Global Starch Ethers Market

Market Size in USD Billion

USD

1.70 Billion

USD

2.38 Billion

2024

2032

USD

1.70 Billion

USD

2.38 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.70 Billion | |

| USD 2.38 Billion | |

| % | |

|

Starch Ethers Market Size

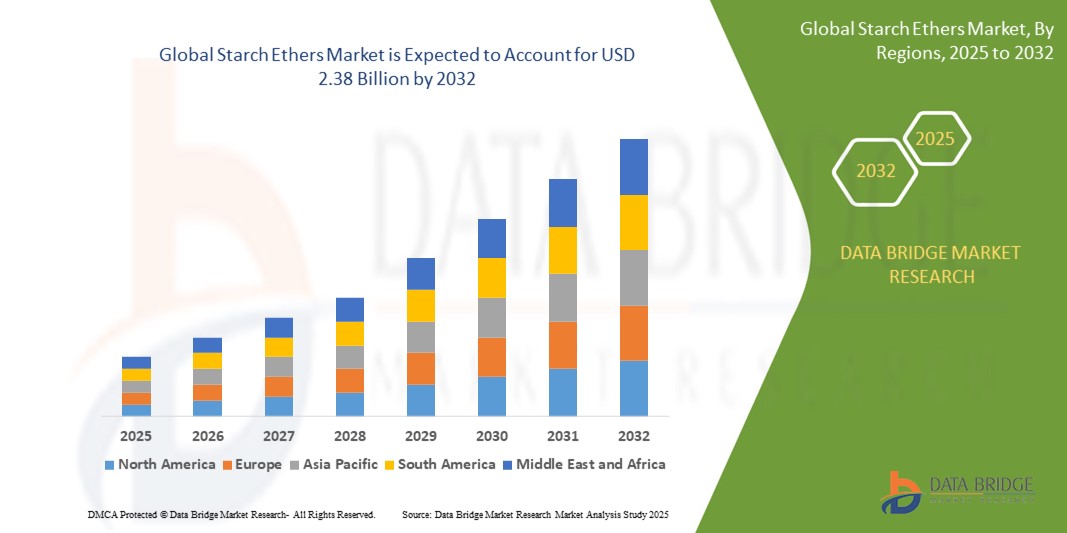

- The global starch ethers market size was valued at USD 1.70 billion in 2024 and is expected to reach USD 2.38 billion by 2032, at a CAGR of 4.3% during the forecast period

- The market growth is primarily driven by the increasing demand for processed and convenience foods, advancements in starch modification technologies, and the growing application of starch ethers in diverse industries such as food, pharmaceuticals, and textiles

- Rising consumer preference for clean-label, sustainable, and plant-based ingredients is further propelling the adoption of starch ethers as versatile functional additives, boosting overall market expansion

Starch Ethers Market Analysis

- Starch ethers, derived from natural starches through chemical modification, are widely used as functional additives in various industries due to their stabilizing, thickening, emulsifying, and binding properties

- The growing demand for starch ethers is fueled by their extensive use in food and beverage applications for texture enhancement, increasing industrial applications in paper and textile production, and rising adoption in pharmaceuticals for drug formulation

- North America dominated the starch ethers market with the largest revenue share of 31.7% in 2024, driven by advanced food processing industries, high consumer demand for convenience foods, and the presence of key market players

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, attributed to rapid industrialization, increasing food processing activities, and rising disposable incomes in countries such as China and India

- The corn-based segment dominated the largest market revenue share of 57.5% in 2024, attributed to its abundant availability, cost-effectiveness, and versatility across industries such as food and beverages, pharmaceuticals, and textiles. Its functional properties, such as thickening and stabilizing, along with growing consumer demand for clean-label and non-GMO products, further boost its dominance

Report Scope and Starch Ethers Market Segmentation

|

Attributes |

Starch Ethers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Starch Ethers Market Trends

“Increasing Integration of Clean-Label and Sustainable Ingredients”

- The global starch ethers market is experiencing a significant trend toward the integration of clean-label and sustainable ingredients, driven by consumer demand for natural and eco-friendly products

