Global Radiation Injury Drug Market

Market Size in USD Billion

USD

4.20 Billion

USD

6.59 Billion

2024

2032

USD

4.20 Billion

USD

6.59 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.20 Billion | |

| USD 6.59 Billion | |

| % | |

|

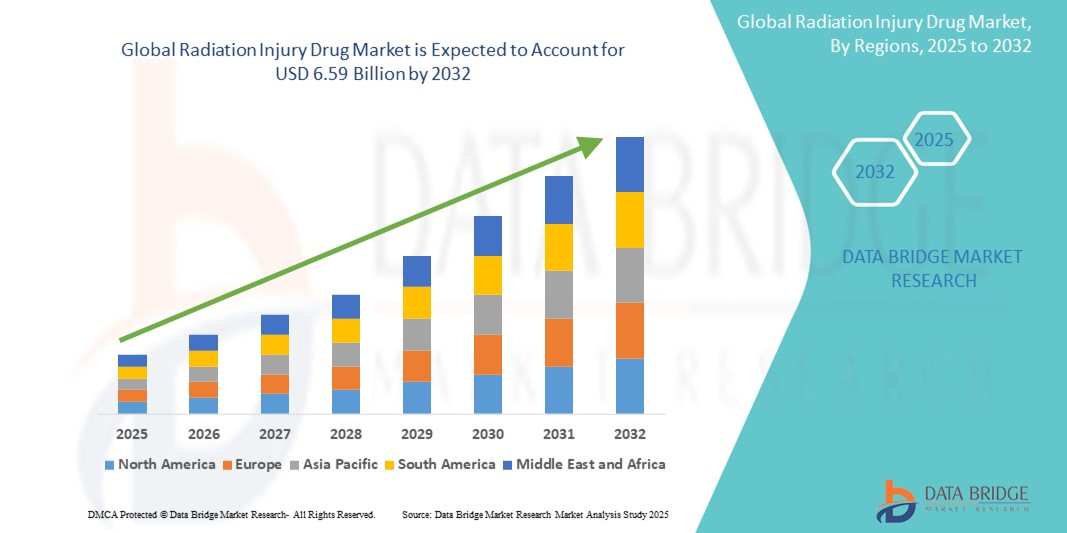

Radiation Injury Drug Market Size

- The global radiation injury drug market size was valued at USD 4.20 billion in 2024 and is expected to reach USD 6.59 billion by 2032, at a CAGR of 5.80% during the forecast period

- The market growth is largely fueled by the growing adoption and technological advancements in emergency preparedness and nuclear medicine, leading to increased development of targeted therapeutics for radiation injuries in both civilian and military populations

- Furthermore, rising global concerns about nuclear accidents, radiological terrorism, and the expanding use of radiation in medical treatments are driving demand for secure, fast-acting, and effective radiation countermeasures. These converging factors are accelerating the uptake of Radiation Injury Drug solutions, thereby significantly boosting the industry's growth

Radiation Injury Drug Market Analysis

- Radiation injury drugs, developed to mitigate damage from exposure to harmful radiation, are becoming increasingly vital components of global preparedness strategies, especially in the context of rising nuclear threats and the expanding use of radiation in medical and industrial applications. These drugs play a crucial role in enhancing survival rates by targeting acute radiation syndromes (ARS) and other complications

- The escalating demand for radiation injury therapeutics is primarily driven by increasing government investments in radiation emergency preparedness, rising concerns over nuclear accidents and terrorism, and a growing emphasis on strengthening national stockpiles and biodefense systems

- North America dominated the radiation injury drug market with the largest revenue share of 41.2% in 2024, attributed to robust governmental support, strategic stockpiling programs led by agencies such as BARDA (Biomedical Advanced Research and Development Authority), and the presence of major pharmaceutical companies actively developing radiation countermeasures

- Asia-Pacific is expected to be the fastest-growing region in the radiation injury drug market during the forecast period, fueled by increasing defense budgets, a heightened focus on disaster readiness in countries such as China, Japan, and India, and improvements in healthcare infrastructure. Regional governments are also increasingly aligning with global biodefense standards, thereby accelerating demand for radiation injury treatments

- The external exposure segment dominated the radiation injury drug market with the largest revenue share of 62.4% in 2024, owing to increased risk from environmental and occupational hazards such as nuclear accidents

Report Scope and Radiation Injury Drug Market Segmentation

|

Attributes |

Radiation Injury Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Radiation Injury Drug Market Trends

