Global Surgical Equipment Market

Market Size in USD Billion

USD

22.53 Billion

USD

43.91 Billion

2025

2033

USD

22.53 Billion

USD

43.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 22.53 Billion | |

| USD 43.91 Billion | |

| % | |

|

What is the Surgical Equipment Market Size and Overview?

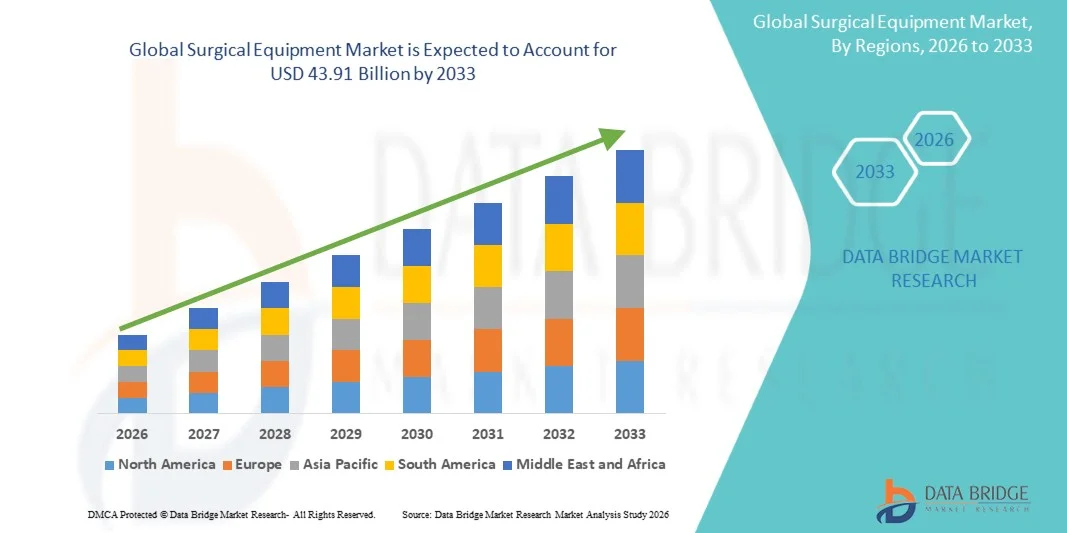

As per Data Bridge Market Research Analysis the global surgical equipment market was valued at USD 22.53 billion in 2025 and is projected to reach USD 43.91 billion by 2033, growing at a CAGR of 8.70% from 2026 to 2033. The market is is witnessing steady expansion driven by the rising volume of surgical procedures worldwide, increasing prevalence of chronic diseases, and continuous advancements in minimally invasive and robotic-assisted surgical technologies. Growing healthcare infrastructure development, particularly in emerging economies, is further supporting market adoption across hospitals and ambulatory surgical centers.

The increasing demand for precision-based and minimally invasive surgeries, coupled with the growing aging population, is significantly boosting the use of advanced surgical instruments and devices. In addition, stricter regulatory standards for surgical safety and sterilization are encouraging healthcare providers to upgrade to high-quality, technologically advanced equipment. Integration of robotics, AI-assisted surgical systems, and enhanced imaging tools is further transforming operating rooms, improving outcomes, reducing recovery time, and enhancing overall procedural efficiency.

Key Market Trends & Insights

- North America dominated the global surgical equipment market with the largest revenue share of 38.92% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, and strong adoption of innovative medical technologies.

- The Handheld Surgical Devices segment led the market with a 44.36% share in 2025, driven by their widespread use across nearly all surgical procedures and their essential role in precision cutting, grasping, and dissecting tissues.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.5% from 2026 to 2033, fueled by expanding healthcare access, rising medical tourism, and increasing investments in hospital infrastructure in China, India, and Southeast Asia.

- Electrosurgical Devices are the fastest-growing product type, projected to register a CAGR of 8.2%, reflecting the surge in demand for adoption of advanced energy-based surgical techniques that improve precision and reduce blood loss.

