Global Pontine Glioma Treatment Market

Market Size in USD Million

USD

915.24 Million

USD

1,242.96 Million

2024

2032

USD

915.24 Million

USD

1,242.96 Million

2024

2032

| 2025 - 2032 | |

| USD 915.24 Million | |

| USD 1,242.96 Million | |

| % | |

|

Pontine Glioma Treatment Market Size

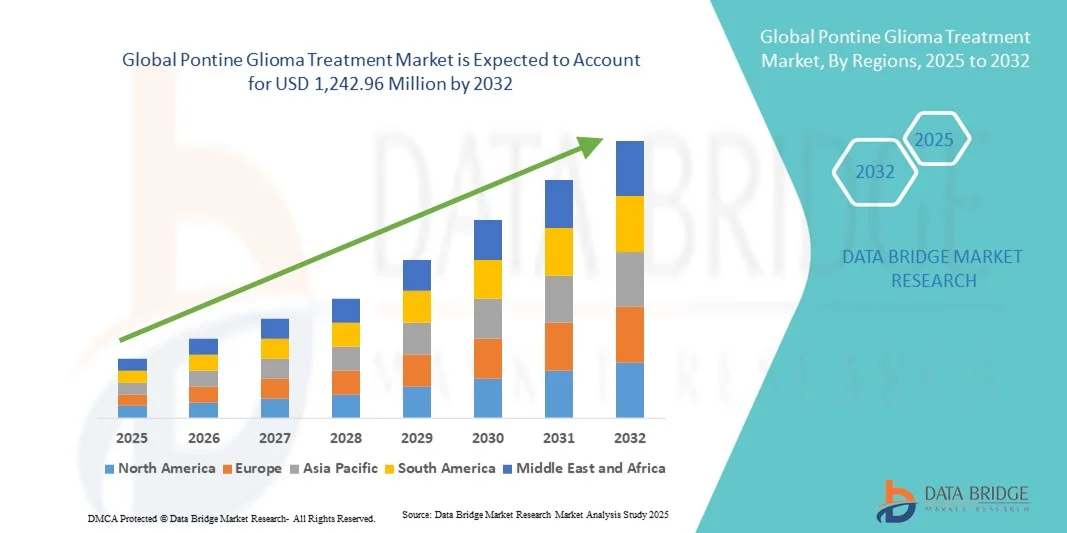

- The global pontine glioma treatment market size was valued at USD 915.24 million in 2024 and is expected to reach USD 1,242.96 million by 2032, at a CAGR of 3.90% during the forecast period

- The market growth is largely fueled by increasing incidence of diffuse intrinsic pontine glioma (DIPG), rising research initiatives, and advancements in targeted therapies, which are enhancing treatment options for this rare and aggressive pediatric brain tumor

- Furthermore, ongoing clinical trials, FDA approvals of novel drugs, and rising awareness among healthcare providers and caregivers are establishing pontine glioma treatments as a critical focus in pediatric oncology. These converging factors are accelerating the adoption of innovative therapies, thereby significantly boosting the industry's growth

Pontine Glioma Treatment Market Analysis

- Pontine glioma treatments, targeting diffuse intrinsic pontine glioma (DIPG), are increasingly critical in pediatric oncology due to the aggressive nature of the tumor, limited survival rates, and the need for precise, targeted therapeutic approaches in both clinical and research settings

- The escalating demand for pontine glioma treatments is primarily fueled by rising incidence rates in children, ongoing clinical trials for novel drugs, and growing awareness among healthcare providers and caregivers about advanced treatment options

- North America dominated the pontine glioma treatment market with the largest revenue share of 43% in 2024, driven by early adoption of advanced oncology therapies, robust healthcare infrastructure, and a strong presence of key pharmaceutical and biotech companies conducting clinical trials for innovative therapies, particularly in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the pontine glioma treatment market during the forecast period due to increasing investment in pediatric oncology research, improved healthcare access, and government initiatives supporting rare disease treatment development

- Radiotherapy segment dominated the pontine glioma treatment market with a market share of 39.1% in 2024, driven by its established efficacy in managing DIPG and ongoing enhancements in precision radiotherapy techniques that improve patient outcomes

Report Scope and Pontine Glioma Treatment Market Segmentation

|

Attributes |

Pontine Glioma Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Pontine Glioma Treatment Market Trends

Advancements in Targeted Therapies and Precision Medicine

- A significant and accelerating trend in the global pontine glioma treatment market is the development of targeted therapies and precision medicine approaches, which aim to attack tumor cells while minimizing damage to healthy brain tissue

