Global Remdesivir Market

Market Size in USD Billion

USD

4.79 Billion

USD

33.39 Billion

2025

2033

USD

4.79 Billion

USD

33.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.79 Billion | |

| USD 33.39 Billion | |

| % | |

|

Remdesivir Market Size

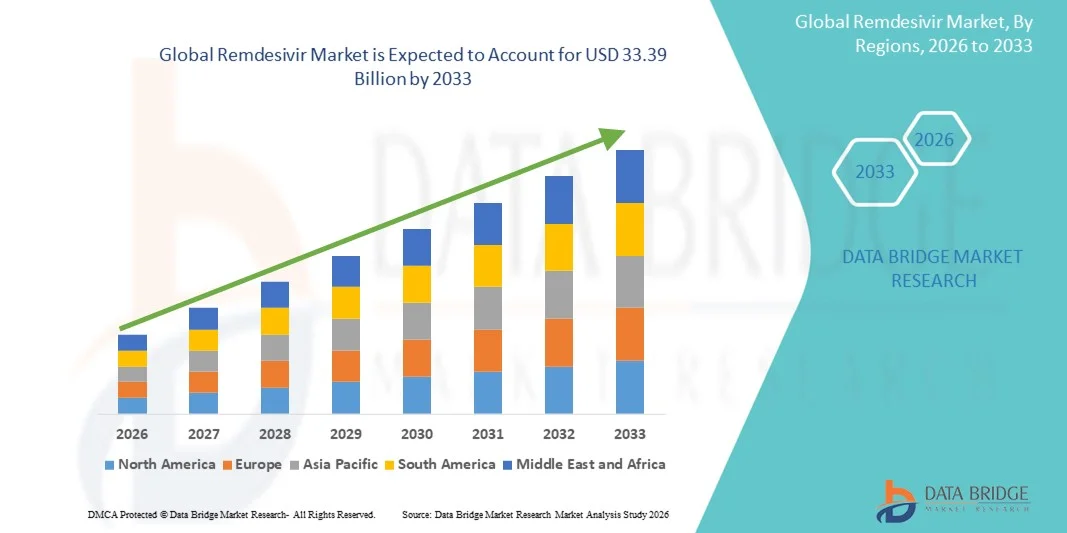

- The global remdesivir market size was valued at USD 4.79 billion in 2025 and is expected to reach USD 33.39 billion by 2033, at a CAGR of 27.46% during the forecast period

- The market growth is largely driven by increasing prevalence of viral infections, including COVID-19, and the expanding adoption of antiviral therapies in both hospital and outpatient settings

- Furthermore, ongoing research, approvals for emergency and routine use, and rising awareness among healthcare providers and patients are boosting demand for effective antiviral treatments. These factors are collectively accelerating the uptake of remdesivir, thereby significantly propelling the industry's growth

Remdesivir Market Analysis

- Remdesivir, an antiviral drug used primarily for the treatment of COVID-19 and other viral infections, is increasingly recognized as a critical component of modern antiviral therapy protocols in both hospital and outpatient settings due to its efficacy, intravenous administration, and emergency use approvals

- The escalating demand for remdesivir is primarily fueled by the rising incidence of viral infections, increasing hospitalization rates, and growing awareness among healthcare providers regarding effective antiviral treatment options

- North America dominated the remdesivir market with the largest revenue share of 38.9% in 2025, characterized by a well-established healthcare infrastructure, early adoption of novel antiviral therapies, and strong government initiatives to support COVID-19 treatment, with the U.S. witnessing significant usage in hospitals and critical care units, driven by approvals and large-scale procurement by healthcare institutions

- Asia-Pacific is expected to be the fastest growing region in the remdesivir market during the forecast period due to increasing healthcare investments, rising prevalence of viral infections, improving hospital infrastructure, and expanding adoption of antiviral therapies across emerging economies such as India, China, and Southeast Asian countries

- Lyophilized powder segment dominated the remdesivir market with a market share of 62.8% in 2025, driven by its stability, ease of storage, and compatibility with established reconstitution protocols in hospital settings

Report Scope and Remdesivir Market Segmentation

|

Attributes |

Remdesivir Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Remdesivir Market Trends

Expansion of Emergency Use Approvals and Treatment Protocols

- A key and accelerating trend in the global remdesivir market is the increasing inclusion of remdesivir in emergency use authorizations and standardized treatment protocols for COVID-19 and other viral infections, enhancing its accessibility across hospitals and clinics worldwide

