Global Point Of Care Infectious Disease Diagnostics Market

Market Size in USD Billion

USD

2.51 Billion

USD

7.33 Billion

2024

2032

USD

2.51 Billion

USD

7.33 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.51 Billion | |

| USD 7.33 Billion | |

| % | |

|

Point of Care Infectious Disease Diagnostics Market Size

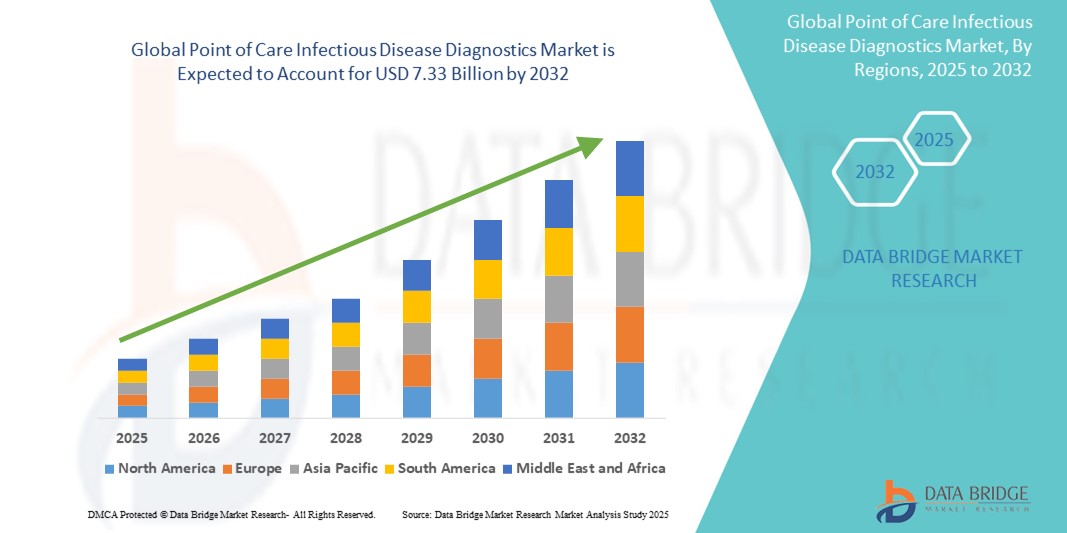

- The global point of care infectious disease diagnostics market size was valued at USD 2.51 billion in 2024 and is expected to reach USD 7.33 billion by 2032, at a CAGR of 14.32% during the forecast period

- The market growth is largely fueled by the growing adoption and technological advancements in rapid diagnostic tools, enabling faster and more accurate detection of infectious diseases at or near the site of patient care

- Furthermore, rising consumer demand for timely, cost-effective, and accessible diagnostic solutions is positioning point of care (PoC) devices as the preferred choice for both developed and developing healthcare systems

Point of Care Infectious Disease Diagnostics Market Analysis

- Point of care infectious disease diagnostics are becoming increasingly vital in healthcare systems across both developed and developing regions, due to their ability to deliver rapid results at or near the site of patient care. These diagnostics play a crucial role in early detection, timely treatment, and effective containment of infectious diseases such as influenza, HIV, COVID-19, malaria, and tuberculosis

- The escalating demand for point of care infectious disease diagnostics is primarily fueled by the growing prevalence of infectious diseases, rising demand for decentralized testing, and increasing adoption of rapid diagnostic technologies in emergency settings, clinics, and remote locations

- North America dominated the point of care infectious disease diagnostics market with the largest revenue share of 38.6% in 2024, driven by advanced healthcare infrastructure, high awareness levels, and substantial investment in R&D. The U.S. leads the region, supported by early adoption of cutting-edge diagnostic platforms and a strong presence of key market players

- Asia-Pacific is expected to be the fastest-growing region in the point of care infectious disease diagnostics market during the forecast period, projected to expand at a CAGR of 12.4% from 2025 to 2032. Factors such as increasing urbanization, rising healthcare expenditure, and government initiatives for strengthening primary healthcare infrastructure contribute to this growth. Countries such as China, India, and Southeast Asian nations are witnessing significant demand for affordable, portable, and accurate diagnostic tools for infectious disease management

