Global Otoplasty Market

Market Size in USD Billion

USD

1.22 Billion

USD

1.91 Billion

2025

2033

USD

1.22 Billion

USD

1.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.22 Billion | |

| USD 1.91 Billion | |

| % | |

|

Otoplasty Market Size

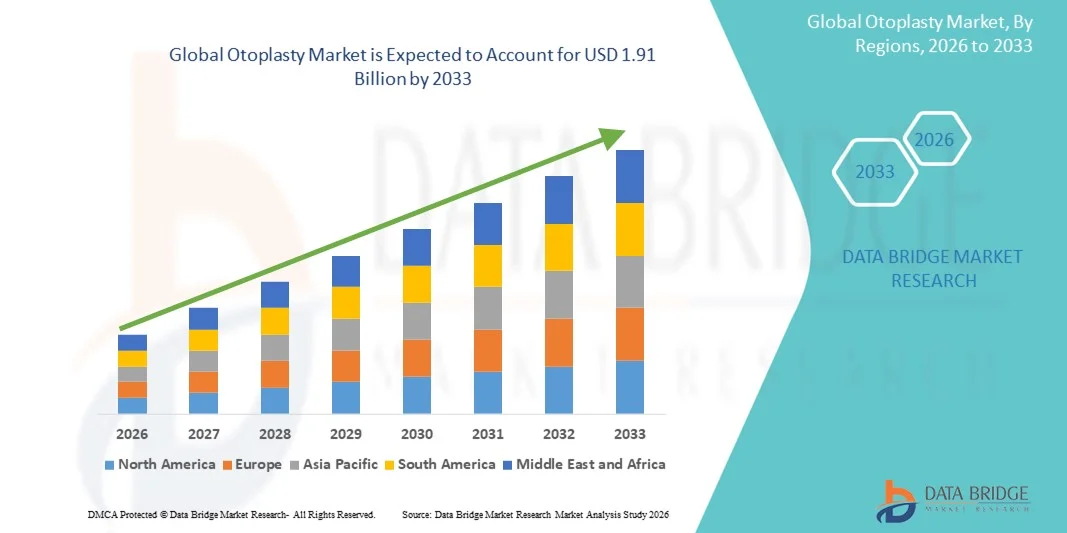

- As per Data Bridge Market Research Analysis the global otoplasty market size was valued at USD 1.22 billion in 2025 and is expected to reach USD 1.91 billion by 2033, at a CAGR of 5.83% during the forecast period

- The market growth is largely fueled by increasing aesthetic awareness among consumers, rising demand for cosmetic and reconstructive ear procedures, and technological progress in minimally invasive surgical techniques, which are improving safety, recovery outcomes, and overall patient acceptance worldwide

- Furthermore, growing incidence of congenital ear deformities, expanding healthcare expenditure, rising disposable income, and broader acceptance of cosmetic surgeries are driving otoplasty adoption across both residential and clinical settings. These converging factors are establishing otoplasty as a preferred solution for ear correction and aesthetic enhancement, thereby significantly boosting the industry’s growth

Market Size & Forecast

- Global Market Value (2025): USD 1.22 billion

- Expected Market Value (2033):USD 1.91 billion

- Forecast CAGR (2026–2033): 5.83%

Otoplasty Market Analysis

- Otoplasty market, including surgical and minimally invasive ear correction procedures, is increasingly recognized as an essential segment of cosmetic and reconstructive plastic surgery due to its ability to improve aesthetic appearance, restore symmetry, and boost patient confidence in both pediatric and adult populations

- The rising demand in the otoplasty market is primarily fueled by growing aesthetic consciousness among consumers, increasing prevalence of congenital ear deformities, and advancements in surgical techniques that reduce recovery time and enhance procedural safety

- North America dominated the otoplasty market with the largest revenue share of 41.3% in 2025, driven by high healthcare expenditure, strong awareness of cosmetic procedures, and the presence of leading plastic surgery centers, with the U.S. showing substantial adoption of minimally invasive and corrective ear procedures, supported by innovations from both established hospitals and specialized clinics

- Asia-Pacific is expected to be the fastest-growing region in the otoplasty market during the forecast period due to rising disposable incomes, increasing awareness of cosmetic surgery, and expanding access to modern healthcare facilities in urban centers

- Surgical segment dominated the market with a share of 60.4% in 2025, driven by their proven effectiveness, long-term results, and wide acceptance among patients seeking both aesthetic and reconstructive outcomes

