Global Paraneoplastic Cerebellar Degeneration Pcd Market

Market Size in USD Million

USD

243.10 Million

USD

332.69 Million

2024

2032

USD

243.10 Million

USD

332.69 Million

2024

2032

| 2025 - 2032 | |

| USD 243.10 Million | |

| USD 332.69 Million | |

| % | |

|

Paraneoplastic Cerebellar Degeneration (PCD) Market Size

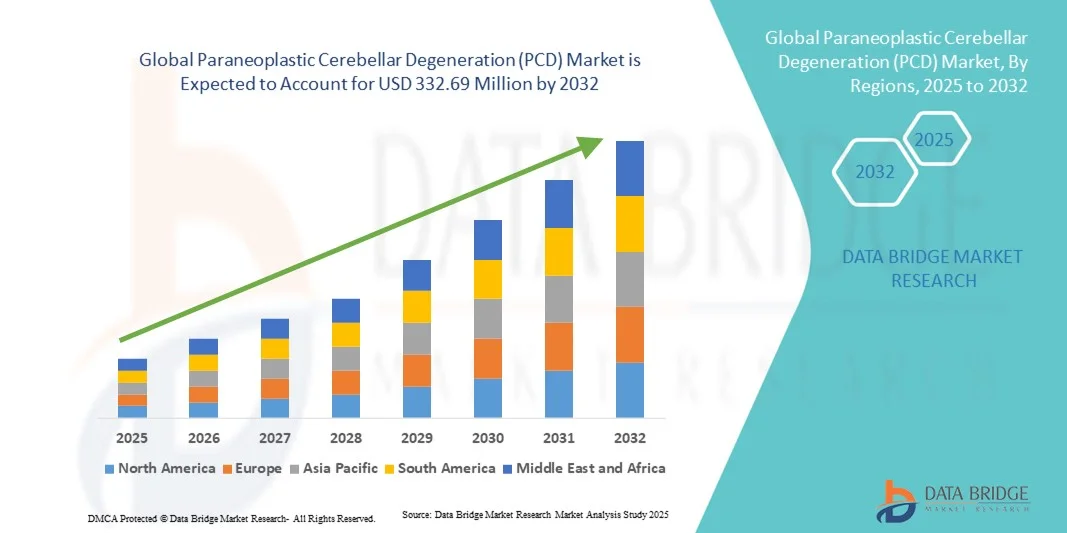

- The global paraneoplastic cerebellar degeneration (PCD) market size was valued at USD 243.10 Million in 2024 and is expected to reach USD 332.69 Million by 2032, at a CAGR of 4.00% during the forecast period

- The market growth is largely fueled by increasing awareness, early diagnosis, and technological advancements in the treatment of paraneoplastic cerebellar degeneration (PCD), leading to improved patient outcomes and wider adoption of innovative therapies

- Furthermore, rising investments in research, personalized medicine approaches, and the development of targeted therapies are accelerating the uptake of paraneoplastic cerebellar degeneration (PCD) solutions, thereby significantly boosting the industry's growth

Paraneoplastic Cerebellar Degeneration (PCD) Market Analysis

- The Paraneoplastic Cerebellar Degeneration (PCD) market refers to the global industry focused on the diagnosis, treatment, and management of PCD, a rare autoimmune neurological disorder affecting the cerebellum, with solutions including medications, therapies, and supportive care

- Furthermore, rising demand for early diagnosis, effective treatment protocols, and patient-centric care solutions is driving the adoption of Paraneoplastic Cerebellar Degeneration (PCD) therapies, significantly boosting the industry’s growth

- North America dominated the paraneoplastic cerebellar degeneration (PCD) market with the largest revenue share of 42.55% in 2024, characterized by well-established healthcare infrastructure, high healthcare spending, and a strong presence of key industry players. The U.S. remains the primary contributor, with increasing research initiatives and clinical trials enhancing the development and deployment of novel PCD therapies

- Asia-Pacific is expected to be the fastest-growing region in the paraneoplastic cerebellar degeneration (PCD) market during the forecast period due to rising healthcare awareness, improving access to advanced healthcare services, and growing investments in neurological research in countries such as China, Japan, and India

- Parenteral dominated with 96% revenue share in 2024, as most immunotherapies, immunoglobulins, and plasma exchange treatments require intravenous delivery

Report Scope and Paraneoplastic Cerebellar Degeneration (PCD) Market Segmentation

|

Attributes |

Paraneoplastic Cerebellar Degeneration (PCD) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Paraneoplastic Cerebellar Degeneration (PCD) Market Trends

