Global Silicone Pressure Sensitive Adhesives Market

Market Size in USD Billion

USD

1.97 Billion

USD

3.42 Billion

2025

2033

USD

1.97 Billion

USD

3.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.97 Billion | |

| USD 3.42 Billion | |

| % | |

|

Silicone Pressure Sensitive Adhesives Market Size

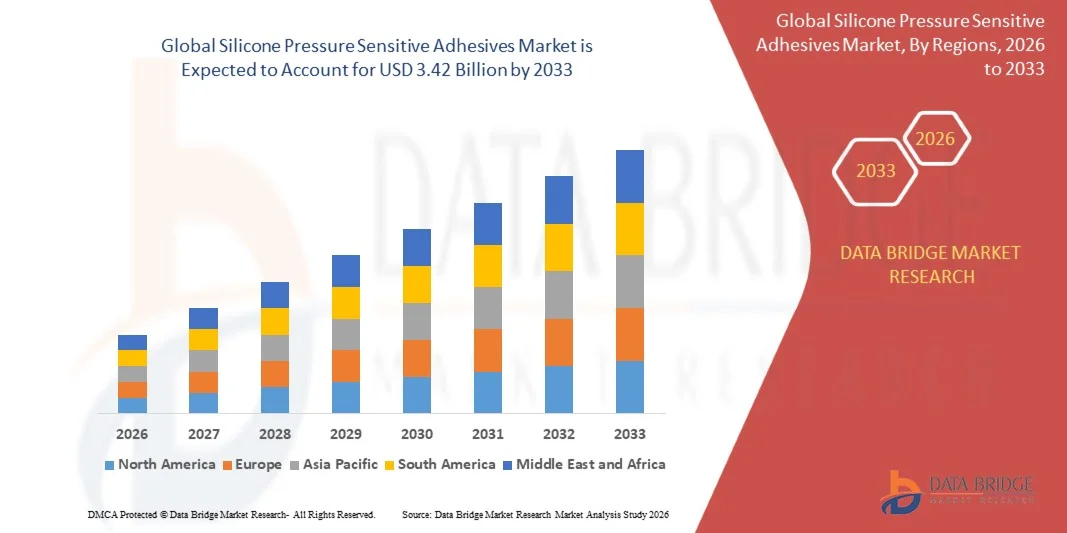

- The global silicone pressure sensitive adhesives market size was valued at USD 1.97 billion in 2025and is expected to reach USD 3.42 billion by 2033, at a CAGR of 7.16% during the forecast period

- The market growth is largely fueled by the increasing adoption of high-performance adhesive solutions across electronics, healthcare, automotive, and industrial applications, driven by the need for durability, heat resistance, and skin-safe bonding materials

- Furthermore, rising demand for advanced materials in medical devices, wearable electronics, and high-temperature industrial applications is establishing silicone pressure sensitive adhesives as a preferred solution for specialized bonding needs. These converging factors are accelerating the uptake of silicone-based adhesives, thereby significantly boosting the industry's growth

Silicone Pressure Sensitive Adhesives Market Analysis

- Silicone pressure sensitive adhesives, offering high-performance bonding without heat or solvent activation, are increasingly vital materials across electronics, healthcare, automotive, and industrial applications due to their excellent thermal stability, biocompatibility, and strong adhesion to low-surface-energy substrates

- The escalating demand for silicone PSAs is primarily fueled by the rapid expansion of electronics manufacturing, growing use in medical tapes and wearable devices, and increasing preference for durable, flexible, and high-temperature resistant adhesive solutions

- North America dominated the silicone pressure sensitive adhesives market with the largest revenue share of 38.6% in 2025, supported by strong demand from the healthcare and electronics industries, advanced manufacturing capabilities, and the presence of key adhesive technology players, with the U.S. witnessing significant adoption in medical devices, automotive electronics, and high-performance industrial applications

- Asia-Pacific is expected to be the fastest growing region in the silicone pressure sensitive adhesives market during the forecast period due to rapid industrialization, expanding electronics production base, and increasing healthcare infrastructure investments across emerging economies

- Tapes segment dominated the silicone pressure sensitive adhesives market with a market share of 42.8% in 2025, driven by its extensive use in industrial bonding, electrical insulation, medical dressings, and high-performance packaging applications

Report Scope and Silicone Pressure Sensitive Adhesives Market Segmentation

|

Attributes |

Silicone Pressure Sensitive Adhesives Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expanding adoption of silicone PSAs in next-generation flexible and wearable electronics · Growing demand for solvent-free and low-VOC adhesive systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Silicone Pressure Sensitive Adhesives Market Trends