Report Scope and Otoplasty Market Segmentation

|

Attributes |

Otoplasty Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Otoplasty Market Trends

Rising Preference for Minimally Invasive and Scarless Techniques

- A significant and accelerating trend in the global otoplasty market is the growing adoption of minimally invasive and scarless ear correction procedures, which reduce recovery time, minimize visible scarring, and enhance patient comfort

- For instance, endoscopic and laser-assisted otoplasty techniques are being increasingly implemented in clinics to achieve precise ear reshaping with minimal tissue trauma and faster healing

- Advancements in surgical instruments and imaging technologies allow surgeons to plan and execute procedures more accurately, improving patient outcomes and satisfaction

- Minimally invasive otoplasty is particularly appealing to younger patients and adults seeking aesthetic enhancements without extended downtime or conspicuous surgical marks

- This trend toward less invasive, highly precise procedures is reshaping patient expectations for cosmetic ear surgery, leading to increased demand in both pediatric and adult segment

- The adoption of these advanced otoplasty techniques is rapidly growing across both private clinics and hospital settings, as consumers increasingly prioritize quicker recovery, reduced scarring, and overall procedure safety

- Increasing social media influence and the rise of cosmetic procedure awareness campaigns are encouraging more patients to consider otoplasty at an earlier age

- Integration of 3D imaging and simulation technologies enables patients to visualize expected outcomes before surgery, further driving adoption and satisfaction

Otoplasty Market Dynamics

Driver

Growing Demand Due to Increasing Aesthetic Awareness and Ear Deformity Corrections

- The rising prevalence of congenital ear deformities and increasing aesthetic consciousness among consumers are significant drivers of heightened demand for otoplasty procedures

- For instance, clinics in North America and Europe are expanding services to include advanced corrective and cosmetic ear procedures, leveraging improved surgical techniques and patient education

- Patients are seeking procedures that improve facial symmetry and boost confidence, making otoplasty an attractive option for both children and adults

- Furthermore, increasing awareness of minimally invasive and outpatient procedures is enhancing accessibility and reducing perceived risks associated with otoplasty

- The availability of skilled plastic surgeons and growing investment in aesthetic clinics are further propelling the adoption of otoplasty across both urban and semi-urban regions

- The convenience of outpatient surgeries, shorter recovery periods, and improved cosmetic outcomes are key factors driving market growth in both elective cosmetic and reconstructive segments

- Expanding medical tourism for cosmetic surgeries, including otoplasty, is creating additional growth opportunities in regions offering cost-effective, high-quality surgical care

- Technological advancements such as laser-assisted and endoscopic techniques are improving precision and safety, attracting a broader patient base globally

Restraint/Challenge

High Costs and Limited Awareness in Emerging Markets

- Concerns surrounding the high cost of otoplasty procedures pose a significant challenge to broader market adoption, particularly in price-sensitive regions

- For instance, the expense of surgical and minimally invasive otoplasty in developed countries often deters middle-income patients from seeking treatment despite clinical need

- In addition, limited awareness of otoplasty options and potential benefits in emerging markets restricts patient adoption, slowing market penetration

- Insurance coverage for cosmetic ear correction is often limited or unavailable, further contributing to cost-related barriers for potential patients

- While procedure outcomes are improving and recovery times are decreasing, the perceived premium for advanced surgical techniques can still hinder adoption in regions with low healthcare expenditure

- Overcoming these challenges through patient education, awareness campaigns, and the introduction of cost-effective surgical solutions will be vital for sustained market growth

- Potential surgical complications, although rare, may discourage some patients, highlighting the need for skilled surgeons and advanced procedural techniques

- Limited availability of specialized otoplasty clinics in rural or underdeveloped regions continues to restrict market penetration and overall adoption

Otoplasty Market Scope

The market is segmented on the basis of type, technique, age distribution, gender, end user, and devices.

- By Type

On the basis of type, the otoplasty market is segmented into ear augmentation, ear reduction, and ear pin back. The ear pin back segment dominated the market with the largest revenue share in 2025, driven by its high demand among patients with prominent ears seeking both cosmetic and psychological benefits. Patients and parents often prioritize ear pin back procedures for their ability to improve facial symmetry and self-confidence, particularly in pediatric and adolescent populations. Clinics and hospitals prefer this type due to its relatively straightforward surgical process, shorter recovery times, and predictable outcomes. In addition, the procedure is widely recognized and commonly performed by plastic surgeons, which contributes to its dominance. The segment also benefits from growing awareness through social media, cosmetic campaigns, and patient education. Its established acceptance across both aesthetic and reconstructive applications continues to drive steady market revenue.

