Global Osteosynthesis Devices Market

Market Size in USD Billion

USD

9.47 Billion

USD

16.64 Billion

2025

2033

USD

9.47 Billion

USD

16.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.47 Billion | |

| USD 16.64 Billion | |

| % | |

|

Osteosynthesis Devices Market Overview

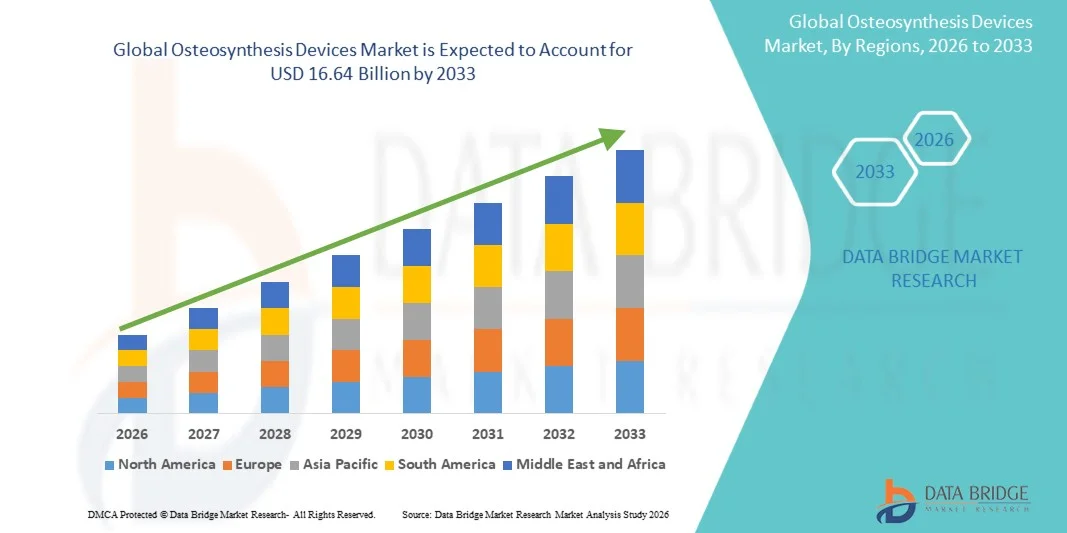

The Osteosynthesis Devices Market was valued at USD 9.47 billion in 2025 and is projected to reach USD 16.64 billion by 2033, growing at a CAGR of 7.30% from 2026 to 2033. Market growth is supported by the rising incidence of orthopedic fractures due to road traffic accidents, sports injuries, and falls among the aging population, alongside increasing adoption of advanced fixation technologies across trauma and orthopedic surgery settings.

The growing preference for minimally invasive surgical techniques, combined with improved patient outcomes, reduced hospital stays, and faster recovery times associated with modern osteosynthesis devices, is driving increased adoption among both patients and orthopedic surgeons. Ongoing technological advancements in osteosynthesis systems, including the development of bioabsorbable implants, anatomically contoured locking plates, and patient-specific instrumentation, are expanding the clinical applicability of osteosynthesis devices across trauma surgery, spinal fixation, and reconstructive orthopedics. In addition, growing healthcare infrastructure investments in emerging markets and the expansion of orthopedic specialty clinics are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Osteosynthesis Devices Market with the largest revenue share of 38.6% in 2025, supported by high procedural volumes, advanced healthcare infrastructure, and the presence of leading orthopedic device manufacturers.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.45% from 2026 to 2033, driven by expanding healthcare infrastructure, rising geriatric population, and increasing demand for orthopedic trauma care.

- The Non-Degradable segment led the material category with a 72.8% market share in 2025, reflecting the widespread clinical use of titanium and stainless-steel implants for permanent fracture fixation across trauma and reconstructive orthopedics.

- The Degradable segment is anticipated to be the fastest-growing material category, driven by increasing adoption of bioabsorbable implants that eliminate the need for secondary removal surgeries and improve patient outcomes.

