Global Photoacoustic Imaging Market

Market Size in USD Million

USD

180.13 Million

USD

709.92 Million

2024

2032

USD

180.13 Million

USD

709.92 Million

2024

2032

| 2025 - 2032 | |

| USD 180.13 Million | |

| USD 709.92 Million | |

| % | |

|

Photoacoustic Imaging Market Size

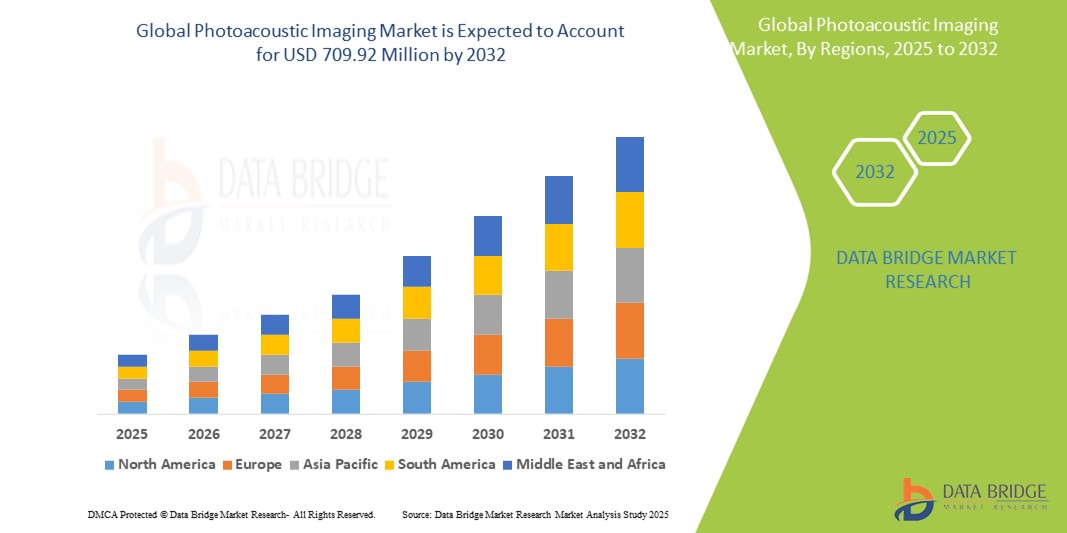

- The global photoacoustic imaging market size was valued at USD 180.13 million in 2024 and is expected to reach USD 709.92 million by 2032, at a CAGR of 18.70% during the forecast period

- The market growth is largely fueled by the rising adoption and ongoing technological advancements in biomedical imaging and diagnostic systems, particularly within the realm of non-invasive and real-time imaging techniques. Photoacoustic imaging, which combines optical and ultrasound modalities, is gaining traction due to its superior resolution, depth of penetration, and ability to visualize both structural and functional information, thereby enhancing diagnostic precision across various medical applications

- Furthermore, the increasing demand for safer, more accurate, and non-ionizing diagnostic tools is positioning photoacoustic imaging as a cutting-edge alternative to conventional imaging techniques such as MRI, CT, and PET. These converging factors are accelerating the adoption of photoacoustic imaging solutions in oncology, cardiology, neurology, and dermatology, thereby significantly boosting the industry's growth trajectory

Photoacoustic Imaging Market Analysis

- Photoacoustic imaging, leveraging the photoacoustic effect to provide high-resolution, high-contrast images of biological tissues, is an increasingly vital component of modern medical diagnostics and research systems in both clinical and preclinical settings due to its non-invasiveness, deep tissue penetration, and functional imaging capabilities

- The escalating demand for photoacoustic imaging is primarily fueled by the growing prevalence of chronic diseases, the increasing need for early and accurate diagnosis, and a rising preference for non-ionizing and non-invasive imaging modalities

- North America dominated the photoacoustic imaging market with the largest revenue share of 39.42% in 2024. This leadership is characterized by significant investments in biomedical research, advanced healthcare infrastructure, a strong presence of key industry players and academic institutions, and high adoption rates of cutting-edge diagnostic technologies

- Asia-Pacific is expected to be the fastest-growing region in the photoacoustic imaging market during the forecast period, due to increasing healthcare expenditure, rising prevalence of chronic diseases, expanding research and development activities, and a growing emphasis on early disease diagnosis in countries such as China, Japan, and India