The ear augmentation segment is expected to witness the fastest growth during 2026–2033, fueled by rising demand for corrective procedures for underdeveloped or asymmetrical ears. Patients increasingly seek natural-looking augmentations using cartilage grafts or synthetic implants to improve ear shape and size. Technological advancements in surgical materials and techniques have enhanced safety, precision, and aesthetic outcomes, encouraging more patients to opt for augmentation procedures. Clinics and specialized centers are expanding their service offerings to meet this demand, especially in regions with growing disposable incomes. Increasing adult adoption of cosmetic ear augmentation for aesthetic enhancement is also contributing to market growth. Social media influence and cosmetic awareness campaigns are further boosting the popularity of this procedure.

- By Technique

On the basis of technique, the otoplasty market is segmented into surgical and non-surgical. The surgical segment dominated the market in 2025 with a market share of 60.4%, driven by its proven effectiveness and long-lasting results. Surgical otoplasty is preferred for complex cases of ear deformities, including congenital abnormalities and severe asymmetry. Hospitals and specialized clinics often recommend surgery due to its ability to deliver precise outcomes with minimal revisions. The dominance of this segment is supported by the availability of skilled plastic surgeons, advanced surgical instruments, and procedural safety improvements. Patients also perceive surgical techniques as more reliable and durable compared to non-surgical alternatives. The high patient satisfaction and repeat recommendation rates further contribute to its market share.

The non-surgical segment is expected to witness the fastest growth during 2026–2033, fueled by rising awareness and acceptance of minimally invasive procedures. Non-surgical techniques, including ear molding and splinting, are particularly popular among infants and young children with congenital deformities. These methods are less invasive, pain-free, and require minimal downtime, making them attractive to parents and caregivers. Clinics offering non-surgical solutions are expanding, especially in urban areas, to cater to growing patient preferences. Technological innovations in molding devices and materials further enhance procedure effectiveness. The convenience and aesthetic appeal of non-surgical options are driving adoption in emerging markets.

- By Age Distribution

On the basis of age, the otoplasty market is segmented into 13–19, 20–29, 30–39, 40–54, and 55 and above. The 13–19 age group dominated the market in 2025, driven by high demand among adolescents correcting prominent ears and other congenital deformities. Parents often prioritize procedures in this age group to prevent psychological distress and enhance social confidence. Pediatric and adolescent plastic surgery clinics are increasingly offering tailored services, making this segment a key revenue contributor. The relatively straightforward surgical procedures and faster healing in younger patients further support market dominance. Awareness campaigns, social media influence, and school-based information also encourage early intervention. Surgeons favor operating in this age group due to predictable outcomes and tissue pliability, strengthening its market share.

The 20–29 age group is expected to witness the fastest growth during 2026–2033, fueled by rising aesthetic consciousness among young adults. Patients increasingly seek cosmetic enhancements, including ear reshaping for improved facial symmetry. Social media influence, peer pressure, and the desire for self-improvement drive demand in this segment. Clinics are offering specialized adult-focused procedures, including minimally invasive options, to cater to this demographic. Technological advancements in surgical and non-surgical techniques enhance outcomes, boosting adoption. Growing disposable incomes and willingness to invest in elective cosmetic procedures further accelerate growth.

- By Gender

On the basis of gender, the otoplasty market is segmented into male and female. The female segment dominated the market in 2025, driven by higher cosmetic surgery adoption among women. Females are more likely to seek ear reshaping procedures to enhance facial aesthetics and self-confidence. Clinics often target female patients through awareness campaigns and marketing strategies, contributing to the segment’s dominance. Minimally invasive and scarless procedures are particularly appealing to female patients concerned with aesthetic outcomes. Social media and influencer impact further drive adoption in the female demographic. The higher disposable income and willingness to invest in elective cosmetic procedures among women also support revenue generation.

The male segment is expected to witness the fastest growth during 2026–2033, fueled by increasing acceptance of cosmetic procedures among men. Rising aesthetic awareness and reduced stigma around male cosmetic surgery are driving demand. Clinics are introducing male-focused promotions and procedures to attract this segment. Non-surgical and minimally invasive techniques are particularly appealing to male patients seeking discreet solutions. Social media influence and celebrity endorsements targeting male audiences further enhance adoption. Growing urbanization and disposable income among men support faster market growth.

