Global Primary Pulmonary Hypertension Pph Treatment Market

Market Size in USD Billion

USD

1.67 Billion

USD

2.50 Billion

2024

2032

USD

1.67 Billion

USD

2.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.67 Billion | |

| USD 2.50 Billion | |

| % | |

|

Primary Pulmonary Hypertension (PPH) Treatment Market Size

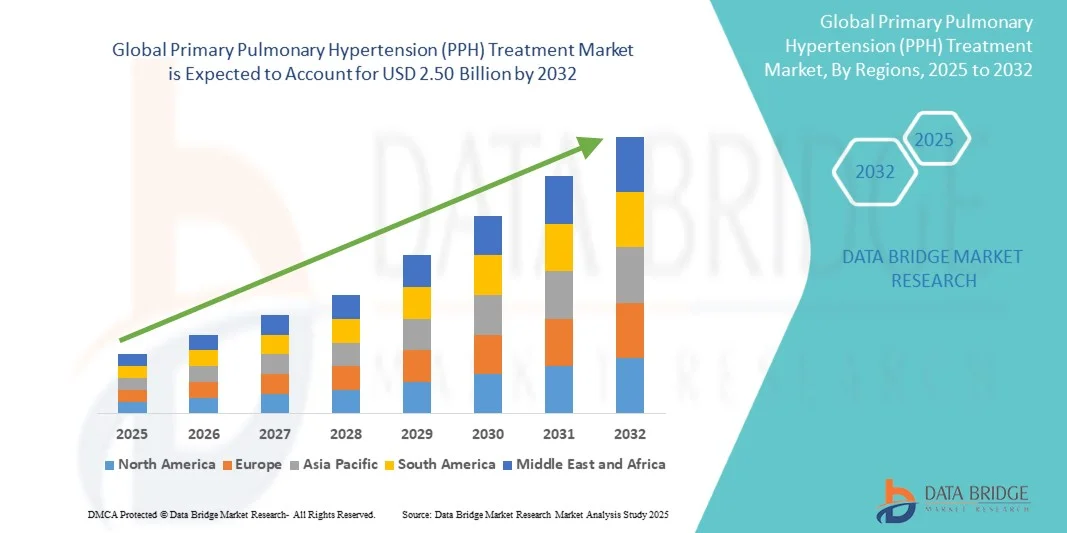

- The global Primary Pulmonary Hypertension (PPH) treatment market size was valued at USD 1.67 billion in 2024 and is expected to reach USD 2.50 billion by 2032, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of pulmonary arterial hypertension (PAH), advancements in drug development, and rising awareness of the condition, driving demand for effective treatment options

- Furthermore, government initiatives supporting rare disease research, favorable reimbursement policies, and growing patient access to innovative therapies are establishing PPH treatments as essential solutions, thereby significantly boosting the industry's growth

Primary Pulmonary Hypertension (PPH) Treatment Market Analysis

- Primary pulmonary hypertension (PPH) treatments, including medication, oxygen therapy, and supportive care, are increasingly vital in managing pulmonary arterial hypertension due to their ability to improve patient survival, exercise capacity, and quality of life

- The escalating demand for PPH treatments is primarily fueled by the rising prevalence of pulmonary arterial hypertension, increasing awareness among patients and healthcare providers, and advancements in pharmacological therapies that offer improved efficacy and safety profiles

- North America dominated the Primary Pulmonary Hypertension (PPH) treatment market with the largest revenue share of 39.6% in 2024, characterized by early adoption of innovative therapies, high healthcare expenditure, and strong presence of leading pharmaceutical companies, with the U.S. showing substantial growth in treatment uptake driven by robust clinical research, reimbursement support, and awareness campaigns

- Asia-Pacific is expected to be the fastest-growing region in the Primary Pulmonary Hypertension (PPH) treatment market during the forecast period due to increasing diagnosis rates, improving healthcare infrastructure, and growing patient access to advanced therapies