Increasing Focus on Personalized Medicine and Targeted Immunotherapies

- A prominent trend in the global paraneoplastic cerebellar degeneration (PCD) market is the growing emphasis on personalized medicine, where therapies are tailored to the individual characteristics of patients, including their genetic profile, tumor type, and immune system status. This approach is transforming how PCD is managed, shifting from a one-size-fits-all strategy to highly targeted interventions that aim to maximize efficacy and minimize side effects

- For instance, in November 2023, Roche initiated a clinical study exploring patient-specific immunotherapy approaches for PCD, underscoring the move towards precision treatment based on biomarker identification and individualized therapy planning

- The adoption of advanced diagnostic tools, such as next-generation sequencing, antibody panels, and refined neuroimaging techniques, is allowing clinicians to better characterize each patient’s disease profile. This, in turn, informs the selection of the most effective therapy, whether it involves immunomodulators, biologics, or combination regimens, improving overall clinical outcomes

- Healthcare providers are increasingly integrating longitudinal patient monitoring into treatment plans, enabling real-time assessment of therapeutic response and adjustments in therapy as needed. Such proactive management enhances the safety and effectiveness of treatment while addressing disease progression more efficiently

- Furthermore, ongoing research into tumor-immune system interactions is enabling the development of innovative targeted immunotherapies that can selectively modulate immune responses, reducing neurological damage while controlling the underlying malignancy

- This trend is driving pharmaceutical companies to invest heavily in R&D for PCD-specific therapies, as the combination of personalized medicine and immunotherapy represents a long-term growth opportunity. It also highlights the market’s shift toward evidence-based, patient-centric approaches that prioritize improved quality of life and clinical outcomes for individuals affected by PCD

Paraneoplastic Cerebellar Degeneration (PCD) Market Dynamics

Driver

Growing Need Due to Increasing Awareness and Advancements in Oncology Care

- The rising prevalence of cancer and the associated risk of neurological complications, including paraneoplastic cerebellar degeneration (PCD), is a major driver for the market, as healthcare providers and researchers seek targeted therapies to improve patient outcomes

- For instance, in March 2023, Novartis announced the expansion of its oncology research program to focus on immune-mediated neurological disorders, including PCD, aiming to accelerate the development of novel treatment options. Such initiatives by leading pharmaceutical companies are expected to propel market growth during the forecast period

- Advances in diagnostic technologies, including enhanced antibody testing and neuroimaging, are enabling earlier detection of PCD, allowing for timely intervention and management, which is boosting demand for specialized therapies

- Furthermore, the growing awareness among oncologists, neurologists, and patients regarding the debilitating effects of PCD is driving increased investment in therapeutic development and patient care programs

- The development of biologics, immunomodulatory therapies, and targeted treatment regimens is expanding treatment options, providing clinicians with more effective tools to manage PCD symptoms and improve quality of life

- Increased collaboration between academic institutions, research hospitals, and pharmaceutical companies is also facilitating clinical trials and real-world studies, further contributing to market growth

Restraint/Challenge

Limited Awareness, Complex Diagnosis, and High Treatment Costs

- The complexity of diagnosing paraneoplastic cerebellar degeneration (PCD), coupled with its rare occurrence, poses significant challenges to timely treatment and broader market adoption. Many patients remain undiagnosed or are misdiagnosed due to overlapping symptoms with other neurological disorders

- For instance, several studies reported in 2022 indicated that delayed diagnosis leads to irreversible neuronal damage, making early detection critical yet challenging for healthcare providers

- High costs associated with immunotherapy, biologics, and long-term patient management can restrict access, particularly in emerging economies with limited healthcare resources. Pharmaceutical pricing and insurance reimbursement challenges further exacerbate this issue, limiting market penetration

- The lack of standardized treatment guidelines and limited availability of specialized care centers for PCD treatment can hinder widespread adoption of novel therapies

- Overcoming these barriers through improved physician education, patient awareness programs, expanded access to diagnostic tools, and the development of cost-effective treatment strategies will be vital for sustained growth in the Paraneoplastic Cerebellar Degeneration (PCD) market

- Continuous research into the underlying mechanisms of PCD and the development of novel immunotherapeutic agents remain critical for enhancing treatment efficacy and expanding the patient base globally

