Global Sleep Related Hypoventilation Market

Market Size in USD Billion

USD

1.81 Billion

USD

2.69 Billion

2024

2032

USD

1.81 Billion

USD

2.69 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.81 Billion | |

| USD 2.69 Billion | |

| % | |

|

Sleep Related Hypoventilation Market Size

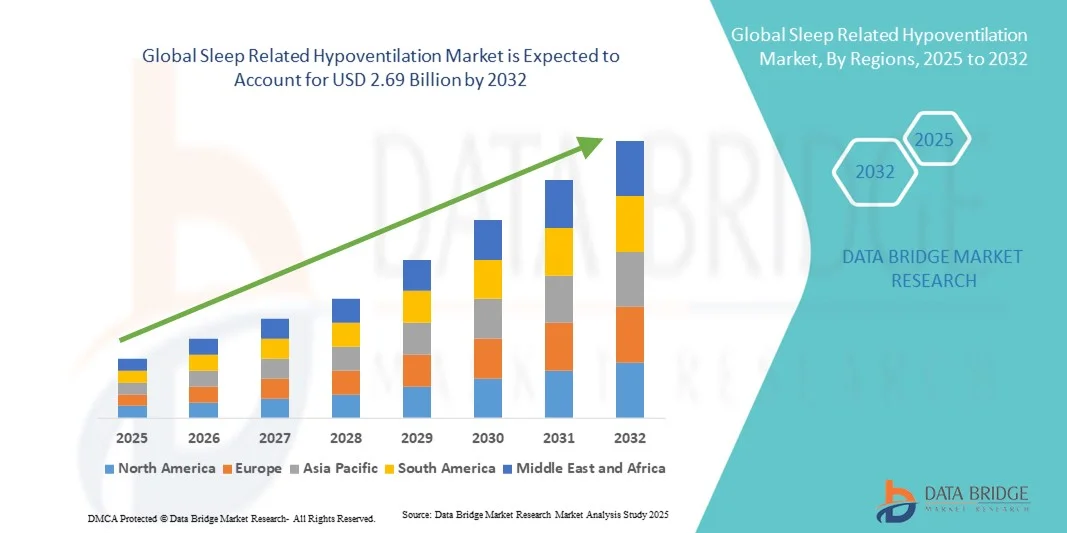

- The global sleep related hypoventilation market size was valued at USD 1.81 billion in 2024 and is expected to reach USD 2.69 billion by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of sleep disorders, advancements in medical technology, and rising awareness about sleep health, driving adoption of devices such as CPAP, BiPAP, and ASV

- Furthermore, the shift towards home healthcare solutions, combined with consumer demand for effective, user-friendly, and comfortable treatment options, is establishing sleep-related hypoventilation management devices as the preferred solution. These converging factors are accelerating the uptake of these devices, thereby significantly boosting the industry's growth

Sleep Related Hypoventilation Market Analysis

- Sleep related hypoventilation management, encompassing diagnostic and therapeutic solutions for disorders such as idiopathic hypoventilation, congenital central alveolar hypoventilation, and comorbid sleep-related hypoventilation, is increasingly vital in both clinical and homecare settings due to its impact on patient health, quality of life, and integration with monitoring technologies

- The escalating demand for sleep related hypoventilation solutions is primarily fueled by the growing prevalence of sleep-related breathing disorders, rising awareness about sleep health, and a preference for effective, patient-friendly treatment options such as Positive Airway Pressure (PAP) therapy and respiratory stimulants

- North America dominated the sleep related hypoventilation market with the largest revenue share of 50.8% in 2024, characterized by advanced healthcare infrastructure, high awareness of sleep disorders, and a strong presence of leading medical device and pharmaceutical companies, with the U.S. experiencing substantial growth in adoption across hospitals, clinics, and homecare settings

- Asia-Pacific is expected to be the fastest growing region in the sleep related hypoventilation market during the forecast period due to increasing urbanization, rising healthcare awareness, growing disposable incomes, and expanding access to advanced medical technologies

