Global Paper Diagnostics Market

Market Size in USD Billion

USD

17.62 Billion

USD

31.42 Billion

2023

2031

USD

17.62 Billion

USD

31.42 Billion

2023

2031

| 2024 - 2031 | |

| USD 17.62 Billion | |

| USD 31.42 Billion | |

| % | |

|

Paper Diagnostics Market Size

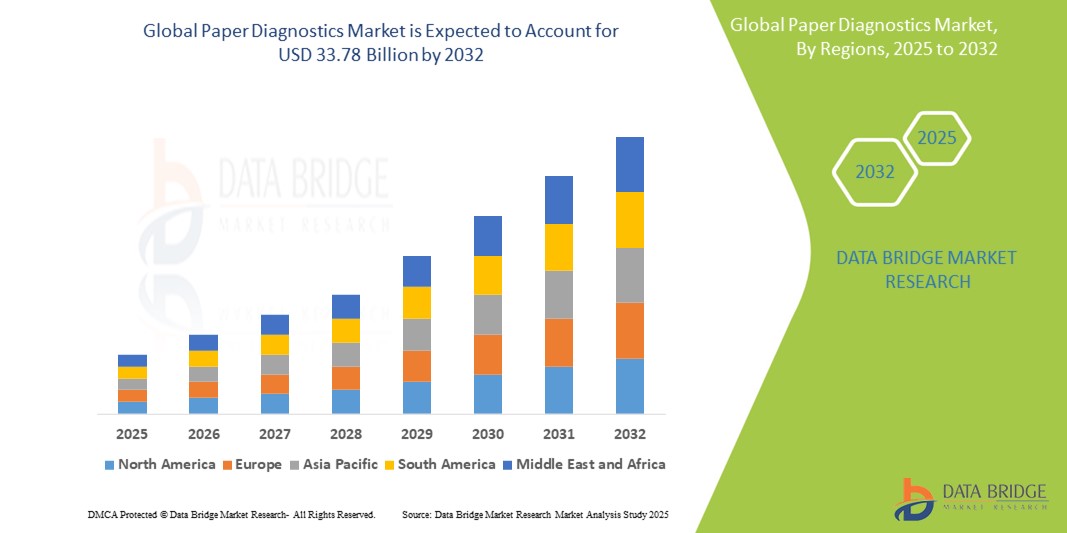

- The global paper diagnostics market size was valued at USD 18.94 billion in 2024 and is expected to reach USD 33.78 billion by 2032, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by the increasing demand for affordable, rapid, and user-friendly diagnostic tools, particularly in low-resource settings and remote areas, where traditional diagnostic infrastructure is lacking

- Furthermore, rising prevalence of infectious diseases, chronic conditions, and the growing focus on point-of-care testing are driving demand for innovative paper-based diagnostic solutions. These factors, along with advancements in microfluidics and bioassay integration, are positioning paper diagnostics as a scalable and efficient alternative for global health diagnostics

Paper Diagnostics Market Analysis

- Paper diagnostics, which utilize cellulose-based substrates to conduct biochemical tests, are becoming increasingly vital in modern healthcare diagnostics due to their low cost, portability, ease of use, and suitability for point-of-care applications, especially in resource-limited settings

- The accelerating demand for paper diagnostics is primarily driven by the rising prevalence of infectious diseases, increased global focus on early disease detection, and the growing need for decentralized diagnostic solutions that minimize dependency on complex lab infrastructure

- North America dominates the paper diagnostics market with the largest revenue share of 38.5% in 2024, characterized by strong healthcare infrastructure, early adoption of innovative diagnostic technologies, and significant investments in R&D from both public and private sectors

- Asia-Pacific is expected to be the fastest growing region in the paper diagnostics market during the forecast period due to the expanding healthcare access, rising government initiatives for affordable diagnostics, and increasing demand for low-cost solutions in densely populated countries such as India and China

- Lateral flow assays segment dominates the paper diagnostics market with a market share of 46.5% in 2024, driven by its wide usage in pregnancy tests, COVID-19 antigen tests, and other rapid diagnostic kits, supported by high scalability, minimal training requirements, and rapid result turnaround

Report Scope and Paper Diagnostics Market Segmentation

|

Attributes |

Paper Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Paper Diagnostics Market Trends

“Rapid Diagnostics and Decentralized Testing through Paper-Based Innovation”

- A significant and accelerating trend in the global paper diagnostics market is the rapid evolution of point-of-care (POC) testing technologies, with paper-based diagnostic tools emerging as key enablers of decentralized and accessible healthcare. This trend is driven by the need for low-cost, easy-to-use diagnostic solutions that can deliver reliable results without complex instrumentation

