Global Stadiometers Market

Market Size in USD Million

USD

530.20 Million

USD

789.34 Million

2024

2032

USD

530.20 Million

USD

789.34 Million

2024

2032

| 2025 - 2032 | |

| USD 530.20 Million | |

| USD 789.34 Million | |

| % | |

|

Stadiometers Market Size

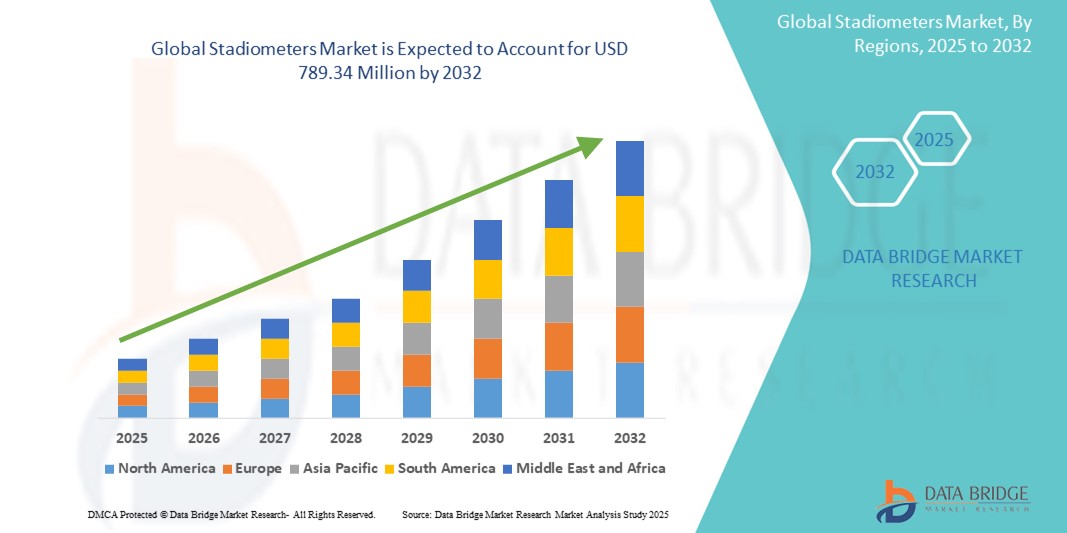

- The global stadiometers market size was valued at USD 530.20 million in 2024 and is expected to reach USD 789.34 million by 2032, at a CAGR of 5.10% during the forecast period

- The market growth is largely fueled by the increasing emphasis on early diagnosis and preventive healthcare, particularly within pediatric, geriatric, and bariatric patient populations, leading to widespread use in hospitals, clinics, and health check-up centers

- Furthermore, rising global healthcare spending and expanding access to primary care services are establishing stadiometers as essential tools for routine physical examinations. These converging factors are driving the demand for accurate and reliable height measurement devices, thereby significantly boosting the industry’s growth

Stadiometers Market Analysis

- Stadiometers, essential medical devices used for precise height measurement, are increasingly integral to routine health assessments across hospitals, clinics, and wellness centers, particularly in pediatric, geriatric, and bariatric care settings, due to their clinical accuracy and simplicity of use

- The escalating demand for stadiometers is primarily fueled by the global rise in preventive healthcare awareness, expanding pediatric populations, and the integration of physical growth monitoring in routine medical evaluations

- North America dominated the stadiometers market with the largest revenue share of 39.2% in 2024, supported by advanced healthcare infrastructure, high patient footfall for annual wellness visits, and widespread use in school health programs, with the U.S. leading due to regular height and BMI tracking protocols

- Asia-Pacific is expected to be the fastest growing region in the stadiometers market during the forecast period due to expanding healthcare access, rising child health monitoring programs, and increasing investments in primary care

- Mechanical stadiometers segment dominated the stadiometers market with a market share of 46% in 2024, driven by their affordability, portability, and continued preference in community health and school-based screenings

