Global Plant Protein Ingredient Market

Market Size in USD Billion

USD

15.98 Billion

USD

27.03 Billion

2024

2032

USD

15.98 Billion

USD

27.03 Billion

2024

2032

| 2025 - 2032 | |

| USD 15.98 Billion | |

| USD 27.03 Billion | |

| % | |

|

What is the Global Plant Protein Ingredient Market Size and Growth Rate?

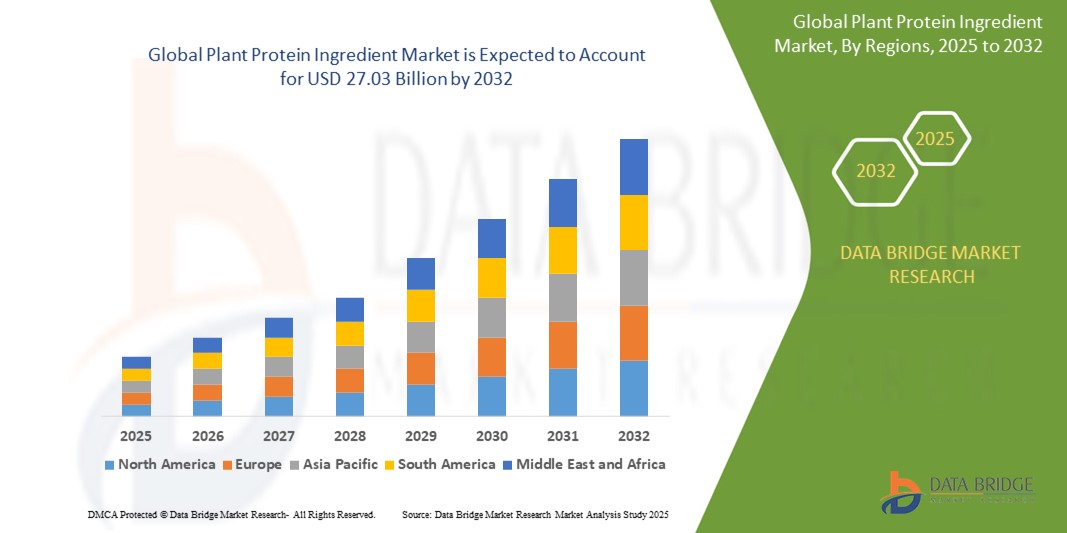

- The global plant protein ingredient market size was valued at USD 15.98 billion in 2024 and is expected to reach USD 27.03 billion by 2032, at a CAGR of 6.79% during the forecast period

- The plant protein ingredient market has experienced substantial growth driven by increasing consumer demand for sustainable and plant-based food options. This growth is supported by rising awareness of health and environmental benefits associated with plant-based diets, including lower greenhouse gas emissions and reduced land and water use compared to animal agriculture

- Key plant protein sources such as soy, pea, and wheat have seen significant adoption in food and beverage applications due to their nutritional profiles and functional properties, such as emulsification and texturization

- The market expansion is further fueled by advancements in extraction technologies that improve the yield and quality of plant proteins, making them more cost-effective and versatile for manufacturers

What are the Major Takeaways of Plant Protein Ingredient Market?

- Growing awareness among consumers about the health benefits associated with plant-based diets, such as reduced cholesterol levels and lowered risks of chronic diseases such as heart disease and diabetes, is a significant driver for the plant protein ingredient market

- As more individuals seek healthier dietary choices, there is a corresponding increase in the demand for plant protein ingredients across various food and beverage categories. This trend is supported by a growing body of scientific research highlighting the nutritional advantages of plant proteins over animal-based alternatives, further solidifying consumer confidence in choosing plant-based options

- North America dominated the plant protein ingredient market, accounting for the largest revenue share of 39.25% in 2024, driven by growing consumer awareness around sustainable nutrition, increasing demand for meat alternatives, and widespread adoption of plant-based diets

- Asia-Pacific region is expected to witness the fastest CAGR of 5.9% from 2025 to 2032, attributed to a rapid shift toward plant-based nutrition, increasing disposable incomes, and dietary transitions in major economies such as China, Japan, and India

- The Conventional segment dominated the plant protein ingredient market with the largest revenue share of 68.4% in 2024, owing to its wider availability, cost-effectiveness, and large-scale production

Report Scope and Plant Protein Ingredient Market Segmentation

|

Attributes |

Plant Protein Ingredient Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Plant Protein Ingredient Market?