- For instance, several countries in Europe and Asia have updated national guidelines to include remdesivir as a first-line antiviral for hospitalized COVID-19 patients, improving timely administration and patient outcomes

- Ongoing research and clinical trials are expanding its indications to treat other viral infections such as Ebola and SARS-CoV, reinforcing its therapeutic versatility and encouraging broader adoption in critical care settings

- The integration of remdesivir into hospital treatment regimens alongside other supportive therapies facilitates more streamlined patient management, reducing ICU stay duration and improving recovery rates

- This trend towards regulatory acceptance and clinical standardization is reshaping physician and hospital expectations for antiviral treatment, prompting pharmaceutical companies such as Gilead Sciences to invest in scaling production and supply chain optimization

- The demand for remdesivir is increasing rapidly across both developed and emerging markets, as healthcare providers prioritize access to approved and clinically validated antiviral therapies to manage viral outbreaks efficiently

- Expanded collaborations between pharmaceutical companies and governments to secure bulk procurement and distribution channels are emerging as a trend, ensuring timely access during infection surges

- Advancements in formulation research, including lyophilized powders and concentrated solutions, are enabling easier storage, transport, and administration in diverse hospital and clinic settings, further driving market adoption

Remdesivir Market Dynamics

Driver

Rising Viral Infection Rates and Hospitalization Demands

- The increasing prevalence of COVID-19 and other viral infections, coupled with rising hospitalization rates, is a major driver for the growing demand for remdesivir

- For instance, in March 2025, Gilead Sciences announced the expansion of its global production capacity to meet rising hospital demand in North America and Asia-Pacific

- As healthcare providers seek effective antiviral therapies to reduce disease severity and ICU duration, remdesivir offers a clinically validated solution with documented efficacy in viral load reduction

- Furthermore, growing awareness among physicians and patients regarding treatment protocols and government initiatives to ensure antiviral availability are reinforcing remdesivir’s adoption in hospital and outpatient settings

- The urgency for effective treatment options, coupled with the increasing prevalence of moderate-to-severe viral infections, continues to propel the remdesivir market globally, making it a critical component of modern antiviral therapy

- Increased funding for public health programs and emergency preparedness initiatives in response to viral outbreaks is further boosting remdesivir demand in both developed and emerging regions

- The rise of telemedicine and remote patient monitoring solutions facilitates early diagnosis and timely administration of remdesivir, enhancing its adoption across hospital and clinic networks

Restraint/Challenge

Limited Supply, High Cost, and Regulatory Hurdles

- Supply constraints, high treatment costs, and stringent regulatory approvals pose significant challenges to the broader adoption of remdesivir across global healthcare systems

- For instance, intermittent shortages reported in hospitals during peak COVID-19 waves limited patient access and delayed therapy initiation in several regions

- The high price of remdesivir compared to alternative supportive treatments can restrict its use, especially in developing countries or price-sensitive healthcare systems

- Furthermore, variations in national regulatory approvals and emergency use authorizations can create inconsistencies in availability and hospital procurement practices, complicating large-scale distribution

- Addressing these challenges through expanded manufacturing, price optimization, and streamlined regulatory processes will be critical for ensuring wider patient access and sustained market growth

- Challenges in cold chain logistics and storage requirements, especially for lyophilized or concentrated forms, can limit distribution in remote or resource-limited regions

- Patent protections and intellectual property rights in certain countries can hinder generic production and local availability, impacting affordability and widespread adoption

Remdesivir Market Scope

The market is segmented on the basis of dosage, patient type, form, application, and end user.

- By Dosage

On the basis of dosage, the remdesivir market is segmented into 2.5MG, 5MG, 100MG, and 200MG. The 100MG segment dominated the market with the largest revenue share in 2025, driven by its standardization in hospital protocols for adult patients and compatibility with recommended intravenous infusion regimens. This dosage is widely preferred by healthcare providers for moderate-to-severe COVID-19 cases due to its established efficacy and ease of administration. Hospitals and clinics prioritize the 100MG dosage for critical care treatments, ensuring consistent dosing and minimizing preparation errors. In addition, the widespread adoption of 100MG vials in global supply chains reinforces its dominance. Its compatibility with existing infusion equipment and ease of storage further supports hospital demand. The segment also benefits from global clinical guidelines recommending 100MG as the primary antiviral dose for adults.

