Global Returnable Packaging Market

Market Size in USD Billion

USD

58.33 Billion

USD

92.97 Billion

2025

2033

USD

58.33 Billion

USD

92.97 Billion

2025

2033

| 2026 - 2033 | |

| USD 58.33 Billion | |

| USD 92.97 Billion | |

| % | |

|

What is the Returnable Packaging Market Size and Overview?

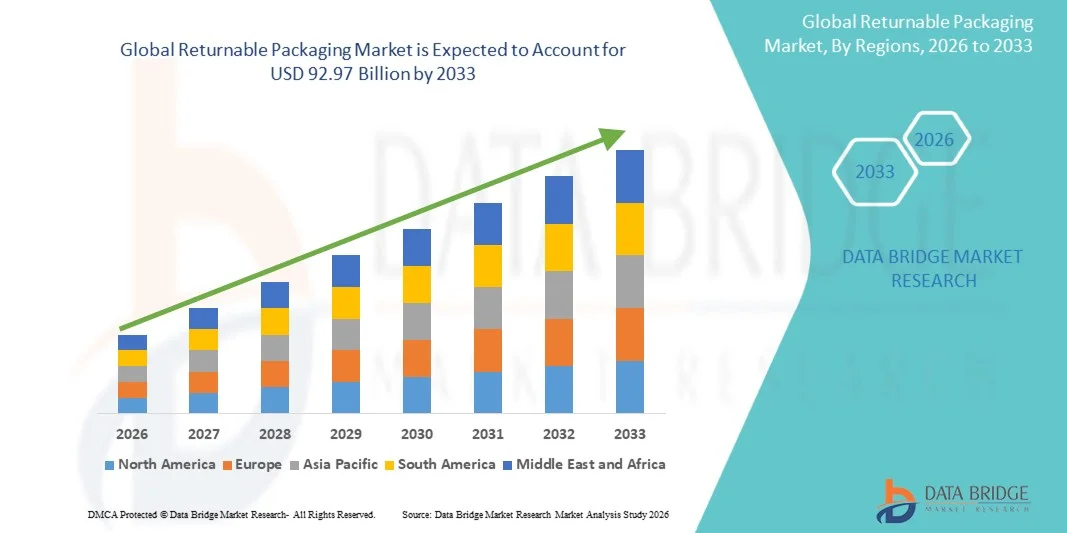

As per Data Bridge Market Research Analysis the global Returnable Packaging Market was valued at USD 58.33 billion in 2025 and is projected to reach USD 92.97 billion by 2033, growing at a CAGR of 6.00% from 2026 to 2033. The market is experiencing steady growth driven by increasing emphasis on circular economy practices, rising demand for sustainable packaging solutions, and expanding adoption of reusable containers, pallets, crates, and bulk packaging across food and beverage, automotive, retail, pharmaceutical, and logistics industries.

Growing concerns regarding single-use plastic waste, combined with stricter packaging waste regulations and corporate sustainability commitments, are encouraging manufacturers, retailers, and logistics providers to shift toward reusable packaging systems. Returnable packaging enables repeated use over multiple supply chain cycles, helping companies reduce material consumption, lower packaging waste generation, and improve long-term operational efficiency. The integration of RFID, QR codes, and IoT-based tracking technologies is further strengthening returnable packaging adoption by improving asset visibility, reducing container losses, and supporting efficient reverse logistics operations across global supply chains.

Market Size & Forecast

- Global Market Value (2025): USD 58.33 Billion

- Expected Market Value (2033): USD 92.97 Billion

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the returnable packaging market with the largest revenue share of approximately 36.8% in 2025, supported by the presence of advanced logistics infrastructure, strong adoption of closed-loop supply chain systems, and growing demand for sustainable packaging solutions. The region’s food and beverages, automotive, healthcare, retail, and e-commerce industries are increasingly using reusable pallets, plastic crates, bulk containers, and dunnage to improve operational efficiency and reduce packaging waste.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 7.2% from 2026 to 2033. Growth is driven by rapid industrialization, expanding e-commerce activity, increasing food and beverage production, and rising investments in automotive manufacturing and logistics infrastructure. The growing availability of cost-effective reusable plastic pallets, crates, and containers is further supporting the adoption of returnable packaging solutions across emerging economies.

- The pallets segment held the largest market revenue share of approximately 56.5% in 2025, driven by its extensive use in closed-loop logistics systems across food and beverages, automotive, healthcare, retail, and industrial manufacturing. Returnable pallets are preferred due to their high load-bearing capacity, compatibility with forklifts and automated warehousing systems, and ability to reduce packaging waste across repeated distribution cycles.

