Global Sly Syndrome Market

Market Size in USD Billion

USD

691.20 Billion

USD

945.95 Billion

2024

2032

USD

691.20 Billion

USD

945.95 Billion

2024

2032

| 2025 - 2032 | |

| USD 691.20 Billion | |

| USD 945.95 Billion | |

| % | |

|

Sly Syndrome Market Size

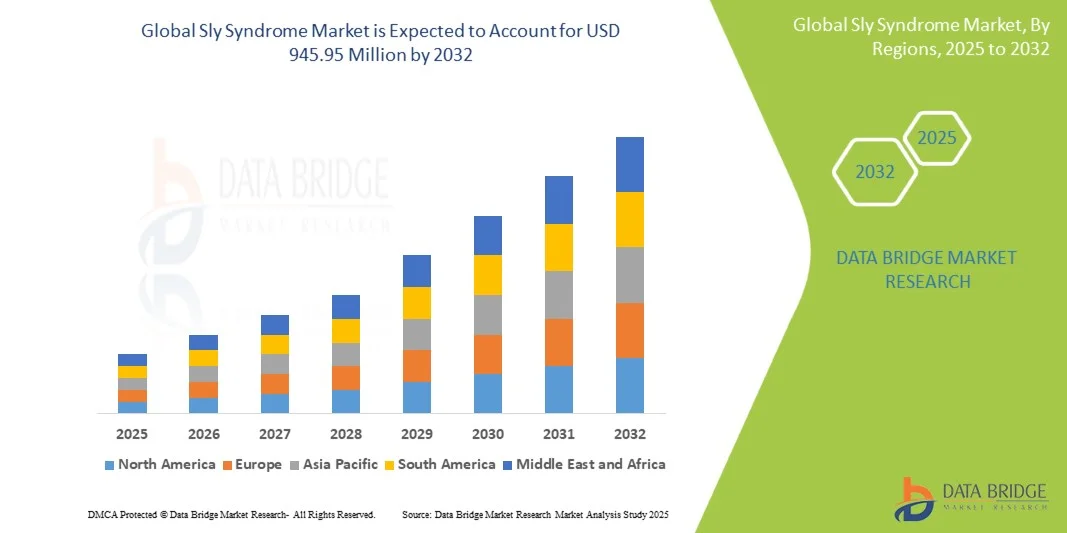

- The global Sly syndrome market size was valued at USD 691.20 million in 2024 and is expected to reach USD 945.95 million by 2032, at a CAGR of 4.0% during the forecast period

- The market growth is largely fueled by the growing adoption of advanced therapeutic solutions and technological progress in rare disease management, leading to increased accessibility and awareness of Sly syndrome treatments in both clinical and homecare settings

- Furthermore, rising patient and caregiver demand for safe, effective, and easy-to-administer treatment options is establishing innovative Sly syndrome therapies as the preferred standard of care. These converging factors are accelerating the uptake of Sly syndrome treatment solutions, thereby significantly boosting the industry's growth

Sly Syndrome Market Analysis

- The Sly Syndrome market, encompassing innovative therapies and management solutions for this rare lysosomal storage disorder, is witnessing steady growth due to rising awareness, early diagnosis, and increasing availability of treatment options

- The escalating demand for Sly syndrome treatments is primarily fueled by the growing prevalence of the disorder, advancements in genetic testing, and the increasing adoption of enzyme replacement and supportive therapies

- North America dominated the Sly syndrome market with the largest revenue share of 44% in 2024, supported by advanced healthcare infrastructure, early adoption of novel therapies, and strong presence of key pharmaceutical and biotechnology players. The U.S. experienced substantial growth in hospital and outpatient treatment centers, driven by innovations in therapy protocols and patient care solutions

- Asia-Pacific is expected to be the fastest-growing region in the Sly syndrome market during the forecast period, driven by rising healthcare access, increasing disposable incomes, and expansion of specialized treatment centers in countries such as India, China, and Japan

- The Intravenous segment dominated the Sly syndrome market with the largest market revenue share of 57.1% in 2024, driven by the established use of IV infusion for ERT therapies. IV administration ensures systemic delivery of the enzyme, providing consistent therapeutic benefits across organs affected by Sly Syndrome

Report Scope and Sly Syndrome Market Segmentation

|

Attributes |

Sly Syndrome Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Sly Syndrome Market Trends

“Rising Adoption of Advanced Therapies and Personalized Treatment Approaches”

