Global Plastic Surgery Instruments Market

Market Size in USD Million

USD

864.26 Million

USD

1,653.79 Million

2024

2032

USD

864.26 Million

USD

1,653.79 Million

2024

2032

| 2025 - 2032 | |

| USD 864.26 Million | |

| USD 1,653.79 Million | |

| % | |

|

Plastic Surgery Instruments Market Size

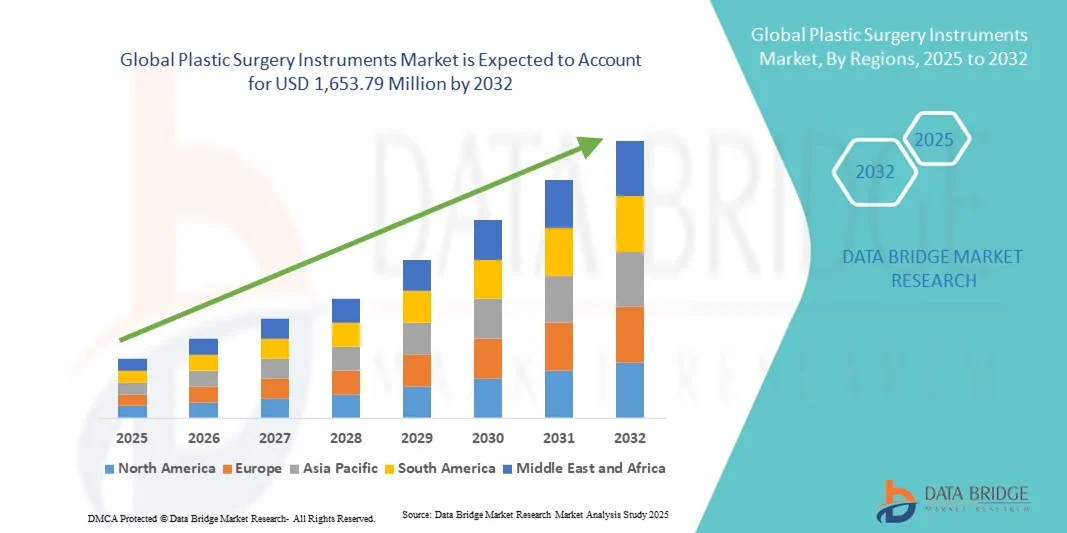

- The global plastic surgery instruments market size was valued at USD 864.26 million in 2024 and is expected to reach USD 1,653.79 million by 2032, at a CAGR of 8.45% during the forecast period

- The market growth is largely driven by the rising number of cosmetic procedures, increasing awareness about aesthetic enhancements, and continuous technological advancements in surgical instruments, which are improving precision, safety, and outcomes

- Furthermore, growing consumer preference for minimally invasive procedures, expanding healthcare infrastructure, and rising disposable incomes are fueling demand for advanced plastic surgery instruments across hospitals, clinics, and specialized cosmetic centers, thereby propelling the market's growth

Plastic Surgery Instruments Market Analysis

- Plastic surgery instruments, including handheld instruments, electrosurgical instruments, and other specialized tools, are crucial for performing precise cosmetic and reconstructive procedures in hospitals and clinics due to their advanced design, safety features, and ergonomic functionality

- The rising demand for plastic surgery instruments is primarily driven by the growing number of cosmetic and reconstructive procedures, increasing awareness of aesthetic enhancements, and continuous innovations that improve surgical outcomes and operational efficiency

- North America dominated the plastic surgery instruments market with the largest revenue share of 38.4% in 2024, supported by a strong healthcare infrastructure, high adoption of cosmetic procedures, and the presence of key market players driving product innovations

- Asia-Pacific is expected to be the fastest-growing region in the plastic surgery instruments market during the forecast period due to increasing medical tourism, urbanization, rising disposable incomes, and growing awareness of cosmetic and reconstructive procedures

- Handheld instruments segment dominated the plastic surgery instruments market with a market share of 42.6% in 2024, driven by their extensive use across both cosmetic and reconstructive surgeries, ease of handling, and reliability in delivering precise surgical outcomes

Report Scope and Plastic Surgery Instruments Market Segmentation

|

Attributes |

Plastic Surgery Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Plastic Surgery Instruments Market Trends

Advancements in Minimally Invasive Surgical Tools

- A notable and growing trend in the global plastic surgery instruments market is the development of minimally invasive instruments, which enhance surgical precision while reducing patient recovery time and procedure-related risks

- For instance, handheld laparoscopic scissors and electrosurgical tools are increasingly designed with ergonomic grips and finer tips to facilitate delicate cosmetic and reconstructive procedures

- These innovations allow surgeons to perform complex surgeries with smaller incisions, reducing scarring and improving aesthetic outcomes, which is highly valued by patients seeking quicker recovery

