Global Synthetic Tissue Engineering Market

Market Size in USD Billion

USD

1.47 Billion

USD

4.22 Billion

2024

2032

USD

1.47 Billion

USD

4.22 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 1.47 Billion |

Market Size (Forecast Year) |

USD 4.22 Billion |

CAGR |

% |

Major Markets Players |

|

Synthetic Tissue Engineering Market Size

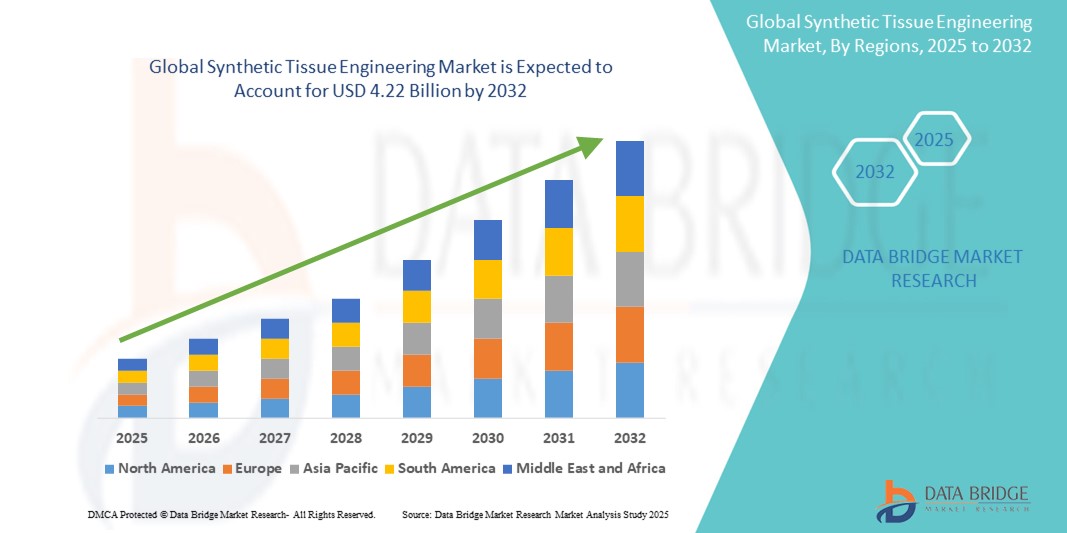

- The global synthetic tissue engineering market size was valued at USD 1.47 billion in 2024 and is expected to reach USD 4.22 billion by 2032, at a CAGR of 14.10% during the forecast period

- The market growth is primarily driven by increasing demand for regenerative medicine and advanced therapies, particularly in orthopedic, dental, and skin tissue reconstruction, where synthetic materials offer scalable, customizable, and durable solutions

- Moreover, ongoing advancements in biomaterials, 3D bioprinting, and scaffold technologies are strengthening the role of synthetic constructs as reliable alternatives to biologically derived tissues. These innovations are rapidly accelerating the adoption of synthetic tissue engineering products, significantly contributing to market expansion

Synthetic Tissue Engineering Market Analysis

- Synthetic tissue engineering, which leverages engineered materials such as polymers, ceramics, and composites to repair or regenerate human tissues, is becoming increasingly essential in regenerative medicine and biomedical applications due to its scalability, consistent quality, and ability to overcome limitations of biologically derived grafts

- The accelerating demand for synthetic tissue engineering solutions is primarily fueled by rising cases of trauma, orthopedic disorders, and chronic wounds, as well as advancements in biomaterials, 3D printing, and nanotechnology that enable more precise and effective tissue reconstruction

- North America dominated the synthetic tissue engineering market with the largest revenue share of 40.1% in 2024, driven by a strong R&D ecosystem, robust regulatory support for innovative therapies, and significant adoption of synthetic scaffolds across orthopedic, dental, and reconstructive procedures in the U.S., supported by academic institutions and biotech leaders