- A key trend shaping the global plant protein ingredient market is the rising consumer demand for clean-label, allergen-free, and functional protein ingredients. This shift is influenced by growing awareness about health, sustainability, and ethical food sourcing

- For instance, pea protein and fava bean protein are witnessing high demand due to their allergen-friendly profile and excellent amino acid composition. Products such as Nestlé’s Garden Gourmet and Beyond Meat’s plant-based lines are leveraging such proteins for clean and sustainable product offerings

- The clean-label trend is also fueling ingredient innovation, including the development of fermented plant proteins and blended protein systems that enhance digestibility and taste. MycoTechnology’s fermented pea protein is an instance that improves functionality while maintaining a natural label

- This consumer preference for transparency is encouraging food companies to eliminate artificial additives and highlight natural sourcing, making plant proteins more appealing to the health-conscious and environmentally aware demographic

- Moreover, the growth of flexitarianism and vegan lifestyles, especially among younger populations, is pushing brands to integrate clean and functional proteins into a wide range of food categories — from beverages to snacks and dairy alternatives

- As brands increasingly compete on nutrition, sustainability, and label simplicity, this trend is expected to significantly shape innovation and marketing strategies in the plant protein ingredient market moving forward

What are the Key Drivers of Plant Protein Ingredient Market?

- The rising consumer shift towards sustainable and ethical diets, combined with increasing cases of lactose intolerance and food allergies, is fueling the demand for plant-based protein ingredients

- For instance, in March 2024, Roquette Frères announced the expansion of its pea protein production facility in Canada to meet soaring demand for clean, plant-based nutrition in North America. Such capacity expansion by key players indicates the growth momentum of this market

- The food & beverage industry is experiencing strong growth in meat analogues, dairy alternatives, and high-protein snacks, creating lucrative opportunities for soy, pea, rice, and fava bean protein ingredients

- Government initiatives promoting plant-based food production and climate-conscious agriculture, such as the EU's Farm to Fork Strategy, are also encouraging manufacturers to replace animal-based protein sources with plant alternatives

- In addition, the increasing popularity of sports and performance nutrition has created a growing market for functional plant proteins that offer muscle recovery, weight management, and energy support, making them appealing across a broad consumer base

Which Factor is challenging the Growth of the Plant Protein Ingredient Market?

- One of the primary challenges in the plant protein ingredient market is the functional and sensory limitations of plant proteins, especially in terms of taste, texture, and solubility, which impact consumer acceptance and product formulation

- For instance, soy and pea proteins may produce off-flavors or gritty textures when used in beverages or dairy alternatives, making it difficult for manufacturers to deliver products comparable to animal-based counterparts

- Addressing these issues requires advanced processing technologies, such as fermentation, enzymatic treatment, or precision extraction, which can be cost-intensive and may not be accessible to all manufacturers

- Another major hurdle is the fluctuating price and limited supply of high-quality non-GMO and organic plant protein ingredients. Global demand surges have at times caused pricing volatility for ingredients such as pea and chickpea protein

- Moreover, concerns over allergenicity (such as soy) and regional dietary restrictions can limit market penetration in certain geographies

- To overcome these barriers, industry players are investing in protein blending strategies, sustainable sourcing, and consumer education to promote acceptance of alternative proteins. Continued R&D and cost innovation will be essential for unlocking the full market potential

How is the Plant Protein Ingredient Market Segmented?

The market is segmented on the basis of source, type, application, form, functionality, and end use.

• By Source

On the basis of source, the plant protein ingredient market is segmented into organic and conventional. The conventional segment dominated the plant protein ingredient market with the largest revenue share of 68.4% in 2024, owing to its wider availability, cost-effectiveness, and large-scale production. Conventional sources continue to lead due to their strong supply chains and the ability to cater to bulk food manufacturing needs across major economies.

The organic segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing consumer demand for clean-label, non-GMO, and pesticide-free products. Rising health consciousness and sustainability concerns are encouraging manufacturers to shift towards organic alternatives.

• By Type

On the basis of type, the market is segmented into pea, soybean, wheat, bean, peanut, legume, chickpea, lentil, rice, and potato. Soybean protein dominated the Plant Protein Ingredient market with the largest market revenue share of 34.6% in 2024, owing to its high protein content, established use in meat alternatives, and broad functional properties. Its strong nutritional profile and cost-effectiveness make it a staple in plant-based formulations globally.

