Global Reiters Syndrome Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.70 Billion

2025

2033

USD

1.70 Billion

USD

2.70 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.70 Billion | |

| USD 2.70 Billion | |

| % | |

|

Reiter’s Syndrome Market Size

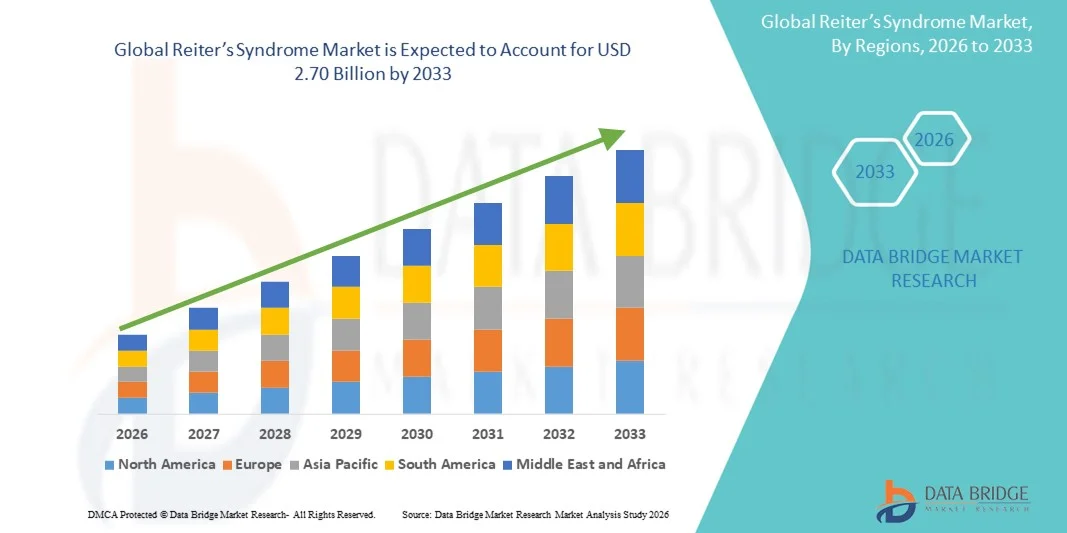

- The global Reiter’s Syndrome market size was valued at USD 1.70 billion in 2025 and is expected to reach USD 2.70 billion by 2033, at a CAGR of 5.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of reactive arthritis and heightened clinical awareness, which are driving the demand for accurate diagnosis and effective therapeutic interventions. Advancements in immunology and targeted therapies are also contributing to improved disease management and expanding treatment adoption globally

- Furthermore, rising patient need for safer, more reliable, and personalized treatment options combined with growing healthcare investments and supportive research initiatives is establishing advanced therapeutics as the standard of care. These converging factors are accelerating the adoption of Reiter’s Syndrome treatment solutions, thereby significantly boosting the industry's growth.

Reiter’s Syndrome Market Analysis

- Reiter’s Syndrome, a form of reactive arthritis triggered by infections and characterized by joint inflammation, urogenital symptoms, and ocular complications, is becoming an increasingly important focus area in rheumatology due to its complex clinical presentation, rising diagnostic awareness, and growing emphasis on early immunological intervention for improved patient outcomes

- The escalating demand for Reiter’s Syndrome treatments is primarily fueled by increasing incidence of infection-related arthritic conditions, enhanced screening capabilities, and a rising preference for targeted therapies that offer better symptom control and reduce long-term complications

- North America dominated the Reiter’s Syndrome market with the largest revenue share of 38.9% in 2025, supported by advanced healthcare infrastructure, high diagnostic rates, greater patient awareness, and the strong presence of pharmaceutical players developing immunomodulatory and anti-inflammatory therapies. The U.S. experienced significant adoption of biologics and combination treatment protocols, driven by ongoing research initiatives and expanded access to rheumatology care

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, backed by rising infection rates, improving healthcare access, expanding clinical evaluation capabilities, and increasing investments in autoimmune disease management

