Global Polyurethane Dispersion Market

Market Size in USD Billion

USD

2.68 Billion

USD

4.65 Billion

2025

2033

USD

2.68 Billion

USD

4.65 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.68 Billion | |

| USD 4.65 Billion | |

| % | |

|

Polyurethane Dispersion Market Overview

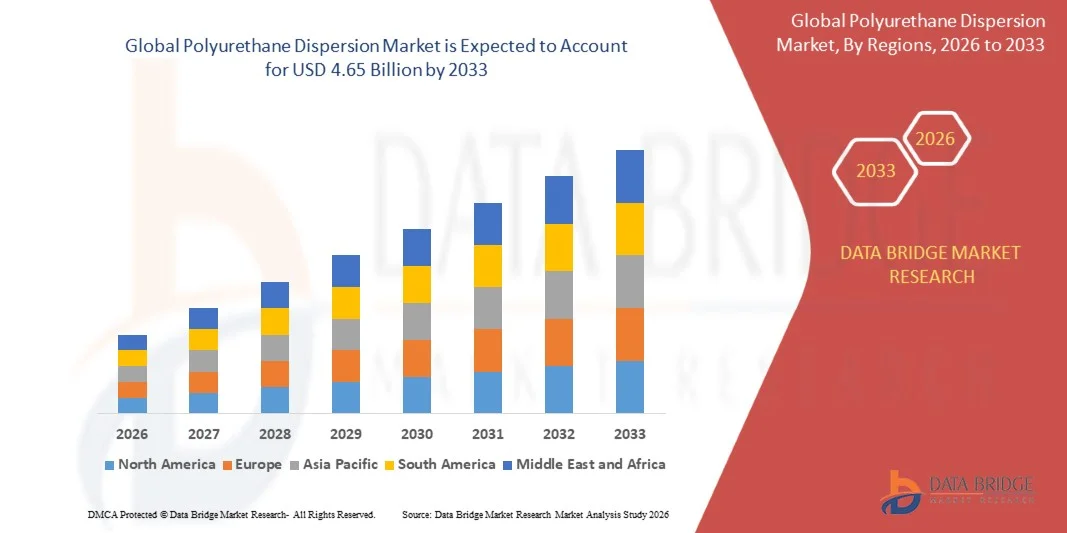

The Polyurethane Dispersion Market was valued at USD 2.68 billion in 2025 and is projected to reach USD 4.65 billion by 2033, growing at a CAGR of 7.15% from 2026 to 2033. The market is experiencing steady growth driven by rising demand for water-based and eco-friendly coating and adhesive solutions, increasing adoption of polyurethane dispersion (PUD) in industries such as automotive, textiles, leather, packaging, and construction, and growing regulatory pressure to reduce volatile organic compound (VOC) emissions.

The shift toward sustainable and high-performance materials, combined with increasing use of polyurethane dispersions in coatings, synthetic leather, adhesives, and sealants, is encouraging manufacturers to adopt advanced waterborne polymer technologies. PUDs are widely preferred due to their excellent flexibility, abrasion resistance, durability, and low environmental impact compared to solvent-based systems. The growing demand for eco-friendly coatings in automotive interiors, footwear, furniture, and industrial applications is further accelerating market growth globally.

Key Market Trends & Insights

- North America dominated the global polyurethane dispersion (PUD) market with the largest revenue share of 34.1% in 2025, supported by strong demand from coatings, adhesives, automotive, and textile industries, along with advanced chemical manufacturing infrastructure and high adoption of water-based sustainable polymer technologies. The region also benefits from stringent environmental regulations that are accelerating the shift from solvent-based systems to eco-friendly polyurethane dispersions.

- The Water-Based segment dominated the market with a 42% share in 2025, driven by stringent environmental regulations, rising demand for low-VOC formulations, and increasing adoption across coatings, adhesives, and textile finishing industries.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rapid industrialization, expansion of textile and leather manufacturing industries, and increasing investments in automotive and construction sectors across China, India, South Korea, and Southeast Asia. Growing demand for cost-effective, high-performance coatings and adhesives is further accelerating regional market growth.

- The adhesives & sealants segment is expected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by increasing use of polyurethane dispersions in automotive assembly, packaging, footwear, and construction applications. The segment is benefiting from rising demand for high-strength, flexible, and durable bonding solutions, particularly in lightweight vehicle manufacturing and eco-friendly packaging trends.