- The lateral flow assay segment dominated the point of care infectious disease diagnostics market with a market share of 43.2% in 2024, attributed to its ease of use, quick turnaround time, and widespread application in detecting infections such as COVID-19, HIV, and influenza. The segment continues to be the preferred choice in low-resource settings and during public health emergencies due to its cost-effectiveness and minimal need for complex laboratory equipmen

Report Scope and Point of Care Infectious Disease Diagnostics Market Segmentation

|

Attributes |

Point of Care Infectious Disease Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Point of Care Infectious Disease Diagnostics Market Trends

“Growing Role of Technological Innovation and User-Centric Diagnostics”

- A significant and accelerating trend in the global point of care infectious disease diagnostics market is the advancement of user-centric diagnostic platforms, supported by integration with real-time data systems and intelligent decision-support tools. This transformation is greatly enhancing convenience, diagnostic speed, and patient engagement in decentralized healthcare settings

- For instance, modern diagnostic devices are becoming increasingly compatible with cloud-based platforms and smartphone applications, enabling healthcare professionals to access test results instantly, track patient records, and make informed decisions remotely. Such capabilities are proving invaluable in managing outbreaks and ensuring rapid treatment initiation

- Smart diagnostic tools are also capable of adapting based on usage trends, delivering tailored alerts and automated guidance for clinicians. Some devices are equipped with learning algorithms that help improve test accuracy over time, reduce human error, and offer early warnings in case of abnormal pathogen activity

- The seamless integration of diagnostic tools with telehealth platforms and electronic medical records (EMRs) creates a centralized interface for managing test results, patient data, and treatment plans. This unified approach is especially critical for managing chronic infectious diseases and monitoring high-risk patients

- This evolution toward more intuitive, connected, and responsive diagnostic solutions is reshaping expectations for rapid testing—especially in non-hospital settings such as mobile clinics, home care, and rural healthcare centers

- The demand for portable, easy-to-use point of care diagnostics that enhance workflow efficiency and clinical accuracy continues to rise, particularly in regions facing infrastructure challenges. Companies are responding with compact devices that support multiple test types and data integration features designed to streamline diagnostics in both routine and emergency situations

Point of Care Infectious Disease Diagnostics Market Dynamics

Driver

“Growing Demand Due to Rising Infectious Disease Burden and Decentralized Testing”

- The increasing prevalence of infectious diseases such as HIV, influenza, tuberculosis, and COVID-19 is significantly driving the demand for rapid, accessible diagnostic solutions. Point of care (PoC) diagnostics enable early detection and treatment initiation, which is critical for disease containment and improved patient outcomes

- For instance, in April 2024, bioMérieux SA expanded its PoC diagnostic portfolio by introducing new multiplex testing panels that enable the simultaneous detection of multiple respiratory pathogens. These efforts are expected to boost the availability and efficiency of diagnostic testing at the primary care and community health levels

- The shift toward decentralized healthcare, supported by rising investments in rural and remote health infrastructure, further promotes the adoption of PoC diagnostics. These tests require minimal infrastructure, deliver quick results, and reduce dependence on centralized laboratory services

- The rising burden of antimicrobial resistance (AMR) has also fueled interest in rapid PoC diagnostics to guide evidence-based antibiotic use and reduce misuse

- In addition, the increased demand for home testing and telehealth integration is encouraging manufacturers to develop compact, user-friendly PoC solutions that deliver clinical-grade accuracy, driving market expansion across various geographies and care settings

Restraint/Challenge

“Regulatory Complexity and Variable Test Accuracy”

- Despite their advantages, point of care infectious disease diagnostics face significant regulatory and performance-related hurdles. Ensuring consistent test accuracy across different patient populations and settings remains a challenge, particularly for novel or multiplex platforms

- Variability in sensitivity and specificity may lead to false negatives or positives, impacting clinical decision-making. This makes regulatory bodies more cautious and results in prolonged approval cycles, especially in Europe and the U.S.