- Nonsteroidal anti-inflammatory drugs (NSAIDs) segment dominated the Reiter’s Syndrome market with a treatment share of 47.2% in 2025, driven by their established efficacy in managing acute inflammatory symptoms and widespread use as the first-line therapeutic approach, with growing utilization supported by clinical familiarity and cost-effectiveness

Report Scope and Reiter’s Syndrome Market Segmentation

|

Attributes |

Reiter’s Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Reiter’s Syndrome Market Trends

Advancement of Targeted Immunotherapies and Precision Diagnostics

- A significant and accelerating trend in the global Reiter’s Syndrome market is the advancement of targeted immunotherapies and precision diagnostic tools, driven by the need for more accurate disease identification and improved long-term symptom management

- For instance, diagnostic platforms integrating molecular assays and PCR testing now aid in detecting infection-related triggers, while companies developing TNF-inhibitors and IL-17 blockers are enhancing therapeutic precision for inflammatory pathways associated with reactive arthritis

- AI-assisted diagnostic support enables clinicians to analyze symptom patterns, predict flare-ups, and choose optimal treatment strategies; for instance, advanced platforms used in some rheumatology clinics can streamline differential diagnosis and improve early detection accuracy for Reiter’s Syndrome cases

- Furthermore, digital health tools such as remote symptom tracking and tele-consultation solutions offer patients improved monitoring capabilities, enabling timely adjustments in treatment plans and reducing the risk of disease progression

- The integration of precision diagnostics with advanced therapeutics is reshaping clinical expectations for care quality; consequently, companies such as AbbVie and Novartis are investing in next-generation immunomodulatory therapies targeting chronic inflammatory responses associated with reactive arthritis

- The demand for more accurate, personalized, and data-driven disease management solutions is growing rapidly across both developed and emerging healthcare systems as clinicians prioritize better long-term outcomes and earlier intervention strategies

Reiter’s Syndrome Market Dynamics

Driver

Increasing Disease Incidence and Rising Adoption of Advanced Therapeutic Approaches

- The increasing prevalence of infection-related arthritic conditions, particularly those linked to chlamydial and gastrointestinal infections, coupled with improving diagnostic precision, is a significant driver strengthening the demand for Reiter’s Syndrome treatments

- For instance, in recent years, several healthcare systems have reported rising cases of reactive arthritis, prompting pharmaceutical companies to expand research into immunomodulatory therapies and biologics designed to address persistent inflammatory pathways

- As clinicians become more aware of evolving infection sources and the need for early intervention, advanced therapies such as biologics, DMARDs, and combination regimens offer improved long-term symptom control, representing a compelling upgrade over traditional anti-inflammatory medications

- Furthermore, the growing availability of rheumatology specialists and the expansion of integrated care models are elevating patient access to sophisticated treatment protocols, strengthening the adoption of advanced care approaches in both hospital and specialty clinic settings

- The convenience of tele-rheumatology consultations, remote disease monitoring tools, and digital platforms enabling real-time patient support are key factors propelling the uptake of modern therapeutic regimens across diverse patient populations

- The trend toward personalized treatment planning and growing investments in autoimmune disease research further contribute to market growth

Restraint/Challenge

Side-Effect Profiles and Diagnostic Complexity as Key Barriers

- Concerns surrounding the side-effects of long-term therapy including gastrointestinal complications from NSAIDs and immune suppression from biologics pose a significant challenge to broader adoption of advanced treatment options

- For instance, reported cases of treatment-related adverse reactions in autoimmune conditions have made some clinicians cautious in prescribing aggressive therapies, especially for patients with comorbidities requiring close monitoring

- Addressing these concerns through improved safety-profile drugs, optimized dosing guidelines, and enhanced patient monitoring programs is crucial for strengthening treatment confidence; companies such as Pfizer and Amgen emphasize safety data and improved formulations to reassure healthcare providers