Market Size & Forecast

- Global Market Value (2025): USD 2.68 Billion

- Expected Market Value (2033): USD 4.65 Billion

- Forecast CAGR (2026–2033): 7.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Polyurethane Dispersion Market Segmentation

|

Attributes |

Polyurethane Dispersion Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• BASF SE (Germany) |

|

Market Opportunities |

· Rising Demand for Eco-Friendly Water-Based Coatings and Adhesives · Expansion of Textile, Leather, and Synthetic Leather Applications · Growing Adoption in Packaging, Paper, and Industrial Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Polyurethane Dispersion Market Trends

Trend: Growth in Waterborne & Sustainable Polyurethane Dispersion Systems

The Polyurethane Dispersion (PUD) market is witnessing strong momentum toward waterborne, low-VOC, and bio-based chemistries driven by tightening environmental regulations and rising demand from coatings, textiles, and adhesives industries. Manufacturers are increasingly shifting from solvent-based systems to high-performance waterborne PUDs to meet sustainability targets while maintaining durability, flexibility, and chemical resistance. For instance, in April 2021, Covestro expanded its waterborne polyurethane dispersion production capabilities in Asia to support growing demand from coatings and textile applications, reflecting the regional shift toward eco-friendly formulations. In March 2023, key industry participants including Lubrizol highlighted advancements in low-VOC polyurethane dispersion technologies aimed at high-performance coatings and adhesive applications. These developments are reinforcing the transition toward sustainable polymer chemistry across end-use industries such as automotive coatings, packaging, and footwear.

Polyurethane Dispersion Market Dynamics

Key Market Driver: Rising Demand from Coatings, Adhesives & High-Performance Applications

The rapid expansion of end-use industries such as automotive coatings, construction, textiles, and flexible packaging is a major driver for the Polyurethane Dispersion market. PUDs are increasingly preferred due to their excellent abrasion resistance, elasticity, and environmental compliance compared to solvent-based alternatives. In June 2022, BASF announced strategic enhancements in its polyurethane dispersion production network in Europe to strengthen supply reliability for coating and adhesive customers. In addition, growing adoption in textile finishing and synthetic leather applications is accelerating demand for high-solid and waterborne PUD formulations across both developed and emerging markets.

Key Restraint/Challenge: Raw Material Price Volatility and Processing Complexity

Despite strong growth, the market faces challenges related to fluctuating raw material costs such as isocyanates and polyols, which directly impact production economics. In addition, formulation complexity in achieving balanced performance (water resistance, flexibility, and mechanical strength) increases R&D costs for manufacturers. Smaller producers face barriers in scaling advanced waterborne dispersion technologies due to high capital requirements and stringent quality consistency standards. Regulatory compliance with evolving environmental norms in North America and Europe further adds operational pressure on manufacturers, especially those relying on legacy solvent-based production systems.

Key Market Opportunity: Expansion of Bio-Based and Sustainable Polyurethane Technologies

The integration of bio-based raw materials and circular economy principles presents a significant growth opportunity for the Polyurethane Dispersion market. Companies are increasingly investing in renewable feedstocks and carbon-reduced production processes to align with global sustainability goals. In September 2024, industry initiatives led by major chemical manufacturers such as Dow focused on advancing bio-based polyurethane material development for coatings and elastomer applications. The growing demand from packaging, automotive interiors, and footwear industries is expected to further accelerate innovation in high-performance, environmentally friendly polyurethane dispersion systems across global markets.

Polyurethane Dispersion Market Scope

The Polyurethane Dispersion market is segmented on the basis of type and application.

- By Type

On the basis of type, the Polyurethane Dispersion Market is segmented into Water-Based and Solvent-Based systems. The Water-Based segment dominated the market with a 68.42% share in 2025, driven by stringent environmental regulations, rising demand for low-VOC formulations, and increasing adoption across coatings, adhesives, and textile finishing industries. Water-based PUDs are widely preferred due to their eco-friendly profile, excellent flexibility, and strong adhesion properties, making them suitable for automotive interiors, synthetic leather, and industrial coatings. Growing regulatory pressure in North America and Europe under REACH and EPA norms further supports the dominance of this segment. Expanding R&D investments by major chemical manufacturers are improving performance characteristics such as water resistance and durability, enhancing commercial adoption. In addition, rising demand from packaging and footwear industries is reinforcing large-scale utilization. Increasing shift from solvent-based systems in emerging economies is also accelerating penetration. Continuous innovation in bio-based polyurethane dispersions is further strengthening this segment’s leadership. The segment benefits from cost-efficiency improvements in production technologies and scalable manufacturing capabilities. Strong compatibility with aqueous systems across multiple industries is another growth enabler. Overall, sustainability trends and regulatory compliance remain the key drivers supporting this dominant position.