- The Disposable Surgical Equipment segment dominated the category with a 57.41% revenue share in 2025, led by rising emphasis on infection prevention, strict hospital hygiene protocols, and increasing awareness of hospital-acquired infections.

- Orthopaedic Surgery accounted for 23.68% of the market, preferred by the rising prevalence of musculoskeletal disorders, sports injuries, and age-related bone conditions.

- The Laparoscopy segment is the fastest-growing application category, with a CAGR of 8.0%, driven by the rising preference for minimally invasive surgical techniques across multiple specialties.

Market Size & Forecast

- Global Market Value (2025): USD 22.53 Billion

- Expected Market Value (2033): USD 43.91 Billion

- Forecast CAGR (2026–2033): 8.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Surgical Equipment Market Segmentation

|

Attributes |

Surgical Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

What is the Key Trend in the Surgical Equipment Market?

Trend: Growth in Minimally Invasive and Robotic-Assisted Surgery

Hospitals are increasingly adopting minimally invasive and robotic-assisted surgical systems to improve precision, reduce patient trauma, and shorten recovery times across complex procedures. Integration of high-definition imaging, advanced endoscopic tools, and AI-guided surgical navigation is enhancing procedural accuracy and surgeon control in real time. Surgical training centers and hospitals are leveraging simulation-based platforms to upskill surgeons and standardize complex procedures, while digital operating rooms create connected environments that improve workflow efficiency and intraoperative decision-making. For instance, adoption of robotic surgery platforms in urology and gynecology is expanding rapidly across tertiary care hospitals.

Global Surgical Equipment Market Dynamics

Key Market Driver: Rising Surgical Procedure Volumes and Aging Population

The increasing global burden of chronic diseases, combined with a rapidly aging population, is significantly driving demand for surgical interventions across cardiovascular, orthopedic, and oncological specialties. Expanding access to healthcare services and improved diagnostic capabilities are resulting in higher rates of elective and emergency surgeries worldwide. Hospitals and surgical centers are scaling up infrastructure and adopting advanced surgical tools to manage growing patient inflow efficiently and safely. For instance, rising volumes of joint replacement and cardiac surgeries in aging populations are accelerating equipment adoption in developed healthcare systems.

Key Restraint/Challenge: High Cost of Advanced Surgical Systems and Maintenance

A major restraint in the global surgical equipment market is the high cost associated with advanced surgical systems, including robotic platforms, imaging-integrated operating rooms, and precision surgical instruments. Significant capital investment is required not only for procurement but also for training, maintenance, and periodic upgrades, which limits adoption in resource-constrained healthcare settings. Smaller hospitals and clinics often face challenges in justifying return on investment despite clinical benefits, slowing widespread penetration. For instance, limited adoption of robotic surgery systems in low- and middle-income countries reflects cost-related barriers to implementation.

Key Market Opportunity: Expansion of Outpatient and Ambulatory Surgical Centers

The growing shift toward outpatient care and ambulatory surgical centers is creating substantial opportunities for cost-effective, portable, and efficient surgical equipment solutions. These facilities focus on same-day procedures, reducing hospital burden while improving patient convenience and lowering healthcare costs. Manufacturers are increasingly developing compact, modular, and energy-efficient surgical systems tailored for such settings. For instance, rising establishment of ambulatory surgery centers for cataract and endoscopy procedures is driving demand for specialized surgical instruments.

Global Surgical Equipment Market Scope

The surgical equipment market is segmented on the basis of product, category, application, and end user.

- By Product

On the basis of product, the global surgical equipment market is segmented into surgical sutures and staplers, handheld surgical devices, and electrosurgical devices. The Handheld Surgical Devices segment dominated the market with a 44.36% share in 2025, owing to their widespread use across nearly all surgical procedures and their essential role in precision cutting, grasping, and dissecting tissues. These instruments are fundamental in general surgery, orthopedics, cardiovascular procedures, and minimally invasive operations. Hospitals and surgical centers prefer handheld devices due to their reliability, reusability options, and compatibility with a wide range of surgical specialties. Continuous advancements in ergonomic design and material quality are further enhancing their performance and surgeon comfort. Growing surgical volumes globally are sustaining consistent demand for these tools. Their versatility across routine and complex procedures reinforces their dominant position.