- Integration of advanced materials such as high-grade stainless steel, titanium, and coated instruments improves durability, sterilization efficiency, and operational safety in both cosmetic and reconstructive surgeries

- This trend towards safer, more precise, and patient-friendly instruments is driving expectations for innovation among manufacturers, prompting companies such as Integra LifeSciences and Medtronic to introduce next-generation handheld and electrosurgical instruments

- The demand for plastic surgery instruments that combine precision, safety, and ergonomics is rapidly increasing across hospitals, clinics, and specialized aesthetic centers, as both surgeons and patients prioritize improved surgical outcomes

Plastic Surgery Instruments Market Dynamics

Driver

Increasing Demand from Rising Cosmetic and Reconstructive Procedures

- The growing number of cosmetic and reconstructive procedures worldwide, fueled by rising awareness of aesthetic enhancements and improved access to healthcare, is a key driver of demand for plastic surgery instruments

- For instance, according to industry reports, the surge in minimally invasive procedures such as liposuction, rhinoplasty, and breast augmentation is creating higher demand for advanced handheld and electrosurgical instruments

- Patients are increasingly seeking precise and safe surgical interventions, prompting healthcare providers to invest in high-quality instruments that optimize outcomes and reduce complications

- Expanding healthcare infrastructure and rising disposable incomes in emerging economies are also supporting the adoption of sophisticated surgical instruments in both hospitals and cosmetic centers

- The growing focus on medical tourism, particularly in Asia-Pacific and the Middle East, is further driving the demand for instruments that meet international surgical standards

- As a result, manufacturers are increasingly focusing on innovative designs and high-performance instruments to cater to the rising procedural volumes and evolving patient expectations

Restraint/Challenge

High Costs and Regulatory Compliance Barriers

- The high cost of advanced plastic surgery instruments and the complexity of obtaining regulatory approvals present significant challenges to market expansion, particularly for smaller healthcare providers

- For instance, new electrosurgical tools and precision handheld instruments often require compliance with FDA, CE, or other regional medical device regulations, which can delay product launches

- Small and medium clinics in developing regions may find the initial investment in high-quality instruments prohibitive, limiting the adoption of advanced surgical technologies

- In addition, stringent sterilization, quality control, and safety standards increase manufacturing costs, which are often passed on to healthcare providers and patients

- While costs are gradually decreasing due to technological improvements and local manufacturing, the perceived premium for high-precision instruments can still restrict widespread adoption

- Overcoming these challenges through cost-optimized designs, simplified regulatory pathways, and effective training programs for surgeons is essential for sustained market growth

Plastic Surgery Instruments Market Scope

The market is segmented on the basis of type, procedure, and end user

- By Type

On the basis of type, the plastic surgery instruments market is segmented into handheld instruments, electrosurgical instruments, and other plastic surgery instruments. The handheld instruments segment dominated the market with the largest revenue share of 42.6% in 2024, driven by their critical role in performing precise cosmetic and reconstructive procedures. Surgeons often prefer handheld instruments for their ergonomics, accuracy, and versatility across multiple surgical applications. The segment benefits from widespread adoption in hospitals and specialty clinics due to their reliability and ease of sterilization. Continuous innovations in design and material quality further enhance their efficiency and safety. High procedural volumes in cosmetic and reconstructive surgeries also sustain the demand for handheld instruments, establishing them as the backbone of plastic surgery operations.

The electrosurgical instruments segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing adoption of minimally invasive procedures and advanced energy-based surgical technologies. Electrosurgical instruments allow precise tissue cutting and coagulation, reducing surgical time and improving patient recovery. Growing awareness of aesthetic procedures and rising healthcare infrastructure investments, particularly in Asia-Pacific and the Middle East, are driving demand. Integration with modern surgical techniques and compatibility with advanced operating rooms further contribute to the segment’s growth. The segment’s growth is also supported by innovations in instrument safety features, reducing risks such as burns or unintended tissue damage. Electrosurgical instruments are increasingly preferred for cosmetic surgeries such as liposuction and rhinoplasty, as well as reconstructive procedures requiring delicate tissue manipulation.

- By Procedure

On the basis of procedure, the plastic surgery instruments market is segmented into cosmetic surgery and reconstructive surgery. The cosmetic surgery segment dominated the market with the largest revenue share of 55.3% in 2024, driven by the rising number of aesthetic procedures globally and growing consumer focus on personal appearance. Surgeons rely heavily on specialized instruments for procedures such as breast augmentation, facelifts, and liposuction to achieve precise outcomes. Technological advancements in surgical tools, coupled with minimally invasive techniques, enhance patient satisfaction and reduce recovery times. High disposable incomes, growing medical tourism, and increasing awareness of cosmetic enhancements are also fueling the segment’s growth. Hospitals and clinics continue to invest in advanced instruments to meet rising procedural volumes and evolving patient expectations. The segment’s dominance reflects the ongoing trend of prioritizing safety, precision, and efficiency in cosmetic procedures.