Paraneoplastic Cerebellar Degeneration (PCD) Market Scope

The market is segmented on the basis of diagnosis, treatment, route of administration, end-user, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the PCD market is segmented into Imaging Test, CSF Analysis, and Paraneoplastic Antibody Assay. The Imaging Test segment dominated the market with a revenue share of 47.5% in 2024, driven by its high precision in detecting cerebellar degeneration associated with paraneoplastic syndromes. Advanced MRI and PET scans are widely used in hospitals and cancer research institutes for early detection and monitoring. The segment benefits from integration with AI-assisted image processing, improving diagnostic accuracy. Imaging tests are non-invasive, highly sensitive, and can track disease progression over time. Growing awareness among clinicians, standardization of imaging protocols, and the presence of skilled radiologists support adoption. Continuous technological innovations enhance imaging resolution and diagnostic capabilities. High adoption in North America and Europe is supported by reimbursement policies. Research collaborations between hospitals and imaging device manufacturers accelerate implementation. Increasing prevalence of cancer-related neurological complications further drives revenue. Government initiatives and healthcare funding improve accessibility. The demand for routine neurological assessments in high-risk cancer patients also contributes to market dominance.

The Paraneoplastic Antibody Assay segment is expected to witness the fastest CAGR of 19.2% from 2025 to 2032, fueled by the rising adoption of molecular diagnostics and immunoassays. These assays enable precise detection of autoantibodies linked to PCD, facilitating early intervention. Technological advancements are improving assay sensitivity and reducing turnaround time. Increasing awareness among clinicians about biomarker-driven therapies boosts demand. Specialized laboratories and biotech firms are expanding assay availability. Integration with personalized medicine strategies enhances treatment outcomes. Government grants and private investments in rare neurological disorder research accelerate deployment. Training programs for lab personnel increase assay utilization. Collaborative research between hospitals and diagnostic companies further expands market reach. High demand in emerging economies is supported by expanding diagnostic infrastructure. Rising patient awareness and advocacy for early testing drive growth. Growing interest in combination diagnostic approaches with imaging tests strengthens the segment’s adoption.

- By Treatment

On the basis of treatment, the PCD market is segmented into Immunotherapy, Corticosteroids, Immunoglobulins, Plasma Exchange, Cyclophosphamide, Tacrolimus, and Rituximab. The Immunotherapy segment dominated the market with 44% revenue share in 2024, due to its proven efficacy in modulating immune responses and controlling paraneoplastic neuronal damage. Hospitals and cancer research centers widely adopt immunotherapy protocols including checkpoint inhibitors, monoclonal antibodies, and adoptive cell therapy. Early intervention with immunotherapy improves patient outcomes and survival rates. The segment benefits from ongoing R&D, regulatory approvals, and increasing clinical evidence of success. Biologic therapies are supported by specialized hospital infrastructure. Adoption is high in developed regions due to healthcare funding and advanced oncology services. Collaborations between pharma companies and hospitals accelerate deployment. Patient awareness and advocacy for rare neurological disorders further support uptake. Integration with personalized medicine improves therapeutic precision. Insurance coverage and reimbursement policies encourage broader adoption. Rising prevalence of paraneoplastic syndromes drives revenue. Continuous innovation in immunotherapy formulations strengthens the segment’s dominance.

The Rituximab segment is expected to witness the fastest CAGR of 18.5% from 2025 to 2032, driven by its targeted B-cell mechanism, improving outcomes in autoimmune PCD cases. Expansion of clinical trials and off-label applications enhances adoption. Favorable reimbursement and insurance coverage facilitate access. Growing research collaborations and biotech innovations support segment growth. Adoption in specialized treatment centers ensures rapid availability. Integration with combination therapies improves effectiveness. Technological improvements reduce adverse effects and increase patient compliance. Hospital protocols increasingly include Rituximab for PCD management. Awareness campaigns highlight benefits in rare neurological conditions. Emerging markets are adopting Rituximab due to improved affordability. Patient advocacy groups promote early therapy initiation. Global pharma launches of new Rituximab formulations boost demand. Rising incidence of autoimmune paraneoplastic syndromes further propels growth.

- By Route of Administration

On the basis of route of administration, the market is primarily Parenteral, which dominated with 96% revenue share in 2024, as most immunotherapies, immunoglobulins, and plasma exchange treatments require intravenous delivery. Hospitals and specialized clinics provide controlled administration, ensuring safety and efficacy. Parenteral delivery allows precise dosing and rapid therapeutic effect. Adoption is supported by clinical guidelines recommending IV delivery for immunomodulatory therapies. Advanced hospital infrastructure facilitates administration. Trained medical staff ensures compliance with treatment protocols. Availability of infusion centers supports increased patient throughput. High adoption in developed countries is backed by reimbursement and healthcare funding. Emerging markets are gradually expanding infusion services. Government healthcare initiatives improve access to parenteral treatments. Integration with hospital information systems enhances monitoring. Research institutes focus on optimizing administration protocols for efficacy. Continuous innovation in IV delivery systems supports segment growth.