- Asia-Pacific is expected to be the fastest growing region in the synthetic tissue engineering market during the forecast period due to rising healthcare expenditure, expanding access to advanced treatments, and growing investments in biomedical research and infrastructure

- The orthopedic segment dominated the synthetic tissue engineering market with a market share of 59.4% in 2024, supported by increasing incidence of musculoskeletal injuries, high demand for bone graft substitutes, and the proven clinical utility of synthetic scaffolds in joint and cartilage repair

Report Scope and Synthetic Tissue Engineering Market Segmentation

|

Attributes |

Synthetic Tissue Engineering Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Synthetic Tissue Engineering Market Trends

“Advancements in 3D Bioprinting and Synthetic Scaffold Innovation”

- A significant and accelerating trend in the global synthetic tissue engineering market is the integration of advanced 3D bioprinting technologies with synthetic biomaterials such as polymers, ceramics, and composites. This convergence is enabling the development of highly customizable and structurally precise tissue scaffolds for regenerative applications

- For instance, companies such as CELLINK and Aspect Biosystems are pioneering bioprinting platforms that utilize synthetic hydrogels and biodegradable polymers to fabricate functional tissue constructs for skin, cartilage, and vascular grafts. Similarly, Nanofiber Solutions is creating electrospun nanofiber scaffolds that mimic the natural extracellular matrix, supporting enhanced cell attachment and tissue regeneration

- Innovations in synthetic scaffolds now include smart, stimuli-responsive materials that can react to environmental changes such as pH, temperature, or mechanical load. These materials can release bioactive agents or adjust stiffness dynamically, improving healing outcomes. For instance, injectable synthetic scaffolds with controlled drug-release profiles are being explored for chronic wound and orthopedic treatments

- The seamless integration of these synthetic constructs into tissue engineering protocols enables researchers and clinicians to standardize and scale treatments, while also customizing implants based on patient-specific anatomy or pathology. This is especially beneficial in orthopedics and maxillofacial surgery

- This trend toward more intelligent, biofunctional, and clinically adaptable synthetic materials is reshaping the landscape of regenerative medicine. Consequently, companies and research institutes are increasingly focused on developing next-generation synthetic platforms that deliver both structural support and biological performance

- The demand for synthetic scaffolds that support precision medicine, reduce reliance on donor tissues, and enable scalable production is growing rapidly across both developed and emerging markets, as healthcare systems prioritize innovative and cost-effective tissue repair solutions

Synthetic Tissue Engineering Market Dynamics

Driver

“Rising Burden of Chronic Diseases and Demand for Regenerative Therapies”

- The growing prevalence of chronic conditions such as osteoarthritis, cardiovascular disease, diabetic ulcers, and traumatic injuries is a major driver for the increasing adoption of synthetic tissue engineering solutions worldwide

- For instance, according to WHO, musculoskeletal conditions impact over 1.7 billion people globally, leading to rising demand for bone, cartilage, and joint repair products. Synthetic scaffolds provide a reliable and reproducible alternative to biologic grafts, reducing complications and improving recovery times

- As traditional biologically sourced grafts face limitations including supply shortages, immune rejection, and donor site morbidity, synthetic alternatives offer significant advantages in scalability, safety, and material customization

- Furthermore, increased funding in regenerative medicine, alongside academic-industry collaborations, is accelerating the development and clinical adoption of synthetic scaffold technologies. Government programs supporting biomaterial R&D and faster approval frameworks for advanced therapies are further boosting market expansion

- The flexibility of synthetic materials to be engineered for specific applications orthopedic, dental, cardiovascular, and wound care makes them a critical solution for personalized and minimally invasive treatments, aligning with the global trend toward precision medicine

Restraint/Challenge

“Biocompatibility Concerns and Complex Regulatory Pathways”

