Global Processor Ip Market

Market Size in USD Billion

USD

7.40 Billion

USD

12.02 Billion

2024

2032

USD

7.40 Billion

USD

12.02 Billion

2024

2032

| 2025 - 2032 | |

| USD 7.40 Billion | |

| USD 12.02 Billion | |

| % | |

|

What is the Global Processor IP Market Size and Growth Rate?

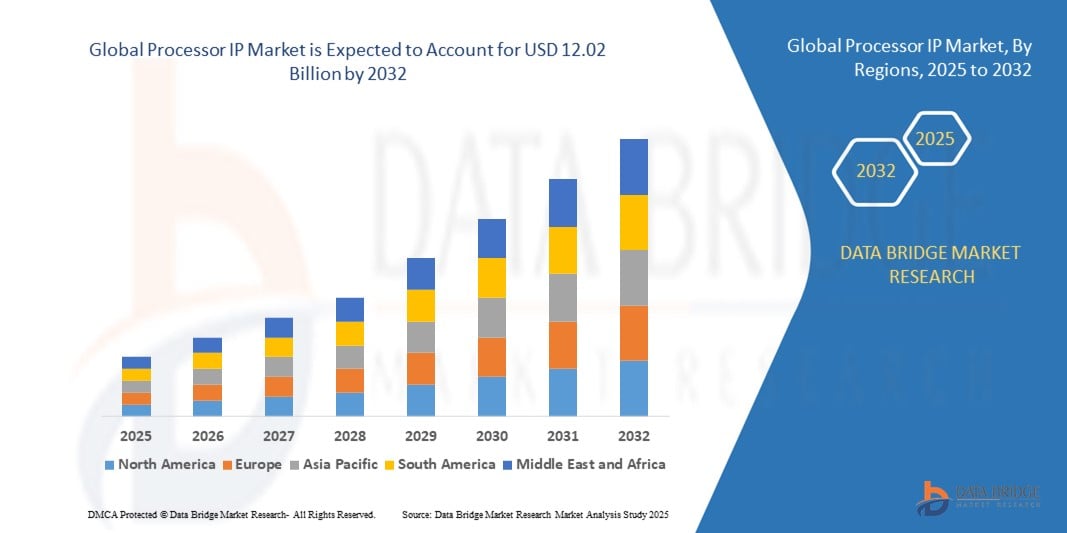

- The global processor IP market size was valued at USD 7.40 billion in 2024 and is expected to reach USD 12.02 billion by 2032, at a CAGR of 6.25% during the forecast period

- Processor IP (Intellectual Property) refers to pre-designed and reusable processor cores, including CPUs and GPUs, licensed for integration into custom System-on-Chip (SoC) designs. These cores are often customizable to meet specific performance, power, and area requirements of various applications. Processor IP enables semiconductor companies to accelerate chip development by leveraging proven and optimized designs, reducing time-to-market and development costs

- Licensing processor IP allows companies to focus on differentiating features while relying on established processor architectures for core functionality. It facilitates the creation of diverse embedded systems, from mobile devices to automotive applications, by providing scalable and efficient computing solutions. In essence, processor IP serves as a foundational component for building complex integrated circuits, driving innovation across various industries

What are the Major Takeaways of Processor IP Market?

- The increasing need for powerful processors to support HPC applications such as AI, big data analytics, and scientific simulations is driving the demand for advanced Processor IP. These applications require efficient and scalable processing solutions, spurring innovation and growth in the market

- The proliferation of IoT devices and the demand for real-time data processing at the edge are driving the global processor IP market. Edge computing requires processors that can deliver high performance within power and space constraints, leading to the adoption of customizable and power-efficient processor IP solutions

- Asia-Pacific dominated the processor IP market with the largest revenue share of 41.6% in 2024, driven by the region’s strong semiconductor manufacturing base, rapid adoption of connected devices, and expanding electronics industry

- North America Processor IP market is poised to grow at the fastest CAGR of 8.3% during 2025 to 2032, driven by advancements in AI, autonomous vehicles, and high-performance computing

- The CPU SIP segment dominated the processor IP market with the largest market revenue share of 28.4% in 2024, driven by its central role in processing functions across a wide range of applications from consumer electronics to automotive systems

Report Scope and Processor IP Market Segmentation

|

Attributes |

Processor IP Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Processor IP Market?