- Photoacoustic computed tomography segment dominated the photoacoustic imaging market with a market share of 58.6% in 2024, driven by its established capability for deep tissue imaging and volumetric data acquisition, making it crucial for applications in cancer detection, brain imaging, and cardiovascular studies

Report Scope and Photoacoustic Imaging Market Segmentation

|

Attributes |

Photoacoustic Imaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Photoacoustic Imaging Market Trends

“Technological Advancements Driving Clinical Adoption and Imaging Accuracy”

- A significant and accelerating trend in the global photoacoustic imaging (PAI) market is the continuous advancement of hybrid imaging systems that integrate PAI with ultrasound, optical coherence tomography (OCT), and other modalities to improve clinical diagnostic accuracy and image depth

- For instance, FUJIFILM VisualSonics has introduced the Vevo LAZR-X system, which combines high-frequency ultrasound and photoacoustics, enabling researchers and clinicians to visualize molecular, functional, and anatomical data simultaneously. This multi-modal integration significantly enhances tissue characterization, particularly in oncology and vascular imaging

- The integration of tunable laser sources and real-time spectral unmixing algorithms has improved the specificity and resolution of photoacoustic images, allowing for better visualization of hemoglobin, melanin, lipids, and other chromophores. This advancement is crucial for applications such as tumor angiogenesis monitoring, hypoxia assessment, and metabolic imaging

- Advanced imaging probes and contrast agents are being developed to target specific molecular markers, enabling molecular photoacoustic imaging for personalized medicine. For example, nanoparticle-based contrast agents tailored for cancer biomarkers are being explored to increase the sensitivity of tumor detection using PAI

- The miniaturization of imaging components is enabling the development of portable and handheld photoacoustic devices, which are particularly promising for point-of-care diagnostics and intraoperative imaging. These compact systems offer real-time guidance during surgical procedures, potentially improving outcomes in tumor resection and vascular surgeries

- This growing emphasis on technological innovation and clinical integration is transforming the photoacoustic imaging landscape. As the industry moves toward broader hospital adoption, companies such as iThera Medical, Seno Medical, and TomoWave Laboratories are accelerating product development and clinical trials to position PAI as a standard imaging tool in oncology, cardiology, and dermatology

Photoacoustic Imaging Market Dynamics

Driver

“Growing Need Due to Rising Demand for Non-Invasive Imaging and Early Disease Detection”

- The increasing demand for non-invasive, high-resolution diagnostic tools in clinical and research settings is a significant driver for the growing adoption of photoacoustic imaging (PAI) technologies across various medical fields

- For instance, in March 2024, FUJIFILM VisualSonics, Inc. announced a new generation of its Vevo LAZR-X system, incorporating enhanced multispectral imaging capabilities for improved tumor characterization and vascular imaging. Innovations such as these are expected to fuel PAI market growth during the forecast period

- As healthcare systems globally shift towards early disease detection and precision diagnostics, PAI offers a compelling alternative to traditional imaging methods by combining optical contrast with ultrasound penetration—enabling detailed visualization of tissues, blood oxygenation, and molecular markers without ionizing radiation

- Furthermore, the rising prevalence of chronic diseases such as cancer and cardiovascular disorders has intensified the need for real-time functional imaging, driving the adoption of photoacoustic solutions in both hospitals and research institutes

- The ability of PAI to visualize biological processes such as angiogenesis, hypoxia, and inflammation in vivo—without the need for invasive procedures—is positioning it as a preferred tool in preclinical research and clinical diagnostics. Growing awareness and clinical validation are expected to accelerate its integration into routine healthcare imaging practices

Restraint/Challenge

“High Cost and Limited Commercial Adoption Due to Technological Complexity”

- Despite its significant clinical and research advantages, the high cost of advanced photoacoustic imaging systems remains a major barrier to broader adoption. These systems require precision lasers, transducers, and specialized software, making them expensive for many institutions, especially in low-resource settings

- For instance, many high-performance PAI platforms currently used in academic or pharmaceutical R&D labs require six-figure capital investments, limiting access primarily to large universities or well-funded research centers

- In addition, the technological complexity of PAI—including the need for operator training, precise calibration, and maintenance—creates operational challenges that can deter clinical use. The learning curve for interpreting multispectral data and integrating PAI into clinical workflows further hinders its adoption in smaller hospitals or diagnostic labs

- Moreover, while PAI has shown promising results in early-stage studies, the lack of widespread regulatory approval and standardization in clinical settings slows down market expansion. The industry must invest in robust clinical trials, regulatory alignment, and real-world evidence to demonstrate the technology’s efficacy and cost-effectiveness in large-scale applications

Photoacoustic Imaging Market Scope

The market is segmented on the basis of type, product, application, and end-user.