- The Internal Fixation segment dominated the type category with a 78.4% market share in 2025, supported by clinical preference for plates, screws, intramedullary nails, and wires in fracture stabilization procedures.

- The External Fixation segment is expected to witness strong growth during the forecast period, driven by increasing use in complex trauma cases, limb lengthening procedures, and open fracture management.

- The Hospitals segment dominated the end-user category with a 65.7% market share in 2025, supported by access to advanced surgical facilities, multidisciplinary orthopedic teams, and comprehensive perioperative care infrastructure.

- The Orthopedic Specialist Clinic segment is expected to witness strong growth during the forecast period, driven by increasing outpatient orthopedic procedures, cost-effective care delivery, and rising patient preference for specialized treatment centers.

Market Size & Forecast

- Global Market Value (2025): USD 9.47 Billion

- Expected Market Value (2033): USD 16.64 Billion

- Forecast CAGR (2026–2033): 7.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Osteosynthesis Devices Market Segmentation

|

Attributes |

Osteosynthesis Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Johnson & Johnson and its affiliates (U.S.) · Stryker (U.S.) · Zimmer Biomet (U.S.) · Smith+Nephew (U.K.) · Medtronic plc (Ireland) · B. Braun SE (Germany) · Globus Medical Inc. (U.S.) · NuVasive Inc. (U.S.) · Arthrex Inc. (U.S.) · Integra LifeSciences Corporation (U.S.) · Acumed LLC (U.S.) · Orthofix Medical Inc. (U.S.) |

|

Market Opportunities |

· Expansion of bioabsorbable osteosynthesis devices reducing the need for secondary implant removal surgeries and improving patient convenience · Development of patient-specific implants and 3D-printed osteosynthesis systems enabling personalized fracture fixation and improved anatomical fit |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Osteosynthesis Devices Market Trends

Trend: Advancement of Bioabsorbable and Patient-Specific Implant Technologies

Clinical adoption of osteosynthesis devices continues to accelerate as technological innovations improve implant design, material science, and surgical precision. Bioabsorbable implants manufactured from poly-L-lactic acid (PLLA), polyglycolic acid (PGA), and magnesium-based alloys are gaining clinical acceptance, eliminating the need for secondary removal surgeries and reducing long-term implant-related complications. Patient-specific instrumentation and 3D-printed anatomically contoured plates enable improved fracture reduction, enhanced biomechanical stability, and faster bone healing.

For instance,

Bioretec Ltd. has advanced magnesium-based bioabsorbable implants that degrade naturally within the body while promoting bone regeneration, addressing a significant unmet clinical need in pediatric orthopedics and sports medicine applications.

In addition, research demonstrates that anatomically precontoured locking plates reduce intraoperative contouring time and improve fracture fixation accuracy compared to conventional straight plates, supporting broader clinical adoption across trauma surgery and reconstructive orthopedics.

Osteosynthesis Devices Market Dynamics

Key Market Driver: Rising Incidence of Orthopedic Fractures and Trauma Cases

The increasing prevalence of orthopedic fractures resulting from road traffic accidents, sports injuries, workplace incidents, and falls among the aging population is a primary driver of market growth. Osteosynthesis devices enable stable fracture fixation, facilitate early mobilization, and improve functional outcomes compared to conservative management approaches. The growing geriatric population, which is more susceptible to fragility fractures due to osteoporosis and reduced bone density, is expanding the patient population requiring orthopedic surgical intervention.

For instance,

According to the International Osteoporosis Foundation, osteoporotic fractures affect approximately 1 in 3 women and 1 in 5 men over the age of 50, with hip fractures alone expected to increase from 1.6 million in 2000 to 6.3 million by 2050 globally, demonstrating significant clinical demand for osteosynthesis devices. Rising fracture incidence is expected to strengthen adoption of advanced fixation technologies globally.

