Global Tissue Engineered Products Market

Market Size in USD Billion

USD

29.39 Billion

USD

85.63 Billion

2025

2033

USD

29.39 Billion

USD

85.63 Billion

2025

2033

| 2026 - 2033 | |

| USD 29.39 Billion | |

| USD 85.63 Billion | |

| % | |

|

Tissue-Engineered Products Market Size

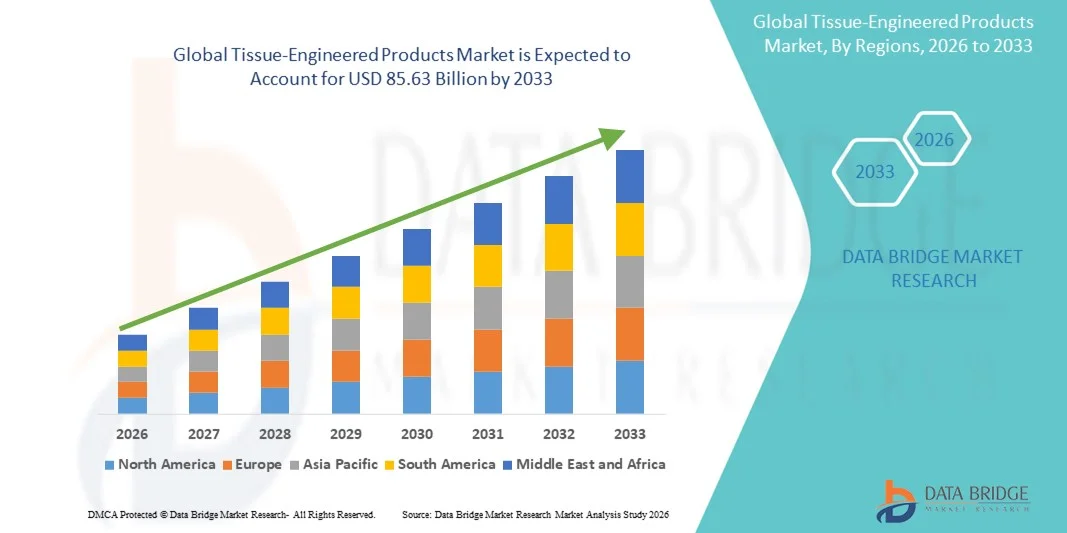

- The global tissue-engineered products market size was valued at USD 29.39 billion in 2025 and is expected to reach USD 85.63 billion by 2033, at a CAGR of 14.3% during the forecast period

- The market growth is largely fueled by increasing adoption of regenerative medicine and advanced biomaterials, coupled with technological advancements in tissue engineering and 3D bioprinting, driving innovative therapies across multiple medical applications

- Furthermore, rising demand for effective treatments for chronic diseases, organ repair, and wound healing is establishing tissue-engineered products as a critical solution in modern healthcare. These converging factors are accelerating the uptake of tissue-engineered solutions, thereby significantly boosting the industry's growth

Tissue-Engineered Products Market Analysis

- Tissue-engineered products, including advanced biomaterials and cell-based constructs, are increasingly vital in modern healthcare for repairing, replacing, or regenerating damaged tissues across various therapeutic areas due to their enhanced efficacy and compatibility with regenerative therapies

- The escalating demand for tissue-engineered products is primarily fueled by technological advancements in biomimetic, composite, nanocomposite, and nanofibrous materials, along with growing prevalence of chronic and degenerative diseases

- North America dominated the tissue-engineered products market with the largest revenue share of 38.9% in 2025, driven by advanced healthcare infrastructure, early adoption of regenerative solutions, high research investments, and the presence of leading industry players

- Asia-Pacific is expected to be the fastest-growing region during the forecast period due to increasing healthcare expenditure, rising prevalence of musculoskeletal and cardiovascular disorders, and expanding regenerative medicine initiatives in countries such as China and India

- Orthopaedics segment dominated the market with the largest market share of 41.8% in 2025, driven by rising incidence of bone and joint disorders, increasing demand for tissue-engineered implants, and ongoing innovations in biologically derived and synthetic materials for musculoskeletal repair

Report Scope and Tissue-Engineered Products Market Segmentation

|

Attributes |

Tissue-Engineered Products Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Tissue-Engineered Products Market Trends

Advancements in 3D Bioprinting and Biomaterials

- A significant and accelerating trend in the global tissue-engineered products market is the integration of 3D bioprinting with advanced biomaterials such as nanocomposites and biomimetic scaffolds, enabling more precise and patient-specific tissue constructs

- For instance, Organovo’s bioprinting platform creates liver and kidney tissue models for drug testing and regenerative applications, allowing for highly customized tissue architectures