- The intermediate bulk containers (IBCs) segment is projected to register the fastest growth from 2026 to 2033, supported by rising demand for safe and reusable bulk transportation of liquids, powders, chemicals, pharmaceutical ingredients, and food products. IBCs are increasingly adopted due to their space-efficient design, improved product protection, lower handling costs, and suitability for reverse logistics networks. The growing use of foldable and RFID-enabled IBCs is further supporting segment expansion across chemical processing, food manufacturing, and pharmaceutical supply chains.

- The plastic segment held the largest market revenue share of approximately 63.4% in 2025, driven by the widespread use of plastic pallets, crates, totes, trays, and IBCs across high-volume distribution networks. Plastic returnable packaging is preferred due to its lightweight structure, moisture resistance, ease of cleaning, long service life, and ability to lower transportation costs compared with heavier alternatives.

- The metal segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand for heavy-duty returnable containers, steel pallets, wire mesh crates, and industrial drums in automotive, chemicals, machinery, and manufacturing applications. Metal packaging offers superior strength, impact resistance, and durability in demanding operating conditions, making it suitable for transporting heavy components and hazardous materials. Growing adoption of durable reusable packaging assets in industrial supply chains is expected to support segment growth.

- The food and beverages segment held the largest market revenue share of approximately 34.4% in 2025, driven by the high frequency of product movement across beverage bottling, dairy, bakery, fresh produce, frozen food, and grocery distribution operations. Reusable crates, pallets, bottles, and insulated containers are increasingly used to improve hygiene, minimize product damage, and support cost-efficient closed-loop supply chain operations.

- The healthcare segment is projected to register the fastest growth from 2026 to 2033, supported by rising pharmaceutical production, expanding medical device distribution, and stringent requirements for hygienic and damage-resistant packaging. Returnable containers are increasingly used for transporting medical instruments, laboratory equipment, diagnostic products, and pharmaceutical materials while supporting traceability and controlled handling. The growing use of specialized reusable packaging in temperature-sensitive healthcare logistics is expected to accelerate segment expansion.

Report Scope and Returnable Packaging Market Segmentation

|

Attributes |

Returnable Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

|

What is the Key Trend in the Returnable Packaging Market Market?

Trend: Expansion Of Circular Economy Models And Reusable Transport Packaging Systems

Increasing emphasis on waste reduction, material efficiency, and sustainable supply chain operations is accelerating the adoption of returnable packaging across food and beverage, automotive, retail, pharmaceuticals, and industrial manufacturing sectors. Unlike single-use packaging, returnable crates, pallets, intermediate bulk containers, drums, and reusable plastic containers can complete multiple distribution cycles, reducing packaging waste generation and lowering long-term procurement costs for end users.

For instance, major beverage companies are expanding refillable bottle systems and reusable crate networks to reduce dependence on virgin packaging materials. In automotive manufacturing, reusable plastic pallets, dunnage trays, and bulk containers are increasingly used for transporting components between suppliers and assembly plants, helping reduce product damage and improve material handling efficiency. The European Union Packaging and Packaging Waste Regulation is also encouraging businesses to increase reuse and refill systems, creating stronger demand for durable and traceable returnable packaging solutions.

Digital tracking technologies, including RFID tags, QR codes, and IoT-enabled sensors, are further improving the management of reusable packaging pools by enabling companies to monitor asset location, circulation frequency, loss rates, and maintenance requirements. For instance, pooled pallet and crate operators are increasingly using digital asset management platforms to improve return rates and optimize reverse logistics operations. Growing adoption of reusable packaging systems is expected to support circular supply chains while reducing the environmental burden associated with disposable packaging.

Returnable Packaging Market Dynamics

Key Market Driver: Rising Demand For Sustainable Packaging And Waste Reduction Solutions

Governments, businesses, and consumers are increasingly prioritizing sustainable packaging solutions due to growing concerns regarding plastic waste, landfill accumulation, and carbon emissions associated with single-use packaging. Returnable packaging provides a practical alternative by allowing containers, pallets, crates, and bulk handling units to be collected, cleaned, repaired, and reused across multiple supply chain cycles.