- These modified starches, derived from sources such as corn, cassava, wheat, and potato, are processed to enhance functionality while maintaining natural properties, appealing to health-conscious consumers

- Advanced processing technologies enable starch ethers to meet clean-label standards, offering improved texture, stability, and shelf life without synthetic additives

- For instances, companies are developing starch ethers for use in organic and non-GMO food products, such as plant-based dairy alternatives and gluten-free baked goods, to cater to evolving consumer preferences

- This trend enhances the appeal of starch ethers for manufacturers in food, pharmaceuticals, and textiles, aligning with sustainability goals and increasing market adoption

- Starch ethers are also being explored for biodegradable packaging solutions, reducing reliance on petroleum-based materials and supporting environmentally friendly applications

Starch Ethers Market Dynamics

Driver

“Rising Demand for Functional and Clean-Label Food Products”

- The growing consumer preference for clean-label, natural, and minimally processed foods is a key driver for the global starch ethers market

- Starch ethers enhance food products by providing functions such as thickening, stabilizing, and emulsifying, improving texture and consistency in items such as sauces, soups, and bakery goods

- Government regulations in regions such as North America and Europe, promoting transparency in food labeling, are encouraging the adoption of starch ethers as natural alternatives to synthetic additives

- The proliferation of plant-based and gluten-free diets, particularly in North America, is driving demand for starch ethers derived from sources such as cassava and potato, which offer functional benefits in food processing

- Manufacturers are increasingly incorporating starch ethers into processed and convenience foods to meet consumer expectations for high-quality, sustainable products

Restraint/Challenge

“High Production Costs and Regulatory Compliance”

- The high cost of producing starch ethers, including raw material sourcing and advanced modification processes, can be a significant barrier, particularly for manufacturers in emerging markets

- The complexity of modifying starches to meet specific functional requirements, such as clean-label or non-GMO standards, adds to production costs

- Data from industry reports indicates that fluctuating prices of raw materials such as corn, cassava, and wheat further complicate cost management for starch ether producers

- Regulatory challenges related to food safety and labeling standards vary across regions, creating compliance issues for international manufacturers and limiting market expansion

- Consumer concerns about the environmental impact of starch production, particularly in water-intensive processes, may also deter adoption in regions with high sustainability awareness

Starch Ethers market Scope

The market is segmented on the basis of source, function, and end use.

- By Source

On the basis of source, the global starch ethers market is segmented into corn-based, cassava-based, wheat-based, potato-based, and others. The corn-based segment dominated the largest market revenue share of 57.5% in 2024, attributed to its abundant availability, cost-effectiveness, and versatility across industries such as food and beverages, pharmaceuticals, and textiles. Its functional properties, such as thickening and stabilizing, along with growing consumer demand for clean-label and non-GMO products, further boost its dominance.

The cassava-based segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its high starch content, cost-effectiveness, and increasing demand for gluten-free and natural ingredients. Cassava starch’s unique properties, such as high paste clarity and freeze-thaw stability, make it a preferred choice in food, pharmaceutical, and textile applications, particularly in Asia-Pacific, where cassava production is abundant.

- By Function

On the basis of function, the global starch ethers market is segmented into stabilizers, thickeners, emulsifiers, binders, and others. The thickeners segment dominated the market with a revenue share of 49% in 2024, driven by its extensive use in food and beverage applications to enhance texture, consistency, and mouthfeel in products such as soups, sauces, and dairy items. Thickeners are also critical in pharmaceuticals and cosmetics for improving formulation viscosity and stability.

The stabilizers segment is anticipated to experience the fastest growth rate from 2025 to 2032, fueled by rising demand for processed and convenience foods, where stabilizers enhance shelf life and product stability. Advancements in starch modification technologies are enabling the development of stabilizers with improved thermal stability and viscosity, further driving adoption across food, pharmaceutical, and industrial applications.

