Global Overactive Bladder Treatment Market

Market Size in USD Billion

CAGR :

%

USD

3.93 Billion

USD

5.37 Billion

2025

2033

USD

3.93 Billion

USD

5.37 Billion

2025

2033

| 2026 –2033 | |

| USD 3.93 Billion | |

| USD 5.37 Billion | |

| % | |

|

Overactive Bladder Treatment Market Size

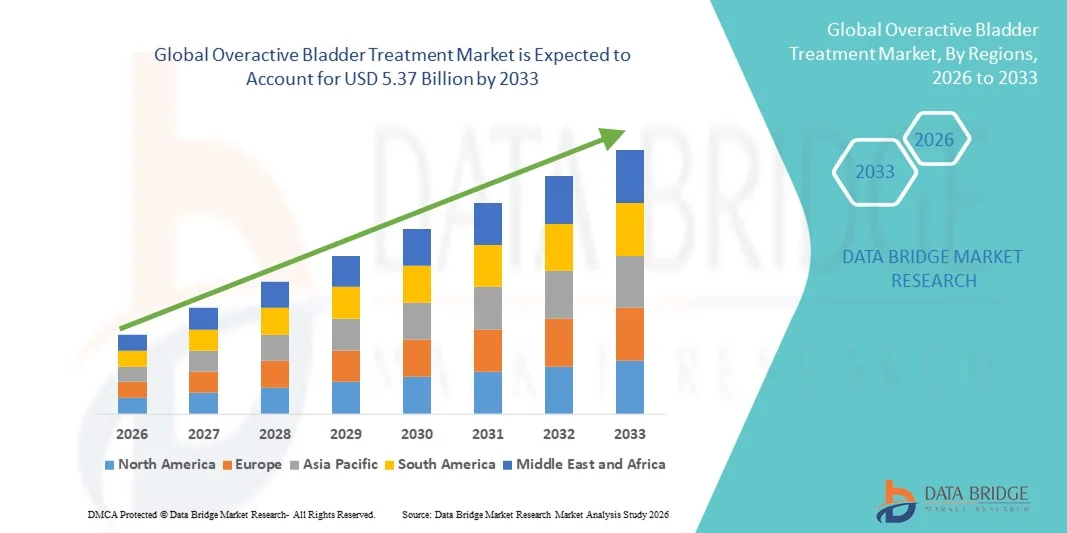

- The global overactive bladder treatment market size was valued at USD 3.93 billion in 2025 and is expected to reach USD 5.37 billion by 2033, at a CAGR of 4.00% during the forecast period

- The market growth is largely driven by the increasing prevalence of urinary disorders, rising geriatric population, and growing awareness about overactive bladder and its management options across both developed and emerging regions

- Furthermore, advancements in pharmacological therapies, minimally invasive procedures, and combination treatment approaches are expanding the range of effective solutions, while rising patient preference for convenient and targeted treatments is establishing overactive bladder therapies as the standard of care. These factors are collectively driving market adoption, thereby significantly propelling the industry’s growth

Overactive Bladder Treatment Market Analysis

- Overactive bladder treatments, including pharmacotherapy and disease-specific interventions, are increasingly essential for managing urinary urgency, frequency, and incontinence in both adult and geriatric populations due to their effectiveness, safety, and role in improving quality of life

- The rising demand for overactive bladder therapies is primarily driven by the growing prevalence of urinary disorders, increasing patient awareness, and preference for convenient and targeted treatment options

- North America dominated the overactive bladder treatment market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and strong adoption of pharmacological and minimally invasive therapies, with the U.S. witnessing significant uptake in prescription drugs and clinical management strategies

- Asia-Pacific is expected to be the fastest-growing region in the overactive bladder treatment market during the forecast period due to a growing geriatric population, rising healthcare awareness, and improving access to treatment options

- Anticholinergics segment dominated the pharmacotherapy category of the overactive bladder treatment market with a market share of 46.5% in 2025, driven by their effectiveness in symptom management and extensive clinical use across both idiopathic and neurogenic bladder overactivity

Report Scope and Overactive Bladder Treatment Market Segmentation

|

Attributes |

Overactive Bladder Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Overactive Bladder Treatment Market Trends

Rising Preference for Combination and Personalized Therapies

- A significant and accelerating trend in the global overactive bladder treatment market is the growing adoption of combination therapies and personalized treatment plans tailored to patient-specific symptoms and disease type, enhancing treatment efficacy and patient compliance

- For instance, clinicians are increasingly prescribing anticholinergic drugs in combination with β3-adrenergic agonists to optimize symptom control while minimizing side effects for patients with idiopathic bladder overactivity