- 3D bioprinting enables rapid fabrication of complex tissue structures, enhances cell viability, and supports integration with biologically derived materials, significantly improving therapeutic outcomes

- The combination of advanced materials and bioprinting platforms facilitates scalable production of tissue-engineered products across orthopaedic, cardiovascular, and skin applications, supporting clinical and commercial adoption

- This trend toward more sophisticated, patient-tailored, and reproducible tissue constructs is fundamentally transforming expectations in regenerative medicine. Consequently, companies such as CELLINK are developing biomaterial inks and bioprinting systems for enhanced tissue functionality

- The demand for tissue-engineered products leveraging 3D bioprinting and novel biomaterials is growing rapidly across both research and clinical applications, as healthcare providers increasingly prioritize regenerative solutions with higher precision and efficacy

- Integration of AI and computational modeling in tissue design is emerging, allowing predictive simulation of tissue growth and improved design of scaffolds for specific patient needs

Tissue-Engineered Products Market Dynamics

Driver

Increasing Demand Due to Chronic Diseases and Aging Population

- The rising prevalence of chronic diseases and an aging global population are significant drivers of heightened demand for tissue-engineered products

- For instance, Stryker’s tissue-engineered bone grafts are increasingly utilized in orthopaedic and spinal procedures to address age-related degenerative conditions

- As patients and healthcare providers seek effective regenerative solutions, tissue-engineered products offer advanced alternatives to traditional grafts, reducing complications and improving recovery times

- Furthermore, growing awareness of the benefits of regenerative therapies in cardiac, skin, and musculoskeletal applications is boosting adoption across hospitals and research centers

- The expanding healthcare infrastructure, rising investments in regenerative medicine, and technological advancements in biomaterials and cell therapies further propel the uptake of tissue-engineered products

- Increasing government initiatives and funding for regenerative medicine research are creating favorable conditions for market growth

- Rising patient preference for minimally invasive and faster-healing therapeutic options is encouraging healthcare providers to adopt tissue-engineered solutions more widely

Restraint/Challenge

High Cost and Regulatory Hurdles

- The high cost of tissue-engineered products, coupled with complex regulatory requirements, poses a significant challenge to broader market adoption

- For instance, regulatory approvals for cell-based therapies and scaffold-based implants often require extensive preclinical and clinical validation, delaying commercialization

- Addressing these challenges through cost-effective manufacturing processes, standardization of biomaterials, and streamlined regulatory pathways is crucial for broader adoption

- In addition, the need for specialized infrastructure, trained personnel, and quality control adds to the operational complexity, limiting penetration in emerging markets

- While technological advancements are reducing production costs, the perceived premium of tissue-engineered solutions compared to traditional therapies can still hinder adoption among budget-conscious healthcare providers

- Overcoming these challenges through improved manufacturing efficiency, regulatory harmonization, and strategic partnerships will be vital for sustained market growth in the global tissue-engineered products market

- Limited long-term clinical data on efficacy and safety of certain tissue-engineered products creates hesitation among some healthcare providers and insurers

- Variability in reimbursement policies across regions further restricts market access and can delay adoption, especially in emerging economies

Tissue-Engineered Products Market Scope

The market is segmented on the basis of material, type, and application.

- By Material

On the basis of material, the tissue-engineered products market is segmented into biomimetic materials, composite materials, nanocomposite materials, and nanofibrous materials. Biomimetic Materials dominated the market with the largest revenue share in 2025, driven by their ability to closely mimic the natural extracellular matrix, enhancing cell adhesion, proliferation, and differentiation. These materials are widely used in orthopaedic and skin tissue applications due to their high biocompatibility and functional similarity to human tissues. The demand is further supported by clinical adoption in regenerative therapies and the ability to accelerate tissue repair. Biomimetic scaffolds also offer versatility in combining with growth factors or stem cells, making them ideal for advanced regenerative medicine applications. Their proven performance in preclinical and clinical studies enhances confidence among healthcare providers and researchers.

Nanofibrous Materials are anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in electrospinning and nanofabrication technologies. Nanofibrous scaffolds provide a high surface area-to-volume ratio, supporting better cell interaction and nutrient exchange, which is critical for complex tissue engineering. They are increasingly applied in cardiovascular, musculoskeletal, and skin regeneration due to their tunable porosity and mechanical strength. The growing integration of nanofibrous materials with bioactive molecules and stem cells further expands their therapeutic potential. Rising research interest and funding for nano-enabled regenerative solutions contribute to their accelerated market adoption.