- By End Use

On the basis of end use, the global starch ethers market is segmented into food and beverages, animal feed, paper, pharmaceuticals, and textiles. The food and beverages segment accounted for the largest market revenue share of 44% in 2024, driven by the critical role of starch ethers in enhancing texture, stability, and shelf life in products such as bakery items, sauces, and confectionery. The rising global demand for convenience and processed foods further propels this segment’s dominance.

The pharmaceuticals segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the increasing use of starch ethers as excipients in tablet formulations for their binding and disintegration properties. The global rise in pharmaceutical demand, fueled by population growth and healthcare needs, along with the shift toward clean-label and non-GMO ingredients, is accelerating adoption in this sector.

Starch Ethers Market Regional Analysis

- North America dominated the starch ethers market with the largest revenue share of 31.7% in 2024, driven by advanced food processing industries, high consumer demand for convenience foods, and the presence of key market players

- Consumers prioritize starch ethers for their role as stabilizers, thickeners, and emulsifiers, enhancing product texture and shelf life, particularly in regions with high demand for convenience foods

- Growth is supported by advancements in starch ether production technologies, such as improved modification processes, alongside rising adoption in food, pharmaceuticals, and paper industries

U.S. Starch Ethers Market Insight

The U.S. starch ethers market captured the largest revenue share of 72.9% in 2024 within North America, fueled by strong demand in the food and beverage sector and growing consumer preference for clean-label and plant-based ingredients. The trend toward functional foods and increasing regulations promoting safe additives further boost market expansion. The use of starch ethers in pharmaceuticals and paper industries complements growth, creating a diverse application ecosystem.

Europe Starch Ethers Market Insight

The Europe starch ethers market is expected to witness significant growth, supported by regulatory emphasis on sustainable and safe food additives. Consumers seek starch ethers that enhance product stability and texture while meeting clean-label standards. Growth is prominent in both food processing and pharmaceutical applications, with countries such as Germany and France showing significant uptake due to rising environmental concerns and demand for high-quality products.

U.K. Starch Ethers Market Insight

The U.K. market for starch ethers is expected to witness rapid growth, driven by demand for improved food texture and stability in urban and suburban markets. Increased interest in clean-label products and rising awareness of the functional benefits of starch ethers encourage adoption. Evolving regulations on food safety and sustainability influence consumer choices, balancing functionality with compliance.

Germany Starch Ethers Market Insight

Germany is expected to witness rapid growth in the starch ethers market, attributed to its advanced food processing and pharmaceutical sectors and high consumer focus on product quality and sustainability. German consumers prefer technologically advanced starch ethers that enhance product texture and contribute to energy-efficient production processes. The integration of these products in premium food and pharmaceutical applications supports sustained market growth.

Asia-Pacific Starch Ethers Market Insight

The Asia-Pacific region is expected to witness the fastest growth rate, driven by expanding food and beverage production and rising disposable incomes in countries such as China, India, and Japan. Increasing awareness of functional ingredients, such as stabilizers and thickeners, is boosting demand. Government initiatives promoting sustainable food processing and pharmaceutical advancements further encourage the use of advanced starch ethers.

Japan Starch Ethers Market Insight

Japan’s starch ethers market is expected to witness rapid growth due to strong consumer preference for high-quality, functional ingredients that enhance food texture and pharmaceutical efficacy. The presence of major food and pharmaceutical manufacturers and the integration of starch ethers in processed foods and drugs accelerate market penetration. Rising interest in clean-label and sustainable products also contributes to growth.

China Starch Ethers Market Insight

China holds the largest share of the Asia-Pacific starch ethers market, propelled by rapid urbanization, rising food processing demands, and increasing adoption of functional ingredients. The country’s growing middle class and focus on innovative food and pharmaceutical solutions support the adoption of advanced starch ethers. Strong domestic manufacturing capabilities and competitive pricing enhance market accessibility.

Japan Starch Ethers Market Insight

Japan’s starch ethers market is expected to witness robust growth due to strong consumer preference for high-quality, technologically advanced telematics solutions that enhance driving comfort, safety, and connectivity. The presence of major automotive manufacturers and integration of telematics systems in OEM vehicles accelerate market penetration. Rising interest in aftermarket customization and connected car services also contributes to growth.