- Medication segment dominated the Primary Pulmonary Hypertension (PPH) treatment market with a market share of 42.8% in 2024, driven by its established clinical efficacy, ease of administration, and widespread adoption across hospitals, specialty clinics, and home healthcare settings

Report Scope and Primary Pulmonary Hypertension (PPH) Treatment Market Segmentation

|

Attributes |

Primary Pulmonary Hypertension (PPH) Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Primary Pulmonary Hypertension (PPH) Treatment Market Trends

“Advancements in Targeted Therapies and Personalized Medicine”

- A significant and accelerating trend in the global PPH treatment market is the development of targeted therapies such as endothelin receptor antagonists, phosphodiesterase-5 inhibitors, and prostacyclin analogs, improving patient outcomes and survival

- For instance, Adempas® (riociguat) demonstrates personalized treatment approaches by tailoring dosages based on individual patient response and hemodynamic parameters, enhancing efficacy and minimizing side effects

- The integration of novel therapies with patient-specific care plans allows clinicians to optimize treatment regimens, monitor disease progression more effectively, and improve quality of life for patients across various age groups

- Personalized medicine approaches, combined with telemedicine and remote patient monitoring, facilitate continuous care and adjustment of therapy based on real-time health data, enabling proactive disease management

- This trend towards more precise, individualized, and outcome-driven treatment strategies is reshaping therapeutic expectations, prompting pharmaceutical companies such as Actelion to innovate further in drug development and patient care

- The demand for advanced, targeted, and personalized PPH therapies is growing rapidly across both adult and pediatric populations, as healthcare providers increasingly focus on improving clinical outcomes and long-term survival

Primary Pulmonary Hypertension (PPH) Treatment Market Dynamics

Driver

“Increasing Prevalence and Awareness of Pulmonary Hypertension”

- The rising prevalence of pulmonary arterial hypertension, along with growing awareness among healthcare providers and patients, is a significant driver for increased adoption of PPH treatments

- For instance, the Pulmonary Hypertension Association (PHA) initiatives in 2024 have increased diagnosis rates and patient education, directly influencing the demand for advanced therapies

- As early diagnosis improves, patients gain timely access to effective medications, oxygen therapy, and supportive care, contributing to better disease management and increased treatment uptake

- Furthermore, healthcare infrastructure improvements and the availability of reimbursement programs in key regions are making PPH treatments more accessible, supporting consistent market growth

- The adoption of guideline-based treatment protocols and the inclusion of PPH therapies in hospital formularies and specialty clinics are propelling the market by ensuring that patients receive appropriate and effective care

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Regions”

- The high cost of advanced PPH therapies, including branded medications and combination treatments, poses a significant challenge to widespread market penetration, particularly in developing economies

- For instance, the price of therapies such as Tracleer® (bosentan) can be prohibitive for uninsured patients or regions with limited healthcare funding, restricting adoption despite clinical efficacy

- Limited access to diagnostic tools, specialist care, and advanced medications in certain regions further constrains market growth and delays timely intervention

- In addition, side effects associated with long-term use of some PPH medications can influence patient adherence, creating challenges for healthcare providers in managing treatment continuity

- Overcoming these challenges through cost-effective generic alternatives, improved healthcare access, and patient assistance programs is crucial for sustaining long-term market expansion and improving patient outcomes

Primary Pulmonary Hypertension (PPH) Treatment Market Scope

The market is segmented on the basis of diagnosis, treatment, drug type, population, route of administration, end-users, and distribution channel.