- Idiopathic hypoventilation segment dominated the sleep related hypoventilation market with a market share of 45.5% in 2024, driven by its higher prevalence, need for continuous monitoring, and wide adoption of PAP therapy, which remains the cornerstone of effective treatment across clinical and homecare environments

Report Scope and Sleep Related Hypoventilation Market Segmentation

|

Attributes |

Sleep Related Hypoventilation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sleep Related Hypoventilation Market Trends

Enhanced Convenience Through Connected and Smart Devices

- A significant and accelerating trend in the global sleep related hypoventilation market is the adoption of connected PAP devices and respiratory monitoring systems, allowing patients and clinicians to track therapy effectiveness in real time and adjust treatment remotely

- For instance, ResMed AirSense 10 CPAP integrates with mobile applications, providing patients with daily usage reports and clinicians with remote compliance data for personalized therapy adjustments

- Smart device integration enables features such as automated pressure adjustments based on detected breathing patterns, intelligent alerts for therapy interruptions, and improved patient adherence through reminders and notifications

- The seamless connection of hypoventilation devices with smartphones and cloud platforms facilitates centralized management of therapy, enabling users to monitor sleep quality, device performance, and treatment trends from a single interface

- This trend towards more connected, intuitive, and user-friendly devices is fundamentally reshaping patient expectations for sleep disorder management, with companies such as Philips Respironics developing smart CPAP and BiPAP devices featuring remote monitoring and adaptive therapy

- The demand for sleep related hypoventilation devices that offer intelligent connectivity and remote management is growing rapidly across clinical and homecare sectors, as patients increasingly prioritize convenience and comprehensive therapy monitoring

Sleep Related Hypoventilation Market Dynamics

Driver

Growing Need Due to Rising Sleep Disorder Prevalence and Homecare Adoption

- The increasing prevalence of sleep-related breathing disorders, coupled with the growing adoption of homecare therapy solutions, is a significant driver for the heightened demand for sleep related hypoventilation devices

- For instance, in March 2024, Philips Respironics launched an advanced home-use BiPAP system with cloud-based monitoring, designed to improve therapy adherence and ease of use

- As patients and clinicians become more aware of potential health risks from untreated hypoventilation, devices offering remote monitoring, compliance reporting, and adaptive pressure adjustments provide a compelling upgrade over traditional therapy options

- Furthermore, the rising popularity of homecare treatment and telemedicine is making connected hypoventilation devices an integral component of patient management, offering seamless integration with digital health platforms

- Features such as automated therapy adjustments, smartphone-based monitoring, and real-time clinician feedback are key factors propelling the adoption of connected hypoventilation devices in both clinical and homecare settings

Restraint/Challenge

Device Affordability and Regulatory Compliance Hurdle

- Concerns surrounding the relatively high cost of advanced connected hypoventilation devices pose a significant challenge to broader market adoption, particularly in developing regions or among price-sensitive patients

- For instance, some premium PAP and BiPAP devices with cloud connectivity and adaptive pressure features are priced significantly higher than standard therapy devices, limiting access for certain patient groups

- Addressing cost barriers through more affordable device options, rental programs, and insurance coverage is crucial for expanding adoption while maintaining therapy quality

- In addition, regulatory compliance across different regions, including medical device certifications and data privacy regulations, can slow market penetration and product launches

- Overcoming these challenges through cost optimization, patient education, and adherence to regional regulatory standards will be vital for sustained growth of the sleep related hypoventilation market