- A significant and accelerating trend in the global Sly syndrome market is the increasing adoption of advanced therapies, including enzyme replacement therapy (ERT), gene therapy, and substrate reduction therapy. These treatment modalities are enhancing patient outcomes, slowing disease progression, and improving quality of life for individuals affected by Sly Syndrome

- For instance, in 2024, several clinical trials focused on next-generation gene therapies demonstrated promising results in improving enzyme activity and reducing systemic complications associated with Sly Syndrome. Such developments are expected to reshape therapeutic strategies and expand the treatment landscape

- Personalized medicine is increasingly being applied, with clinicians leveraging genetic and biomarker information to tailor treatment plans according to disease severity, age of onset, and patient-specific characteristics. This approach ensures optimized efficacy and safety while minimizing adverse effects

- Improved diagnostic capabilities, including early genetic testing and newborn screening programs, are facilitating timely intervention, which is critical for preventing irreversible organ damage and improving long-term prognosis

- The integration of multidisciplinary care—combining pharmacological treatment, physiotherapy, and supportive care—enhances overall patient management and ensures holistic treatment of Sly Syndrome complications

- Growing awareness among healthcare providers and patients, along with increasing investment by pharmaceutical and biotechnology companies, is driving the uptake of innovative therapies across hospitals, specialty clinics, and research institutions

- The trend toward accessible, targeted, and patient-centric treatment options is fundamentally transforming clinical management of Sly Syndrome, fostering greater adoption of advanced therapies and stimulating research into novel therapeutic solutions

Sly Syndrome Market Dynamics

Driver

“Growing Need Due to Rising Disease Awareness and Adoption of Advanced Therapies”

- The increasing prevalence of Sly syndrome, coupled with heightened awareness among healthcare providers and patients, is a significant driver for the growing demand for effective treatment solutions

- For instance, in April 2024, several research institutions announced advancements in gene therapy and enzyme replacement therapy (ERT) for Sly Syndrome, highlighting the potential to significantly improve patient outcomes. Such initiatives by key healthcare and pharmaceutical players are expected to drive the Sly Syndrome market growth in the forecast period

- As patients and clinicians become more aware of disease complications and long-term health impacts, there is a rising emphasis on early diagnosis and proactive management strategies, which encourages the adoption of advanced therapies

- Furthermore, the increasing availability of specialized treatment centers and access to innovative pharmacological solutions is improving overall patient care and supporting comprehensive disease management

- The adoption of personalized treatment approaches, tailored to patient-specific genetic profiles and disease severity, is also contributing to the market growth by offering optimized efficacy and improved safety

- Increasing government and private sector investment in rare disease research, along with educational campaigns and patient advocacy programs, is enhancing awareness and encouraging treatment uptake

Restraint/Challenge

“Challenges Due to High Therapy Costs and Limited Access to Care”

- The relatively high cost of advanced therapies, including gene therapy and enzyme replacement therapy, poses a significant challenge to broader market penetration, particularly in price-sensitive regions. Patients in developing countries often face financial constraints that limit their access to specialized treatments, making affordability a key barrier

- Limited access to specialized healthcare centers, experienced clinicians, and diagnostic facilities in emerging markets can delay early diagnosis and treatment initiation, which may adversely impact patient outcomes. The geographic disparity in healthcare infrastructure creates uneven availability of therapies

- In addition, the logistical challenges of transporting and storing biologics or gene therapies, which often require strict temperature control and handling procedures, further complicate access in less-developed regions

- Even in regions with moderate healthcare infrastructure, the lack of insurance coverage or reimbursement policies for high-cost therapies can discourage patients from pursuing treatment, slowing market adoption

- Addressing these challenges through expanded insurance coverage, government funding, patient assistance programs, telemedicine initiatives, and the development of more cost-effective therapies is crucial for ensuring wider accessibility

- While awareness campaigns are increasing, the perceived complexity, high cost, and limited availability of treatment options may still hinder adoption, particularly among populations with limited healthcare resources

- Overcoming these barriers through patient education, expansion of healthcare infrastructure, partnerships between public and private stakeholders, and development of affordable therapeutic options will be vital for sustained market growth in the Sly Syndrome sector

Sly Syndrome Market Scope

The market is segmented on the basis of symptoms, treatment, route of administration, and end users.