- In addition, the relatively high cost of biologics and advanced diagnostics compared to standard anti-inflammatory drugs can be a barrier for patients in low- and middle-income regions, where reimbursement limitations further restrict access

- While affordability initiatives and expanded healthcare coverage are gradually improving access, the perceived premium associated with advanced immunotherapies can still hinder widespread adoption, particularly among patients with limited financial resources

- Overcoming these challenges through safer therapeutic innovations, clinician education on updated guidelines, and broader availability of cost-effective diagnostic solutions will be vital for sustained market growth

Reiter’s Syndrome Market Scope

The market is segmented on the basis of treatment, diagnosis, dosage, route of administration, symptoms, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the market is segmented into antibiotics, corticosteroids, nonsteroidal anti-inflammatory drugs (NSAIDs), immunosuppressive drugs, physical therapy, and others. The NSAIDs segment dominated the market with the largest market revenue share of 47.2% in 2025, driven by its established efficacy in managing acute pain, inflammation, and joint stiffness associated with Reiter’s Syndrome. Clinicians widely prescribe NSAIDs for their immediate symptom-relieving properties and long-standing clinical acceptance. The segment benefits from high patient familiarity, affordability, and strong prescription volumes across primary and specialty care. NSAIDs are preferred for both outpatient and long-term management, contributing to consistent market demand. In addition, their broad availability in generic and prescription forms reinforces segment dominance. High adherence rates among patients further strengthen the market position of NSAIDs. The segment’s strong clinical guideline support also makes it a default first-line therapy in most healthcare systems.

The Immunosuppressive Drugs segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption for patients who do not respond adequately to NSAIDs or corticosteroids. These therapies target chronic inflammation and autoimmune pathways, providing longer-term symptom control. Growing clinical evidence supporting methotrexate, sulfasalazine, and biologics is driving physician confidence. Investments in autoimmune research and wider availability of specialty drugs are accelerating uptake. Improved access to rheumatology care also supports rapid adoption. Patient awareness of advanced treatment options is further contributing to segment growth. The development of novel biologics with improved safety profiles is expected to sustain growth momentum.

- By Diagnosis

On the basis of diagnosis, the market is segmented into blood tests, joint fluid tests, x-ray, and others. The Blood Tests segment dominated the market in 2025 due to its crucial role in detecting inflammatory markers and infection triggers associated with reactive arthritis. Clinicians widely rely on tests such as ESR, CRP, and HLA-B27 to evaluate disease severity. Blood tests provide rapid results, broad accessibility, and strong reliability, making them the preferred diagnostic method. They are essential for differential diagnosis and early intervention, further reinforcing dominance. Widespread clinician familiarity supports their routine use in both hospital and outpatient settings. Continuous advancements in assay sensitivity strengthen their adoption. Increasing awareness of early diagnosis benefits among patients is also driving test utilization.

The Joint Fluid Tests segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use for precise assessment of synovial inflammation and exclusion of septic arthritis. These tests offer high diagnostic accuracy, particularly for atypical or complex Reiter’s Syndrome presentations. Clinicians are increasingly adopting synovial fluid analysis for early disease detection. Advancements in ultrasound-guided aspiration and lab technology facilitate wider usage. Specialist rheumatology centers in emerging regions are expanding access. Early intervention enabled by joint fluid analysis further supports market growth. In addition, growing research on inflammatory biomarkers enhances clinical confidence in joint fluid testing.

- By Dosage

On the basis of dosage, the market is segmented into tablet, injection, and others. The Tablet segment dominated the market in 2025 due to convenience, high patient adherence, and widespread use for NSAIDs, antibiotics, and immunosuppressive drugs. Oral formulations are cost-effective, easily administered, and preferred in outpatient care. They allow dose titration and long-term therapy management. Tablets are the most accessible dosage form across global healthcare systems. High availability of generic tablets further strengthens adoption. Their dominance is reinforced by physician preference and patient familiarity. Tablets are also preferred for self-administration, improving overall compliance and treatment continuity.