- By End User

On the basis of end user, the otoplasty market is segmented into hospitals and clinics, ambulatory surgical centers, academic and research institutes, and others. The hospitals and clinics segment dominated the market in 2025, driven by the availability of advanced surgical facilities, skilled surgeons, and comprehensive patient care services. Hospitals often serve both pediatric and adult patients, making them a primary revenue contributor. Clinics specializing in cosmetic and reconstructive surgery further strengthen market dominance. Patients prefer hospitals and clinics for complex cases requiring precise surgical techniques and post-operative monitoring. The established reputation and trust associated with these facilities encourage patient adoption. Urban centers with concentrated healthcare infrastructure are key contributors to this segment’s dominance.

The ambulatory surgical centers segment is expected to witness the fastest growth during 2026–2033, fueled by the increasing demand for outpatient, minimally invasive procedures. These centers offer convenience, shorter recovery times, and cost-effective solutions, attracting patients seeking elective cosmetic surgery. The rise of same-day procedures and advanced surgical setups in ambulatory centers is encouraging adoption. Clinics and centers are expanding networks in urban and semi-urban regions to capture this growing segment. Patient preference for privacy, comfort, and reduced hospital stay further supports rapid growth. Technological advancements enabling safe outpatient otoplasty procedures also accelerate market expansion.

- By Devices

On the basis of devices, the otoplasty market is segmented into ear-splint, tubing, and others. The ear-splint segment dominated the market in 2025, driven by its wide use in both surgical recovery and non-surgical corrective procedures. Ear splints are particularly effective for infants and young children with congenital ear deformities, offering a non-invasive solution. Hospitals and clinics prefer ear splints due to ease of application and predictable outcomes. The device’s role in minimizing complications and supporting proper ear shaping post-surgery enhances its adoption. Availability in various sizes and materials for age-specific applications contributes to dominance. The high reliability and patient satisfaction further strengthen its market share.

The tubing segment is expected to witness the fastest growth during 2026–2033, fueled by innovations in non-surgical correction devices and customizable tubing solutions. These devices are increasingly used in outpatient settings for molding and shaping procedures. Technological improvements in tubing materials improve comfort, effectiveness, and durability, attracting both patients and clinicians. Growing awareness among parents and adult patients regarding non-surgical options boosts adoption. The convenience and minimally invasive nature of tubing devices further drive market growth. Expanding availability in emerging markets contributes to the segment’s faster CAGR.

Otoplasty Market Regional Analysis

- North America dominated the otoplasty market with the largest revenue share of 41.3% in 2025, driven by high healthcare expenditure, strong awareness of cosmetic procedures, and the presence of leading plastic surgery centers, with the U.S. showing substantial adoption of minimally invasive and corrective ear procedures, supported by innovations from both established hospitals and specialized clinics

- Patients in the region highly value the availability of advanced surgical techniques, minimally invasive procedures, and highly skilled plastic surgeons, which ensure effective outcomes and reduced recovery times

- This widespread adoption is further supported by high healthcare expenditure, strong aesthetic consciousness, and the presence of leading hospitals and specialized clinics, establishing otoplasty as a preferred solution for both pediatric and adult patients seeking ear correction or enhancement

U.S. Otoplasty Market Insight

The U.S. otoplasty market captured the largest revenue share of 38% in 2025 within North America, fueled by increasing awareness of cosmetic and corrective ear surgeries. Patients are increasingly prioritizing aesthetic enhancement and the correction of congenital ear deformities. The growing preference for minimally invasive procedures, combined with robust demand for outpatient and quick-recovery surgeries, further propels the otoplasty market. Moreover, the availability of highly skilled plastic surgeons, advanced surgical techniques, and specialized cosmetic clinics is significantly contributing to the market’s expansion.

Europe Otoplasty Market Insight

The Europe otoplasty market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing aesthetic consciousness and rising demand for reconstructive procedures. The increase in urban population, coupled with the prevalence of congenital ear deformities, is fostering the adoption of otoplasty. European patients are also drawn to minimally invasive and outpatient procedures that offer faster recovery and natural-looking results. The region is experiencing significant growth across hospitals, cosmetic clinics, and specialized centers, with otoplasty being incorporated into both elective and reconstructive surgeries.

