Global Supplementary Cementitious Materials Market

Market Size in USD Billion

USD

25.19 Billion

USD

39.54 Billion

2024

2032

USD

25.19 Billion

USD

39.54 Billion

2024

2032

| 2025 - 2032 | |

| USD 25.19 Billion | |

| USD 39.54 Billion | |

| % | |

|

Supplementary Cementitious Materials Market Size

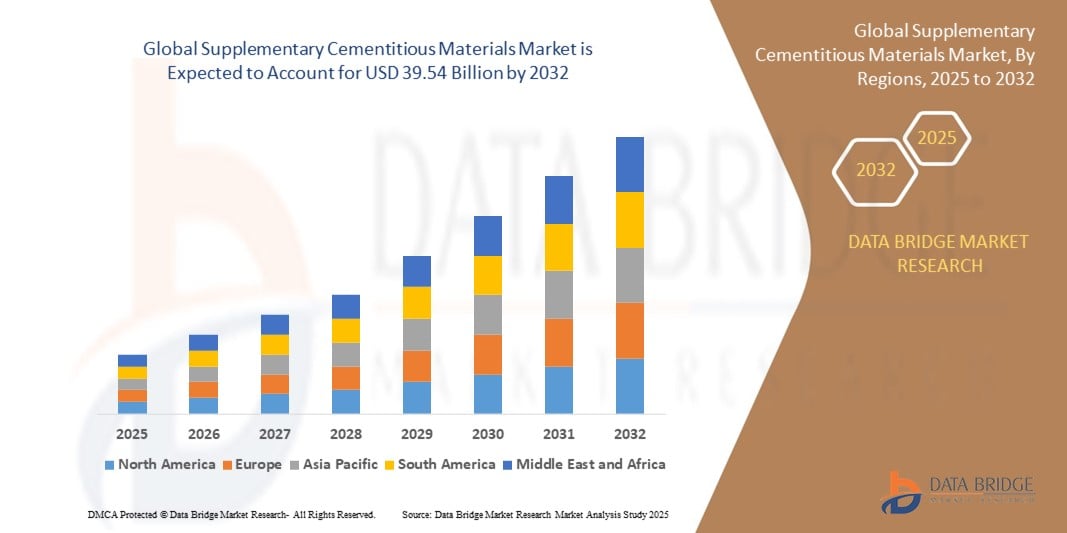

- The global supplementary cementitious materials market size was valued at USD 25.19 billion in 2024 and is expected to reach USD 39.54 billion by 2032, at a CAGR of 5.80% during the forecast period

- The market growth is largely fueled by the rising demand for sustainable and low-carbon construction materials, driven by global efforts to reduce greenhouse gas emissions and increase the use of industrial by-products in cement manufacturing. Government regulations and green building codes are pushing for alternatives to traditional clinker-based cement, propelling the adoption of supplementary cementitious materials across infrastructure and commercial sectors

- Furthermore, increasing investments in infrastructure development and urbanization, especially in emerging economies, are expanding the application scope of SCMs in concrete production. These converging factors are accelerating the integration of materials such as fly ash, slag cement, and calcinated clay in construction, thereby significantly boosting the market's growth

Supplementary Cementitious Materials Market Analysis

- Supplementary cementitious materials (SCMs) are industrial by-products or natural materials—such as fly ash, slag, silica fume, and calcinated clay—that are used to partially replace Portland cement in concrete mixtures, improving strength, durability, and sustainability. These materials help reduce cement-related CO₂ emissions while enhancing long-term concrete performance

- The growing emphasis on eco-efficient construction, combined with the availability of SCMs through industrial recycling, is driving their increased usage across residential, commercial, and infrastructure projects. Supportive environmental policies and advancements in blended cement technologies are further catalyzing market expansion

- North America dominated the supplementary cementitious materials market in 2024, due to increased infrastructure rehabilitation, growing adoption of sustainable construction practices, and government support for low-carbon building materials

- Asia-Pacific is expected to be the fastest growing region in the supplementary cementitious materials market during the forecast period due to rapid urbanization, government infrastructure investments, and increasing environmental consciousness in countries such as China, India, and Japan