“Rising Shift Toward High-Performance and Specialty Adhesive Applications”

- A significant and accelerating trend in the global silicone pressure sensitive adhesives market is the increasing adoption of advanced silicone-based formulations in high-performance applications such as medical wearables, flexible electronics, and automotive electronics due to their superior thermal stability and skin compatibility

- For instance, medical-grade silicone PSAs are widely used in wound care dressings and wearable glucose monitoring patches, where long wear time and skin-friendly removal are critical requirements

- Integration of silicone PSAs in next-generation electronics enables reliable bonding in foldable displays, sensors, and insulation layers, while maintaining flexibility and resistance to extreme temperature conditions in compact device architectures

- The shift toward low-VOC, solvent-free, and environmentally compliant adhesive systems is driving innovation in 100% solid silicone PSA technologies, enabling safer industrial and packaging applications with reduced environmental impact

- Increasing use of silicone PSAs in renewable energy applications such as solar panel assembly and EV battery insulation is expanding their role in high-performance industrial ecosystems requiring long-term durability and thermal resistance

- This trend towards highly specialized, durable, and regulation-compliant adhesive systems is fundamentally reshaping material expectations across industries, with companies such as Dow and 3M developing advanced silicone PSA solutions for medical and electronics markets

- The demand for silicone PSAs with enhanced performance characteristics is growing rapidly across healthcare, electronics, automotive, and energy sectors, as manufacturers increasingly prioritize durability, safety, and multi-surface adhesion capabilities

Silicone Pressure Sensitive Adhesives Market Dynamics

Driver

“Expanding Demand Driven by High-Performance Industrial and Healthcare Applications”

- The increasing requirement for high-performance adhesive solutions in healthcare, electronics, and automotive industries, coupled with the rapid growth of advanced manufacturing ecosystems, is a significant driver for the heightened demand for silicone pressure sensitive adhesives

- For instance, in March 2025, key adhesive manufacturers expanded production of medical-grade silicone PSAs for use in wearable health monitoring devices and advanced wound care solutions to meet rising healthcare demand

- As industries prioritize durability, heat resistance, and biocompatibility, silicone PSAs offer superior performance advantages over conventional adhesives, making them essential in critical applications such as medical tapes and electronic assemblies

- Furthermore, the rising adoption of wearable technologies and miniaturized electronic devices is making silicone PSAs an integral component in flexible bonding and skin-contact applications across consumer healthcare markets

- Increasing use of silicone PSAs in high-growth sectors such as EV batteries and renewable energy systems is further accelerating demand due to their excellent thermal insulation and long-term stability

- Expansion of advanced manufacturing in emerging economies is also supporting higher consumption of silicone PSAs in industrial assembly and specialty packaging applications

- The ease of application, long-term stability, and compatibility with sensitive surfaces are key factors propelling adoption of silicone PSAs in both industrial and medical sectors, supported by increasing R&D investments and material innovations

Restraint/Challenge

“High Production Costs and Complex Formulation Constraints”

- Concerns surrounding the relatively high production cost and complex formulation processes of silicone pressure sensitive adhesives pose a significant challenge to broader market penetration, especially in cost-sensitive applications and developing regions

- For instance, the use of specialized raw materials such as silicone polymers and curing agents increases manufacturing complexity, limiting large-scale substitution of conventional acrylic and rubber-based adhesives in price-driven markets

- Addressing cost challenges through process optimization, material innovation, and scalable manufacturing techniques is crucial for improving affordability and expanding adoption across mass-market applications

- In addition, technical limitations in achieving strong adhesion on certain substrates without surface treatment can restrict usage in some industrial bonding applications compared to alternative adhesive chemistries

- Volatile raw material pricing for silicone intermediates can further impact production economics, creating margin pressure for manufacturers operating in competitive global markets

- Stringent regulatory compliance requirements for medical and electronics-grade silicone adhesives also increase development time and certification costs, slowing commercialization cycles

- While demand continues to rise, the higher price point of silicone PSAs compared to conventional adhesives can still hinder widespread adoption, particularly in packaging and low-cost consumer goods segments

- Overcoming these challenges through cost-efficient production methods and improved formulation efficiency will be vital for sustained market growth and broader commercialization of silicone pressure sensitive adhesives

Silicone Pressure Sensitive Adhesives Market Scope

The market is segmented on the basis of type, technology, application, and end use.