“Rising Demand Due to Increasing Radiation Exposure Risks and Emergency Preparedness”

- The radiation injury drug market is experiencing accelerated growth due to the increasing threat of nuclear accidents, radiological terrorism, and occupational exposure in healthcare, nuclear energy, and defense sectors. This has led to heightened demand for effective countermeasures and therapeutic interventions

- For instance, various governments, especially in North America and Europe, are expanding their radiation emergency preparedness programs, which include the stockpiling of radiation injury drugs such as potassium iodide, Neupogen (filgrastim), and Prussian blue to protect against radiation exposure in emergency situations

- In addition, the growing number of cancer patients undergoing radiation therapy also contributes to the market's expansion, as there is an increasing need to treat radiation-induced side effects and injuries, including bone marrow suppression and gastrointestinal damage

- The pharmaceutical industry is responding to this need by developing novel drugs aimed at reducing cellular damage and accelerating tissue repair. Companies are also investing in formulations that are stable, have longer shelf lives, and can be administered quickly during mass-casualty events

- Furthermore, growing awareness of radiation’s long-term health impacts, including the risk of cancer and genetic mutations, is encouraging healthcare providers and emergency management agencies to adopt preventive and therapeutic solutions, thus boosting the market

- The availability of government funding, regulatory incentives for orphan drug development, and the strategic inclusion of radiation countermeasures in national stockpiles present a significant opportunity for pharmaceutical companies to innovate and expand their presence in this critical public health domain

Radiation Injury Drug Market Dynamics

Driver

“Growing Need Due to Rising Radiation Exposure Risks and Global Preparedness Initiatives”

- The increasing frequency of radiation exposure incidents, both accidental (such as, nuclear plant leaks) and intentional (radiological terrorism), has significantly heightened the demand for Radiation Injury Drugs across healthcare, defense, and emergency preparedness sectors

- For instance, in October 2024, the U.S. Department of Health and Human Services (HHS) announced an initiative to expand the national stockpile of radiation countermeasures, including potassium iodide and filgrastim, to prepare for potential nuclear emergencies. Such strategic stockpiling and preparedness efforts by governments and agencies worldwide are expected to drive Radiation Injury Drug industry growth in the forecast period

- As public health agencies and healthcare systems become more aware of the long-term effects of radiation, such as cancer, genetic mutations, and bone marrow damage, there is a growing emphasis on the availability of effective and rapid-response therapies

- Furthermore, the increase in radiation therapy usage for cancer treatments has contributed to the rising demand for drugs that can mitigate side effects such as tissue inflammation, burns, or radiation-induced immune suppression

- The availability of government grants and orphan drug designations for radiation injury countermeasures is attracting new players and stimulating R&D activities. The market is also expanding due to increased awareness about radiation preparedness in military operations, aerospace missions, and nuclear industries

- As regulatory bodies such as the FDA and EMA prioritize fast-tracking such therapies, pharmaceutical companies are investing in radiation-specific biologics and hematopoietic agents, further contributing to market growth

Restraint/Challenge

“Stringent Regulatory Pathways and Limited Commercial Viability”

- One of the primary challenges in the radiation injury drug market is the complexity and cost of drug development, given the ethical limitations in human clinical trials for radiation exposure, which forces companies to rely on animal efficacy studies under the FDA’s Animal Rule

- Moreover, since radiation injury drugs are often used in emergency or rare scenarios, the commercial return on investment can be uncertain, deterring some pharmaceutical companies from entering the market

- For instance, some governments procure these drugs in bulk for stockpiles, but inconsistent procurement patterns and limited recurring usage create challenges for companies in forecasting demand and justifying R&D expenses

- Additional hurdles include strict regulatory requirements, high production costs, and the need for long shelf life and rapid administration, which complicate formulation strategies

- Overcoming these barriers will require continued government support, public-private partnerships, and incentives such as advanced market commitments (AMCs) and priority review vouchers (PRVs) to encourage innovation and ensure global readiness for radiological emergencies

Radiation Injury Drug Market Scope

The market is segmented on the basis of exposure, source, effects, symptoms, diagnosis, treatment, route of administration, end user, and distribution channel.

• By Exposure

On the basis of exposure, the radiation injury drug market is segmented into internal exposure and external exposure. The external exposure segment dominated the market with the largest revenue share of 62.4% in 2024, owing to increased risk from environmental and occupational hazards such as nuclear accidents.

The internal exposure segment is projected to grow at the fastest CAGR of 9.7% from 2025 to 2032, driven by cases involving inhalation or ingestion of radioactive substances.

