Global Spinal Traction Market

Market Size in USD Billion

USD

5.96 Billion

USD

9.45 Billion

2025

2033

USD

5.96 Billion

USD

9.45 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.96 Billion | |

| USD 9.45 Billion | |

| % | |

|

Spinal Traction Market Size

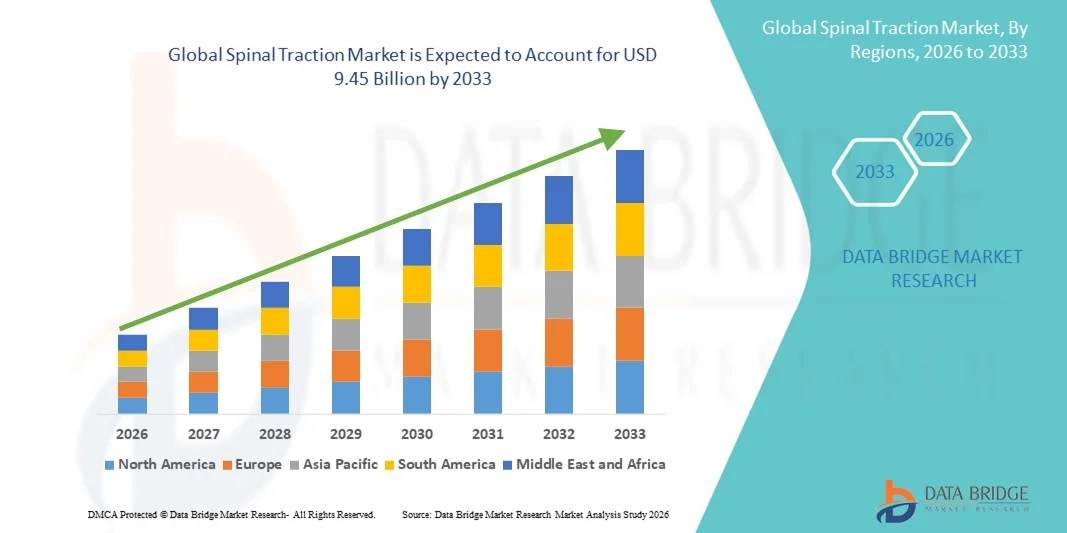

- The global spinal traction market size was valued at USD 5.96 billion in 2025 and is expected to reach USD 9.45 billion by 2033, at a CAGR of 5.94% during the forecast period

- The market growth is largely driven by the increasing prevalence of spinal disorders, rising geriatric population, and growing awareness regarding non-invasive treatment options for back and neck pain

- Furthermore, advancements in traction devices, including motorized and portable systems, along with rising adoption in clinics, hospitals, and homecare settings, are fueling the demand for spinal traction solutions. These factors collectively are propelling market expansion and positioning spinal traction as a preferred therapeutic intervention for spinal ailments

Spinal Traction Market Analysis

- Spinal traction, offering mechanical or manual decompression for the spine, is increasingly recognized as an essential therapeutic solution in both clinical and homecare settings due to its non-invasive nature, customizable protocols, and effectiveness in relieving back and neck pain and managing spinal disorders

- The escalating demand for spinal traction is primarily fueled by the rising prevalence of spinal conditions, growing geriatric population, and increasing preference for non-surgical and rehabilitative treatment options for conditions such as herniated discs, degenerative disc disease, and sciatica

- North America dominated the spinal traction market with the largest revenue share of 38.9% in 2025, driven by advanced healthcare infrastructure, high awareness of physiotherapy interventions, and widespread adoption in hospitals, rehabilitation centers, and homecare settings, with the U.S. witnessing significant growth due to innovations in mechanical and gravity-dependent traction devices

- Asia-Pacific is expected to be the fastest growing region in the spinal traction market during the forecast period due to rising incidences of spinal disorders, expanding healthcare access, and increasing disposable incomes in emerging economies

- Mechanical spinal traction segment dominated the spinal traction market with a market share of 46.7% in 2025, driven by its precision, ease of use, and effectiveness in clinical and homecare applications

Report Scope and Spinal Traction Market Segmentation

|

Attributes |

Spinal Traction Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Spinal Traction Market Trends

Increasing Adoption of Portable and Digital Traction Devices

- A notable trend in the global spinal traction market is the rising adoption of portable and digitally enabled traction devices that allow for home-based therapy and remote monitoring, improving patient compliance and convenience

- For instance, the Saunders Cervical Traction Device offers adjustable settings for home use, while the Pro-Adjustable Lumbar Traction systems can be operated with minimal clinical supervision, supporting patient self-management