The Electrosurgical Devices segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by increasing adoption of advanced energy-based surgical techniques that improve precision and reduce blood loss. These devices are widely used in minimally invasive and laparoscopic surgeries, where controlled tissue cutting and coagulation are critical. Technological advancements such as bipolar and ultrasonic energy systems are improving safety and procedural efficiency. Rising demand for outpatient surgeries and faster recovery procedures is further accelerating adoption. Hospitals are increasingly integrating electrosurgical units into modern operating rooms for enhanced surgical outcomes. For instance, growing use of advanced cautery systems in oncology and gynecology surgeries is supporting rapid expansion.

- By Category

On the basis of category, the global surgical equipment market is segmented into reusable surgical equipment and disposable surgical equipment. The Disposable Surgical Equipment segment dominated the market with a 57.41% share in 2025, owing to rising emphasis on infection prevention, strict hospital hygiene protocols, and increasing awareness of hospital-acquired infections. These products are widely used in high-volume surgical environments where sterility and patient safety are critical. Hospitals prefer disposable instruments to reduce cross-contamination risks and eliminate reprocessing costs. Expanding surgical volumes and regulatory guidelines on sterilization are further strengthening demand. Manufacturers are continuously innovating cost-effective and high-quality single-use devices. For instance, growing use of disposable sutures, gloves, and drapes in operating rooms supports strong segment dominance.

The Reusable Surgical Equipment segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing focus on cost efficiency and sustainability in healthcare systems. These instruments offer long-term economic advantages, especially in high-frequency surgical settings. Technological improvements in sterilization methods and durable material design are enhancing product lifespan and safety. Hospitals in developed regions are increasingly adopting hybrid models combining reusable and disposable tools. Growing environmental concerns regarding medical waste are also supporting demand. For instance, rising adoption of reusable laparoscopic instruments in large tertiary hospitals reflects this growth trend.

- By Application

On the basis of application, the global surgical equipment market is segmented into neurosurgery, plastic and reconstructive surgeries, wound closure, urology, obstetrics and gynaecology, thoracic surgery, microvascular surgery, cardiovascular surgery, orthopaedic surgery, laparoscopy, and others. The Orthopaedic Surgery segment dominated the market with a 23.68% share in 2025, owing to the rising prevalence of musculoskeletal disorders, sports injuries, and age-related bone conditions. Increasing demand for joint replacement, fracture fixation, and spinal surgeries is significantly driving equipment usage. Advanced surgical tools and implants are widely used in orthopedic procedures for improved precision and faster recovery. Hospitals are increasingly investing in specialized orthopedic surgical suites. For instance, growing volumes of knee and hip replacement surgeries in aging populations support strong segment dominance. Continuous innovation in orthopedic instruments further strengthens adoption.

The Laparoscopy segment is projected to register the fastest growth at a CAGR of 8.0% from 2026 to 2033, driven by rising preference for minimally invasive surgical techniques across multiple specialties. Laparoscopic procedures reduce patient recovery time, hospital stays, and post-operative complications. Increasing adoption in gastrointestinal, gynecological, and bariatric surgeries is fueling demand. Technological advancements in imaging systems and surgical instruments are enhancing procedural accuracy. Surgeons are increasingly trained in minimally invasive techniques, supporting broader adoption. For instance, rising use of laparoscopic equipment in obesity and appendectomy surgeries is accelerating segment growth.

