Global Pathogen Detection Market

Market Size in USD Billion

USD

5.71 Billion

USD

10.57 Billion

2024

2032

USD

5.71 Billion

USD

10.57 Billion

2024

2032

| 2025 - 2032 | |

| USD 5.71 Billion | |

| USD 10.57 Billion | |

| % | |

|

Pathogen Detection Market Size

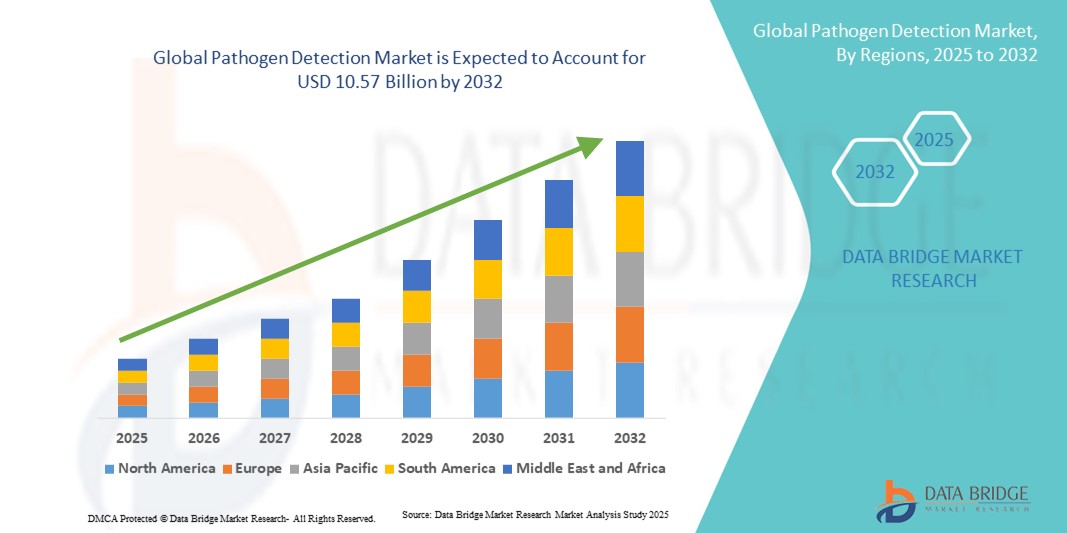

- The global pathogen detection market size was valued at USD 5.71 billion in 2024 and is expected to reach USD 10.57 billion by 2032, at a CAGR of 8.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of infectious diseases and the growing need for rapid, accurate, and reliable pathogen detection solutions across healthcare, research, and industrial sectors

- Furthermore, rising awareness among healthcare professionals, regulatory focus on timely disease diagnosis, and technological advancements in diagnostic instruments and assays are driving the adoption of pathogen detection solutions

Pathogen Detection Market Analysis

- Pathogen detection solutions, encompassing molecular, immunological, and rapid diagnostic platforms, are increasingly vital components of modern healthcare, research, and public health infrastructure due to their ability to provide rapid, accurate, and reliable identification of infectious agents across clinical and laboratory settings. These solutions enable hospitals, diagnostic laboratories, and public health authorities to respond swiftly to outbreaks, monitor disease prevalence, and implement timely interventions, significantly improving patient outcomes and disease management

- The escalating demand for Pathogen Detection solutions is primarily driven by increasing awareness of infectious diseases, rising prevalence of outbreaks, and the need for rapid, accurate, and reliable diagnostic tools in both clinical and research settings. Advanced detection systems are becoming critical for hospitals, diagnostic laboratories, and public health authorities to ensure timely identification and control of pathogens

- North America dominated the pathogen detection market with the largest revenue share of 32.5% in 2024, supported by advanced healthcare infrastructure, strong R&D activities, early adoption of novel diagnostic technologies, and favorable reimbursement policies. The U.S. remains the largest contributor within the region, experiencing substantial growth due to the adoption of innovative molecular, immunological, and rapid detection platforms in hospitals, research institutes, and diagnostic laboratories

- Asia-Pacific is expected to be the fastest-growing region in the Pathogen Detection market during the forecast period, driven by increasing urbanization, rising healthcare access, expanding laboratory networks, and growing awareness about infectious disease diagnostics in emerging economies such as China and India. The region’s rising disposable incomes and government initiatives for disease surveillance and epidemic preparedness further accelerate adoption

- The Rapid Tests segment dominated the pathogen detection market with the largest market revenue share of 56.4% in 2024, owing to its ability to deliver accurate results within short timeframes across clinical, food, and environmental applications

Report Scope and Pathogen Detection Market Segmentation

|

Attributes |

Pathogen Detection Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Pathogen Detection Market Trends

Growing Importance of Advanced and Rapid Diagnostic Tools

- A significant and accelerating trend in the global pathogen detection market is the increasing adoption of advanced molecular, immunological, and rapid diagnostic platforms. These technologies are significantly enhancing the accuracy, speed, and reliability of pathogen identification across clinical, research, and public health settings

- For instance, high-throughput PCR and real-time molecular assays allow hospitals and diagnostic laboratories to detect multiple pathogens simultaneously, enabling faster clinical decision-making and outbreak control. Similarly, rapid antigen and serological tests provide timely results in point-of-care and field-based applications, supporting immediate interventions

- Advanced diagnostics in Pathogen Detection enable features such as high sensitivity for low pathogen loads, multiplexing capabilities, and integration with laboratory information systems, facilitating efficient workflow management and precise reporting. These tools also reduce false negatives and improve the identification of asymptomatic carriers, crucial for public health surveillance and epidemiological studies

- The integration of diverse diagnostic platforms within laboratories allows centralized management of pathogen detection, from sample preparation to reporting. Through standardized protocols, laboratories can efficiently handle high sample volumes while maintaining accuracy and reproducibility, improving operational efficiency and scalability

- This trend toward more sensitive, rapid, and reliable diagnostic solutions is fundamentally reshaping expectations for pathogen detection and public health preparedness. Consequently, companies such as Qiagen, Roche, and Thermo Fisher are developing innovative platforms with automated workflows, multiplex detection, and enhanced data management capabilities

- The demand for rapid, accurate, and scalable Pathogen Detection solutions is growing rapidly across both healthcare and research sectors, as hospitals, diagnostic laboratories, and public health authorities increasingly prioritize timely disease detection, outbreak management, and epidemiological monitoring

Pathogen Detection Market Dynamics

Driver

Growing Need Due to Rising Infectious Disease Threats and Rapid Diagnostics Adoption

- The increasing prevalence of infectious diseases and outbreaks, coupled with the growing demand for rapid, accurate, and reliable diagnostic solutions, is a significant driver for the heightened adoption of Pathogen Detection systems

- For instance, in April 2024, Thermo Fisher Scientific announced the launch of its next-generation multiplex PCR platform, designed to enable faster and more precise detection of multiple pathogens simultaneously. Such innovations by key companies are expected to drive the Pathogen Detection industry growth in the forecast period

- As healthcare providers, research institutes, and public health authorities become more aware of emerging pathogens and the need for early intervention, advanced detection systems offer features such as high sensitivity, specificity, and reproducibility, providing a compelling advantage over conventional diagnostic methods

- Furthermore, the growing prevalence of hospital-acquired infections, zoonotic diseases, and community outbreaks is encouraging institutions to adopt comprehensive Pathogen Detection solutions capable of real-time monitoring, high-throughput screening, and automated reporting

- The increasing focus on point-of-care testing, outbreak preparedness, and integration of diagnostics with laboratory information management systems is propelling the adoption of advanced Pathogen Detection platforms in hospitals, diagnostic laboratories, and research facilities. The trend towards standardized, easy-to-use, and reliable detection systems further contributes to market growth

Restraint/Challenge

Concerns Regarding High Costs and Complex Implementation

- The relatively high initial investment required for advanced Pathogen Detection systems, including molecular and immunological platforms, can pose a barrier to adoption, particularly in developing regions or for smaller healthcare facilities with budget constraints

- In addition, the complexity of operating sophisticated detection platforms and the need for skilled personnel may limit adoption among laboratories lacking technical expertise or proper training infrastructure

- Addressing these challenges through cost-effective system designs, modular platforms, and comprehensive training programs is crucial for expanding market penetration. Companies such as Qiagen and Roche emphasize user-friendly interfaces, integrated workflows, and scalable solutions to reassure potential buyers

- While prices are gradually decreasing, the perceived premium for high-precision diagnostic technologies can still hinder widespread adoption, especially for facilities that do not require high-throughput or multiplex testing capabilities

- Overcoming these challenges through technology miniaturization, improved affordability, and initiatives to enhance laboratory capacity and workforce training will be vital for sustained growth in the Pathogen Detection market

Pathogen Detection Market Scope

The market is segmented on the basis of type, consistency, culture media, contaminant type, total count, technology, customer type, application, end user, and distribution channel.

- By Type

On the basis of type, the pathogen detection market is segmented into Products and Services. The Products segment dominated the largest market revenue share of 62.5% in 2024, owing to the widespread use of pathogen detection kits, instruments, and culture media across clinical, food, and environmental laboratories. These products provide rapid, reliable, and highly reproducible results, which are essential for effective outbreak monitoring and regulatory compliance. Laboratories heavily rely on these solutions to improve operational efficiency and minimize manual errors, while integration with automated systems enhances testing throughput. Continuous technological advancements in multiplex detection and point-of-care products further strengthen the segment’s leadership. Moreover, government initiatives and private sector investments in diagnostic infrastructure provide strong support for market growth, reinforcing the segment’s dominance.

The Services segment is expected to witness the fastest CAGR of 19.8% from 2025 to 2032, driven by increasing outsourcing of pathogen testing to specialized laboratories. These services provide expert analysis, high-throughput testing, and adherence to strict regulatory standards, making them attractive to industries, research institutions, and governmental organizations. The rising demand for third-party testing, especially in food safety, environmental monitoring, and clinical diagnostics, is fueling rapid adoption. Services also allow smaller labs or organizations lacking advanced infrastructure to access sophisticated testing solutions, further boosting growth potential.

- By Consistency

On the basis of consistency, the pathogen detection market is segmented into solid media and liquid media. The liquid Media segment dominated the largest market revenue share of 54.3% in 2024, driven by its adaptability in supporting a wide range of pathogens and compatibility with automated detection systems. Liquid media is widely preferred in clinical, food, and environmental laboratories for its rapid workflow, high reproducibility, and seamless integration with high-throughput platforms. Continuous innovations in selective enrichment and nutrient formulations further enhance the segment’s appeal. Regulatory approvals and standardized protocols make liquid media a reliable and trusted choice for critical pathogen detection applications.

The Solid Media segment is expected to witness the fastest CAGR of 18.5% from 2025 to 2032, supported by rising demand for pre-prepared agar plates and chromogenic media in both laboratory and field applications. Solid media allows visual confirmation of pathogen growth, colony differentiation, and detailed research studies, which are essential for outbreak investigations and epidemiological surveillance. Adoption is further driven by low-cost, ready-to-use formats that are easy to store and transport. Laboratories and research institutions increasingly rely on solid media for its robustness and versatility in various testing scenarios.

- By Culture Media

On the basis of culture media, the pathogen detection market is segmented into chemical composition and synthetic media. The Chemical Composition segment dominated the largest market revenue share of 57.8% in 2024, driven by its standardized formulations that provide reproducible and accurate pathogen growth. This segment is widely utilized across food, clinical, and environmental testing for ensuring compliance with regulatory standards. Laboratories prefer chemical media due to its reliability, long validation history, and compatibility with both traditional and automated workflows. Advances in selective and differential media formulations have further reinforced the segment’s dominance by enabling precise detection of targeted pathogens.

The Synthetic Media segment is expected to witness the fastest CAGR of 21.2% from 2025 to 2032, propelled by increasing research demand for chemically defined media. Synthetic media supports precise pathogen growth without interference from undefined components, making it ideal for high-precision microbiological and molecular testing. Its adoption is further boosted by the growing application of synthetic formulations in academic and industrial research laboratories. Laboratories value synthetic media for its consistency, reproducibility, and suitability for advanced pathogen detection studies.

- By Contaminant Type

On the basis of contaminant type, the pathogen detection market is segmented into Salmonella, E. Coli, Listeria, Campylobacter, Clostridium Perfringens, Pseudomonas, Cronobacter, Coliforms, Legionella, and Others. The Salmonella segment dominated the largest market revenue share of 21.5% in 2024, owing to its high prevalence in foodborne outbreaks and strict regulatory monitoring. Pathogen detection solutions targeting Salmonella are widely adopted across food processing units, clinical diagnostics, and environmental monitoring systems to prevent contamination and outbreaks. Rapid detection systems and automated testing platforms further reinforce the segment’s dominance. The segment’s growth is driven by increasing consumer safety awareness, stringent compliance requirements, and the necessity for efficient contamination prevention measures.

The Listeria segment is expected to witness the fastest CAGR of 20.7% from 2025 to 2032, fueled by rising contamination risks in ready-to-eat foods and stringent food safety regulations. Listeria testing has gained significant importance due to its potential public health impact and the high economic cost of product recalls. Advances in molecular detection techniques, immunoassays, and point-of-care testing kits have accelerated rapid identification of Listeria, facilitating timely interventions. The segment is further supported by increasing adoption in food safety monitoring, research applications, and regulatory compliance initiatives.

- By Total Count

On the basis of total count, the pathogen detection market is segmented into spoiling organisms, yeast and moulds, and others. The Spoiling Organisms segment dominated the largest market revenue share of 49.6% in 2024, driven by the essential role of monitoring quality in the food and beverage industry. Detecting spoilage organisms ensures product safety, minimizes wastage, and supports compliance with stringent regulatory standards. Laboratories are increasingly relying on automated systems and integration with laboratory information management systems (LIMS) to enhance efficiency and data accuracy. This segment benefits from technological advances in rapid detection kits and high-throughput screening tools, enabling timely identification of contamination. The increasing global demand for high-quality, safe consumables further reinforces its market dominance.

The Yeast and Moulds segment is expected to witness the fastest CAGR of 18.9% from 2025 to 2032, driven by growing detection demand in dairy, beverages, and pharmaceutical products. Early identification of fungal contamination helps prevent spoilage, extend product shelf-life, and maintain regulatory compliance. Rapid molecular tools, innovative kits, and automated workflows facilitate precise detection. Laboratories and manufacturing units are adopting these solutions to safeguard production lines and ensure consumer safety. Rising awareness regarding quality control and the increasing prevalence of fungal contamination in processed foods fuel market growth in this segment.

- By Technology

On the basis of technology, the pathogen detection market is segmented into rapid, traditional, and other molecular-based tests. The rapid tests segment dominated the largest market revenue share of 56.4% in 2024, owing to its ability to deliver accurate results within short timeframes across clinical, food, and environmental applications. Rapid tests enable timely interventions, high-throughput screening, and prevention of pathogen-related outbreaks. Laboratories benefit from user-friendly kits and automated systems that reduce manual errors and enhance productivity. The segment is widely preferred due to its cost-effectiveness, operational simplicity, and suitability for both on-site and laboratory-based testing. Continuous innovation in immunoassays and lateral flow tests strengthens adoption.

The molecular-based tests segment is expected to witness the fastest CAGR of 22.1% from 2025 to 2032, fueled by advances in PCR, next-generation sequencing, and biosensor technologies. Molecular testing offers high sensitivity, specificity, and rapid identification of low-level pathogens, critical for emerging infections and research applications. Growing investments in diagnostic R&D, increasing adoption in academic and industrial labs, and the need for regulatory-compliant testing drive growth. The integration of molecular tests with automated platforms further enhances throughput and precision, positioning this segment for robust market expansion.

- By Customer Type

On the basis of customer type, the pathogen detection market is segmented into service lab, industry, and governmental/non-profit organization. The Industry segment dominated the largest market revenue share of 51.2% in 2024, driven by the extensive need for pathogen testing in food, pharmaceutical, and biotechnology sectors. Industries increasingly rely on validated protocols, high-throughput systems, and automation to ensure safety and regulatory compliance. Routine quality monitoring, process optimization, and contamination prevention are major factors driving adoption. Growing consumer awareness of product safety and regulatory scrutiny further reinforce its dominance. The segment is strengthened by technological advancements in rapid detection and molecular tools, enabling timely interventions.

The Governmental/Non-Profit Organization segment is expected to witness the fastest CAGR of 19.4% from 2025 to 2032, driven by initiatives in public health surveillance, outbreak monitoring, and government-funded programs. Increased funding for disease prevention, regulatory emphasis, and public safety initiatives support rapid adoption. Government laboratories and NGOs are leveraging advanced pathogen detection tools to enhance data accuracy and improve epidemiological tracking. Collaborations with academic and industrial research centers further accelerate growth in this segment.

- By Application

On the basis of application, the pathogen detection market is segmented into diagnostics, pathology, forensics, clinical research, and drug discovery. The Diagnostics segment dominated the largest market revenue share of 55.3% in 2024, driven by the growing importance of early pathogen detection for preventive healthcare and food safety. Diagnostics applications are critical for timely interventions, outbreak control, and ensuring regulatory compliance across clinical, environmental, and food testing sectors. Technological innovations in rapid testing, high-throughput analysis, and molecular platforms further support segment adoption. Laboratories and industries increasingly rely on diagnostics to maintain safety standards, improve operational efficiency, and enhance product quality. Rising consumer awareness regarding early detection and preventive measures strengthens market leadership.

The clinical research segment is expected to witness the fastest CAGR of 21.6% from 2025 to 2032, supported by increasing investments in R&D for emerging pathogens, drug development, and advanced detection technologies. Academic and industrial research laboratories are adopting molecular and rapid detection tools to accelerate innovation and ensure accurate pathogen identification. Growing collaborations between research institutes, pharmaceutical companies, and governmental agencies boost adoption. The focus on developing novel therapeutics, vaccines, and preventive strategies further drives segment growth. Expansion of research programs in emerging markets also contributes to the rising CAGR.

- By End-User

On the basis of end-user, the pathogen detection market is segmented into pathology laboratories, diagnostic centers, hospitals, biotechnology companies, pharmaceutical companies, culture collection repositories, cooling towers, blood banks, and others. The Pathology Laboratories segment dominated the largest market revenue share of 47.5% in 2024, owing to its advanced equipment, skilled workforce, and large testing capacity. These laboratories serve hospitals, research institutions, and commercial clients, providing comprehensive pathogen detection solutions. Adoption is driven by high-throughput testing, automated workflows, and compliance with regulatory standards. Integration with data management systems ensures accuracy and timely reporting. Continuous investment in cutting-edge technologies and infrastructure reinforces the segment’s leadership.

The diagnostic centers segment is expected to witness the fastest CAGR of 20.2% from 2025 to 2032, driven by growing outsourcing of pathogen testing and expansion of independent laboratories. Diagnostic centers provide flexible, cost-effective, and rapid testing solutions for urban and semi-urban populations. Increasing adoption of molecular and rapid detection methods enables accurate and timely results. These centers are preferred for their accessibility, specialized testing services, and scalability. Rising awareness and demand for decentralized testing further accelerate the segment’s growth trajectory.

- By Distribution Channel

On the basis of distribution channel, the pathogen detection market is segmented into direct tender and retail sales. The direct tender segment dominated the largest market revenue share of 53.1% in 2024, driven by bulk procurement by hospitals, industries, and governmental agencies for high-volume pathogen testing. This channel ensures reliability, continuous supply, and compliance with regulatory requirements. Long-term contracts, efficient logistics, and consistency in product quality strengthen adoption. Large organizations prefer direct tenders for cost-effective, high-capacity operations. The segment also benefits from centralized purchasing strategies and robust supplier relationships.

The retail sales segment is expected to witness the fastest CAGR of 18.7% from 2025 to 2032, fueled by growing demand for ready-to-use pathogen detection kits suitable for smaller laboratories, academic research, and field applications. Retail channels offer convenience, affordability, and accessibility for users with limited procurement capacity. Ready-to-use formats reduce setup time, simplify workflows, and facilitate rapid results. Adoption is further supported by the increasing presence of diagnostic solutions in decentralized locations and emerging markets. Technological improvements in user-friendly kits and reagents reinforce market growth.

Pathogen Detection Market Regional Analysis

- North America dominated the pathogen detection market with the largest revenue share of 32.5% in 2024, supported by advanced healthcare infrastructure, strong R&D activities, early adoption of novel diagnostic technologies, and favorable reimbursement policies. The U.S. remains the largest contributor within the region, experiencing substantial growth due to the adoption of innovative molecular, immunological, and rapid detection platforms in hospitals, research institutes, and diagnostic laboratories

- Consumers and institutions in the region highly value the accuracy, speed, and reliability of advanced Pathogen Detection systems, which enable early diagnosis and effective outbreak management

- This widespread adoption is further supported by high healthcare spending, a technologically advanced medical ecosystem, and strong governmental support for infectious disease monitoring and control, establishing Pathogen Detection as a critical component in both clinical and research applications

U.S. Pathogen Detection Market Insight

The U.S. pathogen detection market captured the largest revenue share in 2024 within North America, fueled by the swift uptake of advanced diagnostic platforms and increasing investment in healthcare technologies. Hospitals and research institutions are increasingly prioritizing rapid and precise pathogen identification for effective disease management. The growing emphasis on laboratory automation, multiplex testing, and integration with hospital information systems further propels the Pathogen Detection industry. Moreover, regulatory support and reimbursement policies continue to drive the expansion of advanced diagnostic testing across clinical and research facilities.