- Digital spinal traction devices integrate features such as real-time tension monitoring, automated session adjustments, and user-friendly interfaces, enabling patients to track progress and receive optimized treatment protocols

- These devices can be paired with mobile apps or connected platforms to provide physiotherapists with remote data access, allowing healthcare providers to fine-tune therapy and ensure safety and effectiveness

- The trend towards smart, portable, and digitally connected spinal traction devices is reshaping patient expectations, with companies such as DJO Global developing systems with integrated monitoring and customizable traction programs

- Healthcare providers are increasingly adopting hybrid systems that combine mechanical traction with complementary modalities such as heat, massage, or electrical stimulation to enhance patient outcomes

- The demand for spinal traction solutions that offer portability, digital control, and home-use convenience is expanding rapidly across both clinical and homecare segments, as patients increasingly seek non-invasive and flexible treatment options

Spinal Traction Market Dynamics

Driver

Rising Prevalence of Spinal Disorders and Preference for Non-Surgical Treatment

- The increasing incidence of spinal disorders, coupled with growing preference for non-surgical and rehabilitative interventions, is a key driver of heightened demand for spinal traction devices

- For instance, in May 2025, BTL Industries launched a motorized spinal traction system designed for homecare and clinical use, emphasizing safe and effective non-invasive therapy, expected to drive market growth

- As awareness grows regarding the benefits of spinal traction in conditions such as herniated discs, degenerative disc disease, and sciatica, more patients and clinics are adopting these therapies as first-line interventions

- Furthermore, the integration of user-friendly mechanical and gravity-dependent traction devices in physiotherapy centers and hospitals is expanding treatment access and increasing adoption rates

- The convenience of home-use traction systems, adjustable therapy settings, and the ability to personalize treatment protocols are key factors propelling spinal traction adoption in both clinical and homecare settings

- Rising investments in spinal rehabilitation centers and physiotherapy clinics are further boosting adoption of advanced spinal traction solutions in urban and semi-urban areas

- Increasing awareness campaigns and educational initiatives highlighting the long-term benefits of spinal traction therapy are driving higher acceptance among patients and healthcare professionals

Restraint/Challenge

Device Costs and Patient Compliance Concerns

- The relatively high initial cost of advanced spinal traction systems, particularly motorized and digital models, poses a challenge to broader market penetration, especially in developing regions or price-sensitive patient segments

- For instance, high-priced motorized lumbar traction systems may limit adoption despite their clinical benefits, creating a barrier for smaller clinics and homecare users

- Patient compliance and proper usage issues, particularly in home-based settings, can impact the effectiveness of spinal traction therapy, limiting perceived value and satisfaction

- Overcoming these challenges requires enhanced patient education, cost-effective device designs, and training on safe and correct usage to ensure therapy effectiveness and adherence

- While prices for basic mechanical traction devices are lower, the perceived premium for advanced digital systems continues to restrict widespread adoption, especially where clinical supervision is limited

- Addressing cost barriers, improving device accessibility, and providing patient guidance and monitoring will be essential to support sustained growth in the spinal traction market

- Strict regulatory requirements for medical devices and variable reimbursement policies across regions can delay market entry and affect adoption rates.

- Limited availability of trained physiotherapists and technicians to guide patients on device usage in homecare settings may restrict effective utilization of spinal traction solutions

Spinal Traction Market Scope

The market is segmented on the basis of type, applications, and devices.

- By Type

On the basis of type, the spinal traction market is segmented into manual spinal traction and mechanical spinal traction. The mechanical spinal traction segment dominated the market with the largest revenue share of 46.7% in 2025, driven by its precision, ease of use, and widespread adoption in clinical and homecare settings. Mechanical traction devices allow for controlled tension and automated adjustments, which enhance patient safety and treatment effectiveness. Hospitals, physiotherapy centers, and rehabilitation clinics prefer mechanical spinal traction for managing complex spinal disorders such as herniated discs and degenerative disc disease. The segment’s dominance is also supported by increasing innovations in motorized and digital traction devices, offering features such as real-time monitoring and customizable therapy sessions. Patients and clinicians alike favor mechanical traction for its reliability, consistent therapeutic outcomes, and ability to integrate with complementary rehabilitation treatments.

The manual spinal traction segment is anticipated to witness the fastest growth rate during the forecast period, fueled by its affordability, portability, and ease of use in homecare and outpatient settings. Manual devices are particularly suitable for emerging markets and small clinics where cost constraints limit access to motorized traction systems. They are also preferred by patients seeking non-invasive, self-managed spinal therapy under remote supervision. The simplicity, low maintenance, and lightweight design of manual spinal traction devices make them increasingly popular among elderly users and those with mobility restrictions. Growing awareness about self-care and home physiotherapy is expected to accelerate adoption, further supporting segment growth.