The Injection segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of injectable corticosteroids and biologics for severe or refractory cases. Injections ensure rapid therapeutic onset and precise dosing. The segment benefits from expanding infusion centers and growing use of advanced immunomodulators. Injectable formulations are preferred for acute flare management and systemic inflammation. Increased clinician confidence and patient awareness support adoption. Long-acting injectable development further drives segment growth. Hospitals and specialty clinics increasingly provide training and support for injection administration, boosting adoption.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The Oral segment dominated the market in 2025 due to widespread use of oral NSAIDs, antibiotics, and immunosuppressants. Oral administration promotes adherence, convenience, and long-term treatment. Most first-line therapies are delivered orally, reinforcing market share. Oral formulations are cost-effective and widely available. Physicians prefer oral delivery for mild to moderate symptoms. Availability of new oral immunomodulators strengthens the segment further. Oral administration also supports patient self-management and reduces hospital dependency.

The Intravenous segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of IV corticosteroids and biologics in severe or refractory cases. IV administration ensures rapid onset and controlled drug delivery. Hospitals and specialty clinics rely on IV therapies requiring monitoring. Expansion of infusion centers accelerates growth. Severe patient cases often require IV treatment. Adoption of advanced autoimmune protocols further fuels the segment. IV administration also allows combination therapy for better disease control, enhancing clinical preference.

- By Symptoms

On the basis of symptoms, the market is segmented into eye inflammation, skin problems, pain and stiffness, swollen toes or fingers, enthesitis, low back pain, urinary problems, and others. The Pain and Stiffness segment dominated the market in 2025 due to its high prevalence and role as a primary symptom prompting medical consultation. Pain and stiffness are central to diagnosis and management. NSAIDs and corticosteroids are commonly used to control these symptoms. Their persistent nature drives long-term therapy usage. Clinician focus on pain management reinforces segment dominance. Patients prioritize relief from these symptoms, sustaining demand. The segment’s frequent monitoring and follow-up care also support revenue growth.

The Eye Inflammation segment is expected to witness the fastest growth rate from 2026 to 2033 due to rising awareness of ocular complications such as conjunctivitis and uveitis. Early identification of eye symptoms is increasing through improved ophthalmology and rheumatology screenings. Eye involvement signals systemic disease progression, prompting rapid treatment. Specialized ocular monitoring is being integrated in clinics. Clinician awareness drives referrals. Adoption of targeted therapies supports growth. Advances in imaging and patient education further strengthen segment expansion.

- By End-Users

On the basis of end-users, the market is segmented into clinic, hospital, and others. The Hospital segment dominated the market in 2025 due to availability of advanced diagnostics, multidisciplinary care, and infusion therapy for severe cases. Hospitals provide specialized rheumatology care and IV therapy administration. Severe and recurrent cases are primarily managed in hospital settings. Integration of lab services ensures timely diagnostics. Hospital infrastructure supports complex treatment delivery. Patient trust in hospital care further reinforces dominance. Hospitals also serve as centers for clinical trials and early access programs, driving additional demand.

The Clinic segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing outpatient consultations and tele-rheumatology adoption. Clinics provide accessible care for mild to moderate symptoms. Community rheumatology clinics expand reach. Early symptom evaluation and monitoring promote clinic visits. Clinics offer lower treatment costs and shorter wait times. Growing patient preference for outpatient management accelerates segment growth. Expansion of digital health platforms also enhances clinic-based treatment accessibility.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The Hospital Pharmacy segment dominated the market in 2025 due to its role in dispensing IV therapies, biologics, and specialized drugs. Hospital pharmacies ensure immediate availability for inpatients and outpatients. Integration with clinical departments streamlines therapy delivery. High prescription volumes reinforce market share. Hospitals manage severe or complex cases, supporting segment dominance. Pharmacist expertise in monitoring high-risk medications further strengthens adoption. Hospital pharmacies also offer patient counseling and adherence programs, boosting usage.