Europe Pathogen Detection Market Insight

The Europe pathogen detection market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations and the rising need for accurate infectious disease diagnostics. Increasing investments in laboratory infrastructure and technological upgrades are fostering the adoption of advanced detection systems. European healthcare institutions are also focused on rapid diagnostics and early intervention strategies, which further fuels market growth. The region is witnessing significant expansion across hospitals, diagnostic laboratories, and research centers.

U.K. Pathogen Detection Market Insight

The U.K. pathogen detection market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing government initiatives for disease surveillance and improved laboratory networks. Rising awareness regarding infectious diseases and the demand for early and accurate diagnostics are encouraging healthcare providers to adopt advanced detection platforms. The country’s robust healthcare infrastructure and strong research ecosystem are expected to continue stimulating market growth.

Germany Pathogen Detection Market Insight

The Germany pathogen detection market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of infectious disease management and growing investments in healthcare technology. Germany’s well-developed healthcare infrastructure, coupled with its emphasis on research and innovation, promotes the adoption of advanced pathogen detection solutions. Hospitals, diagnostic laboratories, and research institutions are increasingly relying on high-precision diagnostic platforms to ensure timely identification and treatment of infections.

Asia-Pacific Pathogen Detection Market Insight

The Asia-Pacific pathogen detection market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, rising healthcare access, expanding laboratory networks, and growing awareness about infectious disease diagnostics in emerging economies such as China, Japan, and India. The region’s rising disposable incomes and government initiatives for disease surveillance and epidemic preparedness further accelerate adoption.

Japan Pathogen Detection Market Insight

The Japan pathogen detection market is gaining momentum due to the country’s high-tech healthcare ecosystem, rapid urbanization, and strong focus on disease prevention and early diagnosis. Healthcare providers are increasingly adopting advanced molecular, immunological, and rapid detection systems. The aging population and rising emphasis on proactive healthcare management further support market expansion in both clinical and research settings.

China Pathogen Detection Market Insight

The China pathogen detection market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country's expanding middle class, rapid urbanization, and increasing investments in healthcare infrastructure. Hospitals, diagnostic laboratories, and research centers are adopting advanced detection platforms to meet the growing demand for rapid and accurate pathogen identification. Government initiatives promoting epidemic preparedness, disease surveillance programs, and development of domestic diagnostic technologies are key factors propelling market growth in China.

Pathogen Detection Market Share

The pathogen detection industry is primarily led by well-established companies, including:

- Merck KGaA (Germany)

- Thermo Fisher Scientific Inc. (U.S.)

- BIOMÉRIEUX (France)

- Agilent Technologies, Inc. (U.S.)

- BD (U.S.)

- SGS Société Générale de Surveillance SA (Switzerland)

- Veritas (India)

- Intertek Group plc (U.K.)

- Eurofins Scientific (Luxembourg)

- Mérieux NutriSciences (France)

- ifp-labs GmbH (Germany)

- Microbac Laboratories, Inc. (U.S.)

- FoodChain ID Group (U.S.)

- AsureQuality (New Zealand)

- Campden BRI (U.K.)

- ANGLE plc (U.K.)

Latest Developments in Global Pathogen Detection Market

- In September 2024, Roche Diagnostics introduced the cobas Respiratory flex test, the first to utilize its novel TAGS (Temperature-Activated Generation of Signal) technology. This advancement enables the simultaneous detection of up to 15 pathogens in a single PCR test, enhancing high-throughput molecular diagnostics for respiratory infections

- In December 2024, chemists at the University at Albany developed a rapid salmonella detection test employing a paper strip that changes color in the presence of the bacterial genome. This innovation allows for quick screening of salmonella in food products, reducing detection time from days to hours

- In October 2024, Bioeureka, in collaboration with Mila, launched an AI-powered pathogen recognition app designed for laboratory use. This portable solution leverages machine learning to identify pathogens swiftly and accurately, aiming to become a standard tool in microbiology laboratories globally

- In August 2025, researchers highlighted the role of metagenomic next-generation sequencing (mNGS) in pathogen detection. The integration of AI with mNGS facilitates the identification of novel pathogens, enhancing outbreak response capabilities and epidemiological surveillance

- In March 2025, Oak Ridge National Laboratory (ORNL) introduced BOVC (Bio-Optical Volatile Compound) instrumentation, capable of detecting unique volatile organic compounds emitted by plants and pathogens. This technology offers a non-invasive method for early identification of plant diseases, potentially transforming agricultural pathogen monitoring

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.