- By Type

On the basis of type, the silicone pressure sensitive adhesives market is segmented into solvent-based silicone PSAs, water-based silicone PSAs, solvent-free silicone PSAs, silicone rubber-based adhesives, and silicone resin-based adhesives. The solvent-based silicone PSAs segment dominated the market with the largest revenue share of 38.9% in 2025, driven by its strong adhesion strength, proven reliability, and extensive use in high-performance industrial and medical applications. It is widely preferred in tapes, electronics assembly, and automotive bonding due to its excellent thermal resistance and durability under extreme conditions. Established manufacturing processes and broad substrate compatibility further support its dominance across developed regions. Strong demand from legacy industrial applications also sustains its leadership position. However, environmental concerns around solvent emissions are gradually limiting long-term expansion in some regions. Despite this, it continues to remain the most widely used formulation in mature markets.

The solvent-free silicone PSAs segment is expected to witness the fastest growth rate of 22.4% from 2026 to 2033, driven by increasing regulatory pressure on VOC emissions and rising demand for sustainable adhesive solutions. These adhesives eliminate solvent use while maintaining high bonding performance, making them suitable for electronics, medical devices, and packaging applications. Their adoption is rapidly increasing in wearable healthcare products and skin-contact applications due to improved safety profiles. Technological advancements in curing and formulation are improving scalability and cost efficiency. Growing focus on green manufacturing practices is further accelerating adoption across industries. Expanding use in high-end electronics and eco-friendly packaging is also contributing to strong growth momentum.

- By Technology

On the basis of technology, the silicone pressure sensitive adhesives market is segmented into solvent-based technology, water-borne technology, hot-melt technology, radiation-cured systems, and solventless systems. The solvent-based technology segment dominated the market with the largest revenue share of 36.7% in 2025, due to its well-established industrial adoption, high performance, and versatility across multiple end-use industries. It provides excellent adhesion, chemical resistance, and stability, making it suitable for tapes, automotive parts, and electronics. Its widespread availability and mature production infrastructure support large-scale commercialization. The technology is highly preferred in applications requiring long-term durability and reliability. Strong presence in North America and Europe also reinforces its dominance. However, regulatory pressure on solvent emissions is gradually encouraging alternative technologies.

The radiation-cured segment is expected to witness the fastest growth rate of 23.1% from 2026 to 2033, driven by increasing demand for fast-processing, energy-efficient, and environmentally friendly adhesive solutions. UV and electron beam curing systems enable precise control of adhesive properties and significantly reduce production time. These systems are gaining traction in electronics, optical films, and medical applications due to their high performance and clean processing characteristics. Elimination of solvents makes them compliant with strict environmental standards. Continuous innovation in curing equipment and materials is improving adoption rates. Rising demand from advanced manufacturing industries is further accelerating segment growth.

- By Application

On the basis of application, the silicone pressure sensitive adhesives market is segmented into tapes, labels & stickers, protective films, medical adhesives, electronics assembly, automotive components, industrial bonding, and consumer goods applications. The tapes segment dominated the market with the largest revenue share of 42.8% in 2025, driven by its extensive use in industrial, electrical insulation, construction, and packaging applications. Silicone PSAs provide high temperature resistance and long-term stability, making them ideal for demanding environments. They are widely used in specialty tapes for electronics, automotive wiring, and aerospace applications. Strong industrial demand and versatility across multiple sectors support segment leadership. Increasing use in high-performance masking and protective tapes also contributes to growth. Established supply chains further reinforce dominance in global markets.

The medical adhesives segment is expected to witness the fastest growth rate of 24.5% from 2026 to 2033, driven by rising demand for advanced wound care products, surgical tapes, and wearable medical devices. Silicone PSAs are highly preferred due to their skin-friendly properties, hypoallergenic nature, and painless removal. Increasing prevalence of chronic diseases and aging populations is boosting demand for long-term wearable healthcare solutions. Expanding adoption in remote patient monitoring devices is further accelerating growth. Continuous innovation in medical-grade adhesives is improving performance and safety standards. Rising healthcare expenditure globally is also supporting rapid segment expansion.

