Global Professional Diagnostics Market

Market Size in USD Billion

USD

45.00 Billion

USD

75.60 Billion

2025

2033

USD

45.00 Billion

USD

75.60 Billion

2025

2033

| 2026 - 2033 | |

| USD 45.00 Billion | |

| USD 75.60 Billion | |

| % | |

|

Professional Diagnostics Market Size

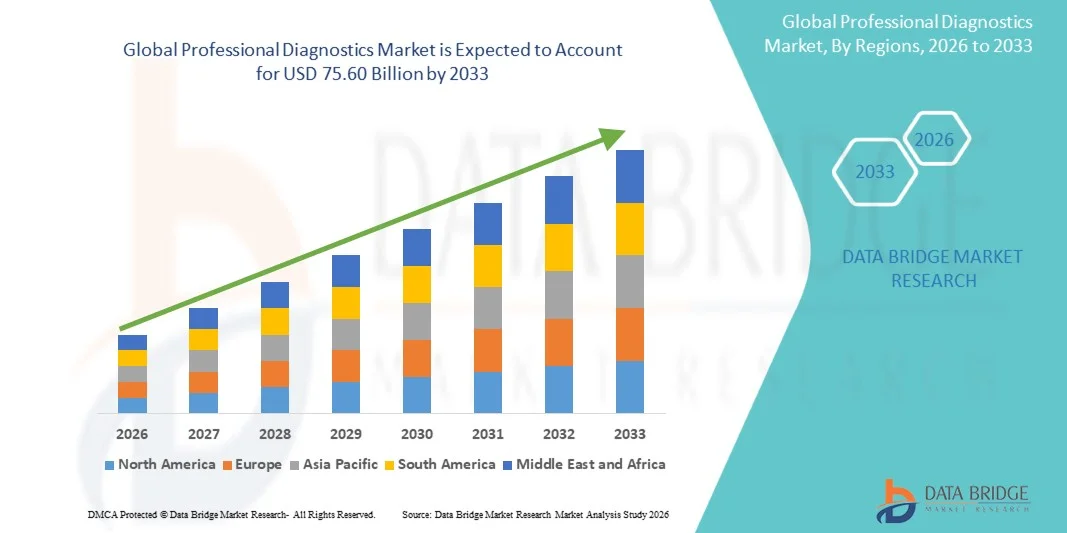

- The global professional diagnostics market size was valued at USD 45.00 billion in 2025 and is expected to reach USD 75.60 billion by 2033, at a CAGR of 6.70% during the forecast period

- The market growth is largely fueled by the growing prevalence of chronic and infectious diseases, continuous technological advancements in diagnostic tools (including molecular and point‑of‑care diagnostics), and expanding healthcare infrastructure worldwide, which together drive higher demand for accurate, early disease detection

- Furthermore, rising health awareness, increased healthcare spending, and a shift toward preventive and personalized medicine are boosting the uptake of professional diagnostic solutions across clinical laboratories, hospitals, and healthcare facilities, positioning diagnostics as a critical component of modern healthcare delivery and significantly contributing to market expansion

Professional Diagnostics Market Analysis

- Professional diagnostics, encompassing immunochemistry, clinical microbiology, point-of-care tests (POCT), hematology, and haemostasis, are increasingly vital components of modern healthcare systems in hospitals and diagnostic centers due to their critical role in early disease detection, accurate diagnosis, and treatment monitoring

- The escalating demand for professional diagnostics is primarily fueled by the growing prevalence of chronic and infectious diseases, technological advancements in diagnostic tools, and a rising focus on preventive and personalized medicine

- North America dominated the professional diagnostics market with the largest revenue share of 40.00% in 2025, driven by advanced healthcare infrastructure, high healthcare expenditure, early adoption of innovative diagnostic technologies, and a strong presence of key market players, with the U.S. witnessing substantial growth in hospital and diagnostic center testing, supported by innovations in immunochemistry and point-of-care solutions