The 200MG segment is anticipated to witness the fastest growth from 2026 to 2033, fueled by increasing demand for higher-dose regimens in severe cases and emerging applications for viral infections beyond COVID-19. This dosage is gaining traction in regions with rising adult hospitalization rates and in specialized care units where larger doses are required for effective treatment. Ongoing clinical trials exploring optimal dosing strategies for improved patient outcomes are supporting its adoption. The segment is further driven by hospitals seeking flexibility in administering combination therapies with varying dose requirements. In addition, expansion in Asia-Pacific and Latin America healthcare infrastructure is contributing to faster uptake of 200MG vials.

- By Patient Type

On the basis of patient type, the remdesivir market is segmented into adult, pediatric, and geriatric. The adult segment dominated the market in 2025, owing to the high prevalence of COVID-19 and other viral infections among adults requiring hospitalization and antiviral therapy. Adult patients form the majority of hospital admissions for moderate-to-severe cases, making this segment the primary revenue driver. Standardized dosing regimens and treatment protocols are focused on adult patients, further strengthening market share. Hospitals and clinics prefer adult formulations due to ease of administration and established safety profiles. The segment also benefits from greater awareness among healthcare providers and adherence to treatment guidelines. Moreover, adult patients often have higher ICU admission rates, driving bulk procurement of remdesivir for hospital inventories.

The pediatric segment is expected to witness the fastest growth during the forecast period, driven by increasing clinical studies supporting safe pediatric use and rising demand for age-appropriate formulations. Regulatory approvals for pediatric emergency use and growing awareness among caregivers are encouraging wider adoption in this segment. Pediatric hospitals and specialized care units are increasingly integrating remdesivir into treatment protocols. The segment is further supported by efforts to produce pre-measured pediatric doses for ease of administration. Expansion in emerging markets with rising child hospitalization rates also fuels growth.

- By Form

On the basis of form, the remdesivir market is segmented into lyophilized powder and concentrated solution. The lyophilized powder segment dominated the market with a 62.8% share in 2025 due to its longer shelf life, stability at varying temperatures, and ease of transport across hospital and clinic networks. Hospitals prefer lyophilized powder for its reconstitution flexibility and compatibility with standard intravenous administration procedures. Its robustness reduces the risk of degradation, ensuring efficacy during storage and distribution. Global supply chains favor lyophilized formulations for bulk procurement and emergency stockpiling. In addition, the ease of storage and handling makes it ideal for both urban and remote healthcare facilities. The segment is further strengthened by government and NGO programs focusing on stockpiling in preparation for viral outbreaks.

The concentrated solution segment is expected to register the fastest growth during the forecast period, supported by the increasing use in outpatient and smaller clinic settings where rapid reconstitution and direct infusion are preferred. Concentrated solutions reduce preparation time and simplify dosing for healthcare staff, enhancing workflow efficiency. The segment benefits from hospitals and clinics seeking immediate-use solutions for urgent cases. Its compact form and reduced storage requirements make it suitable for facilities with limited cold chain infrastructure. In addition, growing telemedicine and home care initiatives are supporting the adoption of concentrated solutions.

- By Application

On the basis of application, the remdesivir market is segmented into Ebola, SARS-COV, MERS-COV, and COVID-19. The COVID-19 segment dominated the market in 2025, driven by the global pandemic and widespread hospitalizations requiring antiviral treatment. Remdesivir is included in treatment protocols for moderate-to-severe COVID-19 cases, reinforcing its critical role in patient care. Government stockpiling, emergency use authorizations, and global awareness campaigns have further expanded its adoption. Hospitals and clinics rely on COVID-19 protocols to standardize dosing and optimize patient outcomes. The segment benefits from ongoing clinical evidence supporting antiviral efficacy, strengthening confidence among healthcare providers. In addition, high patient volumes during successive COVID-19 waves contributed to bulk hospital procurement, solidifying dominance.

The Ebola segment is expected to witness the fastest growth from 2026 to 2033, due to increasing research into repurposing remdesivir for emerging viral infections and outbreaks. Rising investment in antiviral research and potential future outbreaks in Africa and Asia-Pacific are expected to accelerate market expansion in this application. The segment is further supported by international health organizations promoting antiviral research and stockpiling. Clinical trials targeting Ebola patients are increasing the focus on remdesivir’s therapeutic versatility. In addition, collaborations between pharmaceutical companies and governments are improving distribution channels for Ebola treatment programs.