Food and beverage manufacturers are expanding the use of reusable crates, bottles, and transport containers to reduce packaging waste and improve logistics efficiency. For instance, reusable plastic crates are widely used in fresh produce, dairy, bakery, and beverage distribution because they provide better product protection and can withstand repeated handling during transportation and storage. In addition, automotive and industrial manufacturers are adopting reusable dunnage and custom-engineered containers to minimize component damage and reduce recurring packaging procurement expenses.

Regulatory measures supporting recycling, reuse, and extended producer responsibility are also strengthening market demand. The European Union has set targets to reduce packaging waste and increase the use of reusable packaging systems across transport, food service, and e-commerce applications. These regulatory developments are encouraging brand owners, retailers, and logistics providers to invest in durable returnable packaging assets and reverse logistics infrastructure, supporting long-term market expansion.

Key Restraint/Challenge: High Initial Investment And Complex Reverse Logistics Operations

Returnable packaging systems require higher upfront investment than conventional single-use packaging because businesses must purchase durable containers, establish collection systems, and invest in cleaning, repair, sorting, and tracking infrastructure. Small and medium-sized enterprises may face challenges in adopting these systems due to limited capital availability and uncertainty regarding the return on investment.

The effectiveness of returnable packaging depends heavily on efficient reverse logistics. Containers must be returned from retailers, consumers, warehouses, and distribution centers to designated collection points before they can be cleaned and reused. Lost, damaged, or improperly handled packaging assets can increase operating costs and reduce the financial benefits of reuse programs. For instance, pallet, crate, and container pooling systems require strong coordination among manufacturers, logistics providers, distributors, and end users to maintain high circulation rates.

In addition, cleaning and sanitation requirements can create operational complexity in food, beverage, pharmaceutical, and healthcare applications. Companies must ensure that reusable packaging meets hygiene, safety, and quality standards before each reuse cycle. Rising transportation costs, fragmented collection networks, and limited reverse logistics infrastructure in developing economies may further restrict the wider adoption of returnable packaging solutions.

Key Market Opportunity: Growth Of Reusable Packaging In E-Commerce And Organized Retail

The rapid expansion of e-commerce, organized retail, grocery delivery, and omnichannel distribution is creating substantial opportunities for returnable packaging providers. Online retailers and logistics companies require durable packaging solutions that can protect products during repeated handling, sorting, transportation, and last-mile delivery while reducing the volume of disposable cardboard and plastic packaging waste.

Reusable delivery boxes, foldable crates, insulated containers, and returnable transport packaging are increasingly being introduced for grocery, meal-kit, apparel, electronics, and pharmaceutical deliveries. For instance, reusable tote systems are being used by grocery retailers to transport fresh food products from distribution centers to stores, helping improve stackability, product visibility, and handling efficiency. Returnable packaging also supports automated warehousing operations by providing standardized dimensions compatible with conveyors, robotic picking systems, and storage equipment.

The increasing use of RFID-enabled returnable containers offers additional opportunities for companies to improve asset utilization and reduce losses across complex supply chains. Digital tracking allows operators to identify container movement, monitor inventory levels, and improve the recovery of reusable assets from customers and distribution partners. As businesses increasingly adopt circular economy strategies and seek to reduce packaging-related emissions, demand for technologically advanced, lightweight, and high-durability returnable packaging systems is expected to increase.

Returnable Packaging Market Scope

The market is segmented on the basis of product type, material type, and end user.

- By Product Type

On the basis of product type, the returnable packaging market is segmented into pallets, crates, intermediate bulk containers (IBCs), drums and barrels, bottles, dunnage, and others. The pallets segment held the largest market revenue share of approximately 56.5% in 2025, driven by its extensive use in closed-loop logistics systems across food and beverages, automotive, healthcare, retail, and industrial manufacturing. Returnable pallets are preferred due to their high load-bearing capacity, compatibility with forklifts and automated warehousing systems, and ability to reduce packaging waste across repeated distribution cycles.

The intermediate bulk containers (IBCs) segment is projected to register the fastest growth from 2026 to 2033, supported by rising demand for safe and reusable bulk transportation of liquids, powders, chemicals, pharmaceutical ingredients, and food products. IBCs are increasingly adopted due to their space-efficient design, improved product protection, lower handling costs, and suitability for reverse logistics networks. The growing use of foldable and RFID-enabled IBCs is further supporting segment expansion across chemical processing, food manufacturing, and pharmaceutical supply chains.