- By End User

On the basis of end user, the global surgical equipment market is segmented into hospitals, ambulatory surgical centers, and others. The Hospitals segment dominated the market with a 52.18% share in 2025, owing to high patient inflow, availability of advanced surgical infrastructure, and capability to handle complex and high-risk procedures. Hospitals are the primary centers for emergency surgeries, specialized treatments, and multidisciplinary surgical care. Continuous investments in operating room modernization and advanced surgical technologies are further strengthening demand. Skilled surgical teams and access to comprehensive post-operative care support their dominance. For instance, large tertiary care hospitals performing high volumes of cardiovascular and orthopedic surgeries drive strong equipment utilization. Their role as referral centers ensures sustained market leadership.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by the increasing shift toward outpatient and same-day surgical procedures. These centers offer cost-effective care, shorter hospital stays, and faster patient turnaround. Advancements in minimally invasive surgical techniques are enabling more procedures to be performed in outpatient settings. Growing patient preference for convenience and reduced healthcare costs is accelerating adoption. Healthcare systems are increasingly supporting ASCs to reduce hospital burden. For instance, rising number of cataract and endoscopy procedures performed in ASCs reflects strong growth momentum.

Global Surgical Equipment Market Regional Analysis

North America dominated the global surgical equipment market with the largest revenue share of 38.92% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, and strong adoption of innovative medical technologies. The region also benefits from the presence of leading medical device manufacturers, favorable reimbursement frameworks, and widespread use of robotic-assisted and minimally invasive surgical technologies across hospitals. Increasing prevalence of chronic diseases and growing demand for complex surgical interventions continue to strengthen North America’s leadership position in the global market.

U.S. Surgical Equipment Market Insight

The U.S. surgical equipment market is witnessing strong growth due to rising surgical procedure volumes, rapid adoption of robotic-assisted surgery systems, and increasing investments in advanced healthcare infrastructure. The country’s well-established hospital network, strong presence of leading medical device manufacturers, and early adoption of minimally invasive surgical technologies are driving demand across multiple specialties. In addition, growing focus on improving surgical outcomes, reducing hospital stay durations, and enhancing procedural precision is accelerating equipment adoption across hospitals, ambulatory surgical centers, and specialty clinics.

Europe Surgical Equipment Market Insight

The Europe surgical equipment market remains a major contributor to global revenue, driven by strong public healthcare systems, increasing adoption of minimally invasive procedures, and rising demand for advanced surgical technologies. The widespread use of robotic surgery platforms, electrosurgical devices, and high-precision instruments is supporting market expansion across the region. Increasing healthcare expenditure, aging population, and strict regulatory standards for patient safety and infection control continue to enhance the adoption of modern surgical equipment throughout Europe.

U.K. Surgical Equipment Market Insight

The U.K. surgical equipment market is experiencing steady growth, supported by rising demand for advanced surgical procedures, increasing adoption of minimally invasive techniques, and ongoing healthcare modernization initiatives. Investments in robotic surgery systems, digital operating rooms, and precision surgical tools are improving efficiency and clinical outcomes. Furthermore, efforts to reduce surgical waiting lists and expand access to high-quality care are contributing to growing equipment utilization across public and private healthcare facilities.

Germany Surgical Equipment Market Insight

The Germany surgical equipment market is expanding steadily due to its strong hospital infrastructure, advanced medical research ecosystem, and high adoption of innovative surgical technologies. Hospitals and surgical centers are increasingly utilizing robotic-assisted systems, electrosurgical devices, and precision instruments for complex and high-risk procedures. Continuous technological innovation, strong healthcare funding, and emphasis on surgical quality and safety standards are further driving market growth in Germany.

Asia-Pacific Surgical Equipment Market Insight

The Asia-Pacific surgical equipment market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising surgical volumes, and increasing investments in hospital modernization across countries such as China, India, and Japan. Growing awareness of advanced surgical techniques, rising medical tourism, and improving access to healthcare services are supporting regional market expansion. In addition, increasing adoption of cost-effective minimally invasive surgical solutions is accelerating demand across both public and private healthcare systems.

Japan Surgical Equipment Market Insight

The Japan surgical equipment market is witnessing consistent growth due to a rapidly aging population, high prevalence of chronic diseases, and strong focus on advanced medical technologies. Hospitals and research institutions are increasingly adopting robotic-assisted surgical systems, precision instruments, and minimally invasive techniques to enhance surgical accuracy and patient outcomes. Moreover, Japan’s emphasis on innovation, safety, and high-quality healthcare delivery is further contributing to steady market expansion.