Key Restraint/Challenge: High Cost of Advanced Osteosynthesis Systems

The substantial cost associated with advanced osteosynthesis devices, including locking plate systems, bioabsorbable implants, and patient-specific instrumentation, presents a significant barrier to adoption, particularly in price-sensitive markets and resource-limited healthcare settings. The total procedural cost, including implants, surgical instrumentation, and postoperative care, can limit access to optimal fixation technologies for certain patient populations.

For instance,

Healthcare systems in emerging markets often face budget constraints that limit procurement of advanced titanium locking plate systems and bioabsorbable implants, resulting in continued reliance on conventional stainless steel fixation devices despite their clinical limitations. High implant costs may constrain adoption, particularly among budget-sensitive healthcare providers and underinsured patient populations.

Key Market Opportunity: Expansion into Emerging Markets and Ambulatory Surgical Settings

The development of cost-effective osteosynthesis systems and modular surgical instrumentation is creating opportunities for market expansion beyond traditional hospital settings. Ambulatory surgical centers are increasingly incorporating minimally invasive fracture fixation procedures for appropriate cases. Simultaneously, expanding healthcare infrastructure in Asia-Pacific, Latin America, and the Middle East is driving demand for orthopedic trauma care capabilities in previously underserved markets.

For instance,

The global orthopedic trauma devices market is projected to experience sustained growth driven by increasing trauma volumes, expanding outpatient surgical capabilities, and improving reimbursement frameworks in emerging economies. Healthcare infrastructure investments in India, China, and Brazil are enabling establishment of specialized orthopedic centers equipped with advanced osteosynthesis technologies.

Osteosynthesis Devices Market Scope

The osteosynthesis devices market is segmented on the basis of material, type, fracture type, and end user.

By Material

On the basis of material, the Osteosynthesis Devices Market is segmented into degradable and non-degradable. The non-degradable segment dominated the market with a 72.8% market share in 2025, The non-degradable segment's leadership reflects the widespread clinical use of titanium alloy and stainless steel implants for permanent fracture fixation across trauma surgery, spinal fusion, and reconstructive orthopedics. Titanium implants offer superior biocompatibility, corrosion resistance, and mechanical strength, making them the preferred choice for load-bearing applications and complex fracture patterns.

The degradable segment is expected to witness the fastest growth at a CAGR of 10.25% from 2026 to 2033, driven by increasing adoption of bioabsorbable implants manufactured from PLLA, PGA, and magnesium-based alloys. Bioabsorbable osteosynthesis devices eliminate the need for secondary removal surgeries, reduce long-term implant-related complications, and improve patient convenience. Growing clinical evidence supporting the mechanical performance and bone healing properties of degradable implants is expanding their applicability in pediatric orthopedics, sports medicine, and craniomaxillofacial surgery.

By Type

On the basis of type, the Osteosynthesis Devices Market is segmented into internal and external fixation. The internal fixation segment dominated the market with a 78.4% market share in 2025, while the external fixation segment accounted for the remaining 21.6% market share. The internal fixation segment's dominance reflects clinical preference for plates, screws, intramedullary nails, wires, and pins in fracture stabilization procedures. Internal fixation devices provide anatomical reduction, rigid stabilization, and early mobilization, improving functional outcomes across trauma surgery, joint reconstruction, and spinal fusion applications.

The external fixation segment is expected to witness robust growth at a CAGR of 8.15% from 2026 to 2033, driven by increasing use in complex trauma cases, open fractures, limb lengthening procedures, and deformity correction. External fixators provide versatile fracture stabilization while allowing wound access and soft tissue management in contaminated or compromised surgical sites. Technological advancements in circular and hybrid external fixation systems are improving clinical outcomes and expanding applications in pediatric orthopedics and reconstructive surgery.

By Fracture Type

On the basis of fracture type, the Osteosynthesis Devices Market is segmented into patella, tibia or fibula or ankle, clavicle, scapula or humerus, radius or ulna, hand, wrist, vertebral column, pelvis, hip, femur, foot bones, and others. The hip segment dominated the market with a 19.8% market share in 2025. The hip segment's leadership reflects the high incidence of hip fractures among the aging population, particularly fragility fractures resulting from osteoporosis, and the clinical necessity for stable fixation using dynamic hip screws, intramedullary nails, and cannulated screw systems.