- By Material Type

On the basis of material type, the returnable packaging market is segmented into plastic, metal, wood, glass, and foam. The plastic segment held the largest market revenue share of approximately 63.4% in 2025, driven by the widespread use of plastic pallets, crates, totes, trays, and IBCs across high-volume distribution networks. Plastic returnable packaging is preferred due to its lightweight structure, moisture resistance, ease of cleaning, long service life, and ability to lower transportation costs compared with heavier alternatives.

The metal segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing demand for heavy-duty returnable containers, steel pallets, wire mesh crates, and industrial drums in automotive, chemicals, machinery, and manufacturing applications. Metal packaging offers superior strength, impact resistance, and durability in demanding operating conditions, making it suitable for transporting heavy components and hazardous materials. Growing adoption of durable reusable packaging assets in industrial supply chains is expected to support segment growth.

- By End User

On the basis of end user, the returnable packaging market is segmented into automotive, food and beverages, consumer durables, healthcare, and others. The food and beverages segment held the largest market revenue share of approximately 34.4% in 2025, driven by the high frequency of product movement across beverage bottling, dairy, bakery, fresh produce, frozen food, and grocery distribution operations. Reusable crates, pallets, bottles, and insulated containers are increasingly used to improve hygiene, minimize product damage, and support cost-efficient closed-loop supply chain operations.

The healthcare segment is projected to register the fastest growth from 2026 to 2033, supported by rising pharmaceutical production, expanding medical device distribution, and stringent requirements for hygienic and damage-resistant packaging. Returnable containers are increasingly used for transporting medical instruments, laboratory equipment, diagnostic products, and pharmaceutical materials while supporting traceability and controlled handling. The growing use of specialized reusable packaging in temperature-sensitive healthcare logistics is expected to accelerate segment expansion.

Returnable Packaging Market Regional Analysis

North America Returnable Packaging Market Insight

North America dominated the returnable packaging market with the largest revenue share of approximately 36.8% in 2025, supported by the strong presence of organized retail, advanced logistics networks, and well-established closed-loop supply chain systems. Companies across food and beverages, automotive, healthcare, and consumer goods industries are increasingly adopting reusable pallets, crates, bulk containers, and dunnage to reduce packaging waste and improve material handling efficiency. The region’s focus on sustainable packaging, combined with growing investment in reverse logistics and asset-tracking technologies, is further supporting the widespread adoption of returnable packaging solutions across commercial and industrial applications.

U.S. Returnable Packaging Market Insight

The U.S. returnable packaging market captured the largest revenue share in 2025 within North America, driven by rising demand for reusable transport packaging across food distribution, automotive manufacturing, e-commerce, and pharmaceutical supply chains. Businesses are increasingly shifting toward reusable pallets, plastic crates, IBCs, and bulk containers to lower recurring packaging expenses and comply with sustainability commitments. The growing use of RFID-enabled packaging assets, automated warehousing systems, and third-party logistics services is further improving container tracking, return rates, and operational visibility, thereby accelerating market expansion across the country.

Europe Returnable Packaging Market Insight

The Europe returnable packaging market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent packaging waste regulations, circular economy initiatives, and increasing demand for reusable transport packaging across manufacturing and retail sectors. European businesses are increasingly replacing single-use packaging with reusable crates, pallets, bottles, and containers to reduce landfill waste and improve resource efficiency. The region’s well-developed collection, sorting, and reverse logistics infrastructure is enabling efficient reuse cycles, while rising demand from food and beverages, automotive, and e-commerce industries continues to strengthen market growth.

U.K. Returnable Packaging Market Insight

The U.K. returnable packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing emphasis on sustainable supply chains, packaging waste reduction, and reusable delivery solutions. Retailers, food service operators, and e-commerce companies are increasingly introducing returnable crates, reusable delivery boxes, and refillable packaging formats to reduce dependence on disposable materials. The growing adoption of online grocery delivery, expanding reverse logistics networks, and rising consumer awareness regarding sustainable consumption are expected to further stimulate demand for returnable packaging systems across the country.

Germany Returnable Packaging Market Insight

The Germany returnable packaging market accounted for the largest market revenue share in Europe in 2025, attributed to the country’s mature deposit-return infrastructure, strong manufacturing base, and high adoption of circular economy practices. Germany has a well-established market for reusable beverage bottles, transport crates, pallets, and industrial containers, particularly across food and beverages, automotive, chemicals, and retail applications. The country’s strict waste management policies, combined with growing investment in reusable packaging pools and digital asset-tracking solutions, are supporting continued market expansion across commercial and industrial supply chains.