- Fly ash segment dominated the market with a market share of 37% in 2024, due to its widespread availability as a by-product of coal-fired power plants and its proven effectiveness in enhancing concrete durability and workability. Fly ash offers pozzolanic properties that reduce permeability, improve long-term strength, and lower the carbon footprint of cement production, making it a preferred choice for sustainable construction projects across both public and private sectors. The segment’s growth is further bolstered by its cost-efficiency and compatibility with traditional cement mixes, encouraging adoption in both developed and developing economies

Report Scope and Supplementary Cementitious Materials Market Segmentation

|

Attributes |

Supplementary Cementitious Materials Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Supplementary Cementitious Materials Market Trends

“Increasing Construction Activities”

- A significant and accelerating trend in the supplementary cementitious materials (SCM) market is the surge in global construction activities, especially in rapidly urbanizing regions

- For instance, major companies such as LafargeHolcim, CEMEX, and Boral are expanding their SCM offerings to supply large-scale infrastructure and commercial projects across Asia-Pacific, North America, and Europe

- The push for sustainable and durable building materials is driving the adoption of SCMs such as fly ash, slag cement, and silica fume, which enhance concrete performance and reduce the carbon footprint of traditional cement

- Rapid urbanization, population growth, and increased government investment in infrastructure are fueling demand for high-quality and resilient construction materials

- Advances in concrete technology and the pursuit of green building certifications are further encouraging the use of SCMs as essential components in modern construction

- The demand for SCMs is growing rapidly as they offer benefits such as improved strength, durability, and reduced permeability, making them attractive for high-performance and long-lasting structures

Supplementary Cementitious Materials Market Dynamics

Driver

“Increasing Demand for High-performance Concrete”

- The rising need for high-performance concrete in infrastructure, industrial, and commercial construction is a major driver for the SCM market, as such concrete is essential for projects requiring superior strength, durability, and resistance to harsh conditions

- For instance, companies such as HeidelbergCement, Sika AG, and Tata Steel are investing heavily in research and development to create advanced SCM blends that significantly enhance concrete properties, enabling the construction of critical infrastructure such as bridges, tunnels, high-rise buildings, and marine structures that must withstand aggressive environments and heavy loads

- High-performance concrete formulations incorporating SCMs help reduce the carbon footprint of construction, improve workability, and extend the service life of structures, aligning with global sustainability and climate goals

- The trend toward building more resilient, energy-efficient, and sustainable infrastructure is making SCMs a preferred choice for engineers, architects, and builders worldwide who are seeking innovative solutions to meet evolving construction standards

- The expanding use of SCMs in precast concrete elements, ready-mix concrete, and specialty applications such as ultra-high-performance concrete further supports robust market growth, as these materials enable the creation of complex and durable structures with enhanced performance characteristics

Restraint/Challenge

“Increasing Emission of Fly Ash”

- The increasing emission of fly ash, a key byproduct used as an SCM, presents a significant challenge for the market, as environmental and regulatory concerns about fly ash generation from coal-fired power plants intensify

- For instance, while companies such as Charah Solutions and Innovative Ash Solutions are developing advanced processing technologies to utilize fly ash more efficiently in concrete production, the gradual phase-out of coal-based energy in several regions is leading to supply constraints, quality variability, and inconsistent availability of fly ash as an SCM

- Regulatory pressures aimed at reducing emissions from coal-fired plants are impacting the supply of fly ash and also raising concerns about the safe disposal and management of this byproduct, which can contain trace amounts of heavy metals and other contaminants

- The need to balance the environmental benefits of using SCMs in concrete with the challenges of sourcing high-quality fly ash is critical for the sustained growth of the market, particularly as the industry shifts toward more sustainable construction practices

- Overcoming this challenge will require greater innovation in alternative SCMs, such as ground granulated blast furnace slag and silica fume, as well as improved fly ash processing and beneficiation techniques to ensure consistent quality and supply