- Digital health tools and wearable monitoring devices are being integrated into treatment regimens to track urinary patterns, provide feedback, and enable more precise therapy adjustments. For instance, mobile apps allow patients to log voiding episodes and medication adherence, supporting personalized care plans

- The trend toward patient-centric and adaptive therapies is reshaping expectations for overactive bladder management, emphasizing convenience, reduced side effects, and improved quality of life

- The demand for therapies that provide both effective symptom control and tailored treatment strategies is growing rapidly across developed and emerging markets as patients increasingly prioritize quality of life and convenience in chronic disease management

- Increasing integration of minimally invasive neuromodulation therapies with pharmacotherapy is emerging as a key trend, providing alternatives for patients unresponsive to conventional drugs. For instance, sacral neuromodulation devices are being combined with medication therapy to enhance treatment outcomes

- Growing adoption of telehealth and remote patient monitoring for overactive bladder management is also shaping the market, enabling continuous evaluation and timely intervention. For instance, platforms allow healthcare providers to monitor patient adherence and symptom progression virtually

Overactive Bladder Treatment Market Dynamics

Drive

Increasing Prevalence of Urinary Disorders and Awareness

- The rising prevalence of overactive bladder, particularly among the aging population, coupled with growing awareness of available treatment options, is a major driver for the heightened demand for effective therapies

- For instance, in March 2025, Pfizer announced initiatives to raise awareness about urinary disorders and promote early diagnosis and treatment, aimed at expanding patient access to therapies

- As patients and caregivers become more informed about the impact of overactive bladder on daily life, there is a stronger inclination to seek pharmacological and minimally invasive treatment solutions

- Furthermore, the increasing integration of healthcare technology and telemedicine is making it easier for patients to consult specialists and access treatments promptly, enhancing adoption rates

- For instance, online patient support programs and digital consultations by companies such as Allergan have facilitated timely initiation of therapy and improved adherence to treatment regimens

- The combination of rising disease prevalence, awareness campaigns, and improved access to treatment options is significantly propelling the growth of the overactive bladder treatment market globally

- Expansion of research and development into novel drug classes, such as selective β3-adrenergic agonists with improved safety profiles, is creating new growth avenues. For instance, ongoing clinical trials are exploring next-generation compounds to reduce side effects and improve patient outcomes

- Increasing collaborations between pharmaceutical companies and healthcare providers to offer patient education, adherence programs, and combination treatment strategies are also driving market growth. For instance, joint initiatives provide training and resources for proper medication use and lifestyle management

Restraint/Challenge

Side Effects, Safety Concerns, and Regulatory Barriers

- Concerns regarding adverse effects of pharmacological treatments, such as dry mouth, constipation, or cardiovascular risks, pose a significant challenge to broader market adoption, especially among elderly patients with comorbidities

- For instance, anticholinergic drugs have been associated with cognitive impairment in older adults, making some patients hesitant to initiate therapy without medical supervision

- Regulatory hurdles and stringent approval processes for new drugs and minimally invasive devices can delay market entry and limit treatment availability in certain regions

- For instance, delays in FDA or EMA approvals for novel β3-adrenergic agonists or neuromodulation devices have slowed their adoption in clinical practice

- High treatment costs and limited insurance coverage for advanced therapies can further restrict access for patients in developing regions or those with budget constraints

- Overcoming these challenges through improved safety profiles, patient education, regulatory compliance, and cost-effective treatment options will be crucial for sustained market growth

- Limited patient awareness and social stigma associated with urinary disorders can reduce treatment-seeking behavior, particularly in emerging markets. For instance, many patients avoid consultations due to embarrassment, delaying effective management

- Variability in healthcare infrastructure and access to specialists across regions poses a challenge for uniform market growth. For instance, rural areas may lack trained urologists or facilities for minimally invasive procedures, restricting treatment availability

Overactive Bladder Treatment Market Scope

The market is segmented on the basis of pharmacotherapy and disease type.

- By Pharmacotherapy

On the basis of pharmacotherapy, the overactive bladder treatment market is segmented into anticholinergics, solifenacin, oxybutynin, darifenacin, fesoterodine, tolterodine, trospium, and others. The anticholinergics segment dominated the market with the largest market revenue share of 46.5% in 2025, driven by its long-established clinical use and proven efficacy in controlling urinary urgency, frequency, and incontinence. Patients and healthcare providers often prefer anticholinergic drugs for their broad availability, well-documented safety profiles, and familiarity in treatment protocols. The segment’s dominance is further supported by ongoing research enhancing formulations to minimize side effects such as dry mouth and constipation. In addition, anticholinergics are used across both idiopathic and neurogenic bladder overactivity, making them versatile and widely prescribed. Strong marketing efforts and inclusion in treatment guidelines globally also reinforce their market leadership. Moreover, fixed-dose combinations and extended-release formulations are increasing patient adherence, further consolidating market dominance.