- Asia-Pacific is expected to be the fastest-growing region in the professional diagnostics market during the forecast period due to increasing healthcare investments, expanding hospital networks, rising health awareness, and growing demand for accessible diagnostics, particularly in clinical microbiology and POCT applications

- The immunochemistry segment dominated the professional diagnostics market with the largest market share of 43.2% in 2025, driven by its wide application in disease detection, treatment monitoring, and biomarker testing

Report Scope and Professional Diagnostics Market Segmentation

|

Attributes |

Professional Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Professional Diagnostics Market Trends

“Advancements in AI-Enabled and Point-of-Care Testing”

- A significant and accelerating trend in the global professional diagnostics market is the integration of artificial intelligence (AI) with laboratory and point-of-care testing platforms, enhancing diagnostic accuracy, predictive capabilities, and workflow efficiency

- For instance, AI-powered hematology analyzers can automatically flag abnormal cell populations, while POCT devices such as Abbott i-STAT enable rapid bedside testing, allowing clinicians to make faster and more informed decisions

- AI integration in diagnostics enables features such as predictive disease modeling, automated anomaly detection, and intelligent result interpretation, reducing human error and improving patient outcomes. For instance, some immunochemistry platforms utilize AI to optimize assay calibration and suggest actionable insights based on patient history

- The seamless integration of diagnostics with electronic health records (EHRs) and hospital information systems facilitates centralized monitoring and analysis of patient data, enabling clinicians to manage multiple test results and patient profiles from a single interface

- This trend toward more intelligent, rapid, and interconnected diagnostic systems is fundamentally reshaping clinical expectations for healthcare delivery. For instance, companies such as Roche Diagnostics are developing AI-enabled platforms that integrate laboratory testing with clinical decision support systems

- The demand for professional diagnostic solutions that combine AI, point-of-care accessibility, and predictive analytics is growing rapidly across hospitals and diagnostic centers, as healthcare providers increasingly prioritize precision, efficiency, and timely disease management

- Increasing focus on personalized and genomics-based diagnostics is driving innovation in professional diagnostic tools. For instance, AI-driven molecular assays are being used to tailor treatment plans based on individual genetic profiles

Professional Diagnostics Market Dynamics

Driver

“Rising Prevalence of Chronic and Infectious Diseases”

- The increasing incidence of chronic illnesses, infectious diseases, and lifestyle-related disorders is a significant driver for the heightened demand for professional diagnostics

- For instance, in 2025, Siemens Healthineers reported increased adoption of their immunochemistry and POCT solutions in hospitals responding to growing chronic disease burdens

- As healthcare systems focus on early detection and preventive care, diagnostic testing offers critical insights for timely interventions, improving patient outcomes and reducing treatment costs

- Furthermore, the expansion of hospital networks and diagnostic centers, combined with rising health awareness, is making professional diagnostics an essential component of routine care

- For instance, adoption of point-of-care hematology and clinical microbiology tests has accelerated in outpatient and emergency settings due to convenience, speed, and accuracy

- The growing emphasis on personalized medicine, evidence-based treatment, and rapid diagnostics continues to drive the adoption of advanced immunochemistry, POCT, and hematology solutions across both hospital and diagnostic center settings

- Rising government initiatives and healthcare funding for preventive care and infectious disease control are further driving market growth. For instance, public health programs are increasing access to rapid diagnostic testing in community clinics

- Increasing collaborations and partnerships between diagnostics companies and healthcare providers are accelerating adoption of integrated solutions. For instance, joint ventures for AI-driven diagnostics have enabled hospitals to deploy smarter testing workflows

Restraint/Challenge

“High Costs and Regulatory Compliance Hurdles”

- The relatively high cost of advanced diagnostic equipment and consumables can pose a barrier to widespread adoption, particularly in emerging markets or budget-conscious facilities

- For instance, high-end immunochemistry analyzers or molecular diagnostic platforms often require significant capital investment and maintenance, limiting their deployment in smaller hospitals

- In addition, stringent regulatory requirements, including FDA, CE, and ISO certifications, can delay product launches and increase compliance costs, affecting overall market growth