- For instance, 2D and 3D microfluidic paper-based analytical devices (μPADs) are being increasingly deployed in remote and low-resource environments for the detection of infectious diseases such as malaria, HIV, and COVID-19. These tests are valued for their portability, minimal reagent requirements, and ability to provide clear results within minutes

- The integration of paper diagnostics with smartphone-based readout systems is enabling real-time result capture and data sharing. Companies such as CellScope and Foldscope Instruments are at the forefront of developing paper-based test platforms compatible with mobile imaging, enhancing diagnostic reach in underserved areas

- Advances in biosensor technology are allowing paper diagnostics to detect not just infectious agents but also biomarkers for chronic conditions, environmental pollutants, and nutritional deficiencies. Researchers are now embedding nanoparticles and enzymes into paper substrates to improve test sensitivity and specificity, thereby expanding their application beyond traditional lateral flow tests

- This trend toward portable, scalable, and eco-friendly diagnostic systems is fundamentally transforming healthcare delivery, especially in public health surveillance and emergency outbreak responses. As a result, institutions and companies worldwide, including organizations such as PATH and academic labs at MIT and Stanford, are investing heavily in the development of next-generation paper-based diagnostic kits for rapid deployment in pandemic and endemic scenarios

- The demand for innovative, reliable, and low-cost diagnostic alternatives is rapidly increasing across global healthcare ecosystems, positioning paper diagnostics as a vital tool for expanding access to timely and accurate medical testing

Paper Diagnostics Market Dynamics

Driver

“Rising Demand for Affordable, Rapid, and Decentralized Diagnostic Solutions”

- The increasing need for accessible and cost-effective healthcare diagnostics, especially in underserved and remote regions, is a significant driver for the heightened demand for paper-based diagnostic solutions

- For instance, in February 2024, researchers at the University of Washington unveiled a paper-based test capable of detecting multiple respiratory viruses—including COVID-19 and influenza—in under 30 minutes. This innovation highlights how advancements in paper diagnostics are enabling fast, affordable, and scalable healthcare solutions across global markets

- As healthcare systems strive to enhance early disease detection, outbreak response, and community-based screening, paper diagnostics offer vital features such as portability, ease of use, and rapid result delivery, making them a compelling alternative to traditional lab testing

- Furthermore, the growing burden of infectious diseases and chronic health conditions is reinforcing the need for decentralized diagnostic options that can be deployed outside clinical settings—including in homes, mobile health units, and low-resource environments

- The simplicity of use, minimal training requirements, compatibility with smartphone-based readers, and the absence of cold chain logistics make paper diagnostics an increasingly attractive solution for large-scale testing initiatives and global health programs.

- The rising emphasis on equitable healthcare access and early intervention is expected to significantly propel the adoption and development of paper diagnostic technologies during the forecast period

Restraint/Challenge

“Limited Sensitivity and Commercialization Constraints in Complex Applications”

- The relatively lower sensitivity and limited quantitative capabilities of some paper-based diagnostic tests, especially in comparison to traditional laboratory methods, pose a challenge to their broader adoption in high-precision clinical applications

- For instance, lateral flow assays, one of the most commonly used formats in paper diagnostics, may struggle to detect low concentrations of biomarkers, raising concerns in use cases where early detection or quantitative accuracy is critical, such as cancer screening or monitoring chronic conditions

- Addressing these concerns requires innovation in materials, signal amplification methods, and integration with digital readers to improve performance and reliability. However, such improvements can introduce higher production costs and technical complexity, potentially impacting the affordability and scalability that make paper diagnostics attractive in the first place

- Furthermore, the path to large-scale commercialization of paper diagnostics is often hindered by regulatory challenges, variable shelf life, and the need for standardized manufacturing processes. These constraints are especially pronounced in low-resource settings, where infrastructure and distribution capabilities may be limited

- While the market is rapidly evolving and technological advancements are ongoing, overcoming these hurdles—particularly in achieving clinical-grade sensitivity and securing regulatory approvals—will be crucial to ensuring paper diagnostics can fulfill their potential as reliable, scalable tools in global healthcare

Paper Diagnostics Market Scope

The market is segmented on the basis of product, device type, application, and end-use.

- By Product

On the basis of product, the paper diagnostics market is segmented into lateral flow assays, dipsticks, and paper-based microfluidics. The lateral flow assays segment dominated the largest market revenue share of 46.5% in 2024, driven by its widespread use in point-of-care testing and rapid diagnostics. These tests are favored for their ease of use, low cost, and quick turnaround time, making them suitable for infectious disease detection, pregnancy testing, and various screening purposes in both clinical and home settings.