- For instance, ongoing clinical trials with drugs such as ONC201 and Melphalan hydrochloride are investigating molecularly targeted treatments that improve patient outcomes in DIPG

- Precision medicine enables personalized treatment plans based on tumor genetics, epigenetics, and biomarker profiles, increasing the such likelyhood of treatment efficacy and reducing adverse effects

- These therapies are often combined with advanced radiotherapy techniques to optimize tumor control and extend survival, offering a more holistic treatment approach

- The trend towards personalized and molecularly guided therapies is reshaping treatment protocols and raising expectations for improved clinical outcomes

- The demand for innovative targeted therapies and precision medicine is growing rapidly across pediatric oncology centers, as clinicians prioritize more effective and less toxic treatment options

Pontine Glioma Treatment Market Dynamics

Driver

Increasing Pediatric DIPG Incidence and Research Initiatives

- The rising prevalence of diffuse intrinsic pontine glioma (DIPG) in children, coupled with increasing research initiatives, is a significant driver of the pontine glioma treatment market

- For instance, institutions such as Johns Hopkins Hospital and St. Jude Children’s Research Hospital are conducting clinical trials exploring novel therapies for DIPG

- Rising awareness among healthcare providers and caregivers about the aggressive nature of DIPG is contributing to higher demand for effective treatment options

- Funding from government bodies and non-profit organizations for rare pediatric brain tumors is facilitating accelerated drug development and clinical trials

- Increasing approvals of orphan drugs for rare brain tumors are supporting market growth and providing new treatment avenues

- Expansion of pediatric oncology centers globally is enhancing access to advanced treatments and clinical trial participation

- The need for effective treatment solutions and improved survival rates is pushing pharmaceutical companies to invest in innovative therapies and expand treatment pipelines

Restraint/Challenge

Blood-Brain Barrier and Limited Treatment Options

- The presence of the blood-brain barrier (BBB) and limited availability of effective therapies pose significant challenges to pontine glioma treatment adoption and success

- For instance, traditional chemotherapy often fails to reach therapeutic concentrations within the brainstem, reducing efficacy in DIPG patients

- Critical limitations in drug delivery and tumor accessibility hinder the development of universally effective therapies

- High costs associated with clinical trials and experimental therapies may restrict access for certain patient populations, particularly in developing regions

- Limited understanding of the molecular mechanisms of DIPG complicates the identification of novel therapeutic targets

- Regulatory hurdles and lengthy approval processes for pediatric rare disease drugs delay the availability of new treatments to patients

- Overcoming these challenges requires innovative drug delivery technologies, advanced clinical research, and international collaboration to improve treatment accessibility and outcomes

Pontine Glioma Treatment Market Scope

The market is segmented on the basis of grade, classification, diagnosis, treatment, route of administration, end-user, and distribution channel.

- By Grade

On the basis of grade, the pontine glioma treatment market is segmented into Grade I, Grade II, Grade III, and Grade IV. The Grade IV segment dominated the market in 2024 due to the aggressive nature of high-grade tumors such as DIPG, which require intensive therapies and multidisciplinary management. These tumors drive higher treatment expenditure and greater reliance on advanced radiotherapy and targeted chemotherapy. Clinical trials and research initiatives primarily focus on high-grade tumors, increasing demand. The high mortality and rapid progression of Grade IV tumors create urgency for innovative therapies. Hospitals and pediatric oncology centers prioritize treatment for these cases. Caregiver awareness and early intervention efforts further reinforce market dominance.

The Grade II segment is expected to witness the fastest growth during forecast period, as early detection allows timely intervention with targeted and combination therapies. Lower-grade tumors often respond better to therapy, improving survival rates. Pediatric oncology centers are increasingly adopting molecularly guided treatments. Advances in diagnostic imaging facilitate early identification of Grade II tumors. Research into novel drugs and immunotherapies is expanding for lower-grade gliomas. Improved healthcare infrastructure in emerging regions supports rising demand.

- By Classification

On the basis of classification, the pontine glioma treatment market is segmented into diffuse brain stem glioma, focal brain stem glioma, and recurrent brain stem glioma. The diffuse brain stem glioma segment dominated in 2024 due to its prevalence and poor prognosis in pediatric patients. Surgical options are limited due to tumor infiltration, increasing reliance on radiotherapy and systemic therapies. Clinical research focuses heavily on diffuse gliomas because of high unmet medical needs. Government and non-profit funding often prioritizes diffuse tumors. Hospitals and cancer centers treat most of these cases, reinforcing market share. Awareness campaigns and advocacy for aggressive tumors further support dominance.