- For instance, delays in approval for new POCT assays or clinical microbiology kits have occasionally slowed market entry for innovative products

- Addressing these challenges through cost-effective platform development, streamlined regulatory pathways, and increased awareness of the clinical value of diagnostics will be vital for sustained market expansion

- For instance, some companies are focusing on modular POCT solutions and scalable immunochemistry platforms to reduce upfront costs while ensuring compliance with global standards

- Limited skilled personnel to operate advanced diagnostic equipment is another market challenge. For instance, small diagnostic centers in developing regions face difficulties in recruiting trained lab technicians to manage complex assays

- Data privacy and cybersecurity concerns associated with connected diagnostic systems pose a barrier to adoption. For instance, electronic health record integration of AI-enabled devices requires stringent security protocols to protect patient information

Professional Diagnostics Market Scope

The market is segmented on the basis of product type and end users.

- By Product Type

On the basis of product type, the professional diagnostics market is segmented into immunochemistry, clinical microbiology, point-of-care tests (POCT), hematology, and haemostasis. The immunochemistry segment dominated the market with the largest revenue share of 43.2% in 2025, driven by its extensive applications in disease detection, biomarker monitoring, and treatment evaluation. Hospitals and diagnostic centers often prioritize immunochemistry analyzers due to their high throughput, accuracy, and ability to perform a wide range of assays on a single platform. The established reliability of immunochemistry solutions has made them a cornerstone of routine clinical diagnostics, particularly for chronic and infectious disease management. In addition, the segment benefits from continuous technological improvements, such as automated analyzers and multiplex testing capabilities. The compatibility of immunochemistry platforms with laboratory information systems further enhances operational efficiency, driving adoption in both large hospitals and specialized diagnostic centers. Strong demand in developed regions with advanced healthcare infrastructure continues to reinforce its dominant market position.

The point-of-care testing (POCT) segment is anticipated to witness the fastest growth rate during the forecast period from 2026 to 2033, fueled by the increasing need for rapid diagnostics and decentralized testing. POCT devices enable healthcare providers to obtain test results within minutes, supporting timely clinical decisions in emergency rooms, outpatient clinics, and home healthcare settings. The growing adoption of portable and handheld diagnostic devices, coupled with increasing patient awareness of preventive care, is accelerating POCT penetration. Technological innovations, such as smartphone-compatible analyzers and wireless connectivity, are further enhancing the convenience and accessibility of POCT solutions. In addition, the COVID-19 pandemic highlighted the critical role of rapid testing, driving adoption across both developed and emerging markets. The expansion of POCT into chronic disease monitoring and infectious disease screening positions it as a high-growth product segment.

- By End Users

On the basis of end users, the professional diagnostics market is segmented into hospitals, diagnostic centers, and others. The hospital segment dominated the market in 2025 with the largest revenue share, owing to its extensive patient base, advanced infrastructure, and in-house laboratory capabilities. Hospitals rely on professional diagnostic solutions for routine screening, disease monitoring, emergency diagnostics, and critical care decision-making. The ability to perform a wide range of tests in a single facility allows hospitals to maintain high operational efficiency while delivering accurate results quickly. Integration with electronic health records and automated laboratory systems further strengthens hospitals’ preference for advanced diagnostic platforms. Moreover, hospitals often adopt new technologies earlier than other end users due to higher budgets, skilled personnel, and the demand for comprehensive testing services. Continuous investments in modern laboratory equipment and automation ensure that hospitals remain the dominant end-user segment in the professional diagnostics market.

The diagnostic centers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing number of outpatient clinics, specialized diagnostic chains, and decentralized testing facilities. Diagnostic centers provide convenient access to professional testing without the need for hospital admission, making them attractive to patients seeking preventive health check-ups or routine monitoring. Rapid adoption of POCT and modular laboratory platforms allows diagnostic centers to expand service offerings efficiently. Rising awareness of early disease detection and preventive healthcare is also boosting demand for diagnostic services in urban and semi-urban regions. Partnerships with hospitals, corporate wellness programs, and telehealth platforms further accelerate the growth of diagnostic centers as key market players. The cost-effectiveness, flexibility, and patient-centric approach of diagnostic centers position them as a rapidly expanding segment in the market.