The solifenacin segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by its selective receptor targeting, reduced side effect profile, and superior patient tolerance compared to older anticholinergic drugs. Solifenacin’s efficacy in reducing urinary frequency and urgency has driven strong prescription demand, particularly in aging populations prone to overactive bladder. Healthcare providers are increasingly recommending solifenacin for patients who experience intolerance to traditional anticholinergics or have coexisting conditions that limit other drug options. Its once-daily dosing regimen improves patient compliance, making it attractive in chronic treatment scenarios. Solifenacin also benefits from expanding awareness programs and digital patient support tools that educate patients on adherence and symptom tracking. The growing availability of generic versions in emerging markets is further accelerating adoption. Overall, solifenacin’s combination of efficacy, safety, and convenience positions it as the fastest-growing pharmacotherapy segment.

- By Disease Type

On the basis of disease type, the overactive bladder treatment market is segmented into idiopathic bladder overactivity and neurogenic bladder overactivity. The idiopathic bladder overactivity segment dominated the market with the largest revenue share in 2025, driven by its higher prevalence in the general adult population and strong patient awareness. Idiopathic cases are commonly managed with pharmacotherapy, behavioral therapy, and combination approaches, contributing to consistent treatment demand. Physicians frequently initiate therapy with anticholinergics or β3-adrenergic agonists in idiopathic cases due to proven efficacy and established treatment guidelines. The segment also benefits from patient education programs, telemedicine support, and widespread healthcare access in developed regions. Ongoing clinical trials exploring safer and more effective drugs are further consolidating the market position. In addition, lifestyle management and monitoring apps tailored to idiopathic overactive bladder enhance patient adherence, supporting sustained market dominance.

The neurogenic bladder overactivity segment is expected to register the fastest growth rate during the forecast period, owing to rising awareness, increasing prevalence of neurological disorders such as multiple sclerosis and spinal cord injuries, and advances in treatment options. Neurogenic cases often require specialized pharmacotherapy combined with minimally invasive procedures or neuromodulation devices, creating strong growth opportunities. Healthcare providers are adopting personalized treatment strategies to manage symptom severity while minimizing side effects. Improved diagnostic tools and early intervention programs are driving timely treatment initiation. Digital monitoring and wearable devices are also supporting enhanced disease management in neurogenic patients. As a result, the neurogenic bladder overactivity segment is projected to grow rapidly due to increasing patient population, expanding treatment options, and technological innovations in therapy delivery.

Overactive Bladder Treatment Market Regional Analysis

- North America dominated the overactive bladder treatment market with the largest revenue share of 38.7% in 2025, supported by advanced healthcare infrastructure, high healthcare spending, and strong adoption of pharmacological and minimally invasive therapies

- Patients and healthcare providers in the region highly value effective pharmacotherapy, minimally invasive procedures, and combination therapies that improve symptom management and quality of life

- This widespread adoption is further supported by strong healthcare spending, availability of specialist care, and well-established distribution channels, establishing overactive bladder treatments as the preferred choice for managing both idiopathic and neurogenic bladder overactivity in adults and geriatric populations

U.S. Overactive Bladder Treatment Market Insight

The U.S. overactive bladder treatment market captured the largest revenue share of 82% in 2025 within North America, driven by the high prevalence of urinary disorders and advanced healthcare infrastructure. Patients increasingly prioritize effective pharmacotherapy and minimally invasive procedures that improve symptom management and quality of life. The growing awareness of treatment options, coupled with easy access to specialists and innovative therapies, further propels the market. Moreover, integration of digital health tools, telemedicine, and patient support programs is significantly contributing to treatment adherence and market expansion.

Europe Overactive Bladder Treatment Market Insight

The Europe overactive bladder treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing prevalence of urinary disorders and well-established healthcare systems. Rising awareness campaigns, coupled with aging populations in countries such as Germany, France, and Italy, are fostering the adoption of pharmacological and minimally invasive therapies. Patients and physicians are increasingly opting for combination treatment approaches, improving symptom management and patient quality of life. The market is experiencing strong growth across both idiopathic and neurogenic bladder overactivity management in residential and clinical settings.

