Global Papillary Thyroid Cancer Market

Market Size in USD Billion

USD

3.70 Billion

USD

5.38 Billion

2025

2033

USD

3.70 Billion

USD

5.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.70 Billion | |

| USD 5.38 Billion | |

| % | |

|

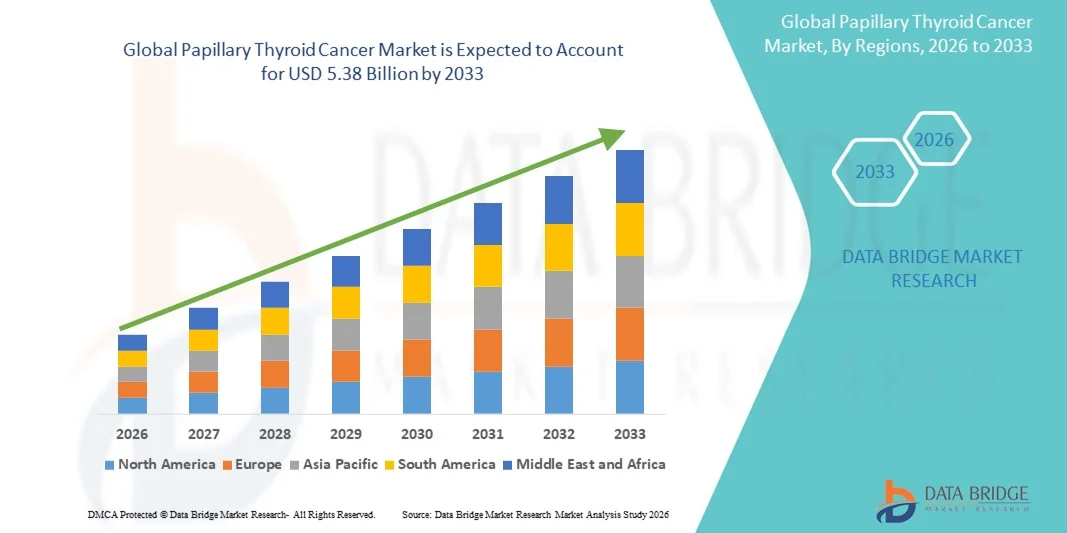

Papillary Thyroid Cancer Market Size

- The global papillary thyroid cancer market size was valued at USD 3.70 billion in 2025 and is expected to reach USD 5.38 billion by 2033, at a CAGR of 4.80% during the forecast period

- The market growth is largely fueled by the rising prevalence of thyroid disorders and continuous advancements in diagnostic imaging, molecular testing, and targeted therapies, leading to earlier detection and more effective disease management

- Furthermore, increasing patient demand for minimally invasive procedures, precision oncology solutions, and personalized treatment approaches is positioning papillary thyroid cancer therapies as a critical focus within the oncology landscape. These converging factors are accelerating clinical adoption and innovation, thereby significantly boosting the industry's growth

Papillary Thyroid Cancer Market Analysis

- Papillary thyroid cancer, the most common subtype of thyroid malignancy, is receiving increasing clinical focus due to its rising global incidence, advancements in diagnostic imaging, and broader adoption of precision-based treatment pathways that integrate surgery, radioactive iodine therapy, and hormone replacement

- The growing demand for effective treatment solutions is primarily driven by heightened awareness of thyroid health, expanding screening programs, and technological progress in imaging and molecular diagnostics that enable early identification and tailored therapy selection

- North America dominated the papillary thyroid cancer market with the largest revenue share of 39.9% in 2025, supported by strong access to advanced oncology services, high healthcare spending, and the presence of leading pharmaceutical innovators, with the U.S. experiencing significant uptake of improved diagnostic tools and optimized postoperative management protocols

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to expanding healthcare infrastructure, increasing incidence of thyroid disorders, and rising adoption of modern diagnostic techniques across emerging economies

- Surgery segment dominated the papillary thyroid cancer market with a market share of 46.8% in 2025, driven by its position as the gold-standard first-line treatment for localized disease, supported by advancements in minimally invasive approaches and superior long-term clinical outcomes that reinforce its widespread adoption