Sleep Related Hypoventilation Market Scope

The market is segmented on the basis of type, treatment, symptoms, dosage, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the sleep related hypoventilation market is segmented into idiopathic hypoventilation, congenital central alveolar hypoventilation, and comorbid sleep-related hypoventilation. The idiopathic hypoventilation segment dominated the market with the largest revenue share of 45.5% in 2024, driven by its higher prevalence among adults and the requirement for continuous therapy. Patients with idiopathic hypoventilation often rely on Positive Airway Pressure (PAP) therapy, which ensures effective long-term management and improved sleep quality. The segment also benefits from adoption in both hospital and homecare settings, where connected devices enable compliance monitoring. Increased diagnosis rates due to awareness campaigns have further contributed to growth. Clinicians prefer this segment because of standardized treatment protocols and well-established therapy options, ensuring predictable patient outcomes. The segment’s dominance is also supported by technological innovations in PAP devices, such as adaptive pressure and smart connectivity features.

The comorbid sleep-related hypoventilation segment is anticipated to witness the fastest growth rate of 6.1% from 2025 to 2032, fueled by rising obesity, COPD, and other chronic conditions that exacerbate hypoventilation. Patients with comorbid conditions increasingly require advanced multi-functional PAP devices for optimal therapy. Growing awareness of comorbid hypoventilation among healthcare professionals has led to higher diagnosis and treatment rates. Homecare adoption and telemedicine platforms are enabling better remote monitoring, contributing to rapid growth. Technological advancements in connected devices help improve patient adherence and therapy outcomes. Furthermore, expanding healthcare infrastructure in emerging regions supports the segment’s fast-paced market penetration.

- By Treatment

On the basis of treatment, the sleep related hypoventilation market is segmented into Positive Airway Pressure (PAP) therapy, respiratory stimulants, and others. The PAP therapy segment dominated the market with a revenue share of 62% in 2024, driven by its proven efficacy in managing hypoventilation and improving sleep quality. These devices are non-invasive, highly reliable, and widely recommended by clinicians for long-term use. Integration with smart monitoring systems ensures adherence tracking and personalized therapy adjustments. Continuous technological improvements, such as adaptive pressure and connected monitoring, support its continued dominance. Patient awareness and support programs from manufacturers further enhance adoption rates. Both homecare and hospital settings see significant reliance on PAP therapy for effective management of sleep-related hypoventilation.

Respiratory stimulants are expected to witness the fastest CAGR of 6.5% from 2025 to 2032, driven by the growing need for pharmacological interventions among patients intolerant to PAP therapy. These stimulants stimulate breathing in specific patient populations and are often used alongside PAP devices for optimal results. Increasing research and approvals of new stimulants expand their clinical adoption globally. The availability of oral and injectable formulations enhances convenience and accessibility. Rising awareness of non-device treatment options among clinicians and patients fuels adoption. Hospitals and specialized clinics are significant contributors to the segment’s rapid growth, particularly in acute care settings.

- By Symptoms

On the basis of symptoms, the sleep related hypoventilation market is segmented into frequent awakenings during sleep, insomnia, morning headaches, daytime sleepiness, faintness, stomach problems, reduced exercise capacity, and others. The daytime sleepiness segment dominated the market in 2024, driven by its high prevalence and impact on quality of life and daily functioning. Persistent daytime sleepiness often prompts patients to seek medical evaluation and therapy, boosting device adoption. PAP therapy has proven effective in alleviating daytime fatigue, reinforcing the segment’s growth. Clinicians prioritize intervention for patients showing significant daytime impairment, further supporting the market. Connected devices allow continuous monitoring of sleep patterns and daytime alertness, enhancing outcomes. Awareness campaigns emphasizing the risks of untreated hypoventilation also contribute to segment dominance.

The reduced exercise capacity segment is anticipated to witness the fastest growth from 2025 to 2032, fueled by rising awareness of how hypoventilation affects physical performance. Patients and clinicians increasingly recognize the importance of addressing exercise intolerance alongside sleep-related symptoms. Adoption of integrated monitoring and therapy solutions improves daytime functionality. Homecare devices enabling activity monitoring are expanding in popularity. Awareness campaigns and rehabilitation programs are driving patient engagement. The segment benefits from growing demand for comprehensive management solutions in both home and clinical settings.