- By Applications

On the basis of applications, the spinal traction market is segmented into slipped discs, bone spurs, degenerative disc disease, herniated discs, facet disease, sciatica, foramina stenosis, and pinched nerves. The herniated discs segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of disc herniation globally and the effectiveness of spinal traction in relieving nerve compression and pain. Herniated discs often result in chronic back pain, limited mobility, and sciatica, prompting patients and clinicians to adopt traction therapy as a first-line, non-surgical intervention. Clinical studies and physiotherapy guidelines recommend spinal traction for controlled decompression of the affected spinal segment, making it a preferred treatment option. In addition, growing awareness among patients about non-invasive alternatives to surgery and the availability of advanced traction devices contribute to the segment’s dominance. Healthcare providers increasingly rely on traction therapy to improve patient outcomes, reduce recovery time, and enhance quality of life.

The sciatica segment is expected to witness the fastest growth rate during the forecast period, fueled by the increasing incidence of nerve compression and related lower back pain worldwide. Sciatica affects a large portion of the working-age population, creating significant demand for conservative management techniques such as spinal traction. Patients prefer traction therapy for its ability to relieve nerve pressure, improve mobility, and reduce reliance on medications. Rising adoption of home-based traction devices and outpatient physiotherapy programs further supports growth. The segment benefits from growing patient awareness of non-invasive therapies and the trend toward personalized treatment plans tailored to symptom severity and spinal condition.

- By Devices

On the basis of devices, the spinal traction market is segmented into continuous traction, gravity-dependent traction, and manual traction. The continuous traction segment dominated the market with the largest revenue share in 2025, driven by its ability to provide uninterrupted, controlled spinal decompression over extended periods. Continuous traction systems are widely used in hospitals and rehabilitation centers for treating severe spinal disorders, ensuring consistent tension and reducing patient discomfort. They allow clinicians to adjust therapy parameters precisely, improving treatment outcomes for conditions such as degenerative disc disease and foramina stenosis. The dominance of continuous traction is also supported by technological advancements such as motorized and digital monitoring systems, which enhance patient safety, comfort, and clinical efficiency. Continuous traction is preferred for long-duration therapies, particularly in patients requiring gradual decompression.

The gravity-dependent traction segment is anticipated to witness the fastest growth rate during the forecast period, fueled by its low cost, simplicity, and ease of use for homecare and outpatient settings. Gravity-dependent traction devices rely on body weight or adjustable angles to apply decompressive force, making them accessible to a broader patient population. They are particularly popular in emerging markets and for patients seeking self-managed spinal therapy. Increasing awareness about home physiotherapy and the growing adoption of portable traction systems are expected to accelerate segment growth. The segment also benefits from healthcare initiatives promoting non-invasive treatments for back and neck disorders.

Spinal Traction Market Regional Analysis

- North America dominated the spinal traction market with the largest revenue share of 38.9% in 2025, driven by advanced healthcare infrastructure, high awareness of physiotherapy interventions, and widespread adoption in hospitals, rehabilitation centers, and homecare settings

- Patients and healthcare providers in the region highly value the precision, safety, and effectiveness offered by mechanical and continuous spinal traction devices in hospitals, physiotherapy centers, and homecare settings

- This widespread adoption is further supported by high awareness of physiotherapy interventions, a strong presence of key industry players, and rising investments in spinal rehabilitation facilities, establishing spinal traction as a preferred treatment option for conditions such as herniated discs, sciatica, and degenerative disc disease

U.S. Spinal Traction Market Insight

The U.S. spinal traction market captured the largest revenue share of 80% in 2025 within North America, fueled by the rising prevalence of spinal disorders and increasing preference for non-surgical treatment options. Patients and healthcare providers are increasingly adopting mechanical and continuous traction systems in hospitals, physiotherapy centers, and homecare settings. The growing awareness of spinal health, combined with the availability of advanced traction devices with digital monitoring and automated tension control, further propels the market. Moreover, the expansion of outpatient rehabilitation programs and home-based therapy options is significantly contributing to the market’s growth.

Europe Spinal Traction Market Insight

The Europe spinal traction market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the increasing incidence of spinal disorders and the growing focus on physiotherapy and non-invasive treatments. Rising urbanization, coupled with the adoption of advanced traction devices in hospitals and rehabilitation centers, is fostering market growth. European healthcare providers are also emphasizing patient-centered care and home-based therapy programs, further boosting the adoption of spinal traction solutions across clinical and homecare applications.

