Global Transcranial Doppler Ultrasound Market

Market Size in USD Million

USD

489.69 Million

USD

804.97 Million

2025

2033

USD

489.69 Million

USD

804.97 Million

2025

2033

| 2026 - 2033 | |

| USD 489.69 Million | |

| USD 804.97 Million | |

| % | |

|

Transcranial Doppler Ultrasound Market Size

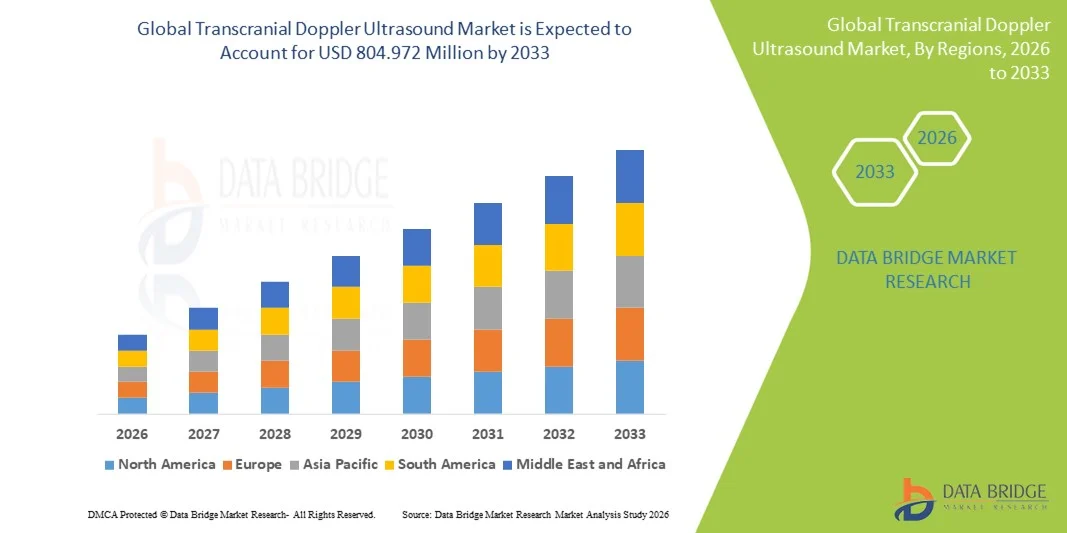

- The global transcranial doppler ultrasound market size was valued at USD 489.69 million in 2025 and is expected to reach USD 804.972 million by 2033, at a CAGR of 6.41% during the forecast period

- The market growth is primarily driven by the increasing prevalence of cerebrovascular disorders, such as stroke and aneurysms, along with rising awareness about non-invasive diagnostic techniques for brain monitoring

- In addition, technological advancements in doppler ultrasound systems, including portable and high-resolution devices, are enhancing accuracy and ease of use in both clinical and research settings. These factors, combined with a growing geriatric population and the expanding healthcare infrastructure, are fueling the adoption of transcranial Doppler ultrasound systems globally

Transcranial Doppler Ultrasound Market Analysis

- Transcranial doppler ultrasound, offering real-time, non-invasive monitoring of cerebral blood flow, is increasingly vital in diagnosing and managing cerebrovascular and neurological disorders, including stroke, sickle cell disease, and intracranial steno-occlusive conditions, due to its portability, safety, and cost-effectiveness

- The rising prevalence of cerebrovascular diseases, growing awareness of early detection, and preference for non-invasive, point-of-care diagnostic tools are driving the adoption of transcranial Doppler ultrasound systems worldwide

- North America dominated the market with the largest revenue share of 41.7% in 2025, supported by advanced healthcare infrastructure, high adoption of neuroimaging technologies, and the presence of major market players offering both portable and standalone systems

- Asia-Pacific is expected to be the fastest-growing region during the forecast period, fueled by increasing hospital and diagnostic center investments, rising incidence of stroke and sickle cell disease, and government initiatives to expand access to advanced neurodiagnostic equipment

- Non-imaging segment dominated with a market share of 55.3% in 2025, driven by their widespread use in hospitals and diagnostic centers for acute ischemic stroke monitoring, micro emboli detection, and intraoperative cerebral blood flow assessment

Report Scope and Transcranial Doppler Ultrasound Market Segmentation

|

Attributes |

Transcranial Doppler Ultrasound Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Transcranial Doppler Ultrasound Market Trends

Advancements in Portable and AI-Enabled Monitoring

- A significant and accelerating trend in the global transcranial Doppler ultrasound market is the development of portable systems integrated with AI algorithms for real-time cerebral blood flow analysis, enhancing diagnostic accuracy and clinical efficiency

- For instance, the SONOWAND TCD system incorporates AI-assisted waveform interpretation, enabling clinicians to detect abnormalities faster and reducing dependency on manual analysis

- AI integration in TCD devices allows features such as automated detection of micro-emboli, stroke risk prediction, and trend analysis over time, improving patient monitoring and decision-making

- Portable transcranial Doppler devices facilitate bedside diagnostics and remote monitoring, allowing use in emergency care, ICU, and outpatient clinics, which enhances workflow and reduces patient transfer requirements

- This trend toward smarter, portable, and AI-enabled monitoring systems is redefining expectations for neurovascular diagnostics, with companies such as Natus Medical developing TCD devices capable of automatic waveform analysis and remote reporting

- The demand for advanced, AI-integrated TCD systems is growing rapidly in both hospital and diagnostic settings, as healthcare providers increasingly prioritize speed, accuracy, and non-invasive cerebral monitoring

- Companies are also focusing on multi-parameter monitoring, combining TCD with other non-invasive neurological diagnostic tools, which allows simultaneous assessment of cerebral perfusion, oxygenation, and hemodