Global Peptide Drug Conjugate Therapeutics Market

Market Size in USD Billion

USD

1.46 Billion

USD

7.07 Billion

2025

2033

USD

1.46 Billion

USD

7.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.46 Billion | |

| USD 7.07 Billion | |

| % | |

|

Peptide-Drug Conjugate Therapeutics Market Size

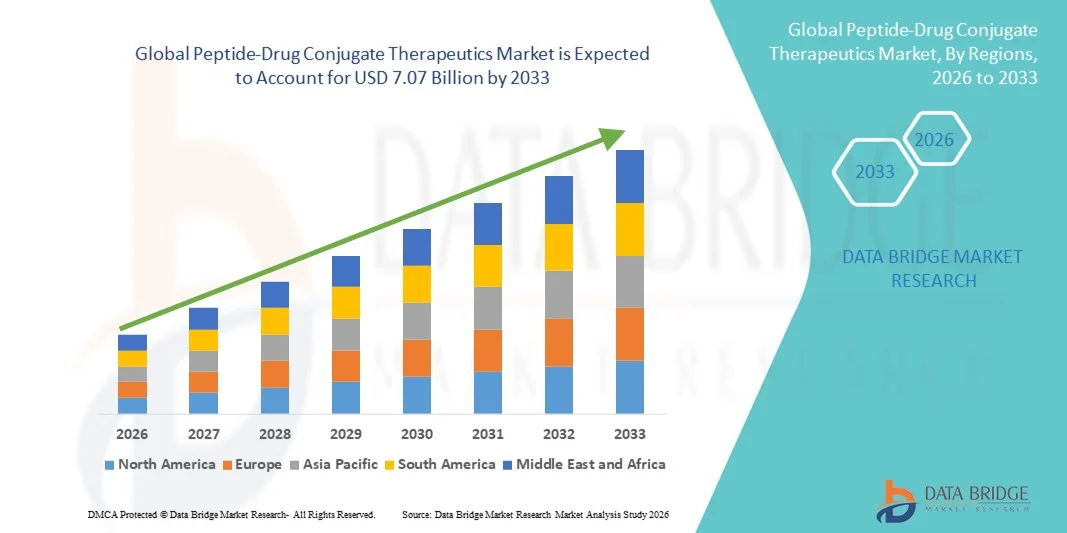

- The global peptide-drug conjugate therapeutics market size was valued at USD 1.46 billion in 2025 and is expected to reach USD 7.07 billion by 2033, at a CAGR of 21.80% during the forecast period

- The market growth is largely fueled by advancements in targeted therapeutic technologies and peptide conjugation platforms, which enhance drug delivery precision, reduce systemic toxicity, and improve clinical outcomes in oncology and other chronic disease segments

- Furthermore, rising prevalence of cancer globally, increasing investment in precision medicine research, and expanding clinical pipelines for peptide‑based conjugates are driving stronger adoption across pharmaceutical and biotech industries, positioning peptide‑drug conjugates as a cornerstone of next‑generation therapeutic solution

Peptide-Drug Conjugate Therapeutics Market Analysis

- Peptide‑drug conjugates (PDCs), combining therapeutic peptides with potent drug molecules, are increasingly vital in modern targeted therapy and precision medicine due to their ability to deliver drugs selectively to diseased cells while minimizing systemic toxicity, making them highly relevant in oncology and other chronic disease treatments

- The escalating demand for peptide‑drug conjugates is primarily fueled by advancements in peptide conjugation technologies, growing investment in targeted therapeutics, and rising clinical adoption for cancer and rare disease therapies

- North America dominated the peptide‑drug conjugate therapeutics market with the largest revenue share of 42.9% in 2025, driven by a strong biotech ecosystem, extensive R&D infrastructure, early adoption of novel therapies, and the presence of key industry players developing advanced PDCs for oncology, infectious diseases, and autoimmune conditions

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to expanding healthcare infrastructure, increasing incidence of cancer, growing biotech investments, and rising awareness of advanced targeted therapies

- Cytotoxic peptide-drug conjugates segment dominated the market with a market share of 45.6% in 2025, driven by their proven efficacy in selectively killing cancer cells and widespread adoption in oncology clinical trials and commercial therapies

Report Scope and Peptide-Drug Conjugate Therapeutics Market Segmentation

|

Attributes |

Peptide-Drug Conjugate Therapeutics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Peptide-Drug Conjugate Therapeutics Market Trends

Precision Targeting and Multimodal Therapy Integration

- A significant and accelerating trend in the global peptide‑drug conjugate therapeutics market is the integration of highly selective targeting peptides with potent drug payloads, enhancing therapeutic efficacy while reducing off-target toxicity

- For instance, Melflufen combines cytotoxic payloads with tumor-homing peptides to selectively target multiple myeloma cells, minimizing systemic exposure and side effects

- Integration with multimodal therapy approaches enables PDCs to be combined with immunotherapy, chemotherapy, or radiotherapy for synergistic effects. For instance, ANG1005 is being evaluated alongside standard chemotherapy to improve brain tumor penetration and therapeutic outcomes

- Advanced linker technologies allow controlled release of drugs at specific sites, optimizing pharmacokinetics and improving patient outcomes through precision therapy

- The trend toward more sophisticated, targeted, and combinational therapeutics is fundamentally reshaping treatment paradigms in oncology and rare diseases, driving the development of next-generation PDC platforms

- The demand for PDCs with enhanced targeting, safety profiles, and combinational potential is growing rapidly across both clinical trial pipelines and commercial therapies, as pharmaceutical companies prioritize precision medicine solutions

- Advancements in bioinformatics and peptide design platforms are enabling faster development of novel PDCs, accelerating pipeline expansion and improving drug discovery efficiency

Peptide-Drug Conjugate Therapeutics Market Dynamics

Driver

Rising Prevalence of Cancer and Investment in Targeted Therapies

- The increasing prevalence of cancer and other chronic diseases, coupled with growing investments in precision medicine, is a significant driver for the heightened demand for peptide‑drug conjugates

- For instance, in June 2025, Nordic Nanovector advanced its Betalutin clinical program targeting follicular lymphoma, highlighting investment in PDC development as a growth catalyst

- As clinicians seek therapies with higher efficacy and fewer side effects, PDCs offer advanced features such as selective tumor targeting, controlled payload release, and reduced systemic toxicity, providing a compelling alternative to conventional treatments

- Furthermore, increasing funding for biotech research and clinical trial expansion is making PDCs an integral component of innovative therapeutic pipelines, accelerating adoption in oncology and rare disease treatment

- The ability to design PDCs for individualized patient profiles and integrate them with combination therapies enhances their therapeutic potential, propelling adoption in both hospital and specialty clinical settings

- Strategic partnerships between biotech firms and large pharmaceutical companies are driving innovation and commercialization, further strengthening market growth

- Expansion of companion diagnostics that identify patients likely to respond to specific PDCs is boosting clinical adoption and improving therapeutic outcomes

Restraint/Challenge

High Development Costs and Regulatory Hurdles

- The complex design, rigorous clinical evaluation, and costly manufacturing of peptide‑drug conjugates pose significant challenges for broader market adoption and scalability

- For instance, the development of ANG1005 required extensive preclinical validation and regulatory approvals to ensure safe blood-brain barrier penetration, reflecting the high barrier to entry

- Navigating strict regulatory requirements and achieving clinical trial success is crucial for market entry, making it a resource-intensive and time-consuming process for smaller biotech firms

- Furthermore, while PDCs offer improved efficacy, pricing for advanced therapies can limit patient access, especially in regions with constrained healthcare budgets or limited insurance coverage

- Overcoming these challenges through streamlined clinical development, regulatory guidance, and cost-effective manufacturing will be vital for sustaining long-term growth and broader adoption of PDC therapies

- Limited long-term clinical data on safety and efficacy may slow adoption, as healthcare providers require robust evidence for widespread use

- Intellectual property complexities and competition from alternative targeted therapies, such as antibody-drug conjugates, can create additional barriers for new entrants and pipeline expansion

Peptide-Drug Conjugate Therapeutics Market Scope

The market is segmented on the basis of product type, application, and end user.