Report Scope and Stadiometers Market Segmentation

|

Attributes |

Stadiometers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Stadiometers Market Trends

“Digitalization and Integration with Electronic Health Records (EHRs)”

- A significant and emerging trend in the global stadiometers market is the digital transformation of healthcare settings, which includes the growing preference for digital and wireless stadiometers integrated with Electronic Health Records (EHRs). This integration is improving workflow efficiency, minimizing manual entry errors, and enhancing the accuracy of growth tracking over time

- For instance, Seca’s 286 Wireless Ultrasonic Stadiometer can transmit height measurements directly to EHR systems, streamlining pediatric and adult growth assessments. Similarly, Charder Medical’s HM200P Digital Stadiometer offers USB and Bluetooth connectivity for seamless data transfer into patient management platforms

- These digital stadiometers also support advanced features such as auto-calibration, voice guidance, and high-precision sensors, which enable consistent and user-friendly measurements, especially in high-throughput environments such as pediatric departments or health camps

- Integration with digital platforms allows for long-term tracking and trend analysis, helping healthcare professionals identify early signs of growth abnormalities or chronic conditions. It also enhances care coordination by enabling remote access to measurement data across facilities

- The trend towards connected and automated measurement solutions is reshaping expectations for anthropometric assessment tools. Companies such as Detecto and Health o meter® Professional Scales are developing smart stadiometers that align with digital record-keeping requirements and clinical protocols, offering plug-and-play compatibility with hospital information systems

- The demand for digital, EHR-compatible stadiometers is increasing rapidly across hospitals, specialty clinics, and schools as healthcare providers seek to modernize infrastructure and improve patient outcomes through technology-driven solutions

Stadiometers Market Dynamics

Driver

“Increasing Emphasis on Preventive Healthcare and Growth Monitoring”

- The rising global focus on early diagnosis, preventive health checkups, and pediatric growth monitoring is a key driver fueling the demand for stadiometers in clinical and community healthcare settings

- For instance, UNICEF and WHO’s growth monitoring initiatives in developing regions have expanded the use of height measurement tools in early childhood health programs. Similarly, the U.S. Preventive Services Task Force recommends regular height screening as part of pediatric and geriatric wellness protocols

- As health systems shift toward value-based care, routine physical assessments—including height measurement are becoming standard practice, especially in managing conditions such as malnutrition, endocrine disorders, and obesity

- Stadiometers enable healthcare providers to collect essential anthropometric data accurately and efficiently, aiding in early intervention and long-term health tracking. In school and workplace wellness programs, stadiometers play a vital role in large-scale health screenings

- The growing availability of portable and digital models, along with government initiatives to improve access to primary healthcare, are further supporting market expansion across both developed and developing regions

Restraint/Challenge

“Cost Sensitivity in Low-Income Settings and Limited Technological Awareness”

- Despite their clinical utility, the adoption of advanced stadiometers in low-income or resource-constrained settings is hindered by cost sensitivity and limited awareness of digital measurement technologies

- Manual stadiometers remain prevalent due to their low cost and ease of use, particularly in rural clinics and public health camps, but they lack the accuracy and data integration capabilities of digital counterparts

- In many regions, healthcare providers are unaware of the advantages offered by digital or EHR-compatible models, limiting their adoption despite growing infrastructure for digital health systems

- Moreover, the perception of height measurement as a basic clinical task can reduce the priority given to investing in more advanced tools, especially where budget constraints exist

- To overcome these challenges, manufacturers are focusing on affordable digital models and awareness campaigns that demonstrate how improved accuracy and data integration can enhance patient care

- Expanding training programs and offering scalable pricing strategies are also critical for broadening market penetration in underserved regions

Stadiometers Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the stadiometers market is segmented into digital stadiometers and mechanical stadiometers. The mechanical stadiometers segment dominated the market with the largest market revenue share of 46% in 2024, owing to their affordability, simplicity, and widespread use in primary healthcare settings, schools, and public health camps. These devices are favored in resource-constrained environments due to their ease of use, portability, and minimal maintenance requirements.