The Online Pharmacy segment is expected to witness the fastest growth rate from 2026 to 2033, due to rising e-prescription adoption and patient preference for home delivery. Patients increasingly order NSAIDs, oral immunosuppressants, and supportive therapies online. Telemedicine integration supports online pharmacy usage. Competitive pricing and subscription refills encourage adoption. Regulatory improvements enable safer distribution. Convenience of doorstep delivery accelerates growth. Rising smartphone penetration and digital literacy further enhance segment expansion.

Reiter’s Syndrome Market Regional Analysis

- North America dominated the Reiter’s Syndrome market with the largest revenue share of 38.9% in 2025, supported by advanced healthcare infrastructure, high diagnostic rates, greater patient awareness, and the strong presence of pharmaceutical players developing immunomodulatory and anti-inflammatory therapies

- Patients and clinicians in the region highly value early diagnosis, availability of advanced therapeutics such as NSAIDs, corticosteroids, and biologics, and the presence of well-established rheumatology care networks

- This widespread adoption is further supported by high healthcare spending, advanced diagnostic facilities, and strong pharmaceutical research presence, establishing North America as a leading market for Reiter’s Syndrome treatments in both hospital and outpatient settings

U.S. Reiter’s Syndrome Market Insight

The U.S. Reiter’s Syndrome market captured the largest revenue share of 80% in 2025 within North America, fueled by increasing awareness of reactive arthritis, rising incidence of infection-related arthritic conditions, and widespread access to advanced healthcare infrastructure. Patients and clinicians are prioritizing early diagnosis, effective symptom management, and availability of NSAIDs, corticosteroids, and biologics. The growing adoption of outpatient rheumatology clinics, telemedicine, and specialized care centers further supports market growth. In addition, robust pharmaceutical research, government healthcare initiatives, and high healthcare spending are driving the uptake of advanced therapeutics. Awareness campaigns and patient support programs are enhancing diagnosis and treatment rates, further propelling the U.S. market.

Europe Reiter’s Syndrome Market Insight

The Europe Reiter’s Syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of autoimmune and infection-related arthritic conditions and strong healthcare infrastructure. Rising urbanization, growing rheumatology specialization, and expanding access to diagnostic facilities are fostering early detection and treatment adoption. European patients are increasingly seeking advanced therapies, such as biologics and immunosuppressive drugs, to manage chronic or recurrent cases. The region also benefits from government healthcare programs supporting autoimmune disease management. Enhanced awareness among clinicians and patients regarding long-term disease management is driving sustained market expansion. Integration of multidisciplinary care models in hospitals is further accelerating growth.

U.K. Reiter’s Syndrome Market Insight

The U.K. Reiter’s Syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising infection-related arthritis cases and increasing emphasis on early diagnosis and patient care. Concerns regarding long-term joint damage and systemic complications are motivating patients and clinicians to adopt advanced therapies. The U.K.’s strong healthcare system, widespread access to diagnostic testing, and high awareness among healthcare professionals are expected to support market growth. Tele-rheumatology services and outpatient clinics are increasingly utilized for early symptom evaluation. The growing availability of immunomodulators and targeted therapies is further stimulating adoption. Patient education programs and government initiatives on autoimmune care are also driving market expansion.

Germany Reiter’s Syndrome Market Insight

The Germany Reiter’s Syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of reactive arthritis, advancements in diagnostics, and availability of specialized rheumatology care. Germany’s well-developed healthcare infrastructure, combined with emphasis on clinical research and patient safety, promotes early intervention and effective disease management. Hospitals and specialty clinics are increasingly providing biologics and immunosuppressive therapies for severe cases. Integration of diagnostic facilities with patient care pathways is becoming prevalent, supporting treatment adherence. The country’s strong regulatory framework and insurance coverage further enhance treatment access. Growing patient and clinician awareness of long-term disease management strengthens market growth.