- A notable challenge in the synthetic tissue engineering market is the concern over biocompatibility and long-term clinical safety of synthetic scaffold materials. While synthetic polymers and composites offer high structural integrity and controlled degradation, they may lack the biological cues needed for seamless tissue integration without surface modification

- For instance, synthetic implants may trigger localized inflammation or fibrosis if not properly engineered or sterilized, raising concerns among clinicians and regulators. The need to enhance biofunctionality through surface coatings or incorporation of growth factors adds complexity and cost to development

- In addition, regulatory hurdles present a significant barrier to commercialization, especially in regions such as the U.S. and Europe where strict clinical validation is required. Navigating FDA or EMA approval processes can be lengthy and resource-intensive, particularly for startups or small-scale innovators

- Cost is another limiting factor while synthetic scaffolds offer long-term value, advanced formulations with nanotechnology or embedded biologics can be expensive to produce, limiting accessibility in cost-sensitive healthcare systems

- Overcoming these challenges through interdisciplinary R&D, improved biomaterial design, strategic partnerships, and supportive regulatory frameworks will be essential to fully realize the potential of synthetic tissue engineering in clinical practice

Synthetic Tissue Engineering Market Scope

The market is segmented on the basis of material type, product type, application, and end user.

- By Material Type

On the basis of material type, the synthetic tissue engineering market is segmented into polymeric materials, ceramic materials, composite materials, and nanomaterials. The polymeric materials segment held the largest market revenue share in 2024 due to their superior biocompatibility, versatility, and tunable degradation rates. Polymers such as PLA, PLGA, and PCL are extensively used for developing scaffolds in bone, cartilage, and soft tissue engineering due to their ease of fabrication and favorable mechanical properties.

The nanomaterials segment is anticipated to witness the fastest growth from 2025 to 2032. This growth is driven by their ability to mimic the native extracellular matrix at the nanoscale, supporting enhanced cell adhesion, proliferation, and differentiation. Nanostructured synthetic materials are increasingly used in advanced wound healing, neural regeneration, and controlled drug delivery applications, offering novel opportunities for therapeutic innovation.

- By Product Type

On the basis of product type, the synthetic tissue engineering market is segmented into synthetic scaffolds, synthetic skin substitutes, synthetic grafts, hydrogels, and others. The synthetic scaffolds segment dominated the market in 2024, supported by their widespread use in bone and cartilage repair, as well as their availability in customizable formats for tissue-specific applications. These scaffolds are preferred due to their structural integrity, scalability, and ability to be tailored for biomechanical performance.

The hydrogels segment is expected to grow at the highest CAGR from 2025 to 2032. Synthetic hydrogels are gaining traction for soft tissue applications, including wound healing, ophthalmology, and drug delivery, due to their high water content, flexibility, and capacity for incorporating bioactive agents.

- By Application

On the basis of application, the synthetic tissue engineering market is segmented into orthopedics, musculoskeletal, skin & wound care, cardiovascular, neurology, dental, urology, and others. The orthopedics segment accounted for the largest share of 59.4% in 2024, driven by a rising number of orthopedic injuries, degenerative bone disorders, and the increasing adoption of synthetic bone graft substitutes. These applications benefit significantly from synthetic materials that provide strength, biocompatibility, and controlled degradation.

The skin & wound care segment is projected to experience the fastest growth during the forecast period. The demand is rising due to a growing aging population, diabetic wound cases, and burn injuries, where synthetic skin substitutes and hydrogels offer effective healing and infection control.

- By End User

On the basis of end user, the synthetic tissue engineering market is segmented into hospitals & clinics, ambulatory surgical centers, specialty clinics, and academic & research institutes. The hospitals & clinics segment led the market in 2024 due to the high volume of surgical procedures and wide adoption of synthetic tissue engineering products in reconstructive and orthopedic interventions. The availability of advanced infrastructure and trained professionals further supports dominance in this segment.