The vertebral column segment is expected to witness the fastest growth at a CAGR of 9.85% from 2026 to 2033, driven by rising incidence of spinal trauma, degenerative spinal conditions, and vertebral compression fractures requiring surgical stabilization. Increasing adoption of minimally invasive spinal fusion techniques and pedicle screw systems is expanding the addressable market for vertebral osteosynthesis devices. Growing prevalence of osteoporotic vertebral fractures among the geriatric population further supports segment growth.

By End User

On the basis of end user, the Osteosynthesis Devices Market is segmented into hospitals, orthopedic specialist clinic, and others. The hospitals segment dominated the market with a 65.7% market share in 2025. The hospitals segment's dominance is supported by access to advanced surgical facilities, multidisciplinary orthopedic teams, emergency trauma care capabilities, and comprehensive perioperative infrastructure. Hospitals serve as primary centers for complex fracture fixation procedures requiring inpatient monitoring, intensive care support, and rehabilitation services.

The orthopedic specialist clinic segment is expected to witness the fastest growth at a CAGR of 9.20% from 2026 to 2033, driven by increasing outpatient orthopedic procedures, cost-effective care delivery, and rising patient preference for specialized treatment centers. Orthopedic specialist clinics offer focused expertise, shorter waiting times, and personalized care for appropriate fracture cases suitable for ambulatory surgical management. Growing payer acceptance of outpatient orthopedic procedures and favorable reimbursement policies support segment expansion.

Osteosynthesis Devices Market Regional Analysis

North America dominated the osteosynthesis devices market with a revenue share of 38.6% in 2025, supported by high procedural volumes, advanced healthcare infrastructure, favorable reimbursement frameworks, and the presence of leading orthopedic device manufacturers. Established clinical training programs, extensive surgeon experience with advanced fixation technologies, and strong patient awareness contribute to regional market leadership.

U.S. Osteosynthesis Devices Market Insight

The U.S. osteosynthesis devices market, holding a dominant 82.4% share within North America in 2025, benefits from the highest procedural volumes for orthopedic trauma surgery globally, extensive surgeon training programs, and strong clinical evidence supporting advanced fixation technologies. Academic medical centers, large health systems, and specialty orthopedic practices continue to expand trauma surgery programs utilizing locking plate systems, intramedullary nails, and bioabsorbable implants. Favorable Medicare and commercial payer reimbursement supports procedural volumes and equipment investment.

Europe Osteosynthesis Devices Market Insight

The Europe osteosynthesis devices market remains a major contributor, with strong hospital-based orthopedic surgery programs across Germany, the U.K., France, and Italy. Growing adoption of anatomically contoured locking plates and minimally invasive fixation techniques is improving surgical outcomes and reducing recovery times. Cross-disciplinary clinical guidelines and structured training pathways are standardizing care delivery across the region.

U.K. Osteosynthesis Devices Market Insight

The U.K. osteosynthesis devices market, accounting for a 14.8% share within Europe in 2025, is characterized by expanding orthopedic trauma programs within NHS hospitals and private healthcare facilities. Investment in advanced fixation technologies for hip fracture management, spinal stabilization, and extremity trauma is improving patient access to optimal surgical care and reducing surgical waiting times.

Germany Osteosynthesis Devices Market Insight

Germany's robust hospital infrastructure and advanced surgical capabilities support comprehensive orthopedic trauma programs across academic medical centers and specialized orthopedic hospitals. Germany held the largest share within Europe at 23.6% in 2025. Strong clinical training networks, favorable reimbursement frameworks, and established relationships with leading device manufacturers contribute to high procedure volumes and technology adoption.