- Furthermore, PoC devices used in resource-limited or non-laboratory settings must withstand temperature, humidity, and handling variations, placing additional burden on manufacturers for robust product design

- The relatively high cost of advanced PoC platforms, especially molecular-based solutions, can also be a barrier in low- and middle-income countries. Many public healthcare systems still struggle with procurement and funding limitations

- To overcome these barriers, stakeholders must focus on developing affordable, portable, and quality-assured PoC diagnostics, while working closely with regulatory agencies to streamline approval processes and validate performance in real-world conditions

Point of Care Infectious Disease Diagnostics Market Scope

The market is segmented on the basis of product, technology, application, and end user.

- By Product

On the basis of product, the point of care infectious disease diagnostics market is segmented into consumables, instruments, and software and services. The consumables segment dominated the largest market revenue share of 67.4% in 2024, owing to the high and recurring demand for test kits, reagents, and cartridges required for PoC diagnostics. The continuous use of consumables in testing for diseases such as HIV, COVID-19, and influenza contributes to this segment’s dominance.

The software and services segment is expected to witness the fastest CAGR of 10.9% from 2025 to 2032, driven by the rising need for cloud integration, data analytics, and connectivity platforms that enhance diagnostic data interpretation, storage, and remote reporting.

- By Technology

On the basis of technology, the point of care infectious disease diagnostics market is segmented into lateral flow, agglutination assays, flow-through, and solid phase. The lateral flow segment held the largest revenue share of 54.6% in 2024, due to its widespread adoption in rapid antigen testing and its ease of use, portability, and cost-efficiency, particularly in low-resource settings.

The solid phase segment is projected to grow at the fastest CAGR of 11.3% during the forecast period, supported by its increasing role in multiplex testing and higher sensitivity in detecting complex biomarkers in infectious diseases.

- By Application

On the basis of application, the point of care infectious disease diagnostics market is segmented into HIV, tropical disease, liver disease, inflammatory disease, respiratory disease, hospital associated infections, and sexual health disorders. The HIV segment dominated the market with the largest revenue share of 28.7% in 2024, driven by global initiatives for early detection, widespread screening programs, and strong NGO/government support, particularly in Africa and Asia.

The respiratory disease segment is anticipated to witness the fastest CAGR of 12.5% from 2025 to 2032, due to heightened demand for rapid influenza and COVID-19 testing, increasing awareness, and government preparedness strategies against respiratory pandemics.

- By End User

On the basis of end user, the point of care infectious disease diagnostics market is segmented into hospitals, healthcare centers, laboratories, independent diagnostic centers, and home care settings. The hospitals segment accounted for the largest revenue share of 36.8% in 2024, fueled by high patient footfall, better funding, and the availability of infrastructure to handle infectious disease outbreaks.

The home care settings segment is projected to grow at the fastest CAGR of 13.2% from 2025 to 2032, owing to the rising trend of self-testing, increased awareness, and availability of FDA-approved PoC tests that allow patients to monitor their health from the comfort of home.

Point of Care Infectious Disease Diagnostics Market Regional Analysis

- North America dominated the point of care infectious disease diagnostics market with the largest revenue share of 38.6% in 2024, driven by a growing demand for rapid diagnostic solutions, rising prevalence of infectious diseases, and an increase in decentralized healthcare delivery models

- The region’s healthcare systems emphasize early disease detection, supported by robust investments in diagnostic innovation and government initiatives

- In addition, a strong presence of key players, advanced healthcare infrastructure, and favorable reimbursement policies are major factors contributing to the widespread adoption of PoC infectious disease diagnostics across hospitals, clinics, and even homecare settings

U.S. Point of Care Infectious Disease Diagnostics Market Insight

The U.S. point of care infectious disease diagnostics market captured the largest revenue share of 81.2% in 2024 within North America, primarily due to the high burden of diseases such as influenza, COVID-19, HIV, and RSV. The market is further bolstered by FDA support for rapid diagnostic tools, increasing public-private partnerships, and a surge in at-home testing solutions. Moreover, growing consumer awareness and rising adoption of digital and mobile health diagnostics support the ongoing expansion of the U.S. market.