- By Product Type

On the basis of product type, the market is segmented into cytotoxic peptide‑drug conjugates, radiolabeled peptide conjugates, peptide–oligonucleotide conjugates, multivalent peptide conjugates, and specific pipeline products. Cytotoxic Peptide‑Drug Conjugates dominated the market with the largest market revenue share of 45.6% in 2025, driven by their ability to selectively deliver potent cytotoxic agents to cancer cells while minimizing systemic toxicity. These PDCs have been widely adopted in oncology clinical trials and commercial therapies, offering improved treatment outcomes for patients with hematological and solid tumors. The market growth is supported by strong clinical evidence, established manufacturing processes, and increasing physician trust in cytotoxic PDC therapies. Furthermore, the cytotoxic segment benefits from multiple approved drugs and a growing number of pipeline candidates. Healthcare providers prefer these conjugates due to their predictable efficacy and integration into standard oncology treatment protocols. Ongoing research continues to optimize linker technologies, payload selection, and targeting peptides, further reinforcing their dominance in the market.

Peptide–Oligonucleotide Conjugates are anticipated to witness the fastest CAGR of 21% from 2026 to 2033, driven by growing demand for gene-targeted therapies and RNA-based treatments. These conjugates enable precise delivery of oligonucleotides into target cells, offering therapeutic options for rare genetic diseases and hard-to-treat conditions. Their adoption is accelerated by advancements in RNA therapeutics and increasing investment in personalized medicine. Biotech firms are developing novel peptide sequences to enhance cellular uptake and stability of oligonucleotides, improving clinical outcomes. The segment also benefits from regulatory incentives for innovative therapies addressing unmet medical needs. Rising awareness among clinicians and patients about gene-targeted treatments is contributing to higher uptake globally.

- By Application

On the basis of application, the market is segmented into cancer treatment, infectious diseases, autoimmune disorders, metabolic diseases, neurological conditions, and other diseases. Cancer Treatment dominated the market with a revenue share of 52% in 2025, as PDCs offer targeted delivery of cytotoxic drugs to tumor cells, improving efficacy while reducing systemic toxicity. Oncology remains the primary focus of PDC research, with multiple approved therapies and ongoing clinical trials. The segment is supported by increasing cancer incidence worldwide, particularly hematological and solid tumors, which drive demand for targeted therapies. Pharmaceutical companies are heavily investing in pipeline development for new oncology indications, further consolidating market dominance. Hospitals and specialty clinics prefer PDCs for oncology due to their ability to integrate with standard chemotherapy protocols. Clinical evidence and real-world data continue to demonstrate superior outcomes, enhancing physician and patient confidence in these therapies.

Infectious Diseases are expected to witness the fastest growth at a CAGR of 19% from 2026 to 2033, fueled by the development of peptide conjugates targeting intracellular pathogens and antibiotic-resistant infections. These therapies enable precision targeting, minimizing off-target effects and reducing antimicrobial resistance risks. Increasing prevalence of infectious diseases in emerging markets is driving adoption. Researchers are exploring novel peptide sequences for enhanced pathogen penetration and immune modulation. Government funding and incentives for infectious disease research are further boosting pipeline expansion. Rising awareness among healthcare providers about targeted antimicrobial therapies is accelerating market acceptance globally.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, clinical research centers, and contract research organizations (CROs). Hospitals dominated the market with a revenue share of 50% in 2025, as they provide centralized administration and monitoring of complex PDC therapies, particularly in oncology settings. Hospitals benefit from the availability of trained clinical staff, infusion infrastructure, and regulatory compliance support, making them ideal settings for PDC administration. The segment is further supported by rising hospital adoption of precision medicine programs and growing cancer patient populations. Integration with clinical trial programs and specialty treatment centers also drives hospital demand. Healthcare providers prefer hospitals due to their ability to deliver controlled, supervised therapy with real-time patient monitoring. Hospitals also facilitate access to advanced PDC therapies covered under insurance and national health schemes.