• By Symptoms

On the basis of symptoms, the Sly syndrome market is segmented into enlarged head, fluid buildup in the brain, coarse facial features, enlarged tongue, enlarged liver, enlarged spleen, problems with the heart valves, and abdominal hernias. The enlarged liver segment dominated the largest market revenue share of 38.6% in 2024, driven by the high prevalence of hepatomegaly among Sly Syndrome patients. Clinicians prioritize monitoring liver size as it is a critical indicator of disease progression and overall patient health. The segment also benefits from routine diagnostic imaging and biomarker assessments, making it easier to track therapy effectiveness. Liver enlargement often correlates with other systemic manifestations, which encourages comprehensive management plans. The availability of targeted therapies such as enzyme replacement therapy (ERT) supports improved outcomes in patients with liver involvement. In addition, patients and caregivers are increasingly aware of the importance of liver health in disease management. This combination of high prevalence, clinical focus, and therapeutic availability underpins the segment’s market leadership.

The Enlarged Head segment is anticipated to witness the fastest CAGR of 22.4% from 2025 to 2032, fueled by increased awareness and early diagnosis through advanced imaging techniques. Macrocephaly is a prominent early sign of Sly Syndrome, prompting timely intervention. Pediatricians and genetic specialists are adopting proactive screening protocols to identify affected children sooner, thereby increasing treatment uptake. Emerging supportive therapies, alongside ERT, are enhancing cranial growth management and patient quality of life. Educational initiatives for caregivers and telehealth monitoring programs further facilitate early intervention. The growing prevalence of diagnosed cases, especially in developed markets with advanced healthcare infrastructure, supports rapid segment growth. In addition, research into novel therapies addressing neurological and cranial complications is expected to drive adoption over the forecast period.

• By Treatment

On the basis of treatment, the Sly syndrome market is segmented into Enzyme Replacement Therapy (ERT) and Others. The ERT segment accounted for the largest market revenue share of 52.3% in 2024, driven by the approval of Mepsevii (vestronidase alfa-vjbk) as the first targeted therapy for Sly Syndrome. ERT is considered the standard of care, providing patients with improved organ function, reduced disease progression, and enhanced quality of life. Hospitals and specialty clinics actively administer ERT due to its clinical efficacy and well-established safety profile. The availability of patient support programs and infusion centers further enhances treatment adherence. Widespread physician awareness and guideline recommendations reinforce ERT’s market dominance. The segment also benefits from ongoing research aimed at optimizing dosing schedules and minimizing infusion times. Strong adoption in both developed and emerging markets contributes to sustained market leadership.

The Others segment, which includes symptomatic therapies and supportive care, is expected to witness the fastest CAGR of 19.7% from 2025 to 2032, driven by the need for individualized treatment plans. These therapies address complications such as cardiac defects, joint stiffness, and respiratory issues, complementing ERT. Growing awareness among caregivers and healthcare providers of holistic disease management is boosting uptake. Emerging treatment modalities, including gene therapy research, are contributing to faster growth. In addition, homecare delivery models for supportive therapies improve accessibility and patient adherence. The segment’s rapid adoption is also fueled by increased investment in rare disease therapeutics and specialized care programs. Rising patient populations and improved diagnostic rates further accelerate market expansion over the forecast period.

• By Route of Administration

On the basis of route of administration, the Sly syndrome market is segmented into Intravenous (IV) and Intracerebroventricular (ICV). The Intravenous segment dominated the largest market revenue share of 57.1% in 2024, driven by the established use of IV infusion for ERT therapies. IV administration ensures systemic delivery of the enzyme, providing consistent therapeutic benefits across organs affected by Sly Syndrome. Hospitals and infusion centers facilitate administration under professional supervision, ensuring patient safety. Patient adherence programs and standardized infusion protocols enhance efficacy and convenience. IV therapy is also preferred due to its predictable pharmacokinetics and ability to tailor dosing according to patient weight and disease severity. The segment benefits from robust clinical data and widespread physician familiarity, supporting ongoing dominance in both pediatric and adult populations.

The ICV segment is expected to witness the fastest CAGR of 23.5% from 2025 to 2032, driven by research targeting neurological manifestations of Sly Syndrome. ICV administration delivers therapy directly to the central nervous system, potentially addressing cognitive and motor impairments more effectively. Clinical trials and preclinical studies are increasing awareness of ICV benefits, particularly in severe cases. Emerging gene therapy approaches administered via ICV are also contributing to rapid adoption. Caregiver education, improved safety protocols, and telemonitoring solutions further support segment growth. The focus on neurological outcomes, combined with advances in drug delivery technology, is expected to drive strong growth in this segment over the forecast period.