- By Dosage

On the basis of dosage, the sleep related hypoventilation market is segmented into tablet, injection, and others. The tablet segment dominated the market in 2024, driven by the convenience, ease of administration, and patient adherence associated with oral respiratory stimulants. Tablets are widely available, cost-effective, and suitable for homecare therapy. Formulation improvements, such as sustained-release tablets, enhance tolerability and efficacy. Clinicians often prefer tablets as the first-line pharmacological therapy. Integration with patient monitoring apps further improves compliance tracking. The segment’s dominance is reinforced by high patient acceptance and consistent therapy outcomes.

The injection segment is expected to witness the fastest CAGR from 2025 to 2032, due to its critical application in hospital and emergency settings. Injectable forms provide precise dosing and immediate effect, particularly for severe cases of hypoventilation. Hospitals increasingly rely on IV administration for acute interventions. Growing awareness among clinicians about injectable stimulants’ benefits supports adoption. Advancements in combination therapies and administration techniques enhance therapeutic outcomes. The segment’s rapid growth is also facilitated by specialized clinics offering emergency respiratory care.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, intravenous, and others. The oral segment dominated the market in 2024, driven by convenience, homecare adoption, and preference for non-invasive therapy. Oral administration ensures higher adherence and is easier to manage in long-term therapy. Formulation enhancements improve absorption and tolerability, supporting continued growth. Patients prefer oral therapy due to comfort and simplicity. Clinicians recommend oral routes for chronic management, reinforcing dominance. Connected monitoring apps complement oral therapy adherence tracking.

The intravenous segment is anticipated to witness the fastest growth from 2025 to 2032, driven by acute care applications in hospitals. IV administration provides immediate therapeutic intervention for severe hypoventilation. Hospitals rely on IV therapy in critical respiratory cases. Rapid onset of action supports urgent management scenarios. Adoption is further aided by specialized training and advanced hospital infrastructure. The segment benefits from increasing emergency care requirements in both developed and emerging markets.

- By End-Users

On the basis of end-users, the sleep related hypoventilation market is segmented into clinics, hospitals, and others. The hospital segment dominated the market with the largest revenue share in 2024, due to specialized sleep clinics, advanced respiratory care units, and availability of trained clinicians. Hospitals serve as primary centers for diagnosis, therapy initiation, and ongoing monitoring. Integration with connected monitoring systems ensures better patient compliance. High patient inflow and centralized treatment facilities support segment dominance. Hospitals also provide training and support for homecare adoption. Continuous innovation in hospital-based therapy enhances outcomes and reinforces market leadership.

The clinic segment is expected to witness the fastest CAGR from 2025 to 2032, due to the rise of specialized outpatient sleep clinics and telemedicine adoption. Clinics provide convenient access to diagnosis and treatment at lower costs. Urban and semi-urban centers see increasing patient preference for clinic-based care. Partnerships with device manufacturers expand therapy availability. Patient education programs and monitoring support adoption. The segment benefits from growth in homecare integration and remote therapy management.

- By Distribution Channel

On the basis of distribution channel, the sleep related hypoventilation market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market in 2024, driven by direct availability of devices and medications at the point of care. Hospitals also provide patient training and ongoing support, ensuring effective therapy outcomes. High adoption of hospital-based monitoring programs reinforces dominance. Integration with clinical workflows ensures adherence and compliance tracking. The segment benefits from established procurement channels and reliable supply chains. Hospitals continue to be primary distribution hubs for hypoventilation management solutions.

The online pharmacy segment is expected to witness the fastest growth from 2025 to 2032, fueled by the rise of e-commerce, convenience of home delivery, and preference for remote purchase of devices and medications. Online platforms support subscription models and recurring device supply. Patients benefit from ease of access and discreet delivery. Growing digital literacy and smartphone penetration accelerate adoption. Integration with digital therapy support tools enhances patient engagement. The segment is expanding rapidly across both developed and emerging markets.