China Starch Ethers Market Insight

The China holds the largest share of the Asia-Pacific starch ethers market, propelled by rapid urbanization, rising vehicle ownership, and increasing demand for connected and intelligent vehicle solutions. The country’s growing middle class and focus on smart mobility support the adoption of advanced telematics systems. Strong domestic manufacturing capabilities and competitive pricing enhance market accessibility.

Starch Ethers Market Share

The starch ethers industry is primarily led by well-established companies, including:

- Emsland Food GmbH (Germany)

- Grain Processing Corporation (U.S.)

- Global Bio-chem Technology Group Company Limited (China)

- Ingredion (U.S.)

- Roquette Frères (France)

- ADM (U.S.)

- AGRANA Beteiligungs-AG (Austria)

- AVEBE (Netherlands)

- Cargill, Incorporated (U.S.)

- Tate & Lyle (U.K.)

- Shandong Dongbao Starch (China)

- Beneo (Germany)

- SPAC Starch Products (India)

- Visco Starch (India)

- Archer Daniels Midland Company (U.S.)

What are the Recent Developments in Global Starch Ethers Market?

- In April 2024, Ingredion Incorporated introduced NOVATION® Lumina 8300, a clean-label functional native starch derived from waxy rice. Engineered for food and beverage applications, this starch delivers enhanced texture, stability, and sensory performance—especially in plant-based, gluten-free, and delicately flavored products. Its smooth, creamy mouthfeel and low flavor and color impact make it ideal for white or lightly colored formulations. NOVATION® Lumina 8300 also boasts excellent freeze/thaw and shelf-life stability, aligning with consumer demand for natural, allergen-friendly ingredients that support clean-label claims

- In March 2024, Cargill deepened its presence in the Asia-Pacific food ingredients market by partnering with Starpro, Thailand’s leading food-grade tapioca starch producer. This strategic alliance focuses on expanding Cargill’s portfolio of starch ethers and modified tapioca starches, which are essential for enhancing viscosity, texture, and sensory performance in processed foods. The collaboration supports regional food manufacturers in meeting evolving consumer expectations—particularly in convenience and foodservice categories—by offering locally produced, high-quality starch solutions tailored to Asian culinary preferences

- In February 2024, Tate & Lyle PLC reaffirmed its strategic expansion in the starch ingredients sector by completing the acquisition of an 85% stake in Chaodee Modified Starch Co., Ltd. (CMS), a Thailand-based manufacturer specializing in tapioca starch ethers. This move significantly enhances Tate & Lyle’s ability to supply high-functionality starches for both food and industrial applications, particularly in the Asia-Pacific region. The acquisition supports the company’s long-term goal of offering clean-label, plant-based solutions with improved texture, stability, and sensory performance—especially in gluten-free and processed food categories

- In January 2024, Emsland Group launched EMWAXY® 2500, a next-generation potato-based starch ether boasting over 99% amylopectin content. Developed through traditional, non-GMO breeding, this high-performance ingredient is specifically designed for snack food applications, offering superior texture, crispiness, and expansion properties. Its unique molecular structure delivers enhanced viscosity, clarity, and shelf-life stability—making it ideal for baked, extruded, and fried snacks. EMWAXY® 2500 exemplifies Emsland’s commitment to clean-label innovation, catering to the growing demand for plant-based, allergen-free, and sustainable ingredients in modern food formulations

- In December 2023, Archer Daniels Midland (ADM) and BASF announced a collaboration to develop sustainable starch ether-based materials aimed at advancing the production of bio-based plastics. This joint effort targets the creation of eco-friendly packaging alternatives, leveraging ADM’s agricultural processing expertise and BASF’s chemical innovation to meet the growing global demand for biodegradable and renewable materials. The partnership reflects both companies’ commitment to circular economy principles and reducing reliance on fossil-based plastics in consumer and industrial applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Starch Ethers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Starch Ethers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Starch Ethers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.