Enhanced Performance through AI-Driven Architecture and Heterogeneous Computing

- A major and fast-evolving trend in the global Processor IP market is the increasing adoption of AI-optimized designs and heterogeneous computing architectures, enabling processors to handle complex workloads with greater efficiency and speed

- For instance, Arm’s Ethos AI processors are purpose-built to accelerate machine learning tasks, while Synopsys DesignWare ARC Processors integrate specialized DSP and neural network capabilities, allowing AI workloads to run directly on edge devices without relying on the cloud

- AI-enabled Processor IPs are now capable of predictive workload management, optimizing resource allocation, and reducing latency for real-time applications such as autonomous driving, industrial automation, and advanced data analytics. Some solutions integrate AI to monitor chip performance and proactively adjust power usage, extending battery life in portable devices

- The combination of AI acceleration with heterogeneous computing—pairing CPUs, GPUs, NPUs, and domain-specific accelerators—allows for faster parallel processing, improving performance in applications such as 5G base stations, smart cameras, and IoT gateways

- This convergence is pushing processor IP beyond traditional performance boundaries, driving demand from sectors such as automotive, consumer electronics, and edge AI devices. Companies such as Cadence and Intel are developing processor IPs that integrate AI capabilities with advanced interconnects, enabling higher throughput and lower power consumption

- The demand for AI-driven, heterogeneous Processor IP solutions is growing rapidly as industries prioritize faster computing, lower energy use, and the ability to run AI workloads directly on-device for enhanced security and responsiveness

What are the Key Drivers of Processor IP Market?

- The rapid expansion of AI, IoT, and 5G applications, combined with the need for high-performance, low-power processing, is a primary driver for the Processor IP market

- For instance, in March 2024, Synopsys announced the expansion of its ARC Processor IP portfolio to support emerging AIoT workloads, offering enhanced energy efficiency and advanced security features, positioning itself to meet growing demand in consumer and industrial markets

- As industries adopt more data-intensive applications, Processor IPs offer customizable architectures, domain-specific acceleration, and built-in security, making them indispensable for next-generation chip designs

- The growing adoption of edge computing is further boosting demand, as processor IP enables AI inference, real-time analytics, and low-latency processing close to the source of data

- Customization flexibility, reduced time-to-market through pre-verified cores, and the scalability to support applications from wearable devices to data centers are key factors accelerating adoption. The rising demand for semiconductor innovation in autonomous vehicles, AR/VR, and connected healthcare devices further strengthens market growth

Which Factor is challenging the Growth of the Processor IP Market?

- The rising complexity of chip design, along with escalating development costs and verification challenges, poses a significant hurdle for market growth. As Processor IP becomes more specialized and performance-intensive, the effort and cost to integrate, validate, and secure these cores increases substantially

- For instance, delays in design cycles or unexpected integration issues can significantly impact time-to-market for semiconductor companies, especially in competitive consumer electronics segments

- In addition, concerns over IP security and potential infringements add another layer of risk, prompting companies to invest heavily in legal protections and secure design processes

- The shortage of skilled semiconductor design engineers also acts as a bottleneck, slowing innovation and scaling efforts for some companies

- High licensing fees for advanced Processor IP, particularly for leading-edge nodes, can be prohibitive for startups and smaller fabless semiconductor firms, potentially limiting their competitiveness against larger players

- Overcoming these challenges will require improved EDA tool automation, increased collaboration between IP vendors and foundries, and the development of cost-effective licensing models that allow broader adoption without compromising profitability

How is the Processor IP Market Segmented?

The market is segmented on the basis of type, form, IP source, channel, and end-user.