- By End User

On the basis of end user, the remdesivir market is segmented into hospitals, clinics, pharmacy and drug stores, and online pharmacies. The hospitals segment dominated the market with a 59.8% share in 2025, due to the intravenous administration of remdesivir requiring trained medical personnel, monitoring, and adherence to treatment protocols. Hospitals are the primary sites for moderate-to-severe cases, and standardized protocols ensure consistent usage. Bulk procurement and centralized supply chains favor hospital adoption. In addition, government support and emergency preparedness programs often route remdesivir through hospital channels. Hospitals benefit from established infrastructure for storage, reconstitution, and infusion. The segment is further strengthened by higher patient volumes and insurance coverage facilitating hospital treatments.

The online pharmacies segment is anticipated to witness the fastest growth during the forecast period, fueled by increasing telemedicine consultations, growing e-pharmacy adoption, and rising demand for convenient access to antiviral therapies in outpatient settings. This channel enables faster delivery to remote or home-bound patients, improving treatment accessibility. The segment benefits from digital prescriptions and rising patient comfort with home-based care. In addition, online platforms allow integration with logistics networks for cold chain distribution. Increasing regulatory acceptance of e-pharmacy channels in emerging markets further accelerates growth.

Remdesivir Market Regional Analysis

- North America dominated the remdesivir market with the largest revenue share of 38.9% in 2025, characterized by a well-established healthcare infrastructure, early adoption of novel antiviral therapies, and strong government initiatives to support COVID-19 treatment, with the U.S. witnessing significant usage in hospitals and critical care units, driven by approvals and large-scale procurement by healthcare institutions

- Healthcare providers in the region prioritize timely administration of antiviral therapies, supported by strong government initiatives, emergency use authorizations, and bulk procurement programs for critical care treatments

- The widespread adoption is further supported by advanced hospital infrastructure, early access to novel antiviral drugs, and a technologically equipped healthcare workforce, establishing remdesivir as a preferred antiviral solution for moderate-to-severe viral infections in both hospitals and clinics

U.S. Remdesivir Market Insight

The U.S. remdesivir market captured the largest revenue share of 42% in 2025 within North America, driven by the high prevalence of COVID-19 and other viral infections requiring hospitalization. Hospitals and clinics prioritize timely administration of antiviral therapy for moderate-to-severe cases, supported by government stockpiling and emergency use authorizations. The widespread availability of advanced healthcare infrastructure and ICU facilities enhances the adoption of remdesivir. In addition, rising awareness among physicians regarding standardized treatment protocols and clinical guidelines further propels market growth. Telemedicine and home care programs facilitating early diagnosis and treatment also contribute to expanding uptake. The integration of remdesivir into hospital formularies ensures consistent supply and accessibility across healthcare facilities.

Europe Remdesivir Market Insight

The Europe remdesivir market is projected to expand at a substantial CAGR during the forecast period, primarily driven by rising COVID-19 cases, increasing hospitalizations, and the inclusion of remdesivir in standardized treatment protocols. Stringent regulatory approvals and government-backed procurement programs support wider access to antiviral therapy. The growing focus on improving hospital infrastructure, ICU capacity, and antiviral availability fosters adoption across residential and critical care settings. European healthcare providers are increasingly aware of remdesivir’s clinical efficacy, boosting its preference in hospital formularies. In addition, the expansion of private hospitals and multi-specialty clinics supports demand for consistent antiviral supply. Collaborative initiatives between pharmaceutical companies and health authorities are enhancing distribution efficiency across the region.

U.K. Remdesivir Market Insight

The U.K. remdesivir market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising demand for effective antiviral therapies amid ongoing viral outbreaks. Hospitals and clinics are adopting remdesivir for moderate-to-severe cases due to well-defined treatment protocols and government support for procurement. Increased patient awareness and healthcare provider confidence in remdesivir’s efficacy further accelerate adoption. The country’s robust healthcare infrastructure and centralized distribution channels ensure timely access across hospitals. In addition, regulatory approvals and emergency use authorizations enhance trust and usage. Telemedicine and outpatient services facilitating early diagnosis also contribute to expanding uptake.

Germany Remdesivir Market Insight

The Germany remdesivir market is expected to expand at a considerable CAGR during the forecast period, fueled by high awareness of antiviral therapies and increasing demand in hospital and critical care settings. Hospitals and clinics prioritize remdesivir for moderate-to-severe viral infections due to clinical guidelines and emergency use approvals. Germany’s advanced healthcare infrastructure and focus on innovative treatments drive adoption across both public and private sectors. The integration of remdesivir into standardized hospital protocols supports consistent dosing and patient outcomes. In addition, collaborations between pharmaceutical companies and healthcare providers ensure adequate supply and availability. Growing awareness of the importance of timely antiviral administration reinforces market growth.

