migraine treatments, poses a challenge for broader adoption, particularly in low- and middle-income countries where healthcare budgets are constrained

- For instance, while CGRP inhibitors show strong clinical efficacy, their premium pricing limits accessibility for many patients, leading healthcare providers in some regions to rely on traditional analgesics or triptans

- Another key challenge is underdiagnosis, as ocular migraines are often misinterpreted as vision problems or other neurological conditions, delaying proper treatment. Limited specialist availability in emerging markets further exacerbates this issue

- Addressing these challenges will require expanding reimbursement frameworks, reducing therapy costs, and implementing widespread awareness campaigns to improve early diagnosis rates

- In addition, partnerships between pharmaceutical innovators and digital health companies can play a role in lowering costs and increasing access to affordable, technology-enabled care pathways

- Overcoming these barriers through improved affordability, awareness, and accessibility will be vital for the sustained growth of the global ocular migraine market

Ocular Migraine Market Scope

The market is segmented on the basis of type of migraine, severity, type of treatment, end user, and distribution channel.

- By Type of Migraine

On the basis of type, the ocular migraine market is segmented into chronic migraine, intermittent migraine, and retinal migraine. The chronic migraine segment dominated the market with the largest revenue share in 2024, as these patients experience headaches and vision-related disturbances on 15 or more days per month, leading to higher medical intervention needs. Chronic migraine patients typically require both preventive and acute treatments, creating a sustained demand for therapies such as CGRP inhibitors, triptans, and monoclonal antibodies. The economic burden associated with chronic migraine management further drives innovation and adoption of effective treatments, while strong physician focus on this category keeps it dominant. Growing awareness programs and diagnostic guidelines also support higher detection and treatment rates in this segment.

The retinal migraine segment is expected to witness the fastest growth from 2025 to 2032, driven by rising recognition of visual symptoms such as temporary vision loss or scotomas linked to migraine attacks. Improvements in ophthalmology-based diagnostic tools are enabling earlier identification of retinal migraines, supporting treatment initiation at an earlier stage. Research investments are increasing into specialized biologics and neurovascular-targeted drugs to manage this rare but impactful condition. Rising patient education and medical campaigns are also reducing underdiagnosis, pushing adoption rates upward. The integration of AI-enabled ophthalmic imaging for diagnosis is another growth catalyst for this segment.

- By Severity

On the basis of severity, the ocular migraine market is segmented into mild, moderate, and severe. The moderate severity segment accounted for the largest market share in 2024, as most diagnosed ocular migraine cases fall within this category, requiring a combination of symptomatic and preventive management. Patients with moderate severity often seek frequent clinical consultations and drug therapy, creating strong demand in hospitals and specialty clinics. Physicians usually prescribe preventive CGRP inhibitors or acute triptans to manage recurring visual aura and headaches, contributing to consistent pharmaceutical revenue. The moderate severity group also forms the focus of clinical studies, ensuring better therapeutic guidelines and patient outcomes. Insurance coverage and growing treatment adherence further consolidate this segment’s dominance.

The severe segment is expected to grow at the fastest CAGR during the forecast period, as more patients report debilitating symptoms such as temporary blindness or severe ocular disturbances requiring urgent care. Advancements in biologics, including novel CGRP monoclonal antibodies, are providing new solutions for patients unresponsive to traditional therapies. Awareness among neurologists and ophthalmologists is improving, leading to earlier identification of severe cases. Furthermore, lifestyle factors such as stress and poor sleep quality are increasing the prevalence of severe forms, boosting treatment uptake. Demand for innovative, high-cost therapies in this category makes it the most attractive growth segment.

- By Type of Treatment

On the basis of treatment, the ocular migraine market is segmented into acute treatments and preventive treatments. The preventive treatment segment held the largest revenue share of 62.08% in 2024, supported by the growing use of CGRP inhibitors, antidepressants, beta-blockers, and anti-seizure medications to reduce migraine frequency and severity. Preventive treatments are increasingly recommended for patients with chronic or moderate-to-severe ocular migraines, as they minimize long-term disability and healthcare costs. Strong R&D pipelines and FDA approvals for novel biologics further strengthen this segment’s dominance. Patient adherence to preventive regimens is improving with physician guidance and digital monitoring tools, creating sustained demand. The rise in long-term management programs also highlights the strategic importance of this segment.