Professional Diagnostics Market Regional Analysis

- North America dominated the professional diagnostics market with the largest revenue share of 40.00% in 2025, driven by advanced healthcare infrastructure, high healthcare expenditure, early adoption of innovative diagnostic technologies, and a strong presence of key market players

- Healthcare providers in the region highly value the accuracy, speed, and reliability offered by professional diagnostic solutions, along with seamless integration into hospital information systems and electronic health records for efficient patient management

- This widespread adoption is further supported by high healthcare expenditure, strong presence of key industry players, skilled medical personnel, and increasing focus on preventive and personalized medicine, establishing professional diagnostics as a critical component of modern healthcare delivery across hospitals and diagnostic centers

U.S. Professional Diagnostics Market Insight

The U.S. professional diagnostics market captured the largest revenue share of 81% within North America in 2025, fueled by widespread adoption of advanced diagnostic technologies and the growing emphasis on early disease detection and preventive healthcare. Healthcare providers are increasingly prioritizing rapid, accurate, and point-of-care testing to improve patient outcomes and operational efficiency. The expansion of hospital networks, coupled with high healthcare expenditure and skilled medical personnel, further drives market growth. Moreover, the integration of AI-powered analyzers, molecular diagnostics, and laboratory automation solutions is significantly contributing to the market’s expansion. The U.S. market also benefits from strong collaborations between diagnostics companies and healthcare providers, enabling faster deployment of innovative solutions.

Europe Professional Diagnostics Market Insight

The Europe professional diagnostics market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory frameworks, rising public health initiatives, and growing awareness of preventive care. Increasing urbanization, coupled with the adoption of advanced diagnostic technologies, is fostering the market’s growth. European healthcare providers value the accuracy, reliability, and efficiency of professional diagnostic solutions. The region is experiencing significant growth across hospitals, diagnostic centers, and outpatient facilities, with immunochemistry and point-of-care testing being increasingly incorporated into routine clinical practice. Continuous technological innovation and government support for early disease detection are also boosting market adoption.

U.K. Professional Diagnostics Market Insight

The U.K. professional diagnostics market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on early disease detection, personalized medicine, and healthcare digitization. Rising concerns about chronic and infectious diseases are encouraging hospitals and diagnostic centers to adopt advanced diagnostic solutions. The U.K.’s well-established healthcare infrastructure, robust regulatory compliance, and high patient awareness are expected to continue stimulating market growth. Moreover, integration with electronic health records, AI-enabled analytics, and rapid point-of-care testing is enhancing workflow efficiency and decision-making in both residential healthcare and commercial diagnostic networks.

Germany Professional Diagnostics Market Insight

The Germany professional diagnostics market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing investment in healthcare infrastructure, awareness of preventive care, and adoption of technologically advanced diagnostic tools. Germany’s emphasis on innovation and quality healthcare services promotes the use of immunochemistry, hematology, and point-of-care testing solutions in hospitals and diagnostic centers. The integration of diagnostic platforms with hospital information systems and AI-based decision support is becoming increasingly prevalent. Strong local manufacturing capabilities, combined with a preference for precise, reliable, and sustainable diagnostic solutions, further drive market growth.

Asia-Pacific Professional Diagnostics Market Insight

The Asia-Pacific professional diagnostics market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare spending, rapid urbanization, and rising health awareness in countries such as China, India, and Japan. Expanding hospital and diagnostic center networks are supporting adoption of point-of-care and molecular diagnostic solutions. Government initiatives promoting digital health and preventive care are further accelerating market growth. In addition, Asia-Pacific is emerging as a manufacturing and innovation hub for diagnostic devices, increasing affordability and accessibility. Rapid technological adoption and growing middle-class populations contribute to the rising demand for professional diagnostic services across residential, clinical, and commercial healthcare settings.