- By End Use

On the basis of end use, the silicone pressure sensitive adhesives market is segmented into electronics & electrical, healthcare & medical, automotive, packaging, construction, aerospace & defense, and consumer goods. The electronics & electrical segment dominated the market with the largest revenue share of 34.6% in 2025, driven by rapid growth in consumer electronics, semiconductors, and flexible device manufacturing. Silicone PSAs are widely used for insulation, bonding, and thermal management in electronic assemblies. Their ability to perform under high temperatures makes them essential in compact and high-performance devices. Strong demand for smartphones, wearables, and display technologies supports segment leadership. Expansion of global electronics manufacturing hubs further strengthens dominance. Continuous miniaturization of devices is also increasing usage intensity.

The healthcare & medical segment is expected to witness the fastest growth rate of 25.3% from 2026 to 2033, driven by increasing adoption of advanced medical tapes, wound dressings, and wearable diagnostic devices. Silicone PSAs offer superior biocompatibility and are ideal for long-term skin contact applications. Rising focus on home healthcare and remote monitoring is significantly boosting demand. Growing incidence of chronic conditions is also increasing usage in continuous monitoring devices. Expanding healthcare infrastructure in emerging economies is further accelerating adoption. Ongoing innovation in medical adhesive technologies is supporting strong long-term growth potential.

Silicone Pressure Sensitive Adhesives Market Regional Analysis

- North America dominated the silicone pressure sensitive adhesives market with the largest revenue share of 38.6% in 2025, supported by strong demand from the healthcare and electronics industries, advanced manufacturing capabilities, and the presence of key adhesive technology players

- Consumers and industrial users in the region highly value the superior performance characteristics of silicone PSAs, including high thermal resistance, biocompatibility, and long-term durability, making them essential in medical devices, wearable technologies, and high-end electronics applications

- This widespread adoption is further supported by high R&D investments, strong presence of key adhesive manufacturers, and increasing use of silicone PSAs in advanced healthcare solutions such as wound care products and diagnostic wearables, establishing the region as a leading innovation hub for high-performance adhesives

U.S. Silicone Pressure Sensitive Adhesives Market Insight

The United States silicone pressure sensitive adhesives market dominated North America with the largest revenue share of 81% in 2025, driven by strong demand from healthcare, electronics, automotive, and industrial applications. The country benefits from advanced manufacturing capabilities and high adoption of innovative adhesive technologies across multiple sectors. Silicone PSAs are widely used in medical devices, wearable health monitors, and surgical tapes due to their excellent biocompatibility, durability, and skin-friendly properties. Increasing integration in high-performance electronics and electric vehicle components is further supporting market growth. Strong presence of leading global adhesive manufacturers and continuous R&D investments are accelerating product innovation. High adoption of smart healthcare solutions and advanced industrial automation continues to strengthen market expansion in the U.S.

Europe Silicone Pressure Sensitive Adhesives Market Insight

The Europe silicone pressure sensitive adhesives market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent environmental regulations and rising demand for sustainable, low-VOC adhesive solutions. The region’s strong automotive, healthcare, and industrial manufacturing base is fostering adoption of high-performance silicone adhesives. Consumers and industries are increasingly focusing on eco-friendly and high-durability bonding solutions for applications such as medical tapes, electronics assembly, and industrial insulation. In addition, increasing adoption of renewable energy systems and electric vehicles is further boosting demand for advanced adhesive technologies. Europe’s emphasis on innovation, sustainability, and regulatory compliance is significantly shaping market development.

United Kingdom Silicone Pressure Sensitive Adhesives Market Insight

The United Kingdom silicone pressure sensitive adhesives market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising demand from healthcare, electronics, and industrial sectors. Increasing adoption of advanced medical devices and wearable healthcare technologies is significantly supporting market expansion. Silicone PSAs are widely used in wound care products, surgical tapes, and diagnostic wearables due to their skin-friendly properties and reliable performance. In addition, growing focus on digital healthcare and smart medical solutions is strengthening demand. The country’s strong pharmaceutical and medical device ecosystem, along with increasing R&D activities in specialty adhesives, is further contributing to market growth.

Germany Silicone Pressure Sensitive Adhesives Market Insight

The Germany silicone pressure sensitive adhesives market is expected to expand at a considerable CAGR during the forecast period, fueled by strong automotive production, advanced industrial manufacturing, and increasing demand for sustainable adhesive solutions. The country’s engineering excellence and innovation-driven ecosystem are supporting adoption of silicone PSAs in electric vehicles, electronics insulation, and industrial bonding applications. Growing focus on renewable energy and green manufacturing practices is further accelerating demand for high-performance adhesives. In addition, increasing integration of silicone PSAs in automation systems and precision engineering applications is strengthening market growth. Germany’s strong industrial base continues to make it a key European market for advanced adhesives.

