Global Respiratory Syncytial Virus Treatment Market

Market Size in USD Billion

USD

1.35 Billion

USD

1.88 Billion

2024

2032

USD

1.35 Billion

USD

1.88 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.35 Billion | |

| USD 1.88 Billion | |

| % | |

|

Respiratory Syncytial Virus Treatment Market Size

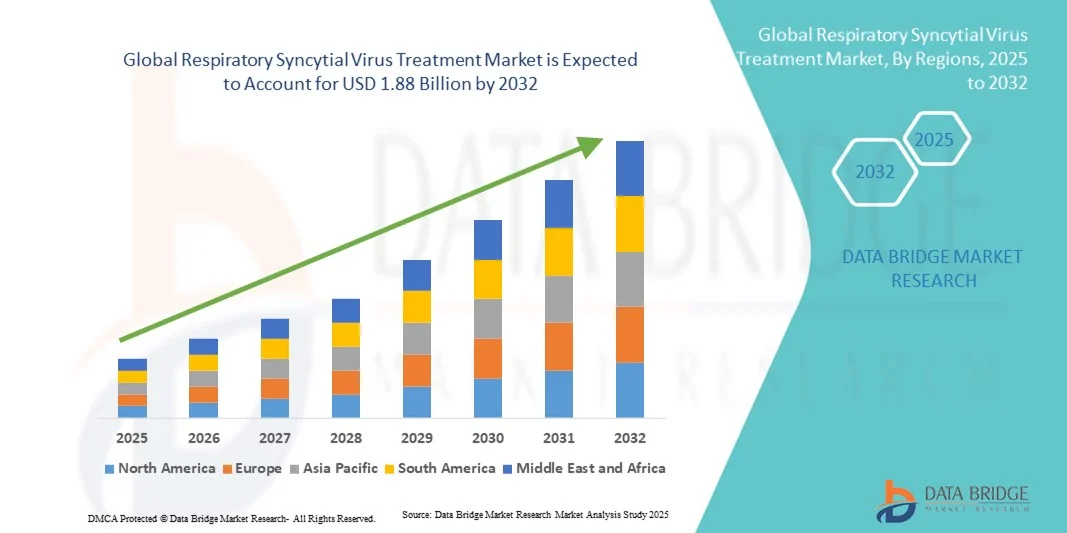

- The global respiratory syncytial virus treatment market size was valued at USD 1.35 billion in 2024 and is expected to reach USD 1.88 billion by 2032, at a CAGR of 4.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of RSV infections, particularly among infants, young children, and older adults, along with the development of innovative treatment options and growing awareness of the disease

- Furthermore, rising demand for effective, safe, and early intervention therapeutics is establishing RSV treatments as a critical component of respiratory healthcare. These converging factors are accelerating the uptake of RSV therapies, thereby significantly boosting the industry's growth

Respiratory Syncytial Virus Treatment Market Analysis

- RSV treatments, including antivirals, monoclonal antibodies, and supportive care therapies, are increasingly vital components of pediatric and adult respiratory healthcare due to their ability to prevent severe infections, reduce hospitalizations, and improve patient outcomes

- The escalating demand for RSV therapeutics is primarily fueled by the rising prevalence of RSV infections, growing awareness among healthcare providers and caregivers, and the increasing focus on early intervention and preventive care

- North America dominated the global respiratory syncytial virus treatment market with the largest revenue share of 39.7% in 2024, characterized by advanced healthcare infrastructure, high awareness of RSV prophylaxis, and a strong presence of key pharmaceutical players, with the U.S. experiencing substantial uptake of RSV diagnostics and treatments, driven by innovations from both established biopharma companies and startups focusing on advanced diagnostic and therapeutic solutions

- Asia-Pacific is expected to be the fastest growing region in the global respiratory syncytial virus treatment market during the forecast period due to increasing healthcare access, rising healthcare expenditure, and growing awareness of RSV-related complications among infants and the elderly

- Molecular diagnostics segment dominated the global respiratory syncytial virus treatment market with a market share of 42.9% in 2024, driven by its high sensitivity and specificity in detecting RSV infections and the expanding adoption of rapid and accurate diagnostic methods in hospitals and specialty clinics worldwide