- By Diagnosis

On the basis of diagnosis, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into Chest X-Ray, ECG, ECHO, PFTs, perfusion lung scan, cardiac catheterization, blood test, and others. The ECHO (Echocardiography) segment dominated the market with the largest market revenue share in 2024, driven by its non-invasive nature, accuracy in detecting pulmonary arterial pressure, and widespread use in routine screening. ECHO allows clinicians to monitor disease progression, assess right heart function, and tailor therapy accordingly. Its availability in hospitals and specialty clinics, combined with cost-effectiveness relative to invasive procedures, makes it the preferred diagnostic tool. The ability to integrate ECHO findings with other clinical assessments enhances patient management and facilitates early treatment intervention. Continuous technological advancements in imaging resolution and portability further solidify ECHO’s dominant position. Clinicians and patients asuch as favor ECHO due to its reliability, efficiency, and minimal risk during repeated examinations.

The Cardiac Catheterization segment is expected to witness the fastest growth from 2025 to 2032 due to its high diagnostic precision and role as a gold standard for confirming PPH diagnosis. It allows direct measurement of pulmonary artery pressure, providing critical data for treatment planning. Increasing awareness of early invasive diagnostics and the expansion of advanced cardiac care facilities are driving the adoption of this segment. The growing number of specialized cardiac centers and increasing insurance coverage for invasive diagnostics further contribute to market growth. Technological improvements in catheterization procedures are enhancing safety and patient comfort. Overall, rising clinical preference and demand for accurate hemodynamic assessment support its rapid expansion.

- By Treatment

On the basis of treatment, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into medication, oxygen therapy, and others. The Medication segment dominated the market with a 42.8% share in 2024, driven by its ability to improve patient survival, reduce symptoms, and enhance quality of life. Targeted drug therapies such as endothelin receptor antagonists, phosphodiesterase-5 inhibitors, and prostacyclin analogs are widely prescribed and have become the cornerstone of PPH management. The availability of branded options and adoption across hospitals, specialty clinics, and home healthcare settings reinforces its dominance. Consistent clinical outcomes and guideline recommendations favoring pharmacological interventions contribute to market leadership. Increased patient adherence to oral medications further strengthens this segment. Long-term studies demonstrating reduced hospitalization rates support sustained demand for drug therapy.

The Oxygen Therapy segment is anticipated to witness the fastest growth during 2025–2032, fueled by its role in alleviating hypoxemia and improving exercise tolerance. Increasing adoption in both hospital and home healthcare settings, combined with rising awareness of long-term benefits for PPH patients, is accelerating market expansion. Portable oxygen delivery systems and telehealth monitoring integration further support its adoption. In addition, patient preference for home-based treatment and growing physician recommendation for supplemental oxygen contribute to segment growth. Expanding insurance coverage and government programs in key regions are also driving adoption.

- By Drug Type

On the basis of drug type, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into branded and generics. The Branded segment dominated the market in 2024, driven by established medications with proven efficacy, strong clinical evidence, and clinician preference. Brand loyalty, marketing efforts by pharmaceutical companies, and regulatory approvals also contribute to sustained market dominance. Branded drugs often provide additional support programs, including patient education and adherence tracking, enhancing adoption. Hospitals and specialty clinics prefer branded drugs for their predictable therapeutic outcomes. Continuous innovation and new product launches in the branded segment strengthen its position. The confidence of prescribers in branded therapies further reinforces demand.

The Generics segment is expected to witness the fastest growth due to increasing healthcare cost sensitivity and the availability of high-quality generic alternatives. Expansion in emerging economies and government initiatives to improve affordability are key drivers for growth. Generics adoption is supported by clinician acceptance, patient affordability, and wider availability. Rising patent expirations of branded drugs provide opportunities for generic market entry. Healthcare systems promoting cost-effective therapies also boost this segment.

- By Population

On the basis of population, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into adults, paediatrics, and neonates. The Adults segment dominated the market in 2024, owing to the higher prevalence of PPH among adult patients and a well-established treatment protocol. Adults represent the largest patient pool for diagnosis, pharmacological intervention, and long-term disease management. The availability of adult-specific therapies and clinical trials further strengthens this segment. Adults benefit from comprehensive treatment plans combining medications, monitoring, and lifestyle management. Hospitals and specialty clinics are more equipped to manage adult cases, supporting continued dominance. Rising awareness and early diagnosis in adult populations sustain market leadership.