Japan Professional Diagnostics Market Insight

The Japan professional diagnostics market is gaining momentum due to the country’s high-tech healthcare infrastructure, aging population, and demand for rapid, reliable testing. Hospitals and diagnostic centers increasingly adopt point-of-care and molecular diagnostic solutions to support timely clinical decision-making. Integration with electronic health records and IoT-enabled diagnostic platforms is enhancing workflow efficiency. The focus on preventive care, personalized medicine, and chronic disease management is further boosting adoption. Moreover, Japan’s emphasis on precision healthcare and quality assurance is encouraging continual investment in advanced immunochemistry and hematology solutions.

India Professional Diagnostics Market Insight

The India professional diagnostics market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising disposable incomes, and increasing healthcare awareness. Hospitals and diagnostic centers are expanding access to point-of-care and laboratory-based diagnostic solutions to meet growing patient demand. The country’s push toward smart cities, telemedicine integration, and government healthcare initiatives is propelling market growth. Affordable diagnostic platforms, combined with local manufacturing capabilities, make professional diagnostics more accessible across urban and semi-urban regions. The growing middle-class population, coupled with an increasing focus on early disease detection and preventive healthcare, is driving the adoption of professional diagnostic technologies across multiple healthcare settings.

Professional Diagnostics Market Share

The Professional Diagnostics industry is primarily led by well-established companies, including:

- F. Hoffmann La Roche Ltd. (Switzerland)

- Thermo Fisher Scientific Inc. (U.S.)

- Abbott (U.S.)

- Beckman Coulter, Inc. (U.S.)

- Danaher (U.S.)

- Siemens Healthineers AG (Germany)

- BIOMÉRIEUX (France)

- Sysmex Corporation (Japan)

- BD (U.S.)

- Cepheid (U.S.)

- Bio Rad Laboratories, Inc. (U.S.)

- Biocartis NV (Belgium)

- CellaVision AB (Sweden)

- ARKRAY, Inc. (Japan)

- Menarini Diagnostics (Italy)

- EKF Diagnostics Holdings plc (U.K.)

- Erba Mannheim GmbH (Germany)

- DiagCor Bioscience Incorporation Limited (Hong Kong)

- Drucker Diagnostics (U.S.)

- QuidelOrtho Corporation (U.S.)

What are the Recent Developments in Global Professional Diagnostics Market?

- In May 2025, the U.S. Food and Drug Administration (FDA) granted the first blood test clearance to aid Alzheimer’s disease diagnosis, significantly advancing clinical diagnostics by enabling a minimally invasive blood‑based assay that detects Alzheimer’s‑associated proteins beta‑amyloid and p‑tau217 with high accuracy, potentially expanding early detection and patient access compared to more invasive PET scans or spinal taps

- In April 2025, Molbio Diagnostics launched India’s first indigenously developed HPV test kits for cervical cancer screening, marking a major step in accessible cancer diagnostics with rapid point‑of‑care RT‑PCR testing for high‑risk HPV genotypes, validated by national research institutes and aligned with WHO cervical cancer elimination goal

- In December 2024, Roche announced the launch of its automated cobas® Mass Spec solution a groundbreaking mass spectrometry platform for routine clinical diagnostics offering more than 60 analytes for hormone, vitamin, drug monitoring, and abuse testing with CE mark approval, bringing high‑resolution mass spec into mainstream laboratories worldwide

- In September 2024, Roche launched the cobas® Respiratory flex test using novel TAGS PCR technology capable of detecting up to 12 respiratory viruses (including influenza and RSV) from a single sample, expanding multiplex pathogen detection and simplifying high‑throughput lab diagnosis

- In April 2024, Bio‑Rad Laboratories introduced the ddPLEX ESR1 Mutation Detection Kit an ultrasensitive multiplexed digital PCR assay for precise detection of seven key ESR1 mutations in breast cancer genomic research and clinical contexts, enhancing molecular oncology diagnostics

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.