• By Source

On the basis of source, the radiation injury drug market is segmented into background radiation and man-made radiation. The man-made radiation segment held the largest revenue share of 71.6% in 2024, attributed to radiation exposure from medical imaging, cancer therapy, and nuclear energy sectors.

The background radiation segment is anticipated to grow at a fastest CAGR of 6.4% during the forecast period due to increased cancer treatments, diagnostic imaging use, and radiation therapy advancements.

• By Effects

On the basis of effects, the radiation injury drug market is segmented into radiation and children, radiation and cancer, and radiation and inherited defects. The radiation and cancer segment accounted for the highest market share of 58.2% in 2024, due to the high link between radiation exposure and cancer formation.

The radiation and children segment is projected to grow at the highest CAGR of 10.1% from 2025 to 2032, due to increasing pediatric sensitivity to radiation exposure.

• By Symptoms

On the basis of symptoms, the radiation injury drug market is segmented into acute radiation illness and local radiation injury. The acute radiation illness segment dominated with a revenue share of 67.9% in 2024, driven by high demand for immediate intervention treatments.

The local radiation injury segment is expected to grow at a fastest CAGR of 8.8% during the forecast period, supported by rising cases of localized exposure in medical settings.

• By Diagnosis

On the basis of diagnosis, the radiation injury drug market is segmented into lymphocytes count, Geiger-Muller counter, blood test, and dosimeter. The lymphocytes count segment held the largest share of 39.5% in 2024, as it is a primary tool in assessing radiation-induced immune suppression.

The dosimeter segment is projected to witness the fastest CAGR of 9.2% from 2025 to 2032, due to the growing use of personal dosimetry in high-risk environments.

• By Treatment

On the basis of treatment, the radiation injury drug market is segmented into treatment for damaged bone marrow, treatment for internal contamination, and others. The treatment for damaged bone marrow segment held the leading share of 52.3% in 2024, due to high demand for bone marrow stimulants and cytokines.

The treatment for internal contamination segment is expected to grow at a fastest CAGR of 10.7% from 2025 to 2032, supported by government stockpiling and increasing R&D on decorporation agents.

• By Route of Administration

On the basis of route of administration, the radiation injury drug market is segmented into oral and parenteral. The parenteral segment accounted for the largest revenue share of 66.1% in 2024, favored for emergency treatment efficacy.

The oral segment is projected to expand at a fastest CAGR of 7.9% from 2025 to 2032, due to its potential for mass emergency use and ease of distribution.

• By End User

On the basis of end user, the radiation injury drug market is segmented into hospitals and others. The hospitals segment led the market with a share of 76.4% in 2024, as they are primary treatment centers during radiation emergencies.

The others segment (including defense and emergency response units) is projected to grow at a CAGR of 8.3% over the forecast period.

• By Distribution Channel

On the basis of distribution channel, the radiation injury drug market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment held the highest share of 61.7% in 2024, due to centralized supply during emergencies.

The online pharmacy segment is expected to grow at the fastest CAGR of 11.2% from 2025 to 2032, driven by increasing e-commerce adoption and telehealth expansion.

Radiation Injury Drug Market Regional Analysis

- North America dominated the radiation injury drug market with the largest revenue share of 41.2% in 2024, driven by strong government investment in emergency preparedness and heightened awareness of radiological threats

- The region benefits from the presence of major pharmaceutical companies, strategic initiatives such as the Strategic National Stockpile (SNS), and favorable support from regulatory bodies such as the FDA and BARDA

- These factors, combined with increased R&D funding and integration of radioprotective solutions into national defense infrastructure, have solidified North America's leadership in the global radiation injury drug market

U.S. Radiation Injury Drug Market Insight

The U.S. radiation injury drug market captured the largest revenue share of 83.1% in 2024 within North America, supported by robust federal initiatives such as Project BioShield and procurement contracts for radioprotective agents. Growing focus on Acute Radiation Syndrome (ARS), gastrointestinal syndrome, and hematopoietic syndrome treatment, along with active involvement of biotech firms in R&D, continues to drive growth. In addition, the U.S. Department of Health and Human Services’ efforts toward emergency stockpiling and preparedness are accelerating market expansion.

Europe Radiation Injury Drug Market Insight

The Europe radiation injury drug market is projected to grow at a substantial CAGR during the forecast period, fueled by investments in civil defense and nuclear safety programs. Urbanization and growing reliance on nuclear energy, especially in countries such as France and Germany, are contributing to increased demand for radioprotective drugs. The region’s collaboration with global health organizations to secure pharmaceutical reserves highlights its proactive approach to radiological threat mitigation.