The Paediatrics segment is anticipated to witness the fastest growth during 2025–2032 due to increasing detection of congenital and idiopathic PPH in children, coupled with advancements in pediatric-specific therapies and diagnostic tools. Rising awareness among pediatricians and caregivers contributes to early intervention and adoption of treatments. Pediatric formulations, weight-based dosing, and child-friendly delivery methods are driving demand. Growth in specialized pediatric cardiology centers supports this segment. Increased government and NGO initiatives for pediatric care further accelerate expansion.

- By Route of Administration

On the basis of route of administration, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into oral, parenteral, and others. The Oral segment dominated the market with the largest revenue share in 2024, driven by convenience, ease of administration, and better patient adherence. Oral therapies are widely preferred in both outpatient and home healthcare settings, making them the cornerstone of long-term PPH management. Clinicians often recommend oral medications for stable patients due to the simplicity of dosing and monitoring. Patient compliance is higher with oral drugs, ensuring sustained therapeutic outcomes. Oral formulations are available in a wide range of dosages, supporting personalization of therapy. Long-term safety and ease of access in pharmacies reinforce dominance.

The Parenteral segment is expected to witness the fastest growth from 2025 to 2032, fueled by the increasing use of intravenous or subcutaneous prostacyclin analogs in severe PPH cases. Rising availability of portable infusion pumps and patient training programs support adoption in hospital and home care settings. Parenteral administration is critical for advanced-stage patients requiring continuous therapy. Advances in pump technology improve safety and mobility. Increased awareness of efficacy in severe cases drives adoption. Healthcare provider recommendation and insurance coverage further boost segment growth.

- By End-Users

On the basis of end-users, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into hospitals, specialty clinics, home healthcare, and others. The Hospitals segment dominated the market in 2024, driven by the availability of comprehensive diagnostic and treatment facilities, trained specialists, and multidisciplinary care teams. Hospitals serve as the primary point of care for newly diagnosed patients and those requiring complex interventions. Access to advanced imaging and treatment technologies further reinforces their dominance. Hospitals manage both acute and chronic cases, providing integrated care. Strong collaborations with pharmaceutical companies and clinical trial participation support growth. Institutional preference for hospital-based treatment ensures continued market leadership.

The Home Healthcare segment is anticipated to witness the fastest growth during 2025–2032 due to rising adoption of home-based oxygen therapy, telemedicine monitoring, and remote drug administration. Increasing patient preference for home care, particularly in chronic and long-term management, is boosting this segment. Portable oxygen and infusion devices facilitate effective at-home treatment. Telehealth integration allows physicians to monitor patient progress remotely. Rising insurance reimbursement for home care services supports adoption. Patient comfort and convenience drive accelerated growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the Primary Pulmonary Hypertension (PPH) treatment market is segmented into direct tender, hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated the market in 2024, driven by direct supply to hospitals, ease of access for patients during hospitalization, and integration with hospital formularies. Hospital pharmacies ensure proper storage, dispensing, and monitoring of PPH medications, strengthening their market position. Hospitals prefer in-house pharmacies for critical and specialty drugs. Coordinated inventory management supports consistent treatment availability. Clinical staff trust hospital pharmacy supplies for quality assurance. Continued hospital investment in pharmacy infrastructure ensures sustained dominance.

The Online Pharmacy segment is expected to witness the fastest growth from 2025 to 2032 due to the rising trend of e-pharmacies, convenience of home delivery, and increasing digital literacy. Growing patient preference for online purchases, coupled with insurance reimbursements, is accelerating adoption in both developed and emerging markets. Online platforms offer accessibility for patients in remote areas. Discounts, subscription services, and doorstep delivery enhance appeal. Integration with telemedicine platforms supports seamless medication management. Expanding smartphone penetration and internet connectivity drive rapid growth in this channel.