The focal brain stem glioma segment is expected to witness the fastest growth during forecast period, as localized tumors are more amenable to surgical resection and targeted therapy. Minimally invasive surgical techniques and improved imaging increase treatment success. Early diagnosis leads to better patient outcomes. Clinical trials increasingly explore focal glioma therapies. Pharmaceutical companies are developing drugs for localized tumors. Rising investment in pediatric neuro-oncology infrastructure supports growth.

- By Diagnosis

On the basis of diagnosis, the pontine glioma treatment market is segmented into CT scan, biopsy, and MRI. The MRI segment dominated in 2024 due to its high-resolution imaging and ability to detect tumor boundaries accurately in the brainstem. MRI is used for both diagnosis and treatment monitoring. Advanced MRI techniques such as functional MRI aid in precise radiotherapy planning. MRI availability in pediatric oncology centers supports widespread adoption. Early detection through MRI is critical for timely intervention. MRI integration into clinical workflows makes it a standard in hospitals. Hospitals rely on MRI for ongoing patient management and treatment evaluation.

The biopsy segment is expected to witness the fastest growth during forecast period as minimally invasive and stereotactic biopsy techniques allow molecular profiling. Molecular data guide personalized therapies. Biopsies support clinical trial enrollment. Advances in biopsy technology reduce procedural risk. Adoption of precision medicine increases demand for biopsies. Expansion of research hospitals offering biopsy-based diagnostics drives growth. Biopsy procedures are becoming essential for tailored DIPG treatment.

- By Treatment

On the basis of treatment, the pontine glioma treatment market is segmented into surgery, radiotherapy, and chemotherapy. The radiotherapy segment dominated in 2024 with a market share of 39.1%, because it is the standard treatment for DIPG and other high-grade pontine gliomas. Advanced radiotherapy techniques improve targeting while minimizing damage to healthy tissue. Radiotherapy is often combined with systemic therapies to improve outcomes. Clinical guidelines recommend radiotherapy for most high-grade tumors. Hospitals with radiotherapy facilities are central to patient care. Ongoing research continues to expand precision radiotherapy adoption. Radiotherapy provides palliative benefits and supports improved survival in aggressive tumors.

The chemotherapy segment is expected to witness the fastest growth during forecast period, driven by the development of targeted and immunotherapeutic agents. Novel drugs designed to cross the blood-brain barrier improve efficacy. Combination therapy protocols are increasingly adopted. Clinical trials for chemotherapy agents are expanding rapidly. Pediatric oncology centers increasingly use systemic treatments alongside radiotherapy. Improved patient compliance with oral and intravenous regimens supports market growth. Chemotherapy innovation offers hope for previously untreatable cases.

- By Route of Administration

On the basis of route of administration, the pontine glioma treatment market is segmented into oral and parenteral. The parenteral segment dominated in 2024 due to intravenous administration of chemotherapy and investigational drugs that bypass the blood-brain barrier. Hospital-based administration ensures controlled dosing and patient safety. Parenteral delivery provides higher bioavailability, essential for high-grade tumors. Pediatric oncology centers provide most parenteral therapies. Clinical trials often require hospital-administered drugs. Regulatory approvals favor controlled hospital-based administration. Hospitals monitor patient response and manage adverse effects with parenteral treatments.

The oral segment is expected to witness the fastest growth during forecast period, as emerging targeted oral therapies allow outpatient treatment and improved patient convenience. Oral drugs improve adherence in pediatric patients. Precision medicine supports personalized oral regimens. Increased availability of investigational oral therapies drives adoption. Home-based treatment programs enhance accessibility. Pharmaceutical R&D focuses on developing effective oral formulations. Oral administration reduces hospital dependency for less aggressive tumors.

- By End-User

On the basis of end-user, the pontine glioma treatment market is segmented into cancer research institutes, diagnostic laboratories, hospitals, and others. The hospitals segment dominated in 2024 due to availability of comprehensive treatment options including surgery, radiotherapy, and chemotherapy. Hospitals are primary sites for clinical trials and diagnostics. Multidisciplinary teams provide integrated patient care. Well-established infrastructure ensures adoption of advanced therapies. Pediatric oncology centers manage complex treatment regimens. Hospitals provide continuous monitoring of treatment outcomes. Hospitals play a central role in treatment, research, and patient support.