The digital stadiometers segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by the increasing adoption of electronic health records (EHRs) and the need for accurate, real-time data integration. Digital stadiometers offer high precision, automatic data transmission, and compatibility with hospital information systems, making them ideal for use in hospitals and advanced clinical settings. Features such as ultrasonic measurement, voice guidance, and wireless connectivity are enhancing their appeal in modern healthcare facilities.

- By Application

On the basis of application, the stadiometers market is segmented into hospitals, clinics, and others. The hospitals segment held the largest revenue share in 2024, driven by the routine use of stadiometers for inpatient and outpatient assessments, particularly in pediatrics, endocrinology, and geriatrics. Hospitals demand high-accuracy tools that integrate seamlessly with digital records, making them major adopters of advanced stadiometry systems. The push for comprehensive patient assessments during annual physicals also supports growth in this segment.

The clinics segment is projected to grow at the fastest rate during the forecast period, as primary care and specialty clinics expand services for preventive and diagnostic care. Clinics increasingly prefer portable and digital stadiometers to support rapid patient throughput and improve diagnostic accuracy. In addition, the "others" category which includes schools, fitness centers, and research institutions continues to grow steadily due to rising health awareness and routine height screening initiatives.

Stadiometers Market Regional Analysis

- North America dominated the stadiometers market with the largest revenue share of 39.2% in 2024, supported by advanced healthcare infrastructure, high patient footfall for annual wellness visits, and widespread use in school health programs, with the U.S. leading due to regular height and BMI tracking protocols

- Healthcare providers in the region highly value the clinical accuracy, reliability, and growing availability of digital stadiometers that seamlessly integrate with electronic health records, enabling efficient growth monitoring and long-term patient tracking

- This widespread adoption is further supported by well-established healthcare infrastructure, high healthcare expenditure, and strong government and institutional support for regular health screenings, making stadiometers an essential diagnostic tool across hospitals, clinics, and community health centers

U.S. Stadiometers Market Insight

The U.S. stadiometers market captured the largest revenue share of 79% in 2024 within North America, driven by routine height assessments in preventive care and a high demand for accurate growth monitoring tools. The strong presence of pediatric and geriatric healthcare services, combined with established use of EHRs, supports the adoption of digital stadiometers across hospitals and clinics. Moreover, increasing initiatives promoting child wellness and standardized screenings in schools and healthcare facilities contribute to the market’s continued expansion.

Europe Stadiometers Market Insight

The Europe stadiometers market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by an aging population, increased emphasis on chronic disease management, and routine anthropometric measurements in clinical practice. Countries across the region are investing in digitized healthcare infrastructure, encouraging the use of integrated measurement systems. The adoption of both digital and portable mechanical stadiometers is increasing in schools, community clinics, and research programs, supporting early detection and monitoring of growth-related abnormalities.

U.K. Stadiometers Market Insight

The U.K. stadiometers market is anticipated to grow at a notable CAGR during the forecast period, supported by the country’s strong focus on pediatric and primary care services. Preventive screening protocols within the National Health Service (NHS) and regular school-based health assessments are key drivers. In addition, the U.K.’s digital health initiatives and growing use of connected diagnostic tools are promoting the adoption of advanced digital stadiometers in both public and private healthcare settings.

Germany Stadiometers Market Insight

The Germany stadiometers market is expected to expand at a significant CAGR during the forecast period, backed by the country’s advanced healthcare infrastructure and emphasis on accurate diagnostic equipment. Germany’s strong public health initiatives, particularly for children and the elderly, and high demand for precision medical devices drive adoption. Integration with EHR systems and a preference for high-quality, locally manufactured stadiometers are also fueling market growth in both clinical and outpatient settings.