The paper-based microfluidics segment is anticipated to witness the fastest growth from 2025 to 2032, supported by advancements in miniaturization and multiplex testing capabilities. These devices enable more complex diagnostics, including quantitative results and multi-analyte detection, within a compact and affordable platform. Their expanding role in low-resource settings and integration with smartphone-based readers is expected to drive significant adoption across emerging markets.

- By Device Type

On the basis of device type, the market is segmented into diagnostic devices and monitoring devices. The diagnostic devices segment held the largest market share in 2024, fueled by rising demand for early disease detection tools in decentralized and home healthcare environments. Paper-based diagnostic devices are increasingly used for infectious disease testing, chronic disease management, and screening programs, particularly in areas lacking sophisticated laboratory infrastructure.

The monitoring devices segment is expected to grow steadily during the forecast period due to the growing emphasis on continuous and cost-effective monitoring of health conditions. Applications in glucose monitoring, urine analysis, and personalized medicine are contributing to the segment’s expansion, particularly as paper diagnostics evolve to support longitudinal data tracking.

- By Application

On the basis of application, the market is categorized into clinical diagnostics, food quality testing, and environmental monitoring. The clinical diagnostics segment accounted for the largest revenue share in 2024, driven by the high demand for affordable, accessible tests for infectious diseases, chronic conditions, and maternal health in both developed and developing regions.

The environmental monitoring segment is projected to witness the fastest CAGR from 2025 to 2032, due to increasing concerns over pollution, water quality, and chemical contamination. Paper-based sensors offer a portable and economical method for on-site testing of air and water contaminants, contributing to the market’s diversification into environmental safety applications.

- By End Use

On the basis of end-use, the paper diagnostics market is segmented into home healthcare, assisted living healthcare facilities, and hospitals and clinics. The home healthcare segment led the market in 2024, fueled by the rising trend toward self-diagnosis and the demand for easy-to-use, disposable diagnostic tools that do not require specialized training.

The hospitals and clinics segment is expected to grow at a substantial rate during the forecast period, driven by increasing institutional adoption of rapid, point-of-care testing solutions that streamline workflows and enable early detection without the need for centralized labs.

Paper Diagnostics Market Regional Analysis

- North America dominates the paper diagnostics market with the largest revenue share of 38.5% in 2024, driven by strong healthcare infrastructure, early adoption of innovative diagnostic technologies, and significant investments in R&D from both public and private sectors

- A health-conscious population, widespread access to medical infrastructure, and government initiatives focused on preventive care further support the region’s dominance

- Moreover, frequent innovations in paper-based microfluidics and home-based diagnostic kits are enhancing patient accessibility and convenience, reinforcing North America’s leadership in the market

U.S. Paper Diagnostics Market Insight

The U.S. paper diagnostics market captured the largest revenue share of 78% in 2024 within North America, driven by advanced healthcare infrastructure and a strong focus on preventive diagnostics. The growing demand for rapid, point-of-care testing, especially in home healthcare and clinical settings, is propelling market growth. Increased adoption of lateral flow assays and paper-based microfluidics for disease detection, coupled with government initiatives to expand access to affordable diagnostics, supports market expansion. The integration of paper diagnostics with mobile health applications further enhances user convenience and real-time health monitoring.

Europe Paper Diagnostics Market Insight

The Europe paper diagnostics market is projected to witness substantial growth over the forecast period, primarily due to stringent healthcare regulations and increasing emphasis on early disease detection. The rising prevalence of chronic and infectious diseases, along with growing consumer awareness, is driving demand for cost-effective and user-friendly diagnostic tools. The market is witnessing strong adoption in clinical diagnostics, food quality testing, and environmental monitoring sectors. Innovations in paper-based biosensors and increased funding for healthcare research further fuel growth in countries such as Germany, France, and the U.K.

U.K. Paper Diagnostics Market Insight

The U.K. paper diagnostics market is expected to grow significantly, supported by the country’s well-developed healthcare system and increasing interest in decentralized testing solutions. Rising awareness of infectious disease control and personalized medicine is encouraging adoption in both clinical and home healthcare applications. The robust digital health ecosystem and favorable government policies aimed at improving healthcare accessibility are additional growth drivers. The U.K.’s active research environment fosters continuous innovation in paper-based diagnostic devices, enhancing market competitiveness.

Germany Paper Diagnostics Market Insight

The Germany’s paper diagnostics market is anticipated to expand steadily, driven by the country’s strong healthcare infrastructure and high investments in research and development. The focus on sustainability and eco-friendly diagnostic solutions aligns with the growing demand for paper-based diagnostics that reduce waste compared to traditional methods. Germany’s aging population and increasing need for efficient disease monitoring systems in hospitals and assisted living facilities support market growth. Integration of paper diagnostics in food safety and environmental monitoring also contributes to the region’s steady demand.