Supplementary Cementitious Materials Market Scope

The market is segmented on the basis of type and end users

- By Type

On the basis of type, the supplementary cementitious materials market is segmented into ferrous slag, fly ash, silica fume, slag cement, calcinated clay, gypsum, and limestone. The fly ash segment dominated the largest market revenue share 37% in 2024, primarily due to its widespread availability as a by-product of coal-fired power plants and its proven effectiveness in enhancing concrete durability and workability. Fly ash offers pozzolanic properties that reduce permeability, improve long-term strength, and lower the carbon footprint of cement production, making it a preferred choice for sustainable construction projects across both public and private sectors. The segment’s growth is further bolstered by its cost-efficiency and compatibility with traditional cement mixes, encouraging adoption in both developed and developing economies.

The calcinated clay segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by its strong potential as a low-carbon alternative amid tightening environmental regulations. Calcinated clay’s widespread raw material availability, particularly in tropical and subtropical regions, and its capacity to significantly reduce clinker content in blended cement contribute to its growing traction. In addition, its adaptability in diverse construction applications and increasing support from global climate initiatives make calcinated clay a key focus area for innovation and capacity expansion in the SCM industry.

- By End Users

On the basis of end users, the supplementary cementitious materials market is segmented into agriculture, residential, commercial, industrial, infrastructure, and others. The infrastructure segment held the largest market revenue share in 2024, driven by the high volume of concrete required for bridges, roads, highways, tunnels, and public transportation systems. SCMs such as slag cement and fly ash are widely used in infrastructure projects for their strength-enhancing, sulfate-resistant, and long-lasting properties, which are crucial for structures exposed to harsh environmental conditions. Government investments in large-scale infrastructure developments and the global push for green construction materials have further reinforced demand within this segment.

The industrial segment is expected to witness the fastest CAGR from 2025 to 2032, propelled by rising awareness around sustainable manufacturing practices and the growing use of SCMs in energy-intensive facilities. In industrial construction, SCMs play a vital role in achieving thermal resistance, reduced carbon emissions, and greater cost-efficiency in structural materials. Industries are increasingly adopting green certifications and environmental compliance programs, accelerating the incorporation of SCMs in new facilities, renovations, and expansions across sectors such as chemicals, power generation, and manufacturing.

Supplementary Cementitious Materials Market Regional Analysis

- North America dominated the supplementary cementitious materials market with the largest revenue share in 2024, driven by increased infrastructure rehabilitation, growing adoption of sustainable construction practices, and government support for low-carbon building materials

- The region’s strong presence of cement and concrete producers, along with environmental regulations promoting fly ash and slag usage, is accelerating market demand

- Favorable policies from the U.S. Environmental Protection Agency (EPA) and green building certifications are encouraging the use of SCMs in public infrastructure and commercial real estate projects

U.S. Supplementary Cementitious Materials Market Insight

The U.S. supplementary cementitious materials market captured the largest revenue share in 2024 within North America, supported by aging infrastructure, federal funding for sustainable public works, and increasing awareness of carbon reduction in cement production. Fly ash and slag cement are widely used in highway, bridge, and dam construction, with initiatives such as the Bipartisan Infrastructure Law spurring demand. In addition, the emphasis on achieving LEED and other green certifications is leading contractors and developers to incorporate SCMs into both new and retrofit projects.

Europe Supplementary Cementitious Materials Market Insight

The Europe supplementary cementitious materials market is projected to expand at a substantial CAGR throughout the forecast period, fueled by the European Union’s strong climate goals and regulations limiting CO₂ emissions in construction materials. EU directives and national legislation are mandating lower clinker usage and encouraging blended cements incorporating SCMs such as slag and calcinated clay. The rise in circular economy practices and the availability of industrial by-products are also supporting the region’s transition to greener construction.

U.K. Supplementary Cementitious Materials Market Insight

The U.K. market is expected to grow steadily during the forecast period, driven by the government’s Net Zero Strategy and increased demand for eco-efficient building materials in both public and private infrastructure. The use of fly ash and ground granulated blast furnace slag (GGBFS) is gaining traction, especially in large infrastructure and housing projects. Local regulations promoting low-embodied carbon and the emphasis on sustainable urban planning are accelerating adoption of SCMs across residential and commercial segments.