U.K. Spinal Traction Market Insight

The U.K. spinal traction market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing awareness of spinal health and the demand for non-surgical, rehabilitative treatment options. In addition, the growing prevalence of conditions such as herniated discs, sciatica, and degenerative disc disease is encouraging hospitals and physiotherapy clinics to adopt spinal traction devices. The U.K.’s emphasis on healthcare innovation, along with the availability of portable and mechanical traction systems, is expected to continue stimulating market growth.

Germany Spinal Traction Market Insight

The Germany spinal traction market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and high adoption of physiotherapy treatments. Germany’s focus on preventive care and non-invasive therapy promotes the use of mechanical and continuous spinal traction devices in hospitals and rehabilitation centers. The integration of smart features such as digital tension monitoring and customizable therapy sessions is also becoming increasingly prevalent, with a strong preference for devices that ensure patient safety and treatment effectiveness.

Asia-Pacific Spinal Traction Market Insight

The Asia-Pacific spinal traction market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing urbanization, rising prevalence of spinal disorders, and expanding healthcare access in countries such as China, Japan, and India. The region’s growing focus on non-surgical treatments and physiotherapy, supported by government initiatives promoting rehabilitation and spinal health, is driving adoption. Furthermore, the availability of cost-effective mechanical and manual traction devices, along with increasing awareness of home-based therapy, is expanding the market to a wider patient base.

Japan Spinal Traction Market Insight

The Japan spinal traction market is gaining momentum due to the country’s high awareness of spinal health, advanced medical infrastructure, and increasing adoption of home-based therapy. The Japanese market emphasizes non-invasive treatment options, and spinal traction devices are widely used in hospitals, physiotherapy clinics, and homecare settings. Moreover, the aging population in Japan is likely to spur demand for easier-to-use, safe, and effective traction devices in both residential and clinical sectors.

India Spinal Traction Market Insight

The India spinal traction market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s growing geriatric population, rising incidence of spinal disorders, and increasing adoption of non-surgical treatment methods. India is emerging as a key market for physiotherapy and rehabilitation services, and spinal traction devices are becoming popular in hospitals, outpatient clinics, and homecare settings. Government initiatives promoting healthcare access, combined with the availability of affordable manual and mechanical traction devices, are key factors propelling the market in India.

Spinal Traction Market Share

The Spinal Traction industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Zimmer Biomet (U.S.)

- BTL Industries (U.S.)

- HMS Medical Systems (India)

- Orthofix Medical Inc. (U.S.)

- Stoll‑Medizintechnik GmbH (Germany)

- Spinetronics, Inc. (U.S.)

- Hill Laboratories Company (U.S.)

- VAX‑D Medical Technologies, LLC (U.S.)

- CERT Health Sciences, LLC (U.S.)

- Saunders Group Inc (U.S.)

- Sechrist Industries (U.S.)

- Kingbrand International (U.S.)

- Innova Medical Group (U.S.)

- Richmarq (U.S.)

- Swash Medical (U.S.)

- Stryker (U.S.)

- Globus Medical, Inc. (U.S.)

- DJO, LLC (U.S.)

What are the Recent Developments in Global Spinal Traction Market?

- In September 2025, ONWARD Medical reported achieving strong commercial traction of its ARC‑EX® system with sales to U.S. clinics and submitted regulatory filings to expand indications including home use, while securing FDA IDE approval for a related lumbar device in its pipeline

- In August 2025, a randomized, controlled clinical study published in BMC Musculoskeletal Disorders reported that use of a traction‑bed device (Movento) in combination with standard rehabilitation significantly improved pain scores, functional outcomes, and quality of life in patients with lumbar osteoarthritis/spondylosis compared with rehabilitation alone, highlighting clinical evidence supporting traction therapy benefits

- In March 2025, Excite Medical exhibited its DRX9000 spinal decompression and traction machines recognized as leading non‑surgical decompression systems at Arab Health Dubai, highlighting continued industry focus on advanced traction solutions

- In February 2025, a multicenter trial protocol for the TracCerv2 study was published, detailing a large randomized controlled trial evaluating the effect of mechanical cervical traction on disability in patients with cervical radiculopathy, underscoring growing clinical research interest in traction therapy’s therapeutic value

- In May 2023, Zimmer MedizinSysteme GmbH’s clTrac powered traction equipment received clearance via an FDA 510(k) submission (K222912), enabling broader clinical use of powered spinal traction devices for non‑invasive decompression therapy in conditions such as herniated discs and degenerative disc disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.