Sleep Related Hypoventilation Market Regional Analysis

- North America dominated the sleep related hypoventilation market with the largest revenue share of 50.8% in 2024, characterized by advanced healthcare infrastructure, high awareness of sleep disorders, and a strong presence of leading medical device and pharmaceutical companies

- Patients and clinicians in the region highly value advanced PAP devices, respiratory stimulants, and connected monitoring systems that enable real-time therapy tracking, improved compliance, and better health outcomes

- This widespread adoption is further supported by high healthcare spending, growing awareness of sleep health, and the integration of telemedicine and homecare solutions, establishing connected hypoventilation devices as the preferred solution for both clinical and home settings

U.S. Sleep Related Hypoventilation Market Insight

The U.S. sleep related hypoventilation market captured the largest revenue share of 82% in 2024 within North America, fueled by the rising prevalence of sleep-related breathing disorders and the well-established healthcare infrastructure. Patients increasingly prioritize advanced PAP devices and respiratory stimulants, supported by connected monitoring systems for therapy tracking and compliance. The growing adoption of homecare solutions and telemedicine platforms further propels market growth. In addition, awareness campaigns on sleep health and physician-led recommendations are contributing to the widespread use of these devices. The integration of remote monitoring technologies, mobile applications, and cloud-based patient management systems significantly enhances the market’s expansion.

Europe Sleep Related Hypoventilation Market Insight

The Europe sleep related hypoventilation market is projected to expand at a substantial CAGR during the forecast period, primarily driven by increasing diagnosis rates and government initiatives supporting respiratory healthcare. The rising prevalence of obesity and chronic respiratory conditions is fostering the adoption of PAP therapy and respiratory stimulants. Patients and clinicians in the region value connected devices that enable remote monitoring and real-time therapy adjustments. Increasing urbanization and demand for homecare solutions further contribute to market growth. Hospitals and specialized clinics in Europe are adopting advanced devices for improved patient outcomes. Enhanced awareness and accessibility of home-use devices are accelerating adoption across residential and clinical settings.

U.K. Sleep Related Hypoventilation Market Insight

The U.K. sleep related hypoventilation market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of sleep disorders and the need for effective homecare management. Concerns regarding untreated hypoventilation and its impact on daytime alertness and health are motivating both patients and clinicians to adopt advanced PAP and monitoring devices. The growing telemedicine infrastructure and digital health initiatives support remote therapy compliance and monitoring. Increasing availability of user-friendly devices for home use also drives market expansion. Adoption across outpatient clinics and specialized sleep centers is further enhancing growth. The U.K.’s robust healthcare system and patient education campaigns continue to stimulate market demand.

Germany Sleep Related Hypoventilation Market Insight

The Germany sleep related hypoventilation market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of sleep health and respiratory disorders. Germany’s well-developed healthcare infrastructure and emphasis on technologically advanced solutions promote the adoption of connected PAP and BiPAP devices. Hospitals and clinics are integrating smart monitoring systems to improve therapy adherence and patient outcomes. The focus on sustainable and energy-efficient healthcare technologies further supports device adoption. The prevalence of chronic respiratory conditions also contributes to market growth. Advanced homecare solutions and insurance coverage policies are accelerating patient access to therapy.

Asia-Pacific Sleep Related Hypoventilation Market Insight

The Asia-Pacific sleep related hypoventilation market is poised to grow at the fastest CAGR of 22% during the forecast period of 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and technological advancements in countries such as China, Japan, and India. Growing awareness of sleep-related breathing disorders and the expansion of homecare therapy adoption are boosting market demand. Government initiatives promoting digital health and connected medical devices are further supporting growth. The region’s emerging healthcare infrastructure and telemedicine platforms are enabling wider access to therapy. Increasing availability of affordable PAP devices and stimulants is expanding the patient base. The rise of private hospitals and specialized sleep clinics is also accelerating adoption across APAC.