- By Type

On the basis of type, the tissue-engineered products market is segmented into synthetic materials, biologically derived materials, and others. Synthetic Materials dominated the market with the largest revenue share in 2025 due to their reproducibility, tunable mechanical properties, and scalability for commercial production. Synthetic scaffolds are widely used in orthopaedic and spinal applications because they can be engineered to meet specific load-bearing requirements while ensuring biocompatibility. These materials allow precise control over degradation rates and structural characteristics, which is important for matching tissue regeneration timelines. Manufacturers favor synthetic materials for consistent performance and ease of regulatory approval. Their integration with growth factors and bioactive coatings enhances their functionality in clinical applications.

Biologically Derived Materials are expected to witness the fastest growth from 2026 to 2033, driven by increasing preference for naturally sourced scaffolds that promote better cell interaction and reduced immunogenic response. Materials such as collagen, fibrin, and decellularized matrices support tissue-specific regeneration and are increasingly adopted in skin, cardiac, and musculoskeletal therapies. Advancements in decellularization and sterilization techniques are improving their safety and performance. The rising trend toward personalized regenerative medicine and tissue-specific therapies is boosting demand for biologically derived materials. Research collaborations and clinical success stories accelerate their adoption in both hospitals and research labs.

- By Application

On the basis of application, the tissue-engineered products market is segmented into orthopaedics, musculoskeletal & spine, neurology, cardiology & vascular, skin & integumentary, and others. Orthopaedics dominated the market with the largest revenue share of 41.8% in 2025, driven by increasing incidence of bone fractures, joint injuries, and degenerative disorders requiring grafts and implants. Tissue-engineered scaffolds and bone substitutes offer faster healing, reduced rejection rates, and improved integration with native tissue. Orthopaedic applications benefit from extensive clinical evidence supporting the efficacy of both synthetic and biologically derived materials. Hospitals and research centers increasingly prefer tissue-engineered products over conventional grafts due to better functional outcomes. Rising ageing population and sports-related injuries further drive market demand. Integration with stem cell therapies and growth factors enhances therapeutic potential in orthopaedic regeneration.

Musculoskeletal & Spine applications are anticipated to witness the fastest growth rate from 2026 to 2033, fueled by technological advances in spinal scaffolds, regenerative implants, and minimally invasive surgical techniques. Rising prevalence of spinal disorders, deformities, and degenerative conditions is driving demand for tissue-engineered solutions that support bone and disc regeneration. These applications benefit from improved scaffold design, mechanical strength, and compatibility with patient-specific implants. Increasing research collaborations and adoption of personalized regenerative therapies accelerate growth. The expansion of healthcare infrastructure in emerging regions further supports the uptake of musculoskeletal and spine tissue-engineered products.

Tissue-Engineered Products Market Regional Analysis

- North America dominated the tissue-engineered products market with the largest revenue share of 38.9% in 2025, driven by advanced healthcare infrastructure, early adoption of regenerative solutions, high research investments, and the presence of leading industry players

- Healthcare providers and research institutions in the region highly value the efficacy, biocompatibility, and customizable nature of tissue-engineered products, supporting widespread clinical and commercial adoption

- This widespread adoption is further supported by strong government initiatives, robust funding for regenerative therapies, and a technologically advanced population, establishing tissue-engineered solutions as a preferred option for orthopaedic, cardiovascular, and skin-related applications

U.S. Tissue-Engineered Products Market Insight

The U.S. tissue-engineered products market captured the largest revenue share of 42% in 2025 within North America, fueled by advanced healthcare infrastructure and early adoption of regenerative medicine. Hospitals and research institutions are increasingly prioritizing personalized tissue-engineered implants and scaffolds for orthopaedic, cardiovascular, and skin applications. The growing trend of minimally invasive procedures, combined with robust demand for stem cell and scaffold-based therapies, further propels market growth. Moreover, government funding and public-private partnerships supporting regenerative medicine research are significantly contributing to the market's expansion.

Europe Tissue-Engineered Products Market Insight

The Europe tissue-engineered products market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong regulatory support and rising adoption of advanced biomaterials. Increasing prevalence of chronic and degenerative diseases, coupled with the growing demand for regenerative therapies in hospitals and clinics, is fostering market adoption. European healthcare providers are also attracted to tissue-engineered products for their potential to reduce recovery times and improve patient outcomes. The region is witnessing significant growth across orthopaedic, musculoskeletal, and skin applications, with products being incorporated into both new therapies and clinical research programs.

U.K. Tissue-Engineered Products Market Insight

The U.K. tissue-engineered products market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing investments in regenerative medicine and home-grown biotech innovation. In addition, rising prevalence of musculoskeletal disorders and cardiovascular conditions is encouraging healthcare providers to adopt tissue-engineered solutions. The U.K.’s focus on personalized medicine, alongside strong clinical research and manufacturing capabilities, is expected to continue to stimulate market growth.