The reconstructive surgery segment is expected to witness the fastest CAGR from 2025 to 2032, driven by the rising prevalence of trauma cases, congenital deformities, and cancer-related surgeries requiring tissue repair and reconstruction. Reconstructive procedures demand highly precise and versatile instruments to restore functionality and aesthetics. Surgeons increasingly prefer advanced handheld and electrosurgical instruments for complex tissue manipulation and grafting procedures. Growing investments in hospital infrastructure and reconstructive surgery centers, particularly in emerging markets, are boosting adoption. The segment benefits from innovations that enhance surgical accuracy, reduce operative time, and improve patient outcomes. Rising awareness about reconstructive treatment options and medical tourism also contribute to the segment’s rapid growth.

- By End User

On the basis of end user, the plastic surgery instruments market is segmented into hospitals and other end users. The hospitals segment dominated the market with the largest revenue share of 62.4% in 2024, due to high procedural volumes and the availability of skilled surgeons equipped to use advanced surgical instruments. Hospitals continue to invest in state-of-the-art tools to improve surgical precision, patient outcomes, and operational efficiency. They also benefit from standardized sterilization protocols and dedicated surgical teams that ensure optimal use of instruments. Government initiatives, healthcare infrastructure development, and medical tourism further strengthen the dominance of hospitals in this segment. Hospitals are increasingly adopting advanced handheld and electrosurgical instruments to cater to both cosmetic and reconstructive surgeries.

The other end users segment, including specialty clinics, ambulatory surgical centers, and cosmetic centers, is expected to witness the fastest growth from 2025 to 2032, driven by the rising number of outpatient and minimally invasive procedures. These centers prefer compact, versatile, and cost-effective instruments that offer efficiency without compromising precision. Growing consumer preference for accessible cosmetic procedures outside traditional hospital settings fuels demand. The segment also benefits from innovations that simplify instrument handling and reduce recovery times. Increasing investments in specialty clinics in emerging economies, coupled with rising awareness of aesthetic procedures, further accelerate growth. The expanding presence of these centers allows patients easier access to advanced surgical interventions, boosting the adoption of high-quality instruments.

Plastic Surgery Instruments Market Regional Analysis

- North America dominated the plastic surgery instruments market with the largest revenue share of 38.4% in 2024, supported by a strong healthcare infrastructure, high adoption of cosmetic procedures, and the presence of key market players driving product innovations

- Surgeons and healthcare providers in the region prioritize precision, safety, and efficiency, leading to widespread adoption of advanced handheld and electrosurgical instruments across hospitals and specialty clinics

- This dominance is further supported by strong medical research and development, presence of key market players, and high disposable incomes, which enable investments in state-of-the-art surgical tools and minimally invasive technologies.

U.S. Plastic Surgery Instruments Market Insight

The U.S. plastic surgery instruments market captured the largest revenue share of 80% in 2024 within North America, fueled by a high prevalence of cosmetic and reconstructive procedures and advanced healthcare infrastructure. Surgeons and clinics prioritize precision, safety, and efficiency, driving the adoption of advanced handheld and electrosurgical instruments. The growing demand for minimally invasive procedures, coupled with rising disposable incomes and medical tourism, further propels the market. Moreover, continuous innovation by key manufacturers and integration of next-generation surgical tools into hospitals and specialty centers is significantly contributing to market expansion.

Europe Plastic Surgery Instruments Market Insight

The Europe plastic surgery instruments market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of aesthetic procedures and the rising prevalence of reconstructive surgeries. Growth in urbanization, higher disposable incomes, and a focus on healthcare quality are fostering the adoption of advanced instruments. European healthcare providers are investing in precision tools to improve patient outcomes and reduce procedural complications. The market is experiencing significant growth across hospitals, cosmetic clinics, and outpatient centers, with instruments being incorporated into both elective cosmetic procedures and medically necessary reconstructive surgeries.

U.K. Plastic Surgery Instruments Market Insight

The U.K. plastic surgery instruments market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing popularity of cosmetic and reconstructive procedures and rising consumer awareness of aesthetic enhancements. Concerns regarding procedural safety and surgical precision are encouraging healthcare facilities to invest in high-quality instruments. The U.K.’s robust healthcare infrastructure, combined with strong research and development activities and well-established cosmetic clinics, is expected to continue stimulating market growth. In addition, the preference for minimally invasive and outpatient surgeries supports the rising adoption of advanced handheld and electrosurgical instruments.