Asia-Pacific Reiter’s Syndrome Market Insight

The Asia-Pacific Reiter’s Syndrome market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by rising urbanization, growing disposable incomes, and increased healthcare awareness in countries such as China, Japan, and India. The region is witnessing rapid expansion of diagnostic infrastructure and rheumatology clinics. Government initiatives promoting early disease detection and autoimmune healthcare programs are accelerating adoption. In addition, increasing availability of advanced therapeutics, including biologics and immunosuppressive drugs, is driving market growth. Expansion of private healthcare networks and telemedicine platforms is improving accessibility. Growing patient awareness and early intervention programs are further contributing to rapid market development.

Japan Reiter’s Syndrome Market Insight

The Japan Reiter’s Syndrome market is gaining momentum due to the country’s aging population, high healthcare standards, and focus on early diagnosis and advanced treatment. Patients and clinicians are increasingly adopting biologics and immunomodulators to manage chronic or recurrent cases. Integration of specialized rheumatology clinics with advanced diagnostic tools supports precise disease management. Telehealth consultations and outpatient services are helping improve treatment adherence. Awareness campaigns targeting autoimmune conditions are encouraging early care-seeking behavior. Government support for chronic disease management and patient education is driving market expansion. The combination of technological advancement and healthcare access strengthens overall market growth.

India Reiter’s Syndrome Market Insight

The India Reiter’s Syndrome market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising prevalence of infection-related arthritis, expanding healthcare infrastructure, and increasing awareness among patients and clinicians. The country’s growing middle class and rising disposable incomes are enabling greater access to diagnostic facilities and treatment options. Telemedicine services, outpatient rheumatology clinics, and specialty centers are supporting early diagnosis and management. Government initiatives promoting autoimmune disease awareness and chronic disease programs are further boosting adoption. Availability of affordable therapeutics, including NSAIDs and corticosteroids, supports broader treatment access. Expansion of private healthcare networks and patient education initiatives is accelerating market growth.

Reiter’s Syndrome Market Share

The Reiter’s Syndrome industry is primarily led by well-established companies, including:

- Pfizer Inc., (U.S.)

- Novartis AG (Switzerland)

- AbbVie Inc., (U.S.)

- Amgen Inc., (U.S.)

- AstraZeneca (U.K.)

- UCB S.A. (Belgium)

- Johnson & Johnson Services, Inc. (U.S.)

- F. Hoffmann La Roche Ltd. (Switzerland)

- Teva Pharmaceutical Industries Ltd., (Israel)

- Bayer AG (Germany)

- Bristol Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc., (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Velcura Therapeutics, Inc. (U.S.)

- Geri-Care Pharmaceuticals (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Cipla Limited (India)

- Takeda Pharmaceutical Company Limited (Japan)

- Boehringer Ingelheim International GmbH (Germany)

What are the Recent Developments in Global Reiter’s Syndrome Market?

- In March 2025, a new systematic‑review titled “Post‑Infectious Reactive Arthritis” was published summarizing 12 studies and reaffirming that classical bacterial triggers remain the predominant cause, while also highlighting persistent inconsistencies in treatment protocols and the need for standardized guidelines

- In June 2024, a large meta‑analysis systematically reviewed data on enteric infections and their association with development of reactive arthritis providing updated epidemiological evidence that supports the classical GI‑infection → ReA link, and helping refine risk estimates for ReA after such infections

- In February 2024, a study published in a rheumatology journal proposed that intestinal dysbiosis and stress can form the intrinsic basis of reactive arthritis suggesting a paradigm shift: beyond acute infections, chronic gut‑microbiome alterations may play a role in ReA pathogenesis

- In January 2024, a case report described chronic reactive arthritis secondary to Chlamydia trachomatis genital infection reinforcing the role of sexually acquired infections as a significant driver of ReA and drawing attention to under‑recognized iatrogenic and infectious triggers in routine clinical practice

- In March 2023, a systematic review was published showing that COVID-19 infection may act as a trigger for reactive arthritis with onset of joint symptoms reported around 22 days after COVID‑19 infection in many cases, indicating that viral infections (not only classical bacterial GI/GU infections) are now being recognized as potential triggers of ReA

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.