Report Scope and Respiratory Syncytial Virus Treatment Market Segmentation

|

Attributes |

Respiratory Syncytial Virus Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Respiratory Syncytial Virus Treatment Market Trends

Advancements in Rapid Diagnostics and Point-of-Care Testing

- A significant and accelerating trend in the global RSV treatment market is the growing adoption of rapid antigen diagnostic tests (RADTs) and molecular diagnostics, which enable faster and more accurate detection of RSV infections at the point of care

- For instance, the Alere™ RSV Test allows clinicians to detect RSV within minutes, helping to guide immediate treatment decisions and reduce hospital stays

- Integration of these diagnostic tools with electronic health records (EHRs) and telemedicine platforms is enhancing workflow efficiency, enabling timely patient management and improved epidemiological tracking

- Advanced diagnostic platforms facilitate simultaneous detection of RSV and other respiratory pathogens, reducing misdiagnosis and enabling more targeted therapeutic interventions

- This trend towards rapid, reliable, and integrated diagnostic solutions is reshaping clinical protocols for RSV management, allowing healthcare providers to implement early interventions and preventive strategies effectively

- The demand for faster and highly sensitive RSV diagnostics is growing across hospitals, specialty clinics, and home healthcare settings as clinicians prioritize timely detection to minimize complications

Respiratory Syncytial Virus Treatment Market Dynamics

Driver

Increasing Disease Burden and Pediatric Healthcare Focus

- The rising prevalence of RSV infections, particularly among infants, young children, and the elderly, is a significant driver for the growing demand for effective RSV therapeutics

- For instance, the U.S. CDC reported a surge in RSV hospitalizations among infants during the 2023–2024 season, prompting greater adoption of prophylactic monoclonal antibodies in high-risk populations

- As awareness about RSV complications increases among healthcare providers and caregivers, the use of preventive and therapeutic interventions is expanding rapidly

- Furthermore, the growing focus on pediatric healthcare infrastructure, early diagnosis, and preventive care programs is making RSV treatment an essential component of respiratory healthcare

- Availability of advanced monoclonal antibodies, antivirals, and supportive therapies enables healthcare providers to reduce the severity of infections and improve clinical outcome

- Rising government initiatives, healthcare spending, and education campaigns on RSV prevention are further accelerating the uptake of treatment solutions across multiple regions

Restraint/Challenge

High Cost of Treatment and Limited Awareness in Emerging Markets

- The high cost of monoclonal antibodies and advanced RSV therapies poses a challenge to broader market adoption, particularly in price-sensitive regions and developing countries

- For instance, the prophylactic RSV antibody Synagis requires repeated dosing, making it less accessible for families in low-income areas despite proven efficacy

- Limited awareness about RSV infections and preventive treatment options among caregivers in emerging markets further hinders widespread adoption

- Healthcare infrastructure limitations, including fewer specialized clinics and diagnostic facilities, restrict timely access to RSV treatment in remote or underdeveloped areas

- Insurance coverage gaps and reimbursement constraints in certain regions add another barrier to patient access for high-cost RSV therapeutics

- Addressing these challenges through awareness campaigns, cost-reduction strategies, and expanded healthcare access will be critical for sustained market growth

Respiratory Syncytial Virus Treatment Market Scope

The market is segmented on the basis of test, route of administration, end user, mode of purchase, and distribution channel.

- By Test

On the basis of test, the global respiratory syncytial virus treatment market is segmented into rapid antigen diagnostic test (RADT), direct fluorescent antibody (DFA) method, molecular diagnostics, chromatography immunoassay, flow cytometry, diagnostic imaging, and gel microdroplets. the Molecular Diagnostics segment dominated the market with the largest revenue share of 42.9% in 2024, driven by its high sensitivity and specificity in detecting RSV infections. Hospitals and specialty clinics often prioritize molecular diagnostics for their ability to provide rapid and accurate results, enabling timely treatment interventions. The segment benefits from integration with electronic health records (EHR) and telemedicine platforms, supporting improved patient management and epidemiological tracking. In addition, molecular diagnostics facilitate differentiation between RSV and other respiratory pathogens, reducing misdiagnosis and guiding targeted therapeutic decisions. The rising adoption of point-of-care molecular assays in pediatric and geriatric populations further boosts its market dominance. High reliability, ease of integration into clinical workflows, and growing physician preference contribute to its sustained market leadership.