• By End User

On the basis of end users, the Sly syndrome market is segmented into hospitals, specialty clinics, and others. The Hospitals segment accounted for the largest market revenue share of 49.8% in 2024, driven by the concentration of pediatric specialists, infusion infrastructure, and multidisciplinary care teams. Hospitals provide centralized monitoring, comprehensive treatment, and adherence programs, making them the preferred choice for Sly Syndrome management. High patient volumes, integration with clinical trials, and insurance coverage contribute to sustained market leadership. Hospitals also offer follow-up care, physiotherapy, and genetic counseling, supporting long-term disease management.

The Specialty Clinics segment is expected to witness the fastest CAGR of 21.2% from 2025 to 2032, fueled by the rise of rare disease centers focusing on personalized treatment. These clinics provide specialized expertise, patient education, and targeted therapies, enhancing disease outcomes. The increasing establishment of rare disease networks, homecare partnerships, and telehealth integration facilitates wider access. Enhanced patient support programs, early diagnosis initiatives, and caregiver engagement strategies further drive rapid adoption. The segment benefits from growing recognition of the need for dedicated care centers for complex disorders like Sly Syndrome, supporting its robust growth trajectory.

Sly Syndrome Market Regional Analysis

- North America dominated the Sly syndrome market with the largest revenue share of 44% in 2024, supported by advanced healthcare infrastructure, early adoption of novel therapies, and the strong presence of key pharmaceutical and biotechnology players

- The market experienced substantial growth in hospitals and outpatient treatment centers, driven by innovations in therapy protocols and patient care solutions. Increased awareness of Sly Syndrome, combined with well-established diagnostic capabilities, ensures timely identification and management of patients. Specialized pediatric centers, infusion facilities, and genetic counseling services contribute to high treatment penetration

- The availability of enzyme replacement therapies (ERT) and supportive care programs further strengthens the region’s market leadership. High healthcare expenditure, robust insurance coverage, and proactive government initiatives promoting rare disease management also support continued growth. In addition, collaboration between biotech companies and hospitals is enhancing patient access to advanced therapies, ensuring sustained market dominance in North America

U.S. Sly Syndrome Market Insight

The U.S. Sly syndrome market captured the largest revenue share in North America in 2024, fueled by rapid adoption of novel therapies and the expansion of specialized treatment centers. Patients and caregivers increasingly prioritize early diagnosis and personalized care, driving demand for enzyme replacement therapy and supportive interventions. The presence of leading biotechnology firms, clinical trial networks, and robust healthcare infrastructure ensures high treatment availability. Innovations in infusion protocols, patient adherence programs, and telehealth monitoring contribute to market expansion. Awareness campaigns and advocacy efforts also encourage timely intervention, enhancing long-term patient outcomes. The integration of multidisciplinary care models, including genetic counseling and physiotherapy, supports comprehensive management. Overall, the U.S. continues to lead the North American Sly Syndrome market in both revenue and therapeutic sophistication.

Europe Sly Syndrome Market Insight

The Europe Sly syndrome market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by advanced healthcare systems, rising awareness of rare diseases, and the availability of specialized treatment centers. Countries like Germany, the U.K., and France are experiencing increased adoption of enzyme replacement therapy and supportive care protocols. The growing focus on rare disease registries, patient advocacy programs, and regulatory support fosters improved access to therapies. European healthcare providers emphasize early diagnosis, multidisciplinary treatment approaches, and patient-centric care, enhancing market growth. Urbanization, rising disposable incomes, and the expansion of pediatric and specialty clinics further contribute to the market’s development. Reimbursement policies and government initiatives supporting rare disease treatment also play a significant role. The region is witnessing steady growth across hospitals, specialty clinics, and outpatient care facilities, ensuring comprehensive patient coverage.

U.K. Sly Syndrome Market Insight

The U.K. Sly syndrome market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of rare pediatric disorders and the emphasis on specialized healthcare solutions. Early diagnosis and access to enzyme replacement therapy are accelerating treatment adoption. Healthcare infrastructure in the U.K., including pediatric specialty centers and rare disease programs, facilitates efficient patient management. Advocacy groups and national rare disease initiatives are supporting caregiver education and treatment accessibility. The availability of clinical trials and research collaborations enhances therapeutic options. Patients and clinicians are increasingly focusing on holistic management, including supportive therapies and monitoring of organ-specific complications. The U.K.’s robust healthcare system, combined with government reimbursement programs, ensures sustained market growth.