U.K. Otoplasty Market Insight

The U.K. otoplasty market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising interest in cosmetic surgeries and the desire for enhanced facial aesthetics. In addition, concerns regarding congenital ear deformities and aesthetic appearance are encouraging patients to opt for corrective procedures. The U.K.’s well-established healthcare infrastructure and high awareness of minimally invasive techniques are expected to continue to stimulate market growth. Clinics and specialized centers increasingly offer patient-focused services, further expanding adoption.

Germany Otoplasty Market Insight

The Germany otoplasty market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of cosmetic and reconstructive ear procedures. Germany’s emphasis on advanced healthcare infrastructure, innovation in surgical techniques, and focus on patient safety promotes the adoption of otoplasty, particularly in hospitals and specialized clinics. Integration of minimally invasive procedures and modern surgical technologies is becoming increasingly prevalent, with patients showing strong preference for effective, safe, and aesthetically pleasing outcomes.

Asia-Pacific Otoplasty Market Insight

The Asia-Pacific otoplasty market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and growing awareness of cosmetic procedures in countries such as China, Japan, and India. The region’s growing inclination toward aesthetic enhancement, supported by social media influence and expanding cosmetic surgery awareness, is driving the adoption of otoplasty. Furthermore, the increasing number of specialized clinics and affordable procedure options are expanding access to a wider patient base.

Japan Otoplasty Market Insight

The Japan otoplasty market is gaining momentum due to the country’s advanced healthcare infrastructure, high aesthetic awareness, and demand for minimally invasive procedures. The Japanese market places a significant emphasis on natural-looking results, and the adoption of otoplasty is driven by an increasing number of clinics offering corrective and cosmetic ear surgeries. Integration of modern surgical techniques and patient-focused services is fueling growth. Moreover, Japan’s aging population is likely to spur demand for easier, safe, and aesthetically effective procedures in both cosmetic and reconstructive segments.

India Otoplasty Market Insight

The India otoplasty market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, growing awareness of cosmetic procedures, and increasing access to specialized clinics. India stands as one of the fastest-growing markets for aesthetic surgeries, and otoplasty is becoming increasingly popular among adolescents and adults. Government initiatives promoting healthcare infrastructure, coupled with the availability of affordable procedures and skilled surgeons, are key factors propelling the market in India.

Otoplasty Market Share

The Otoplasty industry is primarily led by well-established companies, including:

- AbbVie (U.S.)

- Sklar Surgical Instruments (U.S.)

- Invotec International, Inc. (U.S.)

- Phoenix Medical Systems (India)

- Earbuddies (U.K.)

- Stryker (U.S.)

- Zimmer Biomet (U.S.)

- Koken Co., Ltd. (Japan)

- HansBiomed Co., Ltd. (South Korea)

- Silimed (Brazil)

- Guangzhou Wanhe Plastic Materials (China)

- Sebbin (France)

- Polytech Health & Aesthetics (Germany)

- Surtex Instruments (U.S.)

- KLS Martin Group (Germany)

- B. Braun SE (Germany)

- GPC Medical Ltd. (China)

- Medtronic plc (Ireland)

- Integra LifeSciences Holdings Corporation (U.S.)

What are the Recent Developments in Global Otoplasty Market?

- In March 2025, a clinical study reported on the “inside‑out” otoplasty technique for children aged 7–17, showing high rates of aesthetic improvement and parental satisfaction and demonstrating evolving procedural approaches in pediatric ear correction

- In February 2025, the “inside‑out” otoplasty technique showed strong clinical and aesthetic results in school‑age children with prominent ears, demonstrating high parental satisfaction and improved ear symmetry in a retrospective study, highlighting evolving pediatric otoplasty practices

- In September 2024, the American Society of Plastic Surgeons highlighted growing attention to otoplasty as a distinct cosmetic and reconstructive procedure, noting that otoplasty has grown nearly 2 % since 2022, reflecting rising patient interest and awareness of ear‑reshaping surgery and its benefits for both congenital and aesthetic concerns

- In April 2024, EarBuddies early ear correction non‑surgical splinting saw notable patient adoption and success stories shared publicly, showing effective non‑surgical solutions being used to correct infant ear deformities and potentially reduce later otoplasty demand

- In March 2024, researchers published a Modified Fish‑tail Technique for protruding earlobe correction, representing a new otoplasty surgical approach focused on natural‑looking outcomes and tailored lobe reshaping for patients seeking refinement beyond traditional methods

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.