Asia-Pacific Returnable Packaging Market Insight

The Asia-Pacific returnable packaging market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding e-commerce activity, growing food and beverage production, and increasing awareness of sustainable packaging practices. Rising investments in manufacturing, automotive production, retail distribution, and cold-chain logistics are creating strong demand for reusable pallets, crates, containers, and dunnage systems. In addition, the growing availability of cost-effective plastic returnable packaging and the expansion of organized logistics infrastructure are making reusable packaging solutions more accessible across emerging economies.

Japan Returnable Packaging Market Insight

The Japan returnable packaging market is expected to witness significant growth from 2026 to 2033 due to the country’s advanced manufacturing sector, high focus on resource efficiency, and established culture of waste segregation and recycling. Japanese automotive, electronics, food, and pharmaceutical manufacturers are increasingly using reusable trays, pallets, containers, and protective dunnage to improve supply chain efficiency and reduce packaging material consumption. The growing integration of automated logistics systems, robotics, and RFID tracking technologies is further supporting the adoption of durable and standardized returnable packaging solutions across domestic and export-oriented industries.

China Returnable Packaging Market Insight

The China returnable packaging market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by the country’s large-scale manufacturing sector, expanding e-commerce industry, and growing demand for efficient industrial logistics solutions. Reusable plastic pallets, crates, IBCs, and industrial containers are increasingly used across automotive, food and beverages, chemicals, electronics, and consumer goods supply chains. The expansion of smart warehousing, increasing investments in circular economy initiatives, and the availability of locally manufactured returnable packaging products are expected to continue strengthening market growth across China.

Which are the Top Companies in Returnable Packaging Market?

The Returnable Packaging industry is primarily led by well-established companies, including:

- DS Smith (U.K.)

- Akro-Mils / Myers Industries Inc. (U.S.)

- Brambles Ltd (Australia)

- Schoeller Allibert (Netherlands)

- Menasha Packaging Company LLC (U.S.)

- NEFAB GROUP (Sweden)

- Rehrig Pacific Company (U.S.)

- IPL, inc. (Canada)

- SCHÜTZ GmbH & Co. KGaA (Germany)

- Vetropack (Switzerland)

- Amatech Inc. (U.S.)

- Monoflo International (U.S.)

- MJSolpac Ltd (U.K.)

- CABKA Group (Germany)

- UFP Technologies, Inc. (U.S.)

- Ckdpack (India)Multipac Pty. Ltd. (Australia)

- Tri-Wall Limited (Hong Kong)

- Wiegand-Glas Holding GmbH (Germany)

- Mpact Plastic Containers (South Africa)

Latest Developments in Returnable Packaging Market

- In April 2024, GWP Correx launched a new returnable packaging solution called Rapitainer, designed to provide a lightweight, durable, and fully recyclable alternative to traditional one-trip packaging. This innovative system allows for fast assembly without the need for tapes or staples, enhancing efficiency in packing processes. Rapitainer is particularly suited for industries seeking to reduce packaging waste while maintaining strength and protection during transit. It also supports repeated use, aligning with growing sustainability goals across supply chains

- In April 2024, IFCO, a global leader in reusable packaging containers, announced the acquisition of BEPCO, a renowned reusable packaging pooling company based in Tallinn, Estonia. BEPCO is known for specializing in meat and dairy crate pools across the Baltics. This acquisition is a strategic move by IFCO to bolster its market presence in the region, expand its product offerings, and further strengthen its position in the growing reusable packaging industry. The move reflects IFCO's ongoing commitment to expanding its footprint and enhancing service capabilities in the food packaging sector

- In January 2024, a diverse coalition of non-profit organizations, industry stakeholders, and non-governmental organizations (NGOs) launched the Alliance for Sustainable Packaging for Foods (ASPF). The primary mission of the ASPF is to work collaboratively with governments, regulators, and other stakeholders worldwide to promote and advocate for safe, sustainable, and holistic regulations related to food packaging. By fostering harmonized packaging standards globally, the alliance aims to drive the transition towards more environmentally friendly packaging solutions while ensuring the safety and integrity of food products

- In June 2023, Puracy, a company specializing in eco-friendly, plant-based cleaning products, introduced an innovative refill packaging solution designed to enhance convenience and sustainability. The new system features aluminum cans and reusable bottles, offering a streamlined refill process that eliminates the mess and time-consuming steps typically involved with existing refill products. This innovation not only promotes the use of sustainable materials but also helps reduce waste and encourages a circular approach to packaging in the cleaning products industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Returnable Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Returnable Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Returnable Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.