Germany Supplementary Cementitious Materials Market Insight

The Germany market is poised to grow significantly, supported by strong environmental legislation, industrial innovation, and demand for low-carbon concrete solutions. German manufacturers are increasingly investing in alternative binder technologies and SCM integration to meet carbon reduction targets. The push for green infrastructure development, paired with a preference for high-performance construction materials, is positioning SCMs as essential components in both public and industrial building segments.

Asia-Pacific Supplementary Cementitious Materials Market Insight

The Asia-Pacific supplementary cementitious materials market is projected to grow at the fastest CAGR from 2025 to 2032, driven by rapid urbanization, government infrastructure investments, and increasing environmental consciousness in countries such as China, India, and Japan. The region benefits from abundant availability of raw materials such as fly ash and slag due to heavy industrial activity, while rising cement consumption in construction is encouraging the integration of SCMs to improve performance and sustainability.

Japan Supplementary Cementitious Materials Market Insight

Japan’s market is experiencing steady growth due to its advanced construction practices, aging infrastructure requiring sustainable upgrades, and proactive government efforts to reduce cement-related emissions. The country's focus on earthquake-resilient and long-lasting concrete structures has created demand for durable SCM-integrated mixes, particularly in urban redevelopment and public infrastructure projects.

China Supplementary Cementitious Materials Market Insight

China accounted for the largest revenue share in the Asia-Pacific SCM market in 2024, driven by massive urban development, industrial scale cement production, and government mandates encouraging low-carbon construction. Fly ash and slag cement are widely utilized in large-scale infrastructure and housing projects, while China's robust domestic production capacity and commitment to green building standards are further propelling SCM usage.

Supplementary Cementitious Materials Market Share

The supplementary cementitious materials industry is primarily led by well-established companies, including:

- CEMEX S.A.B. de C.V. (Mexico)

- Ferroglobe (U.S.)

- LAFARGE (France)

- Charah Solutions, Inc. (U.S.)

- HEIDELBERGCEMENT AG (Germany)

- Bharathi Cement Corporation Private Limited (India)

- CR Minerals Company, LLC. (U.S.)

- Boral (Australia)

- Sika AG (Switzerland)

- ArcelorMittal SA (Luxembourg)

- BASF (Germany)

- CRH Canada Group Inc. (Canada)

- Tata Steel (India)

- Adelaide Brighton Cement Ltd. (Australia)

- Elkem ASA (Norway)

- FLSmidth (Denmark)

- Argos USA LLC (U.S.)

- 3M (U.S.)

Latest Developments in Global Supplementary Cementitious Materials Market

- In September 2022, Innovative Ash Solutions, a joint venture between Levenseat and Organic Innovative Solutions, announced plans to build a 54,000 tons/year APCR-based SCM plant in the U.K., with two more planned. This initiative aims to replace pulverized fly ash (PFA), boosting SCM supply and supporting the shift toward low-carbon, sustainable construction materials

- In March 2022, Lafarge France allocated 120 million euros to revamp the Martres-Tolosane cement facility, bolstering low-carbon cement output. Operational since February 2022, the investment enhances sustainability and production capacity

- In February 2022, Purebase Corporation forged a strategic alliance with a major vertically integrated materials firm to cultivate a novel supplementary cementitious materials (SCM) market in California, diversifying its resource portfolio

- In December 2021, LafargeHolcim's US division received its inaugural barge delivery of power plant coal ash, marking the recycling and reclamation of 6 million tons for cement production, underscoring commitment to sustainable practices and resource efficiency

- In November 2020, Cemex partnered with Carbon Upcycling Technologies, aiming to optimize the utilization of by-products such as fly ash and slag for manufacturing low CO2 concrete, advancing eco-friendly solutions and reducing environmental impact

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Supplementary Cementitious Materials Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Supplementary Cementitious Materials Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Supplementary Cementitious Materials Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.