Asia-Pacific Silicone Pressure Sensitive Adhesives Market Insight

The Asia-Pacific silicone pressure sensitive adhesives market is poised to grow at the fastest CAGR of 24.6% during the forecast period of 2026 to 2033, driven by rapid industrialization, expanding electronics manufacturing, and rising healthcare investments. The region is a global hub for semiconductor production, consumer electronics, and automotive assembly, significantly boosting demand for high-performance adhesives. Silicone PSAs are increasingly used in flexible electronics, medical applications, and industrial tapes due to their versatility and durability. Government initiatives supporting digitalization and healthcare modernization are further accelerating adoption. In addition, expanding manufacturing capabilities and cost advantages are making the region highly attractive for global adhesive manufacturers.

Japan Silicone Pressure Sensitive Adhesives Market Insight

The Japan silicone pressure sensitive adhesives market is gaining momentum due to its advanced electronics industry, high-precision manufacturing, and strong demand for medical-grade adhesive solutions. Silicone PSAs are widely used in compact electronic devices, sensors, and wearable healthcare products due to their stability and reliability under extreme conditions. The country’s aging population is significantly driving demand for medical adhesives used in long-term care, wound management, and home healthcare monitoring systems. In addition, strong focus on robotics, IoT integration, and smart healthcare solutions is further supporting market growth. Japan’s emphasis on innovation and quality continues to strengthen its position in high-end adhesive applications.

India Silicone Pressure Sensitive Adhesives Market Insight

The India silicone pressure sensitive adhesives market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding industrial base, and strong growth in electronics and healthcare sectors. Increasing adoption of affordable medical devices, wearable technologies, and industrial tapes is significantly driving market demand. Silicone PSAs are gaining traction in packaging, automotive, and consumer electronics applications due to their durability and cost-effectiveness. Government initiatives such as smart cities, Make in India, and healthcare infrastructure development are further boosting adoption. Rising domestic electronics production and growing foreign investments are also enhancing market expansion across multiple end-use industries.

Silicone Pressure Sensitive Adhesives Market Share

The Silicone Pressure Sensitive Adhesives industry is primarily led by well-established companies, including:

- Dow Inc. (U.S.)

- 3M (U.S.)

- Henkel AG & Co. KGaA (Germany)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Wacker Chemie AG (Germany)

- Momentive Performance Materials Inc. (U.S.)

- Elkem ASA (Norway)

- DuPont de Nemours, Inc. (U.S.)

- Avery Dennison Corporation (U.S.)

- H.B. Fuller Company (U.S.)

- Sika AG (Switzerland)

- Arkema S.A. (France)

- Nitto Denko Corporation (Japan)

- Tesa SE (Germany)

- Lohmann GmbH & Co. KG (Germany)

- Master Bond Inc. (U.S.)

- Delo Industrial Adhesives (Germany)

- Permabond LLC (U.S.)

- CHT Group (Germany)

- Novagard Solutions Inc. (U.S.)

What are the Recent Developments in Global Silicone Pressure Sensitive Adhesives Market?

- In December 2025, Henkel introduced Loctite MS 9650, a next-generation adhesive and sealant based on silane-modified polymer technology, designed for automotive display bonding and high-performance industrial applications. The product delivers silicone-like flexibility, UV resistance, and low-VOC performance, improving sustainability in automotive assembly systems

- In October 2025, Henkel launched new electronics-grade adhesive solutions, including EMI shielding films and thermal management materials for automotive and industrial electronics applications. These solutions support high-performance bonding requirements in next-generation electronic systems

- In October 2025, Henkel and Dow announced an expanded partnership to introduce low-carbon feedstocks and renewable energy in adhesive manufacturing, reducing product carbon footprint by up to 40% in selected lines, including pressure-sensitive adhesive technologies

- In July 2025, Henkel showcased recyclable PSA solutions at Labelexpo Europe 2025, focusing on circular packaging systems and CO₂-reducing adhesive technologies for label and tape applications. These PSAs are designed to meet EU PPWR sustainability regulations

- In August 2024, Henkel showcased its PSA portfolio for recyclable packaging applications, including hotmelt, UV, and water-based adhesives designed for label and tape industries, supporting circular economy and food-safe packaging solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Silicone Pressure Sensitive Adhesives Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Silicone Pressure Sensitive Adhesives Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Silicone Pressure Sensitive Adhesives Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.