The Solvent-Based segment is expected to witness the fastest growth with a CAGR of 5.8% from 2026 to 2033, driven by demand in high-performance industrial coatings and specialty applications requiring superior chemical and abrasion resistance. Despite environmental concerns, solvent-based PUDs remain relevant in niche applications such as automotive refinishing and heavy-duty coatings. Technological advancements are enabling reduced emissions and improved formulation stability, supporting gradual adoption. Growth is also supported by demand in regions with less stringent environmental regulations. Industrial infrastructure expansion in developing economies is further contributing to segment growth. Manufacturers are investing in hybrid dispersion systems to balance performance and compliance requirements. Increasing use in protective coatings for marine and construction industries is expanding opportunities. Rising demand for durable coatings in extreme environments also fuels adoption. Continued R&D efforts are improving efficiency and reducing solvent content. However, regulatory pressure remains a limiting factor compared to water-based systems.

- By Application

On the basis of application, the Polyurethane Dispersion Market is segmented into Coatings, Adhesives & Sealants, Leather Finishing, Paper & Textile, Fiberglass Sizing, and Others. The Coatings segment dominated the market with a 34.96% share in 2025, driven by strong demand from automotive, construction, and industrial sectors requiring durable, abrasion-resistant, and weatherproof coatings. Polyurethane dispersions are widely used due to their excellent film-forming ability, flexibility, and chemical resistance. Rising construction activities globally and infrastructure development projects are boosting consumption. Automotive OEMs increasingly use PUD-based coatings for interior and exterior components. Growth in protective coatings for industrial equipment is further supporting demand. Environmental regulations favor waterborne coatings, strengthening segment expansion. Technological improvements are enhancing gloss retention and durability. Increasing use in wood coatings and furniture applications is also contributing to growth. Expanding packaging and consumer goods industries are further driving adoption. Overall, coatings remain the most critical revenue-generating application segment.

The Adhesives & Sealants segment is expected to witness the fastest growth with a CAGR of 6.4% from 2026 to 2033, driven by rising demand in packaging, automotive assembly, and construction industries. PUD-based adhesives offer strong bonding strength, flexibility, and environmental safety advantages. Growth in e-commerce packaging is significantly boosting consumption. Automotive lightweighting trends are increasing demand for high-performance adhesive solutions. Expansion of infrastructure projects in Asia-Pacific is further supporting growth. Increasing replacement of solvent-based adhesives with waterborne alternatives is accelerating adoption. Technological advancements are improving thermal and mechanical resistance properties. Rising use in footwear manufacturing is another key driver. Strong R&D investments in pressure-sensitive adhesives are expanding application scope. Overall, industrial shift toward sustainable bonding solutions is fueling rapid segment growth.

Polyurethane Dispersion Market Regional Analysis

North America dominated the global polyurethane dispersion (PUD) market and accounted for the largest revenue share of 34.1% in 2025, supported by strong demand from coatings, adhesives, automotive, and textile industries, along with advanced chemical manufacturing infrastructure and high adoption of water-based sustainable polymer technologies. The region also benefits from stringent environmental regulations that are accelerating the shift from solvent-based systems to eco-friendly polyurethane dispersions. Rising demand for high-performance, low-VOC materials across industrial and commercial applications is further strengthening market growth in North America.

U.S. Polyurethane Dispersion Market Insight

The U.S. polyurethane dispersion market is witnessing steady growth due to increasing adoption of water-based coatings, adhesives, and sealants across automotive, construction, textile, and industrial sectors. Strong focus on sustainability, regulatory compliance for VOC reduction, and growing preference for eco-friendly materials are driving demand. In addition, advancements in polymer chemistry and rising investments in high-performance coating technologies are supporting market expansion across the country.

Europe Polyurethane Dispersion Market Insight

The Europe polyurethane dispersion market remains a key revenue contributor, driven by strict environmental regulations, strong industrial base, and growing adoption of sustainable coating and adhesive solutions. Industries such as automotive, furniture, packaging, and textiles are increasingly shifting toward water-based PUD systems to meet emission standards and sustainability targets. Continuous innovation in polymer technology and strong emphasis on circular economy practices are further supporting market growth across the region.

U.K. Polyurethane Dispersion Market Insight

The U.K. polyurethane dispersion market is experiencing steady expansion, supported by rising demand for low-VOC coatings, adhesives, and textile finishing solutions. The country’s strong focus on sustainability initiatives and green manufacturing practices is encouraging industries to adopt water-based polyurethane systems. Growth in automotive interiors, construction coatings, and packaging applications is further contributing to market development.

Germany Polyurethane Dispersion Market Insight

The Germany polyurethane dispersion market is expanding steadily due to strong automotive manufacturing, advanced chemical production capabilities, and strict environmental regulations. German industries are increasingly adopting water-based polyurethane dispersions in coatings, adhesives, and industrial applications to meet sustainability and performance requirements. Continuous innovation in materials science and high demand from automotive and industrial sectors are driving further growth.