Primary Pulmonary Hypertension (PPH) Treatment Market Regional Analysis

- North America dominated the Primary Pulmonary Hypertension (PPH) treatment market with the largest revenue share of 39.6% in 2024, characterized by early adoption of innovative therapies, high healthcare expenditure, and strong presence of leading pharmaceutical companies

- Patients and healthcare providers in the region highly value access to innovative medications, comprehensive diagnostic tools, and specialized care centers for effective disease management and improved clinical outcomes

- This widespread adoption is further supported by high healthcare expenditure, strong presence of key pharmaceutical players, and supportive reimbursement policies, establishing North America as a leading region in the PPH treatment market

U.S. Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The U.S. Primary Pulmonary Hypertension (PPH) treatment market captured the largest revenue share of 36% in 2024 within North America, fueled by the early adoption of advanced therapies and well-established healthcare infrastructure. Patients and healthcare providers increasingly prioritize access to innovative medications, comprehensive diagnostic tools, and specialized care centers for effective disease management. The growing prevalence of pulmonary arterial hypertension, combined with supportive reimbursement policies and high healthcare expenditure, further propels the market. In addition, initiatives for early diagnosis, patient education, and clinical research programs are expanding treatment access. The U.S. market also benefits from strong pharmaceutical presence and ongoing drug development activities, sustaining continued growth.

Europe Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The Europe Primary Pulmonary Hypertension (PPH) treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of pulmonary hypertension and growing healthcare investments. Rising urbanization and the availability of advanced diagnostic and therapeutic options are fostering market adoption. European healthcare systems emphasize early diagnosis and guideline-based treatment, enhancing access to medications and oxygen therapy. Government initiatives and reimbursement programs support patient affordability and treatment adherence. The market is experiencing significant growth across hospitals, specialty clinics, and home healthcare settings, with new therapies being incorporated into both established and emerging healthcare facilities.

U.K. Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The U.K. Primary Pulmonary Hypertension (PPH) treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by heightened awareness of pulmonary hypertension and the demand for effective disease management solutions. Concerns regarding patient morbidity and mortality are encouraging both hospitals and specialty clinics to adopt guideline-based therapies. The U.K.’s well-developed healthcare infrastructure, alongside robust access to diagnostic tools and medications, is expected to continue stimulating market growth. In addition, government programs and patient support initiatives facilitate early intervention and adherence to treatment protocols. Increasing participation in clinical trials and the availability of innovative drugs further contribute to market expansion.

Germany Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The Germany Primary Pulmonary Hypertension (PPH) treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by rising prevalence of pulmonary arterial hypertension and growing emphasis on advanced treatment options. Germany’s well-developed healthcare system, coupled with a strong focus on clinical research and innovation, promotes adoption of both pharmacological therapies and oxygen therapy. Hospitals and specialty clinics are increasingly equipped with state-of-the-art diagnostic tools, improving disease detection and management. Patient awareness campaigns and reimbursement support further enhance market penetration. Integration of telemedicine and home healthcare solutions is also becoming increasingly prevalent. Consumers show strong preference for effective, guideline-compliant treatment regimens.

Asia-Pacific Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The Asia-Pacific Primary Pulmonary Hypertension (PPH) treatment market is poised to grow at the fastest CAGR of 11.8% during the forecast period of 2025 to 2032, driven by increasing diagnosis rates, improving healthcare infrastructure, and rising disposable incomes in countries such as China, Japan, and India. Government initiatives to enhance rare disease care and awareness campaigns are driving adoption of treatments. Expansion of hospitals, specialty clinics, and home healthcare services is improving access to advanced medications and oxygen therapy. Technological advancements in diagnostics, alongside telemedicine integration, support efficient disease management. In addition, growing awareness among healthcare professionals and patients is accelerating early diagnosis and treatment uptake. Market growth is also supported by the increasing availability of both branded and generic therapies.