The cancer research institutes segment is expected to witness the fastest growth during forecast period, due to increasing clinical trials and drug discovery initiatives. Research institutes focus on novel DIPG therapies. Collaborations with pharmaceutical companies accelerate treatment development. Institutes provide access to experimental therapies. Government and non-profit funding supports research activities. Expansion of pediatric neuro-oncology programs increases adoption. Institutes play a key role in translational research and therapy innovation.

- By Distribution Channel

On the basis of distribution channel, the pontine glioma treatment market is segmented into hospital pharmacy, retail pharmacy, and others. The hospital pharmacy segment dominated in 2024, as specialized drugs and complex dosing regimens are managed primarily in hospitals. Hospital pharmacies provide investigational and orphan drugs under supervision. Availability of clinical trial medications reinforces dominance. Hospitals ensure safe and effective administration. Pediatric oncology hospitals rely on in-house pharmacies. Regulatory approvals favor hospital-based distribution. Hospital pharmacies also manage drug storage and handling requirements.

The retail pharmacy segment is expected to witness the fastest growth during forecast period, driven by oral therapies and supportive medications for home use. Increased patient convenience fuels adoption. Regulatory changes are enabling wider outpatient access. Home-based treatment programs increase demand. Growing awareness among caregivers supports retail pharmacy use. Expansion of specialty pharmacies offering pediatric oncology drugs contributes to growth. Retail distribution improves accessibility for ongoing oral therapy management.

Pontine Glioma Treatment Market Regional Analysis

- North America dominated the pontine glioma treatment market with the largest revenue share of 43% in 2024, driven by early adoption of advanced oncology therapies, robust healthcare infrastructure, and a strong presence of key pharmaceutical and biotech companies conducting clinical trials for innovative therapies, particularly in the U.S.

- Healthcare providers in the region prioritize advanced treatment modalities such as radiotherapy, targeted therapies, and precision medicine approaches, enhancing adoption of innovative pontine glioma treatments

- This dominance is further supported by the presence of key pharmaceutical and biotech companies conducting extensive clinical trials, strong government and non-profit funding for rare pediatric cancers, and early access to newly approved therapies

U.S. Pontine Glioma Treatment Market Insight

The U.S. pontine glioma treatment market captured the largest revenue share of 83% in 2024 within North America, driven by a high prevalence of pediatric DIPG cases and advanced healthcare infrastructure. Hospitals and specialized pediatric oncology centers prioritize radiotherapy, targeted therapies, and precision medicine approaches. The presence of leading pharmaceutical and biotech companies conducting extensive clinical trials further accelerates market growth. Increasing awareness among caregivers and clinicians about aggressive pontine gliomas enhances adoption of advanced treatment protocols. Government and non-profit funding for rare pediatric cancers supports research and therapy development. Integration of novel diagnostic and treatment technologies in top hospitals strengthens the market position.

Europe Pontine Glioma Treatment Market Insight

The Europe pontine glioma treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of pediatric brain tumors and improved healthcare access. Stringent regulatory frameworks for drug approvals and the adoption of advanced treatment modalities encourage market growth. Urbanization and increasing investment in pediatric oncology infrastructure foster the availability of radiotherapy and novel therapies. European hospitals and cancer centers are incorporating multidisciplinary treatment approaches for better outcomes. Government initiatives supporting rare disease treatment development boost adoption. Collaboration between research institutes and hospitals promotes clinical trial enrollment.

U.K. Pontine Glioma Treatment Market Insight

The U.K. pontine glioma treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by increasing focus on pediatric oncology and early intervention programs. Rising awareness about DIPG and other aggressive pontine gliomas among healthcare providers and caregivers drives demand for advanced treatment solutions. The availability of specialized hospitals and pediatric oncology centers enhances access to radiotherapy and investigational therapies. Growing investment in clinical trials and targeted therapies supports market expansion. Collaboration between healthcare institutions and research organizations accelerates adoption. The emphasis on personalized medicine and precision therapies further stimulates market growth.

Germany Pontine Glioma Treatment Market Insight

The Germany pontine glioma treatment market is expected to expand at a considerable CAGR during the forecast period, driven by advanced healthcare infrastructure and emphasis on innovative treatment solutions. Increasing awareness of pediatric brain tumors and early diagnosis initiatives supports therapy adoption. Hospitals and oncology centers offer multidisciplinary treatment options including radiotherapy, chemotherapy, and targeted therapies. Government and non-profit funding for rare pediatric cancers enhances research and clinical trial activities. Integration of advanced diagnostic technologies aids in precise treatment planning. Germany’s focus on sustainable and patient-centric healthcare promotes the use of novel therapies.