Germany Tissue-Engineered Products Market Insight

The Germany tissue-engineered products market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of advanced regenerative therapies and adoption of biomaterials-based treatments. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and quality, promotes the adoption of tissue-engineered products in hospitals and research facilities. Integration of these products with surgical procedures and clinical trials is becoming increasingly prevalent, with a strong preference for safe, high-efficacy solutions aligning with local healthcare standards.

Asia-Pacific Tissue-Engineered Products Market Insight

The Asia-Pacific tissue-engineered products market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by rising healthcare expenditure, rapid urbanization, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards advanced therapies, supported by government initiatives promoting biotechnology and regenerative medicine, is driving market adoption. Furthermore, APAC is emerging as a hub for manufacturing biomaterials and scaffold-based products, improving accessibility and affordability for a wider patient base.

Japan Tissue-Engineered Products Market Insight

The Japan tissue-engineered products market is gaining momentum due to the country’s high focus on healthcare innovation, aging population, and demand for advanced regenerative solutions. Hospitals and clinics increasingly adopt tissue-engineered scaffolds and implants for musculoskeletal, cardiac, and skin regeneration applications. Integration with stem cell therapies and clinical research programs is fueling growth. Moreover, Japan's emphasis on precision medicine and technological sophistication is expected to spur further adoption in both residential healthcare and specialized clinical settings.

India Tissue-Engineered Products Market Insight

The India tissue-engineered products market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly growing healthcare infrastructure, urbanization, and rising incidence of chronic and degenerative diseases. India is becoming an important market for tissue-engineered implants, scaffolds, and biologically derived materials in orthopaedic, cardiovascular, and skin applications. Government initiatives promoting biotechnology and regenerative medicine, coupled with the availability of cost-effective products and strong domestic manufacturing capabilities, are key factors propelling market growth in India.

Tissue-Engineered Products Market Share

The Tissue-Engineered Products industry is primarily led by well-established companies, including:

- Organogenesis Inc. (U.S.)

- Integra LifeSciences Corporation (U.S.)

- MIMEDX Group, Inc (U.S.)

- Vericel Corporation (U.S.)

- Zimmer Biomet (U.S.)

- Medtronic (Ireland)

- Stryker (U.S.)

- B. Braun SE (Germany)

- Baxter (U.S.)

- AbbVie Inc. (U.S.)

- Smith & Nephew (U.K.)

- Tissue Regenix Group plc (U.K.)

- Organovo Holdings, Inc. (U.S.)

- CollPlant Biotechnologies Ltd. (Israel)

- Xeltis AG (Switzerland)

- Prellis Biologics (U.S.)

- Bit Bio (U.K.)

- Be Biopharma Inc. (U.S.)

- TELA Bio, Inc. (U.S.)

- Orthocell Limited (Australia)

What are the Recent Developments in Global Tissue-Engineered Products Market?

- In November 2025, Humacyte presented positive long‑term clinical results for its acellular tissue‑engineered vessels (ATEV) at the VEITHsymposium, showing host‑cell integration and sustained outcomes across various vascular indications. The presentations highlighted progressive recellularization of the engineered vessels and durable performance in hemodialysis access and trauma cases, indicating strong potential for broader therapeutic applications beyond the initial approved extremity trauma indication

- In May 2025, VERIGRAFT received regulatory green light after completing patient recruitment in its clinical trial of Personalized Tissue‑Engineered Veins (P‑TEV) for chronic venous insufficiency (CVI). This milestone allows the company to proceed toward pivotal efficacy phases, signaling confidence from regulators in the safety data collected and advancing a novel personalized graft capable of addressing long‑term vascular disease management

- In February 2025, Humacyte announced the commercial launch of Symvess, its first acellular tissue‑engineered vessel for extremity vascular trauma, after FDA authorization for commercial shipments. Symvess, designed as an off‑the‑shelf vascular conduit for arterial injury repair when traditional grafts are not feasible, began initial uptake in trauma centers and hospitals, with at least 21 hospitals initiating approval processes. This launch marks a pivotal step toward bringing engineered human tissues into routine clinical care

- In January 2025, Humacyte provided key commercial launch and pricing updates for Symvess, including establishing a pricing model and onboarding a specialized sales force. The company revealed strategy to support adoption among hospitals by demonstrating potential cost advantages over current standards of care through budget impact modeling, and trained an experienced vascular sales team to accelerate market penetration

- In December 2024, the U.S. FDA granted full approval to Symvess, the first acellular tissue‑engineered vessel indicated for adults with extremity arterial injury. This regulatory milestone represents a landmark in regenerative medicine, allowing a bioengineered human tissue product to be used as a vascular conduit to restore blood flow, offering an alternative to vein graft harvesting and synthetic grafts particularly valuable in urgent trauma cases

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.