Asia-Pacific Stadiometers Market Insight

The Asia-Pacific stadiometers market is poised to grow at the fastest CAGR of 23.1% during the forecast period of 2025 to 2032, driven by expanding access to healthcare, rising birth rates, and government-led child health programs. Countries such as China, India, and Japan are witnessing increasing investments in public health screening and early disease detection. The region’s adoption of cost-effective digital solutions and portable stadiometers supports widespread use in schools, rural clinics, and urban hospitals.

Japan Stadiometers Market Insight

The Japan stadiometers market is gaining momentum due to the country’s aging demographic, robust healthcare infrastructure, and growing preference for precise digital diagnostic tools. Routine screenings in hospitals and elderly care facilities fuel demand for high-accuracy stadiometers. Integration with hospital information systems and the use of ultrasonic technologies in height measurement are becoming increasingly common, supporting market expansion.

India Stadiometers Market Insight

The India stadiometers market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to rising child health monitoring initiatives, rapid healthcare infrastructure development, and the growing availability of affordable medical devices. With a strong push toward public health programs, including routine school health screenings and maternal-child health services, India is seeing widespread adoption of mechanical and digital stadiometers, particularly in rural and semi-urban regions.

Stadiometers Market Share

The stadiometers industry is primarily led by well-established companies, including:

- Seca GmbH & Co. KG (Germany)

- Detecto Scale Company (U.S.)

- Health o meter Professional Scales (U.S.)

- Charder Electronic Co., Ltd. (Taiwan)

- Marsden Weighing Group Ltd. (U.K.)

- ADE Germany GmbH (Germany)

- Tanita Corporation (Japan)

- Natus Medical Incorporated (U.S.)

- Invacare Corporation (U.S.)

- Kern & Sohn GmbH (Germany)

- Cardinal Scale Manufacturing Company (U.S.)

- Befour, Inc. (U.S.)

- Yamato Scale Co., Ltd. (Japan)

- Innovative Scales, LLC (U.S.)

- Zhongshan Camry Electronic Co., Ltd. (China)

- HARDIK MEDI-TECH (India)

- Algen Scale Corporation (U.S.)

- GIMA S.p.A. (Italy)

- SR Instruments, Inc. (U.S.)

- Lafayette Instrument Company (U.S.)

What are the Recent Developments in Global Stadiometers Market?

- In March 2024, Seca GmbH & Co. KG, a global leader in medical measuring systems, introduced its updated Seca 286 Wireless Ultrasonic Stadiometer, featuring enhanced wireless connectivity and integration capabilities with Electronic Health Records (EHRs). This innovation is designed to support modern hospital workflows by providing automatic, contactless height measurements with voice guidance and real-time data transmission, reinforcing Seca’s leadership in precision anthropometric devices

- In February 2024, Charder Electronic Co., Ltd. launched its HM300D Digital Stadiometer, targeted at pediatric and primary care settings. This model offers USB and Bluetooth compatibility for seamless integration with health information systems and is equipped with easy-to-read digital displays and auto-calibration features. The release underlines Charder’s commitment to offering technologically advanced yet affordable stadiometry solutions for developing healthcare markets

- In January 2024, Detecto Scale Company, a prominent U.S.-based manufacturer of medical scales and measurement systems, introduced a compact, foldable portable stadiometer designed for mobile clinics and school health programs. The device emphasizes lightweight construction and ease of setup while maintaining clinical accuracy, responding to growing demand for mobility in preventive health screenings and outreach initiatives

- In December 2023, Health o meter® Professional Scales, a leading provider of clinical measurement tools, announced the launch of its 600KL Digital Height Rod, which integrates with its popular line of digital physician scales. This new device aims to improve workflow efficiency in busy clinical environments by enabling simultaneous weight and height measurements, enhancing the accuracy and speed of BMI calculations for patient assessments

- In November 2023, Marsden Group, a UK-based medical measurement specialist, expanded its range of digital stadiometers with the introduction of the M-260, tailored for hospitals and bariatric care units. This new model offers a high weight capacity platform and integrated height rod with digital output, highlighting Marsden’s focus on addressing the needs of diverse patient populations and supporting the shift toward digitally connected healthcare systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.