Asia-Pacific Polyurethane Dispersion Market Insight

The Asia-Pacific polyurethane dispersion market is expected to witness rapid growth at a CAGR of 7.6% from 2026 to 2033, driven by rapid industrialization, expansion of textile and leather manufacturing industries, and increasing investments in automotive and construction sectors across China, India, South Korea, and Southeast Asia. Rising demand for cost-effective, high-performance, and environmentally compliant coating and adhesive solutions is significantly accelerating regional market expansion.

Japan Polyurethane Dispersion Market Insight

The Japan polyurethane dispersion market is witnessing consistent growth due to increasing demand for advanced coatings, adhesives, and textile finishing applications. Strong emphasis on high-quality manufacturing, technological innovation, and environmental compliance is driving adoption of water-based PUD systems. The automotive and electronics industries are also contributing to steady demand for high-performance polyurethane dispersion solutions.

China Polyurethane Dispersion Market Insight

The China polyurethane dispersion market is growing rapidly, driven by expanding manufacturing industries, strong demand from textile and automotive sectors, and increasing environmental regulations promoting low-VOC materials. Rising adoption of water-based coatings and adhesives across construction, packaging, and industrial applications is further boosting market growth. Continued investments in chemical production capacity and sustainable material technologies are positioning China as one of the fastest-growing markets globally.

Polyurethane Dispersion Market Share

The Polyurethane Dispersion industry is primarily led by well-established companies, including:

- Moog Inc. (U.S.)

- Dallara (Italy)

- Exail (France)

- IPG Automotive GmbH (Germany)

- aiMotive (Hungary)

- VI‑grade GmbH (Germany)

- Cruden B.V. (Netherlands)

- Dynisma Ltd. (UK)

- Applied Intuition Inc. (U.S.)

- rFpro (rFpro Limited) (England)

- Siemens AG (Germany)

- Dassault Systèmes SE (France)

- MTS Systems Corporation (U.S.)

- CAE Inc. (Canada)

- NVIDIA Corporation (U.S.)

- AB Dynamics PLC (U.K.)

- Forum8 (Japan)

- Mitsubishi Precision Co., Ltd. (Japan)

- FAAC Incorporated (U.S.)

- DriveSafety (U.S.)

- Simtec Simulation Technology GmbH (Germany)

- MB Dynamics Inc. (U.S.)

- Sanlab Simulation (India)

- SimCraft (U.S.)

- CXC Simulations (U.S.)

- XPI Simulation (United Kingdom)

- Tecknotrove Simulator Systems Pvt. Ltd. (India)

- Zhejiang Kechi Intelligent Technology Co., Ltd. (China)

- Shenzhen Zhongzhi Simulation (China)

- Hindustan Simulators (India)

- DriveSimSolutions (U.S.)

- Teksim Technologies (India)

- iMVR Inc. (U.S.)

- SimXperience (U.S.)

Latest Developments in Polyurethane Dispersion Market

- In April 2021, Covestro AG, a leading materials manufacturer, announced the expansion of its waterborne polyurethane dispersion production capabilities in Asia-Pacific, aimed at meeting rising demand from coatings, adhesives, and textile industries. The expansion focused on strengthening supply reliability and supporting the transition toward low-VOC and environmentally friendly polyurethane systems. This development reflects the accelerating shift in the region toward sustainable coating technologies driven by regulatory pressure and industrial growth

- In June 2022, BASF SE, a global chemical company, expanded its polyurethane dispersion production and supply network in Europe to enhance availability for coatings and adhesive applications. The initiative was aimed at improving supply chain resilience and supporting automotive and construction industries transitioning to waterborne systems. This move reinforced BASF’s position in high-performance, eco-friendly polymer solutions amid tightening environmental regulations

- In March 2023, Covestro AG introduced advancements in waterborne polyurethane dispersion technologies designed for high-performance coatings applications, particularly in automotive and industrial sectors. The innovation focused on improving durability, flexibility, and environmental compliance while reducing volatile organic compound (VOC) emissions. This development highlights ongoing industry efforts to replace solvent-based systems with sustainable alternatives without compromising performance

- In September 2024, major polyurethane manufacturers including Dow Inc. and other global chemical companies advanced bio-based and sustainable polyurethane dispersion initiatives aimed at reducing carbon footprint and improving circular material usage. These developments included R&D investments into renewable feedstocks and next-generation waterborne formulations for coatings and elastomers. This reflects the increasing industry-wide push toward sustainable chemistry solutions across automotive, packaging, and industrial applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polyurethane Dispersion Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polyurethane Dispersion Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polyurethane Dispersion Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.