U.K. Overactive Bladder Treatment Market Insight

The U.K. overactive bladder treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of bladder health and patient preference for effective therapies. In addition, the increasing prevalence of overactive bladder among older adults is encouraging both healthcare providers and patients to adopt pharmacological and neuromodulation solutions. The U.K.’s strong healthcare infrastructure, coupled with advanced prescription drug availability and telehealth services, is expected to continue stimulating market growth.

Germany Overactive Bladder Treatment Market Insight

The Germany overactive bladder treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by a growing geriatric population and the demand for effective, safe, and patient-friendly therapies. Germany’s well-developed healthcare system, emphasis on clinical research, and early adoption of novel pharmacological and minimally invasive treatments promote market growth. Integration of digital health tools for symptom monitoring and treatment adherence is also becoming increasingly prevalent, supporting broader adoption in both idiopathic and neurogenic cases.

Asia-Pacific Overactive Bladder Treatment Market Insight

The Asia-Pacific overactive bladder treatment market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by rising geriatric populations, increasing prevalence of urinary disorders, and improving healthcare accessibility in countries such as China, Japan, and India. Growing awareness of bladder health, coupled with government initiatives promoting healthcare infrastructure and digital health solutions, is driving the adoption of pharmacotherapy and minimally invasive therapies. In addition, expanding healthcare facilities and increasing affordability of treatment options are enhancing market penetration across both urban and semi-urban populations.

Japan Overactive Bladder Treatment Market Insight

The Japan overactive bladder treatment market is gaining momentum due to the country’s rapidly aging population, high healthcare standards, and strong awareness of bladder health. Patients increasingly demand effective, easy-to-administer therapies, including pharmacological and neuromodulation options. Integration of digital monitoring tools and telemedicine services is supporting treatment adherence and timely interventions. Moreover, the rise in smart healthcare solutions and patient education programs is further fueling market growth across residential and clinical settings.

India Overactive Bladder Treatment Market Insight

The India overactive bladder treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s growing geriatric population, rising awareness of urinary disorders, and improving healthcare infrastructure. India’s expanding healthcare access, combined with increasing availability of affordable pharmacotherapy and minimally invasive procedures, is driving adoption across urban and semi-urban regions. Government initiatives promoting healthcare digitalization, patient education programs, and early diagnosis campaigns are also key factors propelling the market in India.

Overactive Bladder Treatment Market Share

The Overactive Bladder Treatment industry is primarily led by well-established companies, including:

- Astellas Pharma Inc. (Japan)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- AbbVie Inc. (U.S.)

- Amneal Pharmaceuticals LLC (U.S.)

- Sumitomo Pharma Co., Ltd. (Japan)

- Novartis AG (Switzerland)

- Endo Inc. (U.S.)

- Hisamitsu Pharmaceutical Co., Inc. (Japan)

- Viatris Inc. (U.S.)

- Medtronic (Ireland)

- Axonics, Inc. (U.S.)

- Valencia Technologies (U.S.)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Zydus Group (India)

- DAIICHI SANKYO COMPANY, LIMITED (Japan)

- KYORIN Pharmaceutical Co., Ltd. (Japan)

- Neuspera Medical, Inc. (U.S.)

What are the Recent Developments in Global Overactive Bladder Treatment Market?

- In July 2025, Eisai Co., Ltd. and KYORIN Pharmaceutical launched Beova® Tablets (vibegron), a once‑daily β3‑adrenergic receptor agonist for overactive bladder treatment, in Thailand after receiving regional approvals, marking expanded access in Southeast Asia

- In June 2025, Neuspera Medical, Inc. received FDA approval for its integrated sacral neuromodulation (iSNM) system to treat urinary urge incontinence, a key symptom of overactive bladder, offering a less invasive neuromodulation therapy option

- In June 2025, Relonchem Ltd. (UK subsidiary of Marksans Pharma) obtained marketing authorization from the UK Medicines and Healthcare Products Regulatory Agency (MHRA) for its Oxybutynin hydrochloride oral solution, expanding treatment availability for OAB symptoms in the UK

- In April 2025, Amara Therapeutics launched a randomized controlled clinical trial (APPROVE Trial) to evaluate its prescription digital therapeutic (RiSolve App) for behavioral therapy in women with overactive bladder, advancing digital therapeutic approaches beyond drugs and devices

- In January 2025, the U.S. FDA expanded approval of Gemtesa (vibegron) for the treatment of overactive bladder symptoms in men with benign prostatic hyperplasia (BPH), enhancing the drug’s clinical indications and addressing an unmet need in this patient subgroup

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.