The Rapid Antigen Diagnostic Test (RADT) segment is anticipated to witness the fastest growth rate of 19.5% from 2025 to 2032, fueled by the increasing demand for quick, on-site RSV detection. RADTs offer results in minutes, enabling healthcare providers to make immediate treatment decisions and minimize the risk of severe complications. Their portability and ease of use make them particularly suitable for outpatient clinics, home healthcare, and remote testing environments. Rising awareness among caregivers and clinicians about the benefits of early RSV detection supports RADT adoption. Furthermore, cost-effectiveness and minimal infrastructure requirements enhance their appeal in emerging markets. The ongoing development of next-generation RADTs with improved sensitivity and multiplexing capabilities is expected to further accelerate growth.

- By Route of Administration

On the basis of route of administration, the global respiratory syncytial virus treatment market is segmented into oral, intravenous, and others. The Intravenous segment dominated the market in 2024, driven by the widespread use of monoclonal antibodies such as Palivizumab for high-risk infants. Intravenous administration allows precise dosing and rapid therapeutic effects, making it the preferred choice in hospitals and specialty clinics. Its dominance is supported by clinical guidelines recommending IV administration for severe RSV cases and prophylaxis in vulnerable populations. The segment also benefits from ongoing advancements in formulation and delivery methods that enhance efficacy and reduce adverse effects. High physician preference and well-established protocols contribute to sustained revenue share. Hospital-based administration ensures monitoring and reduces potential complications, reinforcing the segment’s leadership.

The Oral segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the development of novel oral antivirals for RSV treatment. Oral therapeutics offer convenience, enable outpatient management, and increase patient compliance, especially for pediatric and home-care settings. Growing research into small-molecule antivirals with favorable safety profiles supports adoption. The segment is further fueled by telemedicine and home healthcare expansion, allowing treatment without hospital visits. Rising investments in oral RSV drug development and regulatory approvals are such asly to accelerate market penetration.

- By End User

On the basis of end user, the global respiratory syncytial virus treatment market is segmented into hospitals, specialty clinics, and home healthcare. The Hospitals segment dominated the market in 2024 due to the high prevalence of severe RSV cases requiring inpatient care and monitoring. Hospitals benefit from access to advanced diagnostics, intravenous therapies, and multidisciplinary teams capable of managing complications. They also lead in administering prophylactic monoclonal antibodies for high-risk infants and elderly patients. The segment is supported by established infrastructure, trained healthcare professionals, and adherence to clinical guidelines. High hospitalization rates during RSV outbreaks further reinforce hospitals as the largest revenue contributor.

The Home Healthcare segment is expected to witness the fastest growth rate from 2025 to 2032, driven by increasing adoption of at-home RSV testing, oral antivirals, and telemedicine monitoring. The convenience of home-based care reduces the burden on hospitals and supports timely intervention for mild to moderate cases. Growing awareness among caregivers and increasing availability of portable diagnostics contribute to adoption. Home healthcare also benefits from technological advancements such as remote monitoring devices and connected health platforms. Rising demand in developed and emerging markets for cost-effective, patient-centric care is expected to further accelerate segment growth.

- By Mode of Purchase

On the basis of mode of purchase, the global respiratory syncytial virus treatment market is segmented into prescription and over the counter. The Prescription segment dominated the market in 2024 due to the requirement for controlled administration of monoclonal antibodies and antiviral therapies. Prescriptions ensure proper dosing, monitoring, and adherence to clinical protocols, particularly in pediatric and elderly populations. The segment benefits from physician oversight, hospital protocols, and regulatory compliance, supporting high revenue share. Clinical safety, efficacy data, and insurance coverage further reinforce reliance on prescription-based RSV treatments.