The Pea protein segment is anticipated to register the fastest growth rate during the forecast period, driven by its allergen-free status, growing popularity in sports nutrition, and expanding use in dairy and meat alternatives.

• By Application

On the basis of application, the market is segmented into food and beverages, pharmaceuticals and nutraceuticals, animal feed, personal care, sports nutrition, clinical nutrition, infant nutrition, and others. The food and beverages segment held the largest market revenue share of 41.3% in 2024, propelled by the surging demand for meat and dairy alternatives, snacks, and high-protein functional foods. The shift in consumer preferences towards plant-based eating and flexitarian diets continues to drive this segment.

The sports nutrition segment is expected to grow at the highest CAGR from 2025 to 2032, as athletes and fitness-focused consumers increasingly opt for plant-based protein powders, shakes, and bars for muscle recovery and performance enhancement.

• By Form

On the basis of form, the plant protein ingredient market is segmented into Dry and Liquid. The Dry segment dominated the market with the largest revenue share of 74.9% in 2024, primarily due to its long shelf life, ease of storage, and suitability for a wide range of food and beverage formulations.

The Liquid segment is anticipated to grow at a faster rate, especially in ready-to-drink protein beverages and specialized nutrition applications, where solubility and convenience are key differentiators.

• By Functionality

On the basis of functionality, the market is segmented into Emulsification and Stabilizing, Foaming, Nutrition, Adhesion, and Others. The Nutrition segment held the largest revenue share of 38.7% in 2024, driven by the increasing focus on protein enrichment in everyday foods, clean-label formulations, and health-conscious eating patterns.

The emulsification and stabilizing segment is projected to experience the fastest growth, as plant proteins are increasingly used in processed foods, dairy alternatives, and baked goods for their functional benefits beyond nutrition.

• By End Use

On the basis of end use, the market is segmented into retail consumers, food service and hospitality, industrial food manufacturer, sports nutrition and fitness industry, and pharmaceutical industry. The industrial food manufacturer segment dominated the market with the largest share of 45.1% in 2024, as large-scale producers continue to integrate plant proteins into mainstream food products to meet evolving consumer preferences and regulatory demands.

The retail consumers segment is expected to witness the fastest growth from 2025 to 2032, fueled by the growing availability of plant protein products in supermarkets, health stores, and e-commerce platforms, supported by aggressive brand marketing and product innovation.

Which Region Holds the Largest Share of the Plant Protein Ingredient Market?

- North America dominated the plant protein ingredient market, accounting for the largest revenue share of 39.25% in 2024, driven by growing consumer awareness around sustainable nutrition, increasing demand for meat alternatives, and widespread adoption of plant-based diets

- The region’s strong food processing industry and a rising number of health-conscious consumers have significantly contributed to the popularity of pea, soy, and rice protein ingredients in both food and beverage applications

- In addition, key companies in the U.S. and Canada are heavily investing in product development and clean-label formulations, positioning plant protein as a mainstream dietary component

U.S. Plant Protein Ingredient Market Insight

The U.S. captured the largest revenue share in North America in 2024, driven by the surging demand for vegan and flexitarian diets, the rise of fitness-focused lifestyles, and the prevalence of sports nutrition trends. Major players are introducing a variety of protein-rich products including bars, shakes, powders, and meat substitutes, further supported by well-established retail distribution and e-commerce channels. Consumer preference for non-GMO, allergen-free, and high-protein plant-based options is also driving continuous innovation and competitive pricing across the U.S. market.

Europe Plant Protein Ingredient Market Insight

The Europe plant protein ingredient market is projected to expand at a strong CAGR during the forecast period, driven by regulatory support for plant-based food, carbon footprint reduction goals, and rising vegan and vegetarian populations. Countries such as Germany, France, and the Netherlands are showing substantial uptake in plant protein-based meat and dairy alternatives, supported by sustainability campaigns and environmentally conscious consumer behavior. Growth is especially evident in private label and ready-to-eat segments across European supermarkets.

U.K. Plant Protein Ingredient Market Insight

The U.K. market is expected to witness a notable CAGR during 2025–2032 due to increasing consumer adoption of meat-free lifestyles, expanding vegan product lines, and a vibrant plant-based startup ecosystem. Government-backed initiatives promoting healthier eating habits and environmental sustainability are encouraging innovation across both retail and food service sectors. The rising popularity of alternative protein supplements, especially among young consumers and athletes, further fuels growth.