Asia-Pacific Remdesivir Market Insight

The Asia-Pacific remdesivir market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by rising COVID-19 cases, increasing hospitalizations, and expanding healthcare infrastructure in countries such as China, India, and Japan. Government initiatives to improve hospital and ICU capacity, along with growing adoption of standardized antiviral treatment protocols, are accelerating remdesivir uptake. The region’s increasing focus on epidemic preparedness and critical care capacity further supports market expansion. In addition, improving cold chain logistics and local manufacturing capabilities enhance accessibility and affordability. Rising awareness among healthcare providers about clinical efficacy and dosing guidelines is also driving adoption. Emerging telemedicine platforms are facilitating early diagnosis and timely antiviral administration.

Japan Remdesivir Market Insight

The Japan remdesivir market is gaining momentum due to a high prevalence of viral infections, advanced hospital infrastructure, and increasing adoption of standardized treatment protocols. Hospitals and clinics are the primary end users, leveraging remdesivir for moderate-to-severe COVID-19 and other viral cases. Integration of antiviral therapy into critical care and ICU protocols ensures consistent dosing and monitoring. Government stockpiling and streamlined procurement channels further support availability. In addition, ongoing clinical trials and research collaborations are promoting expanded indications and use. Growing awareness among physicians about antiviral efficacy and safety profiles is increasing market adoption.

India Remdesivir Market Insight

The India remdesivir market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the rising prevalence of COVID-19 and other viral infections, expanding hospital infrastructure, and increased ICU capacity. Hospitals and clinics are the primary end users, administering remdesivir for moderate-to-severe cases under standardized protocols. The government’s initiatives for antiviral stockpiling and procurement ensure consistent supply across healthcare facilities. In addition, growing awareness among physicians and patients regarding treatment efficacy supports adoption. Local manufacturing and increasing affordability of remdesivir are key factors driving market growth. Telemedicine and outpatient care programs further facilitate early diagnosis and timely administration, enhancing accessibility in urban and semi-urban regions.

Remdesivir Market Share

The Remdesivir industry is primarily led by well-established companies, including:

- Gilead Sciences, Inc. (U.S.)

- Cipla Ltd (India)

- Hetero Labs Ltd (India)

- Dr. Reddy’s Laboratories Ltd (India)

- Sun Pharmaceutical Industries Ltd (India)

- Zydus Lifesciences Ltd (India)

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Novartis AG (Switzerland)

- Lupin (India)

- Biocon Limited (India)

- Syngene International Ltd (India)

- Viatris Inc. (U.S.)

- Beximco Pharmaceuticals Ltd (Bangladesh)

- Jubilant Life Sciences Ltd (India)

- Aurobindo Pharma Ltd (India)

- Emergent BioSolutions (U.S.)

What are the Recent Developments in Global Remdesivir Market?

- In January 2025, the World Health Organization (WHO) and partners enabled access to candidate vaccines and treatments including antivirals relevant to Ebola‑family outbreaks to support Uganda’s response to a Sudan virus disease outbreak, facilitating deployment of remdesivir and other therapeutic options as part of outbreak preparedness and response efforts

- In August 2023, the U.S. FDA also approved an update to Veklury®’s label to allow use in people with mild to severe hepatic impairment without dose adjustment, expanding its safety profile and access for patients with liver disease at high risk of COVID‑19 complications

- In July 2023, the U.S. FDA approved a supplemental new drug application for Veklury® (remdesivir) for COVID‑19 treatment in patients with severe renal impairment, including those on dialysis, making it the first antiviral approved across all stages of renal disease without required dose adjustments

- In April 2023, Gilead reported positive Phase 3 and real‑world evidence demonstrating safety and efficacy of remdesivir in people with moderate to severe renal impairment as well as reduced mortality and readmission rates among immunocompromised patients across COVID‑19 variants, reinforcing its clinical utility in vulnerable population

- In January 2022, the U.S. Food and Drug Administration (FDA) approved Veklury® (remdesivir) for the treatment of non‑hospitalized patients at high risk of COVID‑19 progression, allowing outpatient use of the antiviral and expanding its indications beyond hospitalized cases based on Phase 3 data showing significant reduction in hospitalization risk

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.