Europe Point of Care Infectious Disease Diagnostics Market Insight

The Europe point of care infectious disease diagnostics market is projected to expand at a substantial CAGR during the forecast period, fueled by a rise in infectious disease screening campaigns, decentralization of diagnostics, and the increasing number of public health initiatives. Countries across Europe are actively adopting point-of-care technologies to reduce diagnosis turnaround time in both hospital and community settings. Enhanced regulatory frameworks and innovation in lateral flow assays and molecular PoC technologies are also driving regional growth.

U.K. Point of Care Infectious Disease Diagnostics Market Insight

The U.K. point of care infectious disease diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the government's focus on antimicrobial resistance, increased investment in diagnostics innovation, and integration of PoC testing into NHS workflows. Rapid testing solutions for sexually transmitted infections (STIs), respiratory diseases, and COVID-19 have gained popularity across clinics, pharmacies, and home settings. Ongoing research and the adoption of PoC diagnostics in public health surveillance further boost market expansion.

Germany Point of Care Infectious Disease Diagnostics Market Insight

The Germany point of care infectious disease diagnostics market is expected to expand at a considerable CAGR from 2025 to 2032, backed by strong support for precision diagnostics and the integration of PoC solutions in emergency and outpatient care. With its highly structured healthcare infrastructure and emphasis on infection control, Germany continues to lead in the adoption of molecular PoC technologies. The market is further supported by rising government funding, strong diagnostic manufacturing capabilities, and partnerships between academic and commercial entities.

Asia-Pacific Point of Care Infectious Disease Diagnostics Market Insight

The Asia-Pacific point of care infectious disease diagnostics market is poised to grow at the fastest CAGR of 12.4% during the forecast period of 2025 to 2032, driven by rising healthcare expenditures, increasing incidence of infectious diseases such as TB, dengue, and hepatitis, and expanding access to healthcare in rural regions. Countries such as China, India, and Japan are focusing on strengthening their primary care systems, where PoC diagnostics serve as a vital tool for early diagnosis and disease management. Government-led screening programs and public awareness campaigns are catalyzing the adoption of portable and affordable diagnostic solutions.

Japan Point of Care Infectious Disease Diagnostics Market Insight

The Japan point of care infectious disease diagnostics market is gaining momentum, with a projected CAGR of 11.1%, due to a growing aging population, government emphasis on healthcare digitization, and the need for rapid diagnostics in outbreak situations. High levels of technological innovation and integration of PoC diagnostics into hospital and elderly care systems support robust market growth. Japan’s focus on self-care and prevention through community clinics further promotes adoption.

China Point of Care Infectious Disease Diagnostics Market Insight

The China point of care infectious disease diagnostics market accounted for the largest market revenue share in Asia Pacific in 2024, at 33.2%, attributed to its expanding middle class, high disease burden, and strategic government initiatives such as the Healthy China 2030 plan. Domestic manufacturers are playing a significant role in producing cost-effective PoC diagnostic kits. The increasing integration of PoC diagnostics into telemedicine platforms and public health campaigns is further accelerating market growth.

Point of Care Infectious Disease Diagnostics Market Share

The point of care infectious disease diagnostics industry is primarily led by well-established companies, including:

- Siemens Healthineers AG (Germany)

- Trivitron Healthcare (India)

- Abbott (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Biomérieux (France)

- F. Hoffmann-La Roche Ltd (Switzerland)

- BD (U.S.)

- Chembio Diagnostics, Inc. (U.S.)

- Trinity Biotech (Ireland)

- Cardinal Health (U.S.)

- Bio-Rad Laboratories Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- QuidelOrtho Corporation (U.S.)

- OJ-Bio Limited (U.K.)

Latest Developments in Global Point of Care Infectious Disease Diagnostics Market

- In October 2023, QIAGEN achieved CE certification for its IVD kit and automated testing platform, NeuMoDx. This development significantly boosted the company’s revenue and market share

- In May 2023, Danaher Corporation introduced the Dxl 9000 Access Immunoassay Analyzer capable of processing up to 215 tests per hour. This launch expanded the company’s offerings in point-of-care diagnostics

- In May 2023, BD announced 510k clearance for its BD Kiestra Methicillin-resistant Staphylococcus aureus (MRSA) imaging application, which incorporates AI software. This innovation reduces test result turnaround times by automating the labor-intensive process of identifying bacterial growth traditionally done using petri dishes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.