Germany Sly Syndrome Market Insight

The Germany Sly syndrome market is expected to expand at a considerable CAGR during the forecast period, fueled by well-established healthcare infrastructure, strong rare disease awareness, and access to innovative therapies. Hospitals and specialty clinics are actively implementing enzyme replacement therapies alongside supportive care protocols. The country’s emphasis on research and development, coupled with patient support initiatives, contributes to early diagnosis and improved treatment outcomes. Insurance coverage, government rare disease programs, and comprehensive care pathways support widespread adoption. Multidisciplinary management, including genetic counseling, physiotherapy, and organ-specific monitoring, further strengthens market growth. Germany’s focus on technological innovation and healthcare quality ensures sustained expansion in both pediatric and adult patient populations.

Asia-Pacific Sly Syndrome Market Insight

The Asia-Pacific Sly syndrome market is poised to grow at the fastest CAGR during 2025 to 2032, driven by rising healthcare access, increasing disposable incomes, and expansion of specialized treatment centers in countries such as India, China, and Japan. The growing number of pediatric hospitals, infusion centers, and rare disease clinics supports increased patient diagnosis and treatment. Government initiatives promoting rare disease awareness, coupled with enhanced healthcare reimbursement, are accelerating market adoption. Urbanization and technological advancements are contributing to wider availability of enzyme replacement therapies and supportive care. The presence of domestic and multinational biotechnology firms further strengthens therapy accessibility. Emerging patient support programs, telemedicine services, and clinical trial opportunities are boosting regional growth. APAC is rapidly becoming a key market for Sly Syndrome treatment due to the combination of patient population size and expanding healthcare infrastructure.

Japan Sly Syndrome Market Insight

The Japan Sly syndrome market is gaining momentum due to advanced healthcare infrastructure, high awareness of rare diseases, and increasing demand for pediatric and adult care solutions. Specialized treatment centers, hospital networks, and infusion facilities provide comprehensive management for diagnosed patients. Clinical trial participation and government support for rare disease therapies further encourage treatment adoption. Focus on early diagnosis, genetic counseling, and organ-specific monitoring enhances patient outcomes. Caregiver education, patient advocacy, and telehealth services facilitate wider access to therapy. Japan’s aging population and emphasis on convenience and safety drive demand for efficient, easily administered treatments. These factors collectively contribute to robust market growth during the forecast period.

China Sly Syndrome Market Insight

The China Sly syndrome market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding healthcare access, urbanization, and increasing awareness of rare diseases. The growing number of pediatric specialty centers, infusion facilities, and diagnostic services supports early intervention and therapy adoption. Government policies promoting rare disease treatment and reimbursement programs enhance patient access. Rising disposable incomes and healthcare expenditure facilitate treatment affordability. Domestic and multinational biotechnology firms are actively expanding their presence, ensuring therapy availability across regions. Increased patient advocacy, telemedicine initiatives, and research collaborations further support market expansion. Overall, China is emerging as a leading market for Sly Syndrome treatments within APAC.

Sly Syndrome Market Share

The Sly Syndrome industry is primarily led by well-established companies, including:

- Ultragenyx Pharmaceutical Inc. (U.S.)

- REGENXBIO Inc. (U.S.)

- Sangamo Therapeutics (U.S.)

- BioMarin (U.S.)

- Sanofi (France)

- Genpharm Services (UAE)

- Amicus Therapeutics (U.S.)

Latest Developments in Sly Syndrome Market

- In 2021, Ultragenyx Pharmaceutical Inc., the developer of vestronidase alfa (Mepsevii), expanded its clinical research program to assess long-term outcomes in patients with Sly Syndrome (MPS VII), focusing on safety, efficacy, and patient quality of life across multiple countries

- In March 2022, a multicenter observational study was launched to monitor the long-term effectiveness of enzyme replacement therapy (ERT) for Sly Syndrome patients, providing longitudinal insights into clinical progression and biomarker changes

- In April 2023, the Sly Syndrome Disease Monitoring Program (DMP) was expanded in Europe and North America to evaluate real-world patient responses to vestronidase alfa therapy, aiming to optimize treatment protocols and improve patient outcomes

- In June 2023, new guidelines were published by rare disease consortiums recommending early diagnosis and personalized treatment plans for Sly Syndrome patients, emphasizing enzyme replacement therapy and supportive care measures

- In March 2025, ongoing research into adjunct therapies for Sly Syndrome, including hematopoietic stem cell transplantation and novel ERT delivery methods, was highlighted at international rare disease conferences, indicating a growing focus on improving long-term patient outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.