The Over the Counter (OTC) segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing availability of rapid diagnostic tests, supportive care medications, and symptom-relief formulations for RSV. OTC products empower caregivers to identify infections early, manage mild symptoms at home, and reduce unnecessary hospital visits. Growing awareness, convenience, and expansion of retail and online pharmacies accelerate adoption. Regulatory approvals and simplified access to point-of-care diagnostics further boost the segment.

- By Distribution Channel

On the basis of distribution channel, the global respiratory syncytial virus treatment market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The Hospital Pharmacies segment dominated the market in 2024, driven by the central role hospitals play in administering intravenous therapies and managing high-risk RSV patients. Hospital pharmacies ensure availability of prescription monoclonal antibodies and antivirals, aligned with clinical guidelines. Integration with hospital EHR systems enhances inventory management and patient safety. The segment benefits from direct hospital procurement, bulk purchasing, and controlled distribution, contributing to high revenue share.

The Online Pharmacies segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing digital adoption, telemedicine expansion, and the convenience of home delivery. Online platforms allow caregivers to access OTC medications, diagnostics, and some prescription treatments efficiently. Rising e-commerce penetration, consumer trust in online services, and competitive pricing further drive growth. The segment also benefits from partnerships with telehealth providers and improved logistics infrastructure, enabling timely delivery of RSV therapeutics and supporting home healthcare expansion.

Respiratory Syncytial Virus Treatment Market Regional Analysis

- North America dominated the global respiratory syncytial virus treatment market with the largest revenue share of 39.7% in 2024, characterized by advanced healthcare infrastructure, high awareness of RSV prophylaxis, and a strong presence of key pharmaceutical players

- Healthcare providers in the region highly value rapid diagnostics, effective monoclonal antibodies, and antivirals, along with the integration of these treatments into hospital protocols and electronic health record systems for better patient management

- This widespread adoption is further supported by robust government initiatives, high healthcare expenditure, and strong presence of key pharmaceutical and biotech companies, establishing RSV treatments as a preferred solution for both pediatric and adult populations across hospitals, specialty clinics, and home healthcare settings

U.S. Respiratory Syncytial Virus Treatment Market Insight

The U.S. respiratory syncytial virus treatment market captured the largest revenue share of 82% in 2024 within North America, fueled by the high prevalence of RSV infections among infants, young children, and older adults. Healthcare providers increasingly prioritize the use of monoclonal antibodies, antivirals, and rapid diagnostics to prevent severe RSV complications. The growing adoption of pediatric preventive care programs, combined with advanced hospital infrastructure and strong insurance coverage, further propels the market. Moreover, integration of RSV diagnostics with electronic health records (EHRs) and telemedicine platforms is significantly contributing to timely treatment and market expansion.

Europe Respiratory Syncytial Virus (RSV) Treatment Market Insight

The Europe respiratory syncytial virus treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of RSV infections and government initiatives promoting early diagnosis and preventive care. Increasing urbanization, coupled with advanced healthcare infrastructure, is fostering the adoption of RSV therapeutics. European healthcare providers are also drawn to rapid diagnostics and monoclonal antibody therapies due to their proven efficacy in preventing severe infections. The region is experiencing significant growth across hospitals, specialty clinics, and home healthcare, with RSV treatments being integrated into both routine pediatric and geriatric care.

U.K. Respiratory Syncytial Virus (RSV) Treatment Market Insight

The U.K. respiratory syncytial virus treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing focus on pediatric healthcare and heightened awareness of RSV-related complications. In addition, rising concern regarding infant hospitalizations and respiratory illnesses is encouraging healthcare providers to adopt preventive and therapeutic interventions. The U.K.’s robust healthcare system, coupled with advanced diagnostics and telehealth adoption, is expected to continue stimulating market growth. Moreover, growing emphasis on home-based care and outpatient treatment programs supports the expanding demand for RSV therapeutics.

Germany Respiratory Syncytial Virus (RSV) Treatment Market Insight

The Germany respiratory syncytial virus treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of respiratory infections and demand for technologically advanced treatment options. Germany’s well-developed healthcare infrastructure, combined with a focus on preventive care and innovation, promotes the adoption of RSV diagnostics and monoclonal antibody therapies. Integration of RSV management protocols with electronic patient records and hospital-based monitoring systems is becoming increasingly prevalent. In addition, growing emphasis on geriatric and pediatric care aligns with local healthcare priorities, supporting market growth.