Report Scope and Papillary Thyroid Cancer Market Segmentation

|

Attributes |

Papillary Thyroid Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Papillary Thyroid Cancer Market Trends

Expansion of Precision Oncology and AI-Enhanced Diagnostic Support

- A significant and accelerating trend in the global papillary thyroid cancer market is the expanding integration of precision oncology with AI-assisted diagnostic tools, enabling more accurate tumor characterization, improved risk stratification, and optimized treatment planning for patients

- For instance, AI-enabled ultrasound systems are increasingly being used to differentiate benign from malignant thyroid nodules with higher accuracy, supporting clinicians in earlier and more confident decision-making

- AI-driven pathology platforms are being adopted to analyze biopsy samples, offering enhanced pattern recognition and reducing diagnostic variability, while molecular profiling tools are expanding access to mutation-specific insights

- The integration of diagnostic imaging with cloud-based AI platforms allows clinicians to monitor disease progression, identify recurrence risks, and create predictive models for long-term outcomes

- This fusion of AI with precision diagnostic solutions is reshaping expectations among oncologists for more efficient and data-driven management of papillary thyroid cancer, supporting a shift toward highly individualized care pathways

- The increasing demand for AI-powered diagnostic solutions and molecularly guided treatment selection is accelerating adoption across both developed and emerging healthcare systems, reinforcing the shift toward smarter and more accurate oncology workflows

- Growing investment from health-tech companies in thyroid cancer–focused AI systems is improving access to automated diagnostic support tools tailored to diverse clinical settings worldwide

- Increased integration of wearable monitoring devices with oncology management platforms is enabling continuous tracking of thyroid function and recurrence indicators, enhancing long-term patient monitoring

Papillary Thyroid Cancer Market Dynamics

Driver

Growth Fueled by Rising Disease Prevalence and Advancements in Diagnostic Imaging

- The global surge in thyroid disorder incidence, combined with continuous improvements in diagnostic imaging technologies, is a major driver strengthening the demand for early and effective papillary thyroid cancer management

- For instance, advancements in high-resolution ultrasound, CT, MRI, and molecular testing are enabling clinicians to detect papillary thyroid cancer at earlier stages, contributing to more proactive treatment strategies

- As awareness of thyroid health increases, more patients are undergoing routine screenings and nodule evaluations, expanding the pool of diagnosed cases and driving treatment uptake

- Furthermore, the growing shift toward minimally invasive surgical techniques and targeted therapies is positioning the disease as one of the more manageable cancers, encouraging greater adoption of advanced therapeutic approaches

- The availability of improved postoperative monitoring solutions and hormone-replacement therapies is further propelling market growth by supporting comprehensive, long-term disease management

- Rising adoption of genetic and biomarker testing is enabling clinicians to identify high-risk patients more efficiently, thus elevating the demand for personalized care plans

- Increasing government-led cancer screening initiatives across both developed and emerging nations is expanding early-diagnosis rates, directly boosting the treatment pipeline

Restraint/Challenge

High Treatment Costs and Challenges in Diagnostic Accuracy

- Financial burdens associated with advanced diagnostics, surgery, targeted therapies, and long-term hormone replacement present a significant challenge, particularly in low- and middle-income regions where affordability remains a barrier

- For instance, the rising cost of molecular profiling, radioactive iodine procedures, and precision oncology drugs can limit access for patients without strong insurance coverage or financial support programs

- Variability in diagnostic accuracy due to inconsistent availability of advanced imaging tools and trained specialists contributes to delayed or incorrect diagnosis, affecting timely treatment initiation

- While imaging technologies are improving, discrepancies in interpretation between medical centers can still impede consistent care quality, especially in developing healthcare systems

- Overcoming these challenges through cost-effective diagnostic innovations, expanded reimbursement policies, and improved clinical training will be critical for ensuring equitable access and sustaining market growth

- Limited access to well-equipped oncology centers in rural regions continues to restrict timely diagnosis and treatment, prolonging disease progression in underserved populations

- The shortage of skilled endocrinologists, oncology surgeons, and radiology specialists in many regions further complicates accurate diagnosis and optimal management of papillary thyroid cancer