China Surgical Equipment Market Insight

The China surgical equipment market is growing rapidly, driven by expanding healthcare infrastructure, rising surgical procedure volumes, and increasing government investment in hospital development and medical technology adoption. Growing demand for advanced surgical interventions, coupled with improving access to healthcare services, is significantly boosting market expansion. In addition, increasing adoption of robotic surgery systems, minimally invasive techniques, and domestic medical device manufacturing capabilities are positioning China as one of the fastest-growing markets globally.

Which are the Top Companies in Global Surgical Equipment Market?

The Surgical Equipment industry is primarily led by well-established companies, including:

- Johnson & Johnson Services, Inc. (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- Braun SE (Germany)

- BD (U.S.)

- Zimmer Biomet (U.S.)

- Smith & Nephew (U.K.)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Olympus Corporation (Japan)

- Alcon Inc. (Switzerland)

- Teleflex Incorporated (U.S.)

- CONMED Corporation (U.S.)

- Getinge AB (Sweden)

- Integra LifeSciences Holdings Corporation (U.S.)

- Hologic, Inc. (U.S.)

- Dentsply Sirona Inc. (U.S.)

- Baxter (U.S.)

- Siemens Healthineers AG (Germany)

Latest Developments in Global Surgical Equipment Market

- In March 2026, Medtronic received expanded FDA clearance for its Stealth AXiS surgical navigation system, enabling its use in cranial and ENT procedures beyond spine applications. The system integrates AI-based imaging, navigation, and advanced visualization tools to improve surgical precision and safety in complex procedures. This development strengthens Medtronic’s position in digital surgery and image-guided operating room technologies. It also reflects the growing shift toward AI-powered surgical workflows and real-time decision support systems in hospitals. The expansion is expected to accelerate adoption of advanced navigation platforms in neurosurgery and ENT specialties

- In September 2025, Intuitive Surgical expanded the adoption of its next-generation da Vinci 5 robotic surgery system following regulatory clearance. The platform introduces improved imaging, enhanced computing power, and refined surgeon feedback systems for complex procedures. This advancement significantly improves precision and control in minimally invasive surgeries. It highlights the continued dominance of robotic-assisted systems in modern operating rooms. The rollout is expected to increase adoption across multiple surgical specialties globally

- In July 2025, Zimmer Biomet completed its acquisition of Monogram Technologies to strengthen its robotic-assisted surgical portfolio in orthopedic care. Monogram’s semi-autonomous knee surgery technology enhances Zimmer’s capabilities in precision-based joint replacement procedures. The acquisition reflects increasing consolidation in the surgical robotics market, driven by demand for automation in orthopedic surgeries. It also supports the company’s strategy to expand next-generation digital and robotic surgery solutions. This move is expected to enhance surgical accuracy and improve patient recovery outcomes in joint reconstruction procedures

- In January 2025, Stryker announced its acquisition of Inari Medical to expand its minimally invasive surgical and vascular intervention portfolio. The deal strengthens Stryker’s position in catheter-based surgical technologies used to treat venous diseases. It reflects rising demand for less invasive surgical procedures that reduce recovery time and hospital stays. The acquisition supports broader industry consolidation in high-growth surgical device segments. It also enhances Stryker’s presence in advanced interventional and specialty surgical markets

- In February 2024, the global minimally invasive surgical equipment segment continued strong growth driven by increasing adoption of laparoscopic and energy-based surgical devices. Hospitals are rapidly shifting toward procedures that reduce patient trauma, recovery time, and post-operative complications. Manufacturers are focusing on advanced instrumentation, including AI-assisted and high-precision surgical tools. This trend is reshaping operating room workflows and accelerating modernization of surgical infrastructure. It is also driving higher demand for integrated surgical systems across healthcare facilities worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.