U.K. Radiation Injury Drug Market Insight

The U.K. radiation injury drug market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by public health reforms and defense modernization strategies. The increased adoption of emergency medical countermeasures such as potassium iodide tablets and G-CSF therapies supports market growth. Strong academic-industry collaborations are also propelling the development of novel radiation injury therapies.

Germany Radiation Injury Drug Market Insight

The Germany radiation injury drug market is projected to register a considerable CAGR during the forecast period, supported by a strong pharmaceutical manufacturing base and focus on national emergency preparedness. Emphasis on integrating digital health tools with radiation response systems further strengthens the country’s position as a key market within Europe.

Asia-Pacific Radiation Injury Drug Market Insight

The Asia-Pacific radiation injury drug market is poised to grow at the fastest CAGR of 12.4% from 2025 to 2032, driven by rapid urbanization, nuclear safety concerns, and government-led disaster response initiatives. Countries such as China, Japan, and India are increasing investments in clinical trials, manufacturing, and public health infrastructure to enhance radiological preparedness. Growing affordability and regional production capabilities are expanding access to radiation injury treatments across the APAC region.

Japan Radiation Injury Drug Market Insight

The Japan radiation injury drug market is experiencing rapid growth in this space, with an expected CAGR of 11.8%, supported by post-Fukushima safety reforms and biopharma innovation. The country’s high-tech ecosystem, demand for convenience, and rising geriatric population are contributing to the need for advanced and accessible radiation countermeasures.

China Radiation Injury Drug Market Insight

The China radiation injury drug market accounted for the largest market revenue share in Asia-Pacific at 52.4% in 2024, owing to an expanding middle class, fast-paced urbanization, and strong governmental support for nuclear emergency preparedness. The country’s position is bolstered by aggressive local manufacturing, large-scale procurement, and initiatives to establish national stockpiles of radiation therapeutics.

Radiation Injury Drug Market Share

The radiation injury drug industry is primarily led by well-established companies, including:

- PharmaIN Corp (U.S.)

- Synedgen (U.S.)

- Tonix Pharmaceuticals Holding Corp (U.S.)

- Merck & Co., Inc. (U.S.)

- Windtree Therapeutics, Inc. (U.S.)

- AstraZeneca (U.K.)

- Pfizer, Inc. (U.S.)

- Novartis AG (Switzerland)

- Lilly (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Amgen Inc. (U.S.)

- Biomimetix Pharma (U.S.)

Latest Developments in Global Radiation Injury Drug Market

- In December 2024, Humanetics Corporation secured an additional USD 5 million in funding from the U.S. Department of Defense to support the development of BIO 300, a radiation countermeasure intended for prophylactic use. BIO 300 is being designed to protect military personnel and first responders from radiation exposure, underscoring Humanetics' role in advancing medical preparedness for radiological emergencies. The company aims to pursue Emergency Use Authorization (EUA) to fast-track availability of this critical drug in high-risk scenarios

- In November 2024, HOPO Therapeutics received up to USD 226 million in project funding from BARDA to develop HOPO‑101, the first oral drug candidate for radiation and heavy metal exposure. This funding milestone represents a major step in expanding oral, easy-to-distribute medical countermeasures for nuclear events and radiological attacks, supporting HOPO’s vision of accessible treatments for civilian and defense use

- In October 2024, Synedgen, Inc. announced a partnership with BARDA to accelerate the development of MIIST305, a novel oral therapy to treat Gastrointestinal Acute Radiation Syndrome (GI-ARS). The collaboration reflects BARDA’s focus on expanding the stockpile of next-generation radiation injury drugs with improved administration and storage profiles for national emergency response systems

- In September 2024, Chrysalis BioTherapeutics entered a preclinical evaluation agreement with NIAID to test its drug Chrysalin for cutaneous radiation injuries. The peptide-based therapy is designed to speed up tissue regeneration and wound healing after radiation burns. This move signals a shift toward regenerative approaches in radiation injury management, especially for civilian mass casualty settings

- In August 2024, Tonix Pharmaceuticals announced advancement of its TNX‑801 and TNX‑701 compounds, which are being explored as medical countermeasures for radiation exposure and smallpox. Tonix is actively engaging in federal collaborations to accelerate regulatory pathways and deployment in public health emergency contexts

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.