- By End-User

On the basis of end-user, the PCD market is segmented into Cancer Research Institutes, Hospitals, and Others. The Hospitals segment dominated with 52% revenue share in 2024, due to centralized treatment facilities, advanced diagnostics, and the capability to deliver complex immunotherapies. Hospitals handle high patient volumes and integrate multi-disciplinary care teams. Adoption is supported by clinical protocols for rare neurological conditions. Infrastructure for immunotherapy and parenteral treatment is widely available. Availability of trained staff and specialized equipment ensures safety. High adoption in North America and Europe drives revenue. Integration with research and clinical trials enhances hospital capabilities. Funding from government and private sources supports treatment expansion. Hospitals act as hubs for disease monitoring and therapy follow-up. Collaboration with biotech and pharma companies facilitates rapid therapy adoption. Hospitals also provide patient education and monitoring services. Technological integration, such as EMR systems, improves treatment outcomes.

The Cancer Research Institutes segment is expected to witness the fastest CAGR of 17.9% from 2025 to 2032, fueled by rising clinical research activities, early-stage trials, and development of novel therapies for rare neurological disorders. Expansion of research centers and partnerships with biotech companies enhance capabilities. Focus on translational research accelerates therapy development. Funding from grants and private investors supports growth. Access to patient populations for trials improves data collection. Integration of diagnostics and treatment research enables innovation. Research institutes also develop personalized therapeutic strategies. Collaboration with hospitals facilitates clinical implementation. Government policies promoting rare disease research further drive growth. Adoption of advanced laboratory technologies improves throughput. Training programs for researchers ensure effective utilization. Increasing publication of PCD studies raises awareness and fosters adoption. Expansion into emerging markets enhances research coverage.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated with 63% revenue share in 2024, owing to direct availability of immunotherapies, parenteral treatments, and associated medications to patients. Hospitals streamline supply chains for timely access to critical therapies. Adoption is supported by procurement policies and integration with patient care services. High adoption in North America and Europe ensures consistent demand. Hospital pharmacies maintain cold-chain requirements for biologics. Access to trained pharmacists ensures correct handling and administration. Partnership with biotech and pharma manufacturers facilitates rapid distribution. Integration with hospital EMR systems enhances inventory management. Regulatory approvals and quality control ensure safe supply. Availability of hospital pharmacies supports clinical trials and therapy monitoring. Multi-disciplinary coordination improves patient adherence. Hospitals’ focus on rare diseases drives volume demand.

The Others segment is expected to witness the fastest CAGR of 16.8% from 2025 to 2032, driven by emerging biotech suppliers, specialized diagnostic centers, and home-care service integration. Expansion in telemedicine, mobile infusion services, and private clinics supports rapid adoption. Rising investments in rare neurological disorder solutions accelerate market growth. Technological advancements in supply chain tracking improve delivery efficiency. Collaborations with hospitals and research centers enhance market reach. Increased awareness among patients and caregivers boosts adoption. Expansion in underserved regions enables better accessibility. Integration with clinical trials and research programs accelerates uptake. Rising focus on personalized medicine enhances the segment’s relevance. Partnerships with insurance providers improve affordability. Adoption of mobile pharmacy solutions in remote areas supports growth. Regulatory facilitation for innovative delivery models further propels expansion. Increased public-private initiatives for rare disease care strengthen the segment’s presence.

Paraneoplastic Cerebellar Degeneration (PCD) Market Regional Analysis

- North America dominated the paraneoplastic cerebellar degeneration (PCD) market with the largest revenue share of 42.55% in 2024

- Characterized by well-established healthcare infrastructure, high healthcare spending, and a strong presence of key industry players

- The market remains the primary contributor, with increasing research initiatives and clinical trials enhancing the development and deployment of novel PCD therapies

U.S. Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The U.S. paraneoplastic cerebellar degeneration (PCD) market captured the largest revenue share in 2024 within North America, fueled by advanced healthcare capabilities, extensive clinical research, and early adoption of innovative treatment protocols. Ongoing clinical trials and R&D efforts by biotechnology and pharmaceutical companies are accelerating the availability of targeted therapies, while increasing awareness among clinicians and patients is driving higher diagnosis and treatment rates, significantly contributing to market expansion.