- By Type

On the basis of type, the processor IP market is segmented into CPU SIP, Wired SIP, GPU SIP, Memory SIP, DSP SIP, Library SIP, Infrastructure SIP, Digital SIP, Analog SIP, Wireless SIP, and Others. The CPU SIP segment dominated the processor IP market with the largest market revenue share of 28.4% in 2024, driven by its central role in processing functions across a wide range of applications from consumer electronics to automotive systems. CPU SIPs remain highly demanded due to their scalability, performance efficiency, and compatibility with various system architectures.

The GPU SIP segment is anticipated to witness the fastest growth rate of 19.6% from 2025 to 2032, fueled by increasing use in AI, gaming, and high-performance computing. GPU SIPs deliver exceptional parallel processing power, making them essential for graphics-intensive and AI-driven workloads.

- By Form

On the basis of form, the processor IP market is segmented into soft form and hard form. The soft form segment held the largest market revenue share of 57.1% in 2024, driven by its design flexibility, portability across different foundries, and ability to be customized for various applications. Soft form IPs enable faster design cycles and cost-effective integration into diverse SoCs.

The hard form segment is expected to witness the fastest CAGR from 2025 to 2032, driven by its proven silicon performance, reduced design risk, and suitability for high-volume manufacturing where fixed specifications are preferred.

- By IP Source

On the basis of IP source, the processor IP market is segmented into licensing and royalty. The licensing segment dominated the market with the largest market revenue share of 61.3% in 2024, driven by the increasing preference of companies to acquire ready-to-use IP blocks to accelerate time-to-market while reducing in-house design complexities. Licensing allows for predictable cost structures and rapid product development.

The royalty segment is expected to witness the fastest CAGR from 2025 to 2032, supported by the growing number of long-term contracts where IP providers receive ongoing payments based on production volumes.

- By Channel

On the basis of channel, the processor IP market is segmented into direct sources and internet catalogue. The direct sources segment accounted for the largest market revenue share of 64.8% in 2024, driven by established vendor-client relationships, customized support, and integration assistance offered by IP providers.

The internet catalogue segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing adoption of online platforms that offer faster access to a variety of IPs and simplified purchasing processes.

- By End-User

On the basis of end-user, the processor IP market is segmented into automotive, telecom, consumer electronics, industrial, defense, commercial, medical, and others. The consumer electronics segment dominated the market with the largest market revenue share of 35.6% in 2024, driven by the proliferation of smartphones, wearables, and connected devices that demand high-performance and energy-efficient processor architectures.

The automotive segment is expected to witness the fastest CAGR from 2025 to 2032, supported by advancements in autonomous driving systems, in-vehicle infotainment, and electric vehicle technologies requiring robust and reliable Processor IP solutions.

Which Region Holds the Largest Share of the Processor IP Market?

- Asia-Pacific dominated the processor IP market with the largest revenue share of 41.6% in 2024, driven by the region’s strong semiconductor manufacturing base, rapid adoption of connected devices, and expanding electronics industry

- Countries in the region benefit from robust supply chains, cost-effective production, and increasing integration of advanced processor architectures in consumer electronics, automotive, and industrial applications

- Rising investments in R&D, government initiatives promoting digital transformation, and the availability of skilled engineering talent further strengthen APAC’s leadership in the global Processor IP market

China Processor IP Market Insight

The China processor IP market captured the largest revenue share of 46.8% in 2024 within Asia-Pacific, supported by the country’s position as a global manufacturing hub for semiconductors and electronics. China’s rapid urbanization, 5G rollout, and large consumer base are driving adoption across smartphones, IoT devices, and automotive systems. Local innovation, combined with strong domestic IP providers, is enabling competitive pricing and faster time-to-market.

Japan Processor IP Market Insight

The Japan processor IP market is gaining traction due to its focus on high-performance, energy-efficient semiconductor solutions. The nation’s strong automotive and electronics industries are leading adopters of advanced Processor IP, particularly for ADAS, infotainment systems, and robotics. Continuous innovation in AI and IoT integration, alongside the government’s push for smart infrastructure, supports steady market growth.