The acute treatment segment is expected to witness the fastest growth during forecast period, driven by the urgent demand for therapies that provide rapid relief during active migraine attacks. Triptans, NSAIDs, and newer non-invasive devices (such as neuromodulation systems) are gaining popularity for immediate symptom management. Increasing awareness about early intervention to avoid migraine progression is further fueling demand. Many patients prefer acute treatments for occasional or intermittent migraines, which increases adoption across retail and online pharmacies. With ongoing innovation in fast-acting delivery systems, this segment is set to expand significantly during the forecast period.

- By End User

On the basis of end user, the ocular migraine market is segmented into hospitals, specialty clinics, and homecare. The hospitals segment dominated the market in 2024, due to the availability of advanced diagnostic imaging tools, neurologists, and ophthalmologists capable of identifying ocular migraines with precision. Hospitals often serve as the first point of care for patients experiencing severe or frequent episodes, thereby capturing significant patient volume. Access to advanced biologics and specialized treatments is higher in hospital settings, strengthening their dominance. Furthermore, hospitals maintain collaborations with pharmaceutical companies for clinical trials, supporting innovation adoption. The integration of tele-neurology services in hospitals also enhances follow-up care for ocular migraine patients.

The homecare segment is projected to grow at the fastest rate during forecast period, driven by increasing adoption of telemedicine platforms, wearable monitoring devices, and at-home drug delivery programs. Patients are increasingly seeking convenience and cost-effective management for recurring ocular migraines, reducing dependence on frequent hospital visits. E-pharmacies and digital therapeutics enable patients to access preventive and acute therapies at home. The COVID-19 pandemic accelerated the shift toward home-based management, which continues to persist. Rising awareness about lifestyle modifications and digital self-management tools further enhances this segment’s growth potential.

- By Distribution Channel

On the basis of distribution channel, the ocular migraine market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment accounted for the largest market share in 2024, as most biologics, monoclonal antibodies, and advanced migraine therapies are prescribed and dispensed through hospital networks. Hospital pharmacies maintain close links with neurologists and ophthalmologists, ensuring precise therapy management and adherence. They are also primary suppliers for inpatient and outpatient migraine care programs. With hospitals often serving as trial centers for novel drugs, their pharmacies remain the primary distribution hub. The trust factor and physician-driven prescriptions further reinforce the dominance of hospital pharmacies in this market.

The online pharmacies segment is expected to grow at the fastest CAGR during forecast period, fueled by the rapid adoption of digital health ecosystems and e-commerce platforms offering migraine therapies. Patients increasingly prefer the convenience of doorstep delivery and subscription-based refills for preventive medications. Online pharmacies also enhance access for patients in remote or underserved regions, expanding treatment reach. Rising smartphone penetration and favorable regulatory frameworks are further encouraging the growth of e-pharmacies. Cost discounts, patient support apps, and integration with telemedicine consultations strengthen this segment’s rapid expansion.

Ocular Migraine Market Regional Analysis

- North America dominated the ocular migraine market with the largest revenue share of 45.94% in 2024, supported by advanced healthcare infrastructure, higher diagnosis rates, and strong presence of pharmaceutical innovators in neurology and ophthalmology

- Patients in the region benefit from strong access to neurologists, ophthalmologists, and specialty migraine clinics, along with the availability of FDA-approved migraine therapies

- The rising prevalence of migraine-related disorders, coupled with lifestyle stress and genetic predisposition, further fuels demand for effective management solutions. Insurance coverage and reimbursement policies for migraine treatment in the U.S. and Canada also enhance treatment uptake, making North America a key growth hub for the ocular migraine market

U.S. Ocular Migraine Market Insight

The U.S. ocular migraine market captured the largest revenue share of 80% in 2024 within North America, driven by high awareness, advanced diagnostic capabilities, and widespread availability of migraine-specific therapies. Patients increasingly seek specialized neurological and ophthalmological care for ocular migraines, supported by strong reimbursement frameworks. The growing demand for innovative acute and preventive treatments, along with adoption of digital health tools for symptom tracking, further enhances market growth. Moreover, a rising prevalence of stress-related migraines and the presence of leading pharmaceutical players make the U.S. the primary driver of regional expansion.

Europe Ocular Migraine Market Insight

The Europe ocular migraine market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising healthcare investments and growing awareness about migraine-related visual disturbances. An increase in neurological consultations and preventive care adoption is fostering treatment uptake. European patients are also adopting telemedicine platforms for migraine management, enhancing accessibility. The market is witnessing significant adoption across hospitals, specialty clinics, and homecare settings, with governments emphasizing early diagnosis and patient education campaigns to reduce migraine-related disability.