Asia-Pacific Osteosynthesis Devices Market Insight

The Asia-Pacific osteosynthesis devices market is poised for rapid growth with a CAGR of 9.45% during the forecast period, driven by expanding healthcare infrastructure, rising geriatric population, increasing road traffic accidents, and growing demand for orthopedic trauma care. Private healthcare systems in China, Japan, India, and South Korea are investing in advanced orthopedic surgical capabilities to meet growing patient demand and improve clinical outcomes.

Japan Osteosynthesis Devices Market Insight

The Japan osteosynthesis devices market, holding a 21.5% share within Asia-Pacific in 2025, benefits from advanced healthcare infrastructure, strong surgeon expertise, and favorable reimbursement for orthopedic procedures. Hip fracture management and spinal fusion procedures are well-established, with expanding applications in minimally invasive trauma surgery and bioabsorbable implant technologies.

China Osteosynthesis Devices Market Insight

The China osteosynthesis devices market is expected to grow at the fastest rate within Asia-Pacific at a CAGR of 11.20% from 2026 to 2033, driven by healthcare modernization initiatives, expanding hospital networks, and increasing trauma volumes from road traffic accidents and industrial injuries. Domestic orthopedic device manufacturing is complementing imported platforms, improving market accessibility and price competitiveness.

Osteosynthesis Devices Market Share

The osteosynthesis devices industry is primarily led by well-established companies, including:

- Johnson & Johnson and its affiliates (U.S.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Smith+Nephew (U.K.)

- Medtronic plc (Ireland)

- Braun SE (Germany)

- Globus Medical Inc. (U.S.)

- NuVasive Inc. (U.S.)

- Arthrex Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- Acumed LLC (U.S.)

- Orthofix Medical Inc. (U.S.)

Latest Developments in Osteosynthesis Devices Market

- In March 2026, Stryker Corporation announced the acquisition of Inari Medical Inc. for approximately USD 6 billion, expanding its portfolio in interventional technologies and strengthening its position in the broader medical devices market. The acquisition supports Stryker's strategy to diversify its product offerings beyond orthopedic trauma devices.

- In January 2026, Zimmer Biomet Holdings Inc. received U.S. FDA 510(k) clearance for its next-generation Variable Angle Locking Compression Plate system designed for complex periarticular fractures. The system incorporates advanced polyaxial locking technology enabling surgeons to achieve optimal screw trajectory in challenging anatomical regions.

- In November 2025, Smith+Nephew announced the launch of its EVOS WRIST Plating System, a comprehensive anatomically contoured plate system for distal radius fractures. The system offers multiple plate configurations and fragment-specific fixation options to address diverse fracture patterns.

- In September 2025, Johnson & Johnson announced the completion of its acquisition of Shockwave Medical Inc., expanding its interventional technology portfolio and strengthening its position in cardiovascular and peripheral vascular intervention markets while complementing its orthopedic trauma business.

- In July 2025, Arthrex Inc. introduced its BioComposite Interference Screw system for ACL reconstruction and soft tissue fixation procedures. The bioabsorbable screw technology eliminates the need for secondary removal surgeries while providing reliable fixation strength during the healing process.

- In May 2025, Globus Medical Inc. announced the launch of its ANTHEM cervical plate system featuring streamlined instrumentation and optimized plate profiles for anterior cervical discectomy and fusion procedures. The system incorporates enhanced visualization and simplified implantation techniques.

- In February 2025, B. Braun SE expanded its Aesculap orthopedic trauma portfolio with the introduction of anatomically precontoured clavicle plates designed for lateral, midshaft, and medial clavicle fractures. The plate system offers multiple length and thickness options to address diverse patient anatomies.

- In December 2024, NuVasive Inc. received U.S. FDA clearance for its Simplify Cervical Artificial Disc for two-level cervical disc replacement procedures, expanding treatment options for patients with degenerative disc disease at contiguous spinal levels.

- In October 2024, Orthofix Medical Inc. announced the launch of its FIREBIRD SI Screw Fixation System for sacroiliac joint fusion procedures. The system provides minimally invasive stabilization options for patients with sacroiliac joint dysfunction.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.