Papillary Thyroid Cancer Market Scope

The market is segmented on the basis of treatment, diagnosis, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the papillary thyroid cancer market is segmented into iodine therapy, chemotherapy, external radiotherapy, thyroxin treatment, cisplatin, doxorubicin, radioiodine, levothyroxine, surgery, and others. The surgery segment dominated the market with the largest revenue share of 46.8% in 2025, driven by its position as the primary and most effective treatment for localized papillary thyroid cancer. Surgical removal of the thyroid continues to be the standard of care due to its high success rate and ability to eliminate most early-stage tumors. The expansion of minimally invasive and robotic-assisted techniques has further increased patient preference by reducing recovery time and complications. Hospitals across major regions consistently recommend thyroidectomy as the first-line treatment, reinforcing the reliability of this segment. The availability of trained surgical specialists and improved intraoperative imaging technologies strengthens its dominance. Growing patient awareness and early detection trends also contribute to increasing surgical volumes globally.

The radioiodine therapy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of post-surgical targeted ablation therapy. Radioiodine therapy effectively destroys residual thyroid tissue, making it essential for long-term disease control and recurrence prevention. The rising availability of molecular diagnostics allows clinicians to better identify patients who benefit from radioiodine, improving personalized treatment planning. Its non-invasive nature and favorable safety profile further support expanding clinical use. Advancements in dosimetry and personalized radioactive iodine dosing are enhancing treatment precision. Increasing access to nuclear medicine facilities in emerging markets is also accelerating segment growth.

- By Diagnosis

On the basis of diagnosis, the papillary thyroid cancer market is segmented into blood tests, biopsy, CT scan, MRI, ultrasound, and others. The ultrasound segment dominated the market with the largest share in 2025, driven by its status as the primary imaging method for detecting thyroid nodules. Ultrasound remains the preferred first-line diagnostic tool due to its high sensitivity, non-invasive nature, and widespread availability. Advancements in high-resolution and Doppler ultrasound technologies have significantly enhanced diagnostic accuracy. Its essential role in guiding fine-needle aspiration biopsies further reinforces dependence on this modality. Hospitals and clinics across developed and emerging regions integrate ultrasound routinely for both diagnosis and postoperative monitoring. Continuous improvements in portable ultrasound devices also support broader usage across outpatient settings.

The biopsy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing reliance on tissue sampling for definitive cancer confirmation. Fine-needle aspiration biopsy supported by ultrasound guidance enhances clinical accuracy and reduces unnecessary surgeries. The growing adoption of molecular marker analysis and genomic panels is improving risk stratification and treatment personalization. Biopsy-based diagnosis is gaining traction as clinicians seek greater precision beyond imaging alone. Advances in digital pathology and AI-driven cytology interpretation further accelerate adoption. The rise of early screening programs and specialist endocrine clinics is expanding the demand for biopsy procedures.

- By End-Users

On the basis of end-users, the market is segmented into clinics, hospitals, and others. The hospital segment dominated the market with the largest revenue share in 2025, driven by hospitals’ role as comprehensive centers for diagnosis, surgery, radioiodine therapy, and long-term monitoring. Hospitals house multidisciplinary teams including endocrinologists, oncologists, surgeons, and radiologists, enabling integrated cancer management. Access to advanced imaging and nuclear medicine infrastructure further strengthens their dominance. Patient preference for hospital-based treatment is high, especially for complex and advanced-stage cases. Strong reimbursement coverage for hospital-based procedures also supports this leadership. Hospitals In addition serve as major hubs for clinical trials, expanding access to innovative therapies.