The academic & research institutes segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing R&D activities, government funding, and the development of novel synthetic biomaterials. Collaborations between academic institutions and biotechnology firms are accelerating innovation and early-stage clinical testing in tissue engineering.

Synthetic Tissue Engineering Market Regional Analysis

- North America dominated the synthetic tissue engineering market with the largest revenue share of 40.1% in 2024, driven by a strong R&D ecosystem, robust regulatory support for innovative therapies, and significant adoption of synthetic scaffolds across orthopedic, dental, and reconstructive procedures in the U.S., supported by academic institutions and biotech leaders

- The U.S., in particular, leads the regional growth with high clinical demand for orthopedic, dental, and cardiovascular applications, as well as the presence of major biotechnology firms and academic research institutions focused on tissue engineering innovation

- The region's leadership is further supported by favorable regulatory policies, increasing surgical procedures involving synthetic scaffolds, and rising investments in biomaterial R&D, positioning synthetic tissue engineering as a critical component of modern therapeutic strategies across hospitals and specialty clinics

U.S. Synthetic Tissue Engineering Market Insight

The U.S. synthetic tissue engineering market captured the largest revenue share of 82% in 2024 within North America, fueled by strong research funding, early clinical adoption, and a robust ecosystem of biotechnology and medical device companies. Demand is driven by increasing orthopedic surgeries, dental reconstructions, and cardiovascular procedures where synthetic scaffolds are preferred for their reproducibility and safety. The presence of leading academic research institutions and favorable FDA pathways for advanced therapies continues to propel innovation. Moreover, the growing integration of 3D bioprinting and synthetic biomaterials into regenerative treatments is significantly contributing to market expansion.

Europe Synthetic Tissue Engineering Market Insight

The Europe synthetic tissue engineering market is projected to expand at a substantial CAGR throughout the forecast period, supported by regulatory encouragement of advanced therapies and rising demand for tissue substitutes in orthopedic and reconstructive surgeries. The region’s aging population, combined with healthcare digitization and clinical focus on bioengineered solutions, is fostering the adoption of synthetic scaffolds. Countries such as Germany, the U.K., and France are seeing strong growth in academic-industry collaborations and clinical trials. Synthetic tissue products are increasingly used in both public and private healthcare settings, especially for wound care and dental restoration applications.

U.K. Synthetic Tissue Engineering Market Insight

The U.K. synthetic tissue engineering market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by an increasing number of musculoskeletal conditions and the NHS’s growing interest in regenerative solutions. The country’s strong university research network and biotech industry contribute to advancing synthetic biomaterials for clinical use. Government support for life sciences innovation and a focus on reducing transplant wait times further encourage adoption of off-the-shelf synthetic grafts and scaffolds for surgical use across hospitals and specialist centers.

Germany Synthetic Tissue Engineering Market Insight

The Germany synthetic tissue engineering market is expected to expand at a considerable CAGR during the forecast period, fueled by growing investments in biomedical engineering and the country’s reputation for innovation in healthcare technologies. A strong industrial base and academic partnerships support advancements in synthetic polymers and scaffold manufacturing. Increasing demand for sustainable, lab-engineered solutions in orthopedics, dentistry, and reconstructive medicine aligned with stringent quality and biocompatibility standards—positions Germany as a key driver of synthetic tissue engineering in Europe.

Asia-Pacific Synthetic Tissue Engineering Market Insight

The Asia-Pacific synthetic tissue engineering market is poised to grow at the fastest CAGR of 16.1% during the forecast period of 2025 to 2032, driven by expanding healthcare access, rising healthcare investments, and technological innovation in countries such as China, Japan, South Korea, and India. The region is benefiting from a rapidly aging population, rising rates of trauma and chronic disease, and government support for regenerative medicine. Local manufacturing capabilities and lower production costs are enhancing affordability, further broadening the adoption of synthetic scaffolds across clinical settings.