India Processor IP Market Insight

The India processor IP market is expanding rapidly, driven by the government’s “Digital India” initiative, increasing semiconductor design activity, and rising demand for consumer electronics and automotive applications. India’s growing base of fabless semiconductor companies, coupled with international partnerships, is fostering adoption of licensed and royalty-based IP models.

Which Region is the Fastest Growing Region in the Processor IP Market?

North America processor IP market is poised to grow at the fastest CAGR of 8.3% during 2025 to 2032, driven by advancements in AI, autonomous vehicles, and high-performance computing. The region’s strong presence of leading semiconductor IP vendors, coupled with significant investments in chip design for data centers, telecom, and defense applications, is accelerating growth.

U.S. Processor IP Market Insight

The U.S. processor IP market accounted for the largest revenue share of 79.5% in 2024 within North America, supported by robust R&D capabilities, a thriving startup ecosystem, and government-backed initiatives in semiconductor self-reliance. Growing demand for IPs in AI accelerators, 5G infrastructure, and aerospace applications is boosting market potential.

Canada Processor IP Market Insight

The Canada processor IP market is experiencing steady growth, fueled by emerging semiconductor design hubs, university-industry collaborations, and adoption in automotive and industrial IoT sectors. Strategic partnerships with global IP providers are enabling Canadian companies to enter competitive markets with innovative, application-specific processor designs.

Which are the Top Companies in Processor IP Market?

The processor IP industry is primarily led by well-established companies, including:

- Avery Design Systems (U.S.)

- Intel Corporation (U.S.)

- Arm Limited (U.K.)

- Cadence Design Systems, Inc. (U.S.)

- CAST (U.S.)

- Ceva, Inc. (U.S.)

- eSilicon Corporation (U.S.)

- Imagination Technologies (U.K.)

- Kilopass Technology Inc. (U.S.)

- Open-Silicon, Inc. (U.S.)

- Rambus.com (U.S.)

- Stäubli International AG (Switzerland)

- Synopsys, Inc. (U.S.)

What are the Recent Developments in Global Processor IP Market?

- In June 2024, Clarivate Plc introduced the IP Collaboration Hub, aimed at improving efficiency and reducing risks in IP filing and prosecution. Integrated with its IP management systems, the solution automates communication with local agents, streamlining both patent and trademark processes. This initiative aligns with Clarivate’s strategy to enhance IP lifecycle support, ultimately benefiting industries such as Semiconductor Intellectual Property (IP) by fostering better collaboration and minimizing errors, reinforcing its market position

- In March 2024, Synopsys announced the acquisition of Intrinsic ID, a global leader in Physical Unclonable Function (PUF) IP for system-on-chips (SoCs). The acquisition expands Synopsys’ semiconductor IP portfolio, enabling secure SoC designs with unique identifiers. By incorporating PUF technology, Synopsys advances its leadership in delivering cutting-edge semiconductor IP solutions, supporting innovation across smart and connected devices, strengthening its competitive edge

- In August 2023, Intel and Synopsys broadened their partnership to create a robust portfolio of Semiconductor Intellectual Property (IP) on Intel’s advanced process nodes, Intel 3 and Intel 18A. This collaboration boosts Intel Foundry Services (IFS) by accelerating IP availability for SoC designs and improving performance. The agreement supports Intel’s IDM 2.0 strategy to reinforce technology leadership and foundry capabilities, cementing both companies’ influence in the semiconductor industry

- In May 2022, Faraday Technology Corporation launched Soteria's advanced security IP subsystems, offering custom SoC designs that provide hardware security for a variety of IoT applications. Faraday also delivers multiple security solutions, including IP security system software for secure SoC development. This launch strengthens Faraday’s position in the security-focused semiconductor market

- In June 2021, Sondrel introduced a quad-channel IP platform designed for ISO-26262 applications. This IP reference platform simplifies the design and architecture of semiconductor components, enhancing development efficiency and ensuring safety compliance, thereby supporting Sondrel’s reputation for innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.