Germany Plastic Surgery Instruments Market Insight

The Germany plastic surgery instruments market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of reconstructive and cosmetic procedures, technological advancements, and strong healthcare infrastructure. Germany’s emphasis on innovation, safety, and precision in surgical practices promotes the adoption of advanced instruments in hospitals and specialty clinics. Integration of modern tools that enhance efficiency, reduce procedural time, and improve patient outcomes is becoming increasingly prevalent. The market is also supported by a high focus on training surgeons in the use of advanced instruments and the growing popularity of minimally invasive procedures.

Asia-Pacific Plastic Surgery Instruments Market Insight

The Asia-Pacific plastic surgery instruments market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing medical tourism, rising disposable incomes, and growing awareness of cosmetic and reconstructive procedures in countries such as China, Japan, and India. The region’s expanding healthcare infrastructure and the presence of cost-effective surgical instruments are accelerating adoption across hospitals and specialty clinics. Furthermore, government initiatives promoting medical tourism and aesthetic healthcare are boosting demand. APAC is also emerging as a manufacturing hub for surgical instruments, improving affordability and accessibility for a wider consumer base.

Japan Plastic Surgery Instruments Market Insight

The Japan plastic surgery instruments market is gaining momentum due to the country’s high awareness of cosmetic procedures, advanced healthcare infrastructure, and growing demand for minimally invasive surgeries. The Japanese market emphasizes precision, safety, and innovative instrument designs, fueling the adoption of advanced handheld and electrosurgical tools. Integration of instruments into hospitals and outpatient clinics for both cosmetic and reconstructive surgeries is driving growth. Moreover, Japan’s aging population is such asly to spur demand for instruments used in reconstructive procedures to restore function and aesthetics, further boosting market expansion.

India Plastic Surgery Instruments Market Insight

The India plastic surgery instruments market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s rapidly expanding healthcare sector, increasing number of cosmetic procedures, and growing medical tourism. India has emerged as a key market for affordable yet high-quality surgical instruments used in hospitals, cosmetic clinics, and outpatient centers. The government’s initiatives supporting medical infrastructure and smart healthcare facilities, alongside strong domestic manufacturing capabilities, are key factors propelling market growth. Rising consumer awareness and disposable incomes also contribute to the increasing adoption of advanced plastic surgery instruments in both cosmetic and reconstructive procedures.

Plastic Surgery Instruments Market Share

The Plastic Surgery Instruments industry is primarily led by well-established companies, including:

- Zimmer Biomet. (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Stryker (U.S.)

- Integra LifeSciences Corporation (U.S.)

- KLS Martin SE & Co. KG (Germany)

- Sklar Surgical Instruments (U.S.)

- B. Braun SE (Germany)

- Misonix, Inc. (U.S.)

- Surgical Specialties Corporation (U.S.)

- Medline Industries, Inc. (U.S.)

- CONMED Corporation (U.S.)

- Olympus Corporation (Japan)

- Smith + Nephew (U.K.)

- Karl Storz GmbH & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Surgical Innovations Group plc (U.K.)

- MicroAire Surgical Instruments, LLC (U.S.)

- Surgical Instruments Company (U.S.)

What are the Recent Developments in Global Plastic Surgery Instruments Market?

- In October 2025, At the Plastic Surgery The Meeting held in New Orleans, MicroAire showcased its expanding portfolio of innovative surgical instruments. The company highlighted the ADIMATE system, which received CE Mark approval, indicating its compliance with European Union safety and performance standards. This system is designed to enhance the precision and efficiency of various plastic surgery procedures

- In November 2024, the University of South Florida (USF) and Tampa General Hospital (TGH) partnered with a robotics company to introduce life-saving surgical technology to the Tampa Bay area. This collaboration aims to enhance surgical precision and patient outcomes by integrating advanced robotic systems into clinical practices. The initiative highlights the growing trend of adopting cutting-edge technologies in the medical field to improve healthcare delivery

- In October 2024, MMI (Medical Microinstruments, Inc.) introduced the Symani Surgical System, a robotic-assisted microsurgical platform. This system was recognized in TIME's Best Inventions of 2024 for its precision and transformative impact on surgical procedures. It enhances the capabilities of surgeons in delicate operations, offering improved outcomes and efficiency

- In October 2024, St. Vincent’s Hospital in Melbourne became the first health system in Australia to adopt robotic-assisted microsurgery using the Symani Surgical System. This advancement marks a significant step in integrating robotic technology into plastic and reconstructive surgeries, aiming to improve surgical precision and patient outcomes

- In July 2024, Dr. Devgan Scientific Beauty launched a line of ergonomic surgical instruments designed to address gender inequities in surgery. These tools, created by renowned plastic surgeon Dr. Lara Devgan, are tailored for surgeons with smaller hands, aiming to enhance precision and ease of use during procedures

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.