The clinic segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for accessible and cost-effective outpatient thyroid evaluation. Clinics increasingly offer ultrasound services, blood tests, and routine follow-ups, making them essential for early diagnosis. The growth of private endocrine and oncology clinics is improving patient reach, especially in urban regions. Clinics also play a major role in postoperative hormone management and long-term monitoring of recurrence. Portable diagnostic devices are expanding their ability to deliver essential imaging services. Reduced waiting times and lower treatment costs compared to hospitals further encourage adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment held the largest market revenue share in 2025, driven by strong dependency on hospitals for initial treatment, radioactive iodine therapy, and hormone replacement initiation. Hospital pharmacies ensure safe handling and controlled dispensing of radioiodine materials, making them indispensable for oncology workflows. Patients undergoing surgery and postoperative care often continue procuring medications directly from hospital pharmacies for convenience and reliability. Strong coordination between clinicians and in-house pharmacies supports higher treatment adherence. Insurance coverage tends to favor hospital-based medication dispensing, further boosting utilization. Hospitals also maintain robust inventory and quality systems, ensuring availability of essential oncology drugs.

The online pharmacy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing digital adoption and demand for convenient access to chronic thyroid medications. Patients on lifelong levothyroxine therapy increasingly prefer subscription-based home delivery services. Online pharmacies offer competitive pricing and automated refill reminders, improving treatment adherence. The expansion of telemedicine platforms is enhancing prescription-to-delivery integration. Growing internet penetration in emerging markets is accelerating e-pharmacy growth. Enhanced logistics systems and regulatory improvements are making online medicine delivery more reliable and widely accepted.

Papillary Thyroid Cancer Market Regional Analysis

- North America dominated the papillary thyroid cancer market with the largest revenue share of 39.9% in 2025, supported by strong access to advanced oncology services, high healthcare spending, and the presence of leading pharmaceutical innovators, with the U.S. experiencing significant uptake of improved diagnostic tools and optimized postoperative management protocols

- The region benefits from widespread availability of cutting-edge molecular diagnostics, radioiodine therapy, targeted therapies, and high healthcare spending, which collectively enhance patient access to early detection and specialized cancer care

- In addition, the presence of leading cancer treatment centers, favorable reimbursement frameworks, and continuous clinical research focused on improved therapeutic outcomes strengthens North America’s leadership position, making it the most influential regional contributor to market growth

U.S. Papillary Thyroid Cancer Market Insight

The U.S. papillary thyroid cancer market captured the largest revenue share of 82% within North America in 2025, driven by widespread access to advanced diagnostic technologies, strong screening practices, and high awareness of thyroid disorders. The country benefits from robust adoption of molecular testing, targeted therapies, and radioiodine treatment, supported by leading cancer centers and extensive insurance coverage. Rising incidence of thyroid cancer, coupled with continuous clinical research and drug development, further accelerates market expansion. In addition, strong patient preference for minimally invasive surgery and improved treatment pathways reinforces the U.S. position as the most influential market in the region.

Europe Papillary Thyroid Cancer Market Insight

The Europe papillary thyroid cancer market is projected to grow at a substantial CAGR throughout the forecast period, driven by increasing diagnostic accuracy, early detection programs, and rising public awareness of thyroid-related conditions. European nations maintain well-established healthcare infrastructures and reimbursement systems, enhancing access to surgery, radioiodine therapy, and hormone replacement treatments. Growing investments in oncology research, adoption of precision medicine, and integration of advanced imaging modalities support wider treatment adoption. The market further benefits from strong clinical guidelines and multidisciplinary cancer care frameworks.

U.K. Papillary Thyroid Cancer Market Insight

The U.K. papillary thyroid cancer market is anticipated to grow at a noteworthy CAGR, supported by structured cancer screening pathways, rising thyroid disorder prevalence, and advancements in diagnostic imaging across NHS facilities. A heightened focus on early identification of nodules through ultrasound and biopsy contributes to improved treatment uptake. The country's emphasis on evidence-based oncology care, combined with growing access to minimally invasive thyroid surgeries and radioiodine treatment, strengthens market expansion. Increasing adoption of molecular testing for risk stratification also contributes to steady market growth.

Germany Papillary Thyroid Cancer Market Insight

The Germany papillary thyroid cancer market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high diagnostic capability, and increasing preference for advanced therapeutic options. Germany’s focus on precision oncology, along with widespread availability of CT, MRI, and ultrasound systems, supports early detection. A strong network of specialized endocrine cancer centers enhances access to surgery, radioiodine therapy, and long-term hormone replacement treatments. Rising investment in R&D and growing patient awareness around routine thyroid screening further stimulate regional market growth.

Asia-Pacific Papillary Thyroid Cancer Market Insight

The Asia-Pacific papillary thyroid cancer market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rising cancer incidence, expanding healthcare infrastructure, and increased adoption of modern diagnostic tools across China, Japan, South Korea, and India. Rapid urbanization and growing health awareness are leading to higher diagnostic rates and earlier detection of thyroid cancers. Government initiatives promoting cancer care accessibility, coupled with increasing uptake of radioiodine therapy and cost-effective treatment options, are boosting market penetration. APAC’s expanding medical tourism industry also supports treatment growth in key countries.

Japan Papillary Thyroid Cancer Market Insight

The Japan papillary thyroid cancer market is gaining significant traction due to the country’s advanced imaging capabilities and strong emphasis on early cancer detection. The high uptake of ultrasound screening, coupled with a rapidly aging population, contributes to rising diagnosis rates. Japan’s preference for minimally invasive and highly precise surgical approaches supports strong treatment adoption. Growing integration of molecular diagnostics, alongside widespread availability of radioiodine therapy and hormone replacement treatments, enhances patient outcomes and drives sustained market growth.

India Papillary Thyroid Cancer Market Insight

The India papillary thyroid cancer market accounted for the largest revenue share within Asia Pacific in 2025, supported by increased awareness of thyroid disorders and rising adoption of diagnostic imaging across urban and semi-urban regions. Growth is driven by expanding access to ultrasound, biopsy, and radiotherapy services across both public and private sectors. A growing middle-class population, combined with rising healthcare expenditure and government initiatives supporting cancer care access, strengthens market progression. In addition, the availability of cost-effective surgical and radioiodine treatment options significantly broadens patient reach.

Papillary Thyroid Cancer Market Share

The Papillary Thyroid Cancer industry is primarily led by well-established companies, including:

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Thermo Fisher Scientific Inc. (U.S.)

- Siemens Healthineers AG (Germany)

- Abbott (U.S.)

- BD (U.S.)

- GE HealthCare. (U.S.)

- Guardant Health, Inc. (U.S.)

- Natera, Inc. (U.S.)

- Exact Sciences Corporation (U.S.)

- Exelixis, Inc. (U.S.)

- Eisai Co., Ltd. (Japan)

What are the Recent Developments in Global Papillary Thyroid Cancer Market?

- In May 2025, researchers validated a new surgical method, the Burjeel Protocol, involving real-time indocyanine green (ICG) near-infrared fluorescence imaging to protect parathyroid glands during thyroid cancer surgery. This innovation significantly reduces complications such as postoperative hypocalcemia one of the most frequent issues after papillary thyroid cancer surgery

- In February 2025, NICE (U.K.) issued final guidance endorsing selpercatinib for the treatment of RET-altered thyroid cancers, including advanced papillary thyroid cancer. The recommendation covers both previously treated and untreated patients, enabling access through the NHS. This marks a major milestone as the U.K. historically had limited reimbursement for targeted thyroid cancer therapies

- In January 2025, the Society of Nuclear Medicine & Molecular Imaging (SNMMI) launched a dedicated Thyroid Cancer Registry under its RaPTR national registry initiative. This platform collects real-world patient data on radiopharmaceutical therapies used in thyroid cancer, including radioactive iodine therapy central to papillary thyroid cancer management

- In June 2024, the FDA granted traditional approval to selpercatinib (Retevmo) for adult and pediatric patients (≥2 years) with advanced or metastatic RET fusion-positive thyroid cancer that is refractory to radioactive iodine. The decision was based on strong clinical data from the LIBRETTO-001 trial demonstrating durable and meaningful responses in patients previously lacking targeted options

- In November 2023, results from the pivotal LIBRETTO-531 Phase III trial were highlighted in a Nature Reviews Clinical Oncology commentary, confirming the strong efficacy and safety of selpercatinib in RET-mutant thyroid cancers, including papillary thyroid cancer subtypes. The study showed superior outcomes compared with standard multikinase inhibitors, reinforcing selpercatinib’s emerging role as a preferred frontline therapy in RET-driven disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.