Asia-Pacific Respiratory Syncytial Virus (RSV) Treatment Market Insight

The Asia-Pacific respiratory syncytial virus treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing healthcare access, rising disposable incomes, and awareness about RSV complications in countries such as China, Japan, and India. The region's growing focus on early diagnosis, supported by government healthcare initiatives, is driving the adoption of RSV therapeutics. Furthermore, as APAC emerges as a manufacturing hub for RSV diagnostics and therapeutics, affordability and accessibility are expanding, enabling wider adoption in both urban and semi-urban areas.

Japan Respiratory Syncytial Virus (RSV) Treatment Market Insight

The Japan respiratory syncytial virus treatment market is gaining momentum due to the country’s advanced healthcare system, growing focus on infant and elderly care, and adoption of cutting-edge diagnostics. Japanese healthcare providers emphasize preventive interventions using monoclonal antibodies and rapid testing, particularly in high-risk populations. The integration of RSV treatment protocols with digital health platforms and home healthcare services is fueling growth. Moreover, Japan's aging population is such asly to spur demand for easier-to-administer, safe, and effective RSV therapies in both residential and clinical settings.

India Respiratory Syncytial Virus (RSV) Treatment Market Insight

The India respiratory syncytial virus treatment market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to the country’s rising awareness of RSV infections, expanding pediatric healthcare infrastructure, and growing disposable incomes. India is witnessing increasing adoption of rapid diagnostics, monoclonal antibodies, and supportive therapies in hospitals, specialty clinics, and home healthcare. Government initiatives promoting immunization and preventive care, alongside the availability of cost-effective treatment options, are key factors propelling the market. The strong presence of domestic pharmaceutical manufacturers and telemedicine platforms further supports widespread access to RSV therapeutics.

Respiratory Syncytial Virus Treatment Market Share

The Respiratory Syncytial Virus Treatment industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Moderna, Inc. (U.S.)

- AbbVie Ltd (U.S.)

- GSK plc (U.K.)

- Novavax, Inc. (U.S.)

- Arcturus Therapeutics Holdings Inc. (U.S.)

- Vaxart, Inc. (U.S.)

- Boehringer Ingelheim International GmbH (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Abbott (U.S.)

- Enanta Pharmaceuticals, Inc. (U.S.)

- Emergent BioSolutions Inc. (U.S.)

- Bayer AG (Germany)

- Baxter (U.S.)

- Lilly USA, LLC. (U.S.)

What are the Recent Developments in Global Respiratory Syncytial Virus Treatment Market?

- In July 2025, a CDC advisory panel approved Merck’s new RSV preventive shot, Enflonsia (clesrovimab), for infants. The monoclonal antibody is designed for babies 8 months or younger during their first RSV season

- In June 2025, the U.S. Food and Drug Administration approved Merck's new monoclonal antibody, clesrovimab (brand name Enflonsia), as a single-dose preventive treatment against respiratory syncytial virus (RSV) for infants up to one year old

- In March 2024, a study by the Centers for Disease Control and Prevention (CDC) found that the antibody therapy developed by AstraZeneca and Sanofi, branded as Beyfortus and known as nirsevimab, is 90% effective in preventing hospitalizations of infants due to respiratory syncytial virus (RSV)

- In November 2023, reports indicated a shortage of RSV treatments, including the newly approved nirsevimab, due to unexpectedly high demand. The CDC recommended prioritizing the drug for high-risk infants, including those under six months and those with heart and lung conditions

- In July 2023, the U.S. Food and Drug Administration approved Beyfortus (nirsevimab-alip), a long-acting monoclonal antibody developed by Sanofi and AstraZeneca, for the prevention of respiratory syncytial virus (RSV) lower respiratory tract disease in neonates and infants born during or entering their first RSV season, and in children up to 24 months of age who remain vulnerable to severe RSV disease through their second RSV season

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.