Asia-Pacific Pontine Glioma Treatment Market Insight

The Asia-Pacific pontine glioma treatment market is poised to grow at the fastest CAGR of 26% during 2025–2032, driven by rising incidence of pediatric brain tumors and improving healthcare access in countries such as China, Japan, and India. Increasing investment in pediatric oncology infrastructure and government initiatives promoting rare disease treatment accelerate market adoption. The availability of advanced diagnostic tools and treatment centers improves early detection and care. Expanding clinical trial activity and collaborations with global pharmaceutical companies support therapy development. Growing awareness among caregivers about aggressive pontine gliomas fuels demand. Improvements in healthcare reimbursement systems further enhance market accessibility.

Japan Pontine Glioma Treatment Market Insight

The Japan pontine glioma treatment market is gaining momentum due to high healthcare standards, advanced diagnostic capabilities, and increasing focus on pediatric oncology. Hospitals are integrating radiotherapy, chemotherapy, and targeted therapies for optimal patient outcomes. Government and non-profit funding for rare pediatric cancers drives clinical research and adoption of innovative therapies. Awareness campaigns among caregivers enhance early intervention and therapy adherence. The country’s aging population also supports demand for advanced pediatric care infrastructure. Collaborations between hospitals and research institutes promote clinical trials and novel treatment adoption.

India Pontine Glioma Treatment Market Insight

The India pontine glioma treatment market accounted for the largest revenue share in Asia-Pacific in 2024, driven by increasing healthcare infrastructure and growing awareness of pediatric brain tumors. Hospitals and oncology centers are expanding access to radiotherapy, chemotherapy, and investigational targeted therapies. The push towards rare disease treatment programs and government initiatives supporting pediatric oncology research boosts market growth. High incidence of DIPG and other aggressive pontine gliomas increases demand for effective therapies. Availability of affordable treatment options and growing clinical trial participation further contribute to growth. Strong collaboration between domestic and international research institutes enhances therapy development and adoption.

Pontine Glioma Treatment Market Share

The Pontine Glioma Treatment industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AstraZeneca (U.K.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- SERVIER LABORATORIES (France)

- Jazz Pharmaceuticals, Inc. (Ireland)

- MedImmune (U.S.)

- Oncoceutics (U.S.)

- Chimerix (U.S.)

- VBL Therapeutics (Israel)

- DelMar Pharmaceuticals (Canada)

- VBI Vaccines Inc (Canada)

- Kazia Therapeutics Limited (Australia)

- CNS Pharmaceuticals, Inc. (U.S.)

- Istari Oncology (U.S.)

- SonALAsense (U.S.)

What are the Recent Developments in Global Pontine Glioma Treatment Market?

- In August 2025, the U.S. Food and Drug Administration (FDA) granted accelerated approval to dordaviprone (Modeyso) as the first systemic therapy for recurrent H3K27M-mutant diffuse midline glioma (DMG), a rare and aggressive brain tumor affecting children and young adults. The approval was based on data from five clinical studies involving 50 patients, showing tumor shrinkage in approximately 22% of cases, with benefits lasting over ten months for responders

- In July 2025, researchers at Columbia Engineering and Weill Cornell Medicine initiated phase I/II clinical trials to explore the use of focused ultrasound (FUS) to temporarily open the blood-brain barrier in DIPG patients. This non-invasive method aims to enhance the delivery of therapeutic agents directly to the tumor site, potentially transforming treatment for DIPG and other brain conditions

- In May 2025, a study led by Dr. Mark Souweidane at Weill Cornell Medicine and Memorial Sloan Kettering Cancer Center demonstrated the safety of convection-enhanced delivery (CED) for treating DIPG. CED involves using a catheter to deliver medication directly to the brainstem, bypassing the blood-brain barrier. The study showed that CED could safely deliver targeted treatments to the brainstem, offering hope for improved long-term survival rates in DIPG patients

- In April 2025, the FDA granted breakthrough therapy designation to BCB-276, an autologous B7-H3-targeted CAR T-cell therapy, for the treatment of pediatric patients with DIPG. This designation aims to expedite the development and review of the therapy, highlighting its potential to address unmet medical needs in treating this aggressive brain tumor

- In January 2025, researchers at Stanford Medicine reported that chimeric antigen receptor (CAR) T-cell therapy demonstrated promise against pediatric diffuse midline gliomas, including DIPG. The therapy involves engineering immune cells to target tumor cells, offering a potential new treatment avenue for these deadly cancers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.