Clinical Research Centers are expected to witness the fastest CAGR of 20% from 2026 to 2033, driven by the increasing number of PDC clinical trials and early-stage development programs. These centers play a critical role in evaluating novel peptide-drug conjugates for safety, efficacy, and targeted delivery. The growth is fueled by rising R&D investments from biotech firms and pharmaceutical companies. Advanced infrastructure, specialized expertise, and regulatory knowledge at these centers accelerate the testing of innovative PDC candidates. Partnerships with global pharma companies enhance clinical research capabilities and speed up drug development. Expansion of trials into emerging regions also supports faster adoption of PDC therapies in clinical research settings.

Peptide-Drug Conjugate Therapeutics Market Regional Analysis

- North America dominated the peptide‑drug conjugate therapeutics market with the largest revenue share of 42.9% in 2025, driven by a strong biotech ecosystem, extensive R&D infrastructure, early adoption of novel therapies, and the presence of key industry players developing advanced PDCs for oncology, infectious diseases, and autoimmune conditions

- Healthcare providers and research institutions in the region highly value the targeted delivery capability, improved safety profile, and clinical efficacy offered by peptide-drug conjugates, particularly in cancer and rare disease treatment applications

- This widespread adoption is further supported by robust R&D funding, a strong presence of leading biotechnology and pharmaceutical companies, favorable regulatory pathways for innovative therapies, and increasing patient access to advanced targeted treatment options, establishing peptide-drug conjugates as a preferred next-generation therapeutic solution

U.S. Peptide-Drug Conjugate Therapeutics Market Insight

The U.S. peptide-drug conjugate therapeutics market captured the largest revenue share of 79% in 2025 within North America, fueled by strong oncology drug development, substantial federal research funding, and rapid adoption of precision medicine approaches. Healthcare providers are increasingly prioritizing targeted therapies that enhance efficacy while minimizing systemic toxicity in cancer and rare disease treatment. The growing presence of leading biotechnology firms, robust clinical trial activity, and accelerated regulatory pathways for innovative biologics further propel the market. Moreover, expanding collaborations between academic research institutions and pharmaceutical companies are significantly contributing to the market’s expansion.

Europe Peptide-Drug Conjugate Therapeutics Market Insight

The Europe peptide-drug conjugate therapeutics market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong regulatory support for innovative oncology therapies and rising cancer prevalence. Increasing healthcare expenditure, coupled with government-backed research initiatives, is fostering the adoption of targeted conjugate therapies. European healthcare systems emphasize clinical effectiveness and safety, encouraging the integration of peptide-drug conjugates into treatment protocols. The region is experiencing steady growth across hospital oncology departments and specialized cancer centers, with novel therapies being incorporated into both first-line and advanced-stage treatment strategies.

U.K. Peptide-Drug Conjugate Therapeutics Market Insight

The U.K. peptide-drug conjugate therapeutics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investment in life sciences and a strong focus on cancer innovation programs. In addition, the rising burden of chronic diseases is encouraging healthcare providers to adopt targeted therapeutic solutions with improved safety profiles. The U.K.’s established clinical research ecosystem, alongside supportive regulatory frameworks for breakthrough therapies, is expected to continue stimulating market growth.

Germany Peptide-Drug Conjugate Therapeutics Market Insight

The Germany peptide-drug conjugate therapeutics market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced biopharmaceutical manufacturing capabilities and growing demand for precision oncology treatments. Germany’s strong healthcare infrastructure, combined with its emphasis on research innovation and high-quality standards, promotes the adoption of novel conjugate therapies in hospitals and specialty clinics. The integration of peptide-drug conjugates into comprehensive cancer care programs is also becoming increasingly prevalent, aligning with local clinical guidelines and patient expectations for advanced therapeutic solutions.

Asia-Pacific Peptide-Drug Conjugate Therapeutics Market Insight

The Asia-Pacific peptide-drug conjugate therapeutics market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by increasing cancer incidence, expanding healthcare access, and rising investments in biotechnology across China, Japan, and India. The region’s growing focus on advanced medical treatments, supported by government initiatives promoting pharmaceutical innovation, is accelerating adoption. Furthermore, as APAC strengthens its role in biopharmaceutical manufacturing and clinical research, the accessibility and affordability of peptide-drug conjugate therapies are expanding to a broader patient population.