Asia-Pacific Paper Diagnostics Market Insight

The Asia-Pacific paper diagnostics market is poised to register the fastest CAGR of 26% from 2025 to 2032, driven by expanding healthcare access, rising awareness of affordable diagnostic tools, and increasing prevalence of infectious diseases. Countries such as China, India, and Japan are witnessing growing adoption of paper diagnostics in home healthcare, rural clinics, and large-scale screening programs. Government initiatives promoting digital health and smart healthcare infrastructure further accelerate market growth. In addition, the presence of numerous local manufacturers and cost-effective production capabilities enhance the availability and affordability of paper diagnostic products in the region.

Japan Paper Diagnostics Market Insight

The Japan’s paper diagnostics market is gaining momentum due to the country’s technological advancement and aging population requiring efficient, easy-to-use diagnostic solutions. The integration of paper diagnostics with mobile health technologies and IoT devices facilitates real-time health monitoring. Japan’s focus on personalized healthcare and preventive medicine boosts demand for home-based and point-of-care testing kits. Furthermore, government support for innovative medical technologies encourages ongoing development and commercialization of advanced paper diagnostic products.

India Paper Diagnostics Market Insight

The India holds a significant market share in Asia-Pacific, driven by a large population base, increasing healthcare expenditure, and rising demand for rapid and affordable diagnostic solutions. The growing middle class and government programs targeting infectious disease control and rural healthcare expansion support paper diagnostics adoption. Domestic manufacturers are actively innovating low-cost lateral flow assays and dipsticks tailored to local healthcare needs. The push towards smart health infrastructure and increased public awareness of early disease detection are key factors driving market growth in India.

Paper Diagnostics Market Share

The paper diagnostics industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Siemens Healthineers AG (Germany)

- GE HealthCare (U.S.)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QIAGEN (Netherlands)

- Merck KGaA (Germany)

- Abcam Limited (U.K.)

- BD (U.S.)

- Agilent Technologies, Inc. (U.S.)

- BIOMÉRIEUX (France)

- OraSure Technologies, Inc. (U.S.)

- Chembio Diagnostic Systems, Inc. (U.S.)

- ARKRAY, Inc. (Japan)

- QuidelOrtho Corporation (U.S.)

- NG Biotech (France)

- Trividia Health, Inc. (U.S.)

- Access Bio, Inc. (U.S.)

Latest Developments in Global Paper Diagnostics Market

- In June 2025, A groundbreaking development from Massachusetts Institute of Technology (MIT) engineers has led to a novel nanoparticle-based sensor that enables early cancer detection through a simple urine test. This innovative system relies on engineered nanoparticles that respond to tumor-specific enzymes by releasing short DNA sequences ("barcodes") into the bloodstream, which are then excreted in urine. These DNA barcodes can be analyzed using a paper-based test strip, similar to at-home COVID-19 tests, utilizing CRISPR technology. The appearance of a dark line indicates the presence of cancer-related enzyme activity

- In June 2025, Scientists at NYU Abu Dhabi's Advanced Microfluidics and Microdevices Laboratory (AMMLab) have developed a novel Radially Compartmentalized Paper Chip (RCP-Chip) capable of detecting COVID-19 and other infectious diseases in under 10 minutes. This portable, cost-effective device requires no electricity or specialized lab equipment, functioning with only mild heat (around 65°C). Designed from a single sheet of paper, the RCP-Chip integrates sample ports, vents, fluidic resistors, and reaction chambers, pre-loaded with necessary reagents

- In March 2025, A comprehensive review published in EurekaSelect, "Advancements and Challenges in Paper-Based Diagnostic Devices for Low-Resource Settings," explores the development, applications, and future prospects of Paper-Based Diagnostic Devices (PBDDs). The review emphasizes that PBDDs are a breakthrough for affordable, rapid, and point-of-care diagnostics in low-resource settings, utilizing simple materials with microfluidics and various detection methods

- In September 2024, Scientists at the Institute of Nano Science and Technology (INST), Mohali, India, have developed a novel and cost-effective technique for fabricating paper-based devices using an Advanced PAP (A-PAP) pen. This method provides a practical alternative to conventional sensing techniques that require specialized equipment and expertise, making it ideal for resource-limited settings. The new technique allows for rapid fabrication (around 10 seconds) without heating/drying steps and has been successfully demonstrated for chemical detection of heavy metals and nitrites, as well as biological sensing for dopamine. The versatility extends to complex 3D paper-based devices using origami

- In February 2024, Researchers created a paper-based platform that aids in the rapid detection of bacteria causing antibiotic-resistant infections. This development addresses a critical global health challenge by providing a low-cost, point-of-care solution, particularly valuable in resource-limited settings where rapid identification of resistant strains is crucial for effective treatment and infection control

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.