U.K. Ocular Migraine Market Insight

The U.K. ocular migraine market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by rising cases of migraine disorders and heightened awareness of their ocular manifestations. Growing reliance on both acute and preventive therapies, along with the NHS initiatives aimed at improving migraine diagnosis and care, strengthens the market. Concerns around productivity loss due to migraines are also driving demand for effective treatment solutions. The U.K.’s adoption of e-pharmacy channels further expands access to migraine medications.

Germany Ocular Migraine Market Insight

The Germany ocular migraine market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare infrastructure, early adoption of advanced treatment options, and increasing research in neurological disorders. The German market emphasizes evidence-based care and prevention strategies, with patients increasingly favoring prescription therapies over self-medication. Integration of ocular migraine management into digital healthcare apps and insurance-covered treatments further boosts adoption. Germany’s focus on innovation and patient-centric solutions supports the steady expansion of this market.

Asia-Pacific Ocular Migraine Market Insight

The Asia-Pacific ocular migraine market is poised to grow at the fastest CAGR of nearly 25% during the forecast period of 2025 to 2032, driven by rising prevalence of migraine-related disorders and growing healthcare access in countries such as China, Japan, and India. Increasing urbanization, stress levels, and lifestyle-related triggers are contributing to higher patient volumes. Government-led health awareness programs, along with expanded availability of preventive and acute migraine treatments, are accelerating adoption. Affordability of generic drugs and telehealth platforms further support market expansion across APAC.

Japan Ocular Migraine Market Insight

The Japan ocular migraine market is gaining momentum due to the country’s strong healthcare infrastructure, advanced diagnostic practices, and cultural emphasis on early treatment of neurological disorders. The rising prevalence of migraines linked to stress and screen exposure is driving demand for effective therapies. Integration of digital health platforms for migraine tracking and access to specialized migraine clinics further enhances care delivery. Japan’s aging population also increases demand for preventive treatment approaches to reduce long-term migraine impact.

India Ocular Migraine Market Insight

The India ocular migraine market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to its growing patient base, expanding middle-class population, and increasing healthcare awareness. Rising stress levels, lifestyle changes, and higher diagnosis rates of migraines are fueling market growth. India’s strong domestic pharmaceutical sector and wide availability of cost-effective treatments enhance patient access. Government initiatives for digital health and telemedicine further support the ocular migraine care ecosystem, making India a key growth hub within the APAC region.

Ocular Migraine Market Share

The Ocular Migraine industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Lilly USA, LLC (U.S.)

- Amgen Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- H. Lundbeck A/S (Denmark)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- Bayer AG (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- AstraZeneca (U.K.)

- Merck & Co., Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Biohaven Ltd. (U.S.)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Hikma Pharmaceuticals PLC (U.K.)

What are the Recent Developments in Global Ocular Migraine Market?

- In June 2025, AbbVie announced full results from the Phase 3 TEMPLE study, showing that atogepant (Qulipta/Aquipta) outperformed topiramate in both efficacy and tolerability for migraine prevention, reinforcing its position as a reliable, once-daily CGRP antagonist

- In May 2025, the FDA approved Brekiya, a self-administered DHE auto-injector, for the treatment of acute migraine and cluster headaches in adults marking a groundbreaking advancement in patient-controlled, rapid-onset migraine care

- In April 2025, the FDA approved Atzumi, the first and only nasal powder formulation of dihydroergotamine (DHE), for the acute treatment of migraine with or without aura, offering patients a convenient, powder-based alternative to traditional DHE delivery

- In January 2025, the FDA approved Symbravo (a fixed-dose combination of meloxicam and rizatriptan) for the acute treatment of migraine with or without aura in adults providing a novel oral therapy that delivers rapid and sustained relief from migraine attack

- In November 2021, Biohaven Pharmaceutical entered into a strategic collaboration with Pfizer to commercialize rimegepant and zavegepant outside the U.S., leveraging Pfizer’s global commercial infrastructure while allowing Biohaven to continue R&D dominance in the U.S. This alliance includes an upfront payment of USD 500 million and milestone-based royalties, aimed at accelerating global access to these CGRP-targeted migraine treatments and potentially establishing a new standard of care for migraine management

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.