Japan Synthetic Tissue Engineering Market Insight

The Japan synthetic tissue engineering market is gaining momentum due to its leadership in biotechnology, a tech-savvy population, and demand for minimally invasive regenerative solutions. With a growing elderly demographic and a high prevalence of orthopedic and degenerative conditions, Japan is investing heavily in synthetic grafts and 3D bioprinting. The country’s focus on smart healthcare infrastructure and its strong domestic R&D sector are driving clinical and commercial deployment of synthetic tissue solutions, especially in orthopedics and dental care.

India Synthetic Tissue Engineering Market Insight

The India synthetic tissue engineering market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to its large and rapidly urbanizing population, rising middle-class income, and increased investment in healthcare infrastructure. As India expands access to advanced surgical procedures and regenerative therapies, the demand for cost-effective, scalable synthetic scaffolds is surging. Government initiatives supporting biotechnology and medical innovation, alongside domestic manufacturing capabilities, are positioning India as a high-growth market for synthetic tissue engineering in both public and private healthcare sectors.

Synthetic Tissue Engineering Market Share

The synthetic tissue engineering industry is primarily led by well-established companies, including:

- CollPlant Biotechnologies Ltd. (Israel)

- RevBio, Inc. (U.S.)

- BICO Group AB (Sweden)

- CELLINK (Sweden)

- Integra LifeSciences Corporation (U.S.)

- Medtronic (Ireland)

- Organogenesis Holdings Inc. (U.S.)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Stryker (U.S.)

- Baxter International Inc. (U.S.)

- TEI Biosciences Inc. (U.S.)

- Smith + Nephew (U.K.)

- Cook (U.S.)

- Johnson & Johnson Servces, Inc. (U.S.)

- Matricel GmbH (Germany)

- Orthocell Limited (Australia)

- Athersys, Inc. (U.S.)

- Vericel Corporation (U.S.)

- Biocomposites Ltd. (U.K.)

What are the Recent Developments in Global Synthetic Tissue Engineering Market?

- In March 2024, CollPlant Biotechnologies, a regenerative medicine company, announced the successful preclinical results of its collagen-based synthetic bio-ink, designed for 3D bioprinting of tissues and organs. The bio-ink, made from recombinant human collagen, demonstrated excellent biocompatibility and structural support for tissue regeneration. This advancement reinforces CollPlant’s position as a pioneer in biofabrication and highlights the increasing convergence of synthetic biomaterials and 3D printing in tissue engineering applications

- In February 2024, BICO Group AB, a global leader in bio convergence technologies, introduced BIO X6, a six-printhead 3D bioprinter designed for multi-material tissue fabrication using synthetic hydrogels and polymers. The system allows for high-throughput printing of complex tissues and supports pharmaceutical research and regenerative medicine development. This innovation showcases the growing role of customizable, synthetic scaffold solutions in next-generation medical applications

- In January 2024, RevBio, Inc. received FDA Breakthrough Device Designation for its TETRANITE synthetic bone adhesive, intended for cranial and orthopedic applications. This synthetic biomaterial enables rapid bone regeneration and stable fixation, significantly improving outcomes over traditional grafting methods. The recognition marks a major milestone in accelerating regulatory pathways for synthetic tissue engineering products

- In December 2023, researchers at University of Cambridge partnered with a biotech startup to develop electrospun nanofiber scaffolds made from synthetic biodegradable polymers for nerve regeneration. The project received funding from the U.K. Research and Innovation (UKRI) and targets clinical trials in 2025. The innovation underscores the potential of synthetic nanomaterials in addressing complex neurological injuries

- In October 2023, DSM Biomedical, a leading biomaterials company, launched a new line of customizable synthetic polymers specifically engineered for use in cardiovascular and dental tissue engineering. These materials feature tunable degradation rates and improved cell-adhesion properties, catering to device manufacturers seeking scalable synthetic solutions. This development reflects the expanding demand for specialized, application-specific synthetic biomaterials in the medical field

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.