Japan Peptide-Drug Conjugate Therapeutics Market Insight

The Japan peptide-drug conjugate therapeutics market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong emphasis on oncology innovation. The Japanese market places significant importance on treatment safety and precision, driving adoption of targeted conjugate therapies in cancer care. Integration of peptide-drug conjugates with existing chemotherapy and immunotherapy regimens is fueling growth. Moreover, Japan’s supportive regulatory pathways for regenerative and innovative medicines are likely to spur demand for next-generation targeted therapeutics in both hospital and research settings.

India Peptide-Drug Conjugate Therapeutics Market Insight

The India peptide-drug conjugate therapeutics market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding oncology patient pool, improving healthcare infrastructure, and rising adoption of advanced biologics. India is emerging as a key destination for clinical trials and biopharmaceutical manufacturing, supporting the development and commercialization of targeted therapies. The push toward expanding cancer treatment facilities, combined with increasing collaboration between domestic biotech firms and global pharmaceutical companies, is a key factor propelling the peptide-drug conjugate therapeutics market in India.

Peptide-Drug Conjugate Therapeutics Market Share

The Peptide-Drug Conjugate Therapeutics industry is primarily led by well-established companies, including:

- Theratechnologies Inc. (Canada)

- Bicycle Therapeutics (U.K.)

- PeptiDream Inc. (Japan)

- Sanofi (France)

- Novo Nordisk (Denmark)

- Amgen (U.S.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Cybrexa Therapeutics Inc. (U.S.)

- Oncopeptides AB (Sweden)

- Soricimed Biopharma Inc. (U.S.)

- Esperance Pharmaceuticals Inc. (U.S.)

- PepGen Corporation (U.S.)

- Protagonist Therapeutics Inc. (U.S.)

- Alteogen Inc. (South Korea)

- Metsera Inc. (U.S.)

- Zealand Pharma (Denmark)

- Avacta Therapeutics (U.K.)

- Coherent Biopharma (China)

What are the Recent Developments in Global Peptide-Drug Conjugate Therapeutics Market?

- In June 2025, the FDA granted accelerated approval to datopotamab deruxtecan-dlnk for adults with locally advanced or metastatic EGFR-mutated non-small cell lung cancer (NSCLC), expanding its clinical indications and validating the efficacy of conjugated targeted therapies in diverse cancer types. This milestone indicates growing regulatory support for advanced conjugate therapeutics in oncology

- In March 2025, Cybrexa Therapeutics announced new preclinical data on its tumor-selective alphalex™ peptide-drug conjugates presented at the ESMO Targeted Anticancer Therapies Congress, demonstrating tumor-selective delivery of potent anticancer payloads with strong efficacy and immune-modulating activity in multiple cancer models. This preclinical breakthrough highlights progress in antigen-independent PDC platforms that aim to improve therapeutic index and reduce off-target toxicity in oncology treatments

- In January 2025, the FDA approved datopotamab deruxtecan-dlnk (Datroway), an antibody-drug conjugate with peptide linker technology, for unresectable or metastatic HR-positive, HER2-negative breast cancer, providing a new targeted therapeutic option with enhanced delivery mechanisms. Though technically an ADC, this approval demonstrates the clinical acceptance of peptide linker-based conjugation strategies in targeted therapy

- In May 2023, Bayer AG entered a strategic collaboration with Bicycle Therapeutics to develop novel radioconjugates using peptide technology for cancer indications, expanding the PDC pipeline and leveraging peptide-based targeting platforms. This partnership aimed to optimize highly selective peptides for improved delivery of therapeutic payloads, reflecting growing industrial interest in PDC innovation

- In October 2021, Oncopeptides announced the withdrawal of Pepaxto from the U.S. market after clinical trial data failed to show overall survival benefit, underscoring regulatory and safety challenges for PDCs in real-world therapeutic use

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.