• By Type

On the basis of type, the photoacoustic imaging market is segmented into Photoacoustic imaging system and photoacoustic computed tomography system. The photoacoustic imaging system segment dominated the market with the largest revenue share of 58.6% in 2024, driven by its widespread use in preclinical research for studying tumor vasculature, oxygenation, and molecular imaging. The technology’s ability to deliver high-contrast and high-resolution images without ionizing radiation makes it ideal for real-time in vivo imaging.

The photoacoustic computed tomography system segment is projected to witness the fastest growth rate of 12.4% from 2025 to 2032, owing to its expanding role in deep-tissue imaging and increasing clinical trials focusing on oncology and cardiovascular disorders. Its advanced imaging depth and three-dimensional reconstruction capability are gaining traction in translational research and potential clinical diagnostics.

• By Product

On the basis of product, the market is segmented into imaging system, transducers, and software and accessories. The imaging system segment held the largest market share in 2024 due to its essential role in capturing and processing photoacoustic signals across both preclinical and clinical settings. The increasing demand for compact, portable, and high-throughput imaging systems is driving continued innovation and investment in this segment.

The software and accessories segment is expected to register the highest CAGR during the forecast period, supported by the growing importance of image processing, data interpretation, and AI-based analytics in enhancing diagnostic accuracy and workflow efficiency. Advancements in user interfaces and real-time visualization tools are further propelling growth in this category.

• By Application

On the basis of application, the market is segmented into preclinical and clinical. The preclinical segment captured the highest market revenue share in 2024, largely due to its extensive use in academic and pharmaceutical R&D for evaluating drug efficacy, tumor biology, and vascular research. Researchers value photoacoustic imaging for its non-invasive, multi-modal capabilities, particularly in small animal models.

The Clinical segment is projected to grow at the fastest CAGR from 2025 to 2032, driven by increasing interest in applying photoacoustic imaging for human diagnostics, particularly in areas such as breast cancer detection, dermatology, and vascular disorders. As more clinical trials validate its effectiveness, clinical use is expected to expand significantly.

• By End User

On the basis of end-user, the photoacoustic imaging market is segmented into ambulatory surgical centers, research laboratories, hospitals and clinics, diagnostic imaging centers, pharmaceutical and biotechnology companies, and others. The research laboratories segment dominated the market in 2024, owing to high demand for preclinical imaging tools, strong academic funding, and expanding research in functional and molecular imaging. Institutions globally are increasingly adopting PAI systems to advance biomedical discovery and drug development.

The hospitals and clinics segment is forecasted to witness the highest CAGR from 2025 to 2032, supported by the increasing adoption of innovative imaging modalities in clinical settings. The growing emphasis on early disease detection, non-invasive diagnostics, and real-time visualization is accelerating the integration of PAI technologies into routine hospital workflows.

Photoacoustic Imaging Market Regional Analysis

- North America dominates the photoacoustic imaging market with the largest revenue share of 39.42% in 2024, driven by strong investments in biomedical research, the presence of leading academic and clinical institutions, and early adoption of innovative imaging technologies

- The region’s focus on precision medicine, cancer diagnostics, and translational research significantly contributes to the widespread use of photoacoustic imaging (PAI) across preclinical and clinical applications

- In addition, the presence of major market players, well-established healthcare infrastructure, and favorable government funding for imaging technologies further boost market penetration. The U.S., in particular, leads the region with a robust pipeline of oncology-related imaging trials and growing clinical integration of hybrid imaging systems

U.S. Photoacoustic Imaging Market Insight

The U.S. photoacoustic imaging market accounted for the largest global revenue share of 41.2% in 2024, driven by a well-established clinical infrastructure, a strong presence of research institutions, and early adoption of non-invasive diagnostic solutions. Robust funding for imaging technology development and the widespread deployment of preclinical photoacoustic imaging systems are significantly boosting innovation and commercialization across both academic and healthcare settings. The country's focus on precision medicine and advanced diagnostics further reinforces its dominant position in the global market.

Europe Photoacoustic Imaging Market Insight

The Europe photoacoustic imaging market contributed to 27.6% of global revenue in 2024 and is projected to grow steadily, supported by a mature research environment and strong public–private collaborations. Countries such as Germany, the U.K., and France are leading regional adoption, driven by increasing interest in hybrid imaging for oncology, neurology, and dermatology. Government research grants and clinical trials involving PAI technologies are further propelling market expansion throughout the region.