Japan Sleep Related Hypoventilation Market Insight

The Japan sleep related hypoventilation market is gaining momentum due to the country’s high awareness of sleep health, urbanization, and demand for convenient homecare solutions. The adoption of PAP and BiPAP devices is driven by an increasing number of smart-connected homes and healthcare facilities. Integration with digital monitoring platforms allows for improved therapy compliance and patient management. The aging population further spurs demand for easy-to-use, safe, and effective treatment options. Japanese consumers and clinicians highly value connected devices with remote monitoring capabilities. The focus on technological innovation in medical devices supports sustained market growth in both residential and clinical settings.

India Sleep Related Hypoventilation Market Insight

The India sleep related hypoventilation market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to the country’s growing middle class, rising awareness of sleep disorders, and expanding healthcare infrastructure. India represents one of the largest emerging markets for home-use PAP devices and respiratory stimulants. Rapid urbanization, telemedicine adoption, and smart healthcare initiatives are driving device accessibility and adoption. The availability of affordable devices and domestic manufacturing is further enhancing market penetration. Growing government programs focused on respiratory health are supporting market expansion. Both residential patients and healthcare facilities are increasingly integrating connected monitoring systems for therapy compliance and outcome tracking.

Sleep Related Hypoventilation Market Share

The sleep related hypoventilation industry is primarily led by well-established companies, including:

- ResMed Inc. (U.S.)

- Koninklijke Philips N.V (U.S.)

- Fisher & Paykel Healthcare Limited (New Zealand)

- Inspire Medical Systems, Inc. (U.S.)

- SomnoMed (Australia)

- Compumedics Limited (Australia)

- Löwenstein Medical GmbH & Co. KG (Germany)

- BMC Medical Co., Ltd. (China)

- Braebon Medical Corporation (Canada)

- Medtronic (Ireland)

- NIHON KOHDEN CORPORATION (Japan)

- Cadwell Industries, Inc. (U.S.)

- Itamar Medical Ltd. (Israel)

- Acurable Ltd. (U.K.)

- Advanced Brain Monitoring, Inc. (U.S.)

- Belun Technology (Hong Kong)

- Octapharma AG (Switzerland)

- GSK plc (U.K.)

- Pfizer Inc. (U.S.)

- Merck KGaA (Germany)

What are the Recent Developments in Global Sleep Related Hypoventilation Market?

- In July 2025, Compumedics launched the Falcon, a compact home sleep testing device featuring four high-speed channels, inductive bands, airflow measurement, and oximetry. The device includes a touchscreen user interface to assist patients in confirming proper sensor connections, facilitating successful sleep studies in home settings

- In June 2025, Dormotech introduced DormoVision X, a wireless home sleep testing device, at the SLEEP 2025 conference. This FDA-cleared device delivers real-time data with diagnostic accuracy comparable to gold-standard polysomnography, enhancing the scalability of sleep clinics and improving patient access to sleep diagnostics

- In April 2025, researchers from George Washington University published a study suggesting that setmelanotide, an FDA-approved medication for a rare genetic obesity disorder, may offer a pathway for treating obesity hypoventilation syndrome. The study found promising evidence in animal models, indicating potential benefits for patients with this life-threatening form of sleep-disordered breathing

- In April 2025, Apnimed acquired global rights to patents covering sulthiame, a differentiated carbonic anhydrase inhibitor, to develop oral pharmacotherapies for sleep and breathing diseases. This acquisition aims to expand Apnimed's portfolio and address unmet medical needs in sleep medicine

- In December 2024, the U.S. Food and Drug Administration (FDA) approved Zepbound (tirzepatide) as the first medication for treating moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity. This approval marks a significant advancement in pharmacological treatments for sleep apnea, offering an alternative for patients who have difficulty using continuous positive airway pressure (CPAP) devices

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.