Japan Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The Japan Primary Pulmonary Hypertension (PPH) treatment market is gaining momentum due to the country’s well-established healthcare system, rising prevalence of pulmonary arterial hypertension, and demand for improved disease management. Early diagnosis and availability of specialized therapies are driving adoption in both adult and pediatric populations. Hospitals and specialty clinics are integrating advanced diagnostic and monitoring technologies, improving patient outcomes. Telemedicine and home healthcare services are increasingly facilitating continuous care for chronic patients. Government support for rare disease treatments and reimbursement policies further enhance access. In addition, Japan’s aging population is expected to spur demand for long-term care and effective treatment solutions in residential and clinical settings.

India Primary Pulmonary Hypertension (PPH) Treatment Market Insight

The India Primary Pulmonary Hypertension (PPH) treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s growing healthcare infrastructure, increasing patient awareness, and rising prevalence of pulmonary arterial hypertension. India represents a rapidly expanding market for PPH treatments across hospitals, specialty clinics, and home healthcare services. Government initiatives for rare disease management, coupled with rising health insurance penetration, are facilitating access to medications and oxygen therapy. Affordable generic options and domestic pharmaceutical manufacturers further support market growth. Expansion of diagnostic facilities and telemedicine programs is improving early detection and treatment uptake. Strong focus on patient education and disease management programs is driving increased adoption in both urban and semi-urban regions.

Primary Pulmonary Hypertension (PPH) Treatment Market Share

The Primary Pulmonary Hypertension (PPH) Treatment industry is primarily led by well-established companies, including:

- United Therapeutics Corporation (U.S.)

- Johnson & Johnson and its affiliates. (U.S.)

- Bayer AG (Germany)

- Gilead Sciences, Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- GSK plc (U.K.)

- AstraZeneca (U.K.)

- Sun Pharmaceutical Industries Ltd. (India)

- Arena Pharmaceuticals, Inc. (U.S.)

- PhaseBio Pharmaceuticals, Inc. (U.S.)

- Liquidia Technologies, Inc. (U.S.)

- Gossamer Bio, Inc. (U.S.)

- Aerami Therapeutics, Inc. (U.S.)

- Acceleron Pharma, Inc. (U.S.)

- Chiesi Farmaceutici S.p.A. (Italy)

- Roivant Sciences Ltd. (Switzerland)

- Recursion Pharmaceuticals, Inc. (U.S.)

What are the Recent Developments in Global Primary Pulmonary Hypertension (PPH) Treatment Market?

- In June 2025, Insmed announced positive topline results from a Phase 2b study of TPIP as a once-daily therapy in patients with PAH. The company plans to initiate a Phase 3 trial in patients with PAH in early 2026, based on these encouraging results

- In May 2025, the U.S. Food and Drug Administration (FDA) approved YUTREPIA (treprostinil) inhalation powder for adults with pulmonary arterial hypertension (PAH) and pulmonary hypertension associated with interstitial lung disease. This approval marks a significant advancement in the treatment options available for these conditions

- In May 2025, a study found that sotatercept, a relatively new therapy, was effective at preventing death in patients with more advanced stages of PAH. Initially approved for those with mild to moderate disease, sotatercept's efficacy in advanced stages offers new hope for patients with severe PAH

- In March 2025, results from the ZENITH trial were presented, showing that treatment with sotatercept resulted in a lower risk of all-cause death, lung transplantation, and hospitalization for worsening PAH compared to placebo in high-risk adults with PAH on maximum tolerated background therapy. This trial underscores the potential of sotatercept in improving outcomes for patients with advanced disease

- In December 2024, the U.S. Food and Drug Administration (FDA) approved Opsynvi, the first and only once-daily combination pill of macitentan and tadalafil for the treatment of PAH. This approval provides a convenient oral therapy option for patients with functional class II and III PAH

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.