U.K. Photoacoustic Imaging Market Insight

The U.K. photoacoustic imaging market held a notable 6.8% share of the global market in 2024, propelled by its strong academic and medical research landscape. Government-funded initiatives in clinical diagnostics and a rising focus on early cancer detection—particularly in breast cancer screening—are major growth drivers. The country’s growing emphasis on precision medicine and translational research continues to support advancements in photoacoustic technology adoption.

Germany Photoacoustic Imaging Market Insight

The Germany photoacoustic imaging market accounted for 7.4% of the global photoacoustic imaging market in 2024, owing to its leadership in biomedical imaging innovation and research. The country’s extensive investment in photonics, medical technology, and translational research facilitates the steady integration of PAI across hospitals and research centers. Germany's focus on quality and regulatory compliance is also fostering commercial adoption of advanced imaging platforms.

Asia-Pacific Photoacoustic Imaging Market Insight

The Asia-Pacific photoacoustic imaging market is poised to register the fastest CAGR of 14.8% during the forecast period, with the region capturing 21.3% of global revenue in 2024. This rapid growth is fueled by increasing healthcare expenditure, government-led digital health programs, and expanding imaging infrastructure in countries such as China, Japan, and India. A rising number of public–private partnerships, combined with domestic production of medical devices, is enhancing access to affordable, high-quality PAI systems across the region.

Japan Photoacoustic Imaging Market Insight

The Japan photoacoustic imaging market contributed around 5.2% to the global revenue share in 2024, driven by the nation’s long-standing focus on healthcare innovation, an aging population, and the growing demand for non-invasive diagnostic technologies. The country is witnessing rising integration of photoacoustic imaging in areas such as oncology, microvascular analysis, and ophthalmology. Strong support for clinical R&D and advanced hospital infrastructure further support market development.

China Photoacoustic Imaging Market Insight

The China photoacoustic imaging market held the largest share within Asia-Pacific in 2024, representing about 11.7% of global revenue. China’s rapid market growth is supported by a thriving biotech sector, favorable government policies for healthcare innovation, and rising investments in diagnostic infrastructure. Major hospitals across urban regions are actively adopting PAI systems for clinical use, while domestic manufacturers continue to drive affordability and innovation in the field.

Photoacoustic Imaging Market Share

The photoacoustic imaging industry is primarily led by well-established companies, including:

- PreXion Inc. (U.S.)

- iThera Medical GmbH (Germany)

- PST Inc. (South Korea)

- HÜBNER Photonics (Germany)

- Litron Lasers (U.K.)

- FUJIFILM Visualsonics, Inc. (Canada)

- Kibero (Switzerland)

- InnoLas Laser GmbH (Germany)

- QUANTEL LASER (France)

- GE HealthCare (U.S.)

- Ekspla (Lithuania)

- TomoWave Laboratories, Inc. (U.S.)

- Aspectus GmbH (Germany)

- Daylight Solutions (U.S.)

- ADVANTEST CORPORATION (Japan)

- illumiSonics Inc. (U.S.)

- OPOTEK LLC (U.S.)

- Seno Medical (U.S.)

- Vibronix, Inc. (U.S.)

Latest Developments in Global Photoacoustic Imaging Market

- In April 2025, researchers introduced Acoustic Loudness Factor (ALF)—a new benchmark parameter designed for small-molecule photoacoustic probes. ALF enables accurate prediction of dye performance in vivo, accelerating probe design and improving signal quality in diagnostic imaging

- In February March 2025, scientists at Wayne State University used PAI combined with pattern recognition to reveal distinct neural activation patterns in the prefrontal cortex during conditioned learning in rats—highlighting PAI’s emerging role in neuroscience research

- In April 2025, Duke University researchers published findings on using Acoustic Loudness Factor for benchmarking and enhancing small-molecule photoacoustic probes, setting a new standard for design and preclinical evaluation

- In May 2025, a joint A*STAR–NHG group in Singapore unveiled a first-in-human trial combining MSOT and AI-based segmentation for 3D tumor imaging—including basal cell carcinoma diagnostics—demonstrating high-resolution efficacy and potential to guide surgical planning

- In March 2025, Nature Reviews Bioengineering featured a commentary titled “Defining the clinical niche for photoacoustic imaging,” highlighting its growing therapeutic relevance in oncology and cardiovascular diagnostics—underscoring accelerated clinical adoption

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.