Germany Plant Protein Ingredient Market Insight

Germany continues to emerge as a key contributor to Europe's plant protein landscape, with a focus on organic farming, functional foods, and sustainable product development. The market is benefiting from increasing availability of plant-based dairy alternatives, meat substitutes, and high-protein bakery products. Local consumers are particularly inclined toward transparent labeling, minimal processing, and eco-friendly packaging, influencing major food brands to reformulate offerings using plant protein.

Which Region is the Fastest Growing in the Plant Protein Ingredient Market?

Asia-Pacific region is expected to witness the fastest CAGR of 5.9% from 2025 to 2032, attributed to a rapid shift toward plant-based nutrition, increasing disposable incomes, and dietary transitions in major economies such as China, Japan, and India. Government initiatives promoting food security and sustainability, alongside rising lactose intolerance and health awareness, are catalyzing growth in both retail and industrial segments.

Japan Plant Protein Ingredient Market Insight

In Japan, increasing health consciousness, an aging population, and a preference for high-quality, low-fat protein are driving demand for plant protein in functional foods, beverages, and elderly nutrition. The market benefits from advanced food processing capabilities and rising demand for clean-label, low-allergen ingredients. Protein-rich soy-based beverages, supplements, and ready-to-eat snacks are gaining strong consumer traction.

China Plant Protein Ingredient Market Insight

China accounted for the largest revenue share in Asia Pacific in 2024, supported by the country’s rapidly expanding middle class, high awareness of health and wellness, and government backing for plant-based food production. With one of the largest vegan populations and high demand for meat alternatives, China continues to see large-scale investments from both domestic and global players. The availability of affordable plant protein products, integration into traditional foods, and popularity in infant and sports nutrition further fuel market growth.

Which are the Top Companies in Plant Protein Ingredient Market?

The plant protein ingredient industry is primarily led by well-established companies, including:

- ADM (U.S.)

- Kerry Group plc (Ireland)

- Cargill, Incorporated (U.S.)

- AMCO Proteins (U.S.)

- The Scoular Company (U.S.)

- A&B Ingredients, Inc. (U.S.)

- Jungbunzlauer Suisse AG (Switzerland)

- Glanbia PLC (Ireland)

- Roquette Frères (France)

- Reliance Private Label Supplements (U.S.)

- Ingredion (U.S.)

- Batory Foods (U.S.)

- Cambridge Commodities (U.K.)

- PLT Health Solutions (U.S.)

- Axiom Foods, Inc. (U.S.)

- Greenleaf Foods, SPC. (Canada)

- Medix Laboratoires (Canada)

- Prinova Group LLC. (U.S.)

- Sonic Biochem (India)

- Chaitanya Agro Biotech Pvt. Ltd. (India)

- Bioway Organic Group Limited (China)

What are the Recent Developments in Global Plant Protein Ingredient Market?

- In February 2024, Roquette made strides in the plant protein market by introducing four new pea proteins under its NUTRALYS brand. These ingredients are designed to improve the taste, texture, and versatility of plant-based foods and high-protein nutritional products. This expansion strengthens Roquette’s portfolio and empowers food manufacturers with more innovative formulation options in the growing plant-based sector

- In May 2023, Burcon NutraScience Corporation launched its Burcon 2.0 initiative, a strategic move aimed at offering pilot-scale plant protein processing services to food and beverage manufacturers. This effort underscores the company’s commitment to expanding industry access to high-quality plant protein solutions and accelerating innovation across the plant-based value chain

- In January 2023, Roquette announced an investment in Japanese startup Daiz, aimed at exploring novel seed germination techniques for cultivating next-generation plant proteins. This partnership supports Roquette’s strategy of developing advanced meat alternatives by leveraging selective cultivation methods for better functionality and sustainability

- In November 2022, Royal DSM introduced Vertis CanolaPRO, a premium canola protein isolate developed after more than ten years of R&D. Extracted from nutrient-rich canola seeds, the product delivers a complete amino acid profile, offering a nutritious, scalable solution for plant-based food innovation

- In April 2022, Cargill extended the reach of its RadiPure pea protein into Middle East, Turkey, Africa (META), and India, aiming to support the region’s food and beverage producers in addressing evolving plant-based consumer preferences. This move enhances Cargill’s presence in emerging markets and aligns with the global surge in sustainable nutrition demand

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Plant Protein Ingredient Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Plant Protein Ingredient Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Plant Protein Ingredient Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.