Europe Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The Europe paraneoplastic cerebellar degeneration (PCD) market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing awareness of rare neurological disorders, stringent healthcare regulations, and increased funding for research programs. Rising prevalence of paraneoplastic neurological syndromes and improved diagnostic infrastructure are encouraging adoption of novel therapies across clinical settings. The region is witnessing steady growth across hospitals, specialty clinics, and research institutes, reflecting a robust market expansion across multiple healthcare segments.

U.K. Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The U.K. paraneoplastic cerebellar degeneration (PCD) market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increased investments in neurological research and rising prevalence of paraneoplastic syndromes. Enhanced awareness among clinicians, availability of advanced diagnostic tools, and supportive healthcare policies are driving adoption of innovative treatment approaches. Growing emphasis on early diagnosis and patient-centric care is expected to further stimulate market growth.

Germany Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The Germany paraneoplastic cerebellar degeneration (PCD) market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong focus on rare disease research, and high healthcare expenditure. Germany’s emphasis on innovation, clinical trials, and evidence-based treatment protocols promotes the adoption of novel PCD therapies across hospitals, research centers, and specialty clinics. The market is benefiting from continuous government support and investment in neurological research programs, aligning with growing clinical demand.

Asia-Pacific Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The Asia-Pacific paraneoplastic cerebellar degeneration (PCD) market is poised to grow at the fastest CAGR of 23–24% during the forecast period, driven by rising healthcare awareness, improving access to advanced healthcare services, and growing investments in neurological research across countries such as China, Japan, and India. Expanding hospital infrastructure, increasing clinical trials, and government-led initiatives targeting rare neurological disorders are key factors propelling market growth.

Japan Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The Japan paraneoplastic cerebellar degeneration (PCD) market is gaining momentum due to increasing research on rare neurological diseases, advanced healthcare infrastructure, and a focus on patient-centered care. The country’s robust clinical research environment and high adoption of novel therapies are supporting growth, while aging demographics and rising incidence of paraneoplastic syndromes are further driving demand for innovative treatments across hospitals and specialty clinics.

China Paraneoplastic Cerebellar Degeneration (PCD) Market Insight

The China paraneoplastic cerebellar degeneration (PCD) market accounted for the largest revenue share in Asia-Pacific in 2024, driven by rapid healthcare modernization, increasing government initiatives for rare neurological disorders, and substantial investments in hospital and research infrastructure. Expansion of advanced diagnostic facilities, growing awareness among healthcare professionals, and ongoing clinical research programs are major factors supporting adoption of novel PCD therapies across the country.

Paraneoplastic Cerebellar Degeneration (PCD) Market Share

The Paraneoplastic Cerebellar Degeneration (PCD) industry is primarily led by well-established companies, including:

- Biogen Inc. (U.S.)

- Novartis AG (Switzerland)

- Roche Holding AG (Switzerland)

- Sanofi (France)

- Amgen Inc. (U.S.)

- Janssen Pharmaceuticals (U.S.)

- Pfizer Inc. (U.S.)

- Baxter International Inc. (U.S.)

- CSL Behring (Australia)

- Grifols S.A. (Spain)

- Takeda Pharmaceutical Company (Japan)

- Regeneron Pharmaceuticals (U.S.)

- Merck & Co., Inc. (U.S.)

- Fresenius Kabi AG (Germany)

Latest Developments in Global Paraneoplastic Cerebellar Degeneration (PCD) Market

- In July 2021, the International Paraneoplastic Neurologic Syndrome Diagnostic Criteria were updated to enhance the identification of PCD. The revisions incorporated newly discovered antibodies and emphasized the importance of early cancer screening and prompt treatment initiation. The updated guidelines aimed to improve diagnostic accuracy and patient outcomes

- In March 2025, a rare case of anti-Yo antibody-positive PCD was reported in a patient with squamous cell lung carcinoma. The patient showed significant improvement following immunotherapy and oncological treatment, highlighting the potential benefits of early intervention in mitigating neurological deterioration associated with PCD

- In January 2024, a comprehensive review examined the roles of CDR2 and CDR2L proteins in anti-Yo-mediated PCD. The study provided insights into the mechanisms underlying PCD and emphasized the need for further research to understand the pathophysiology and develop targeted therapies

- In February 2025, a case of PCD associated with anti-Hu and anti-Zic4 antibodies was reported, treated with high-dose intravenous methylprednisolone and plasmapheresis. The patient's condition improved, suggesting that early immunotherapy may be effective in managing PCD symptom

- In February 2025, a study highlighted that the PD-1 inhibitor pembrolizumab, used in cancer immunotherapy, may exacerbate PCD in some patients. This finding underscored the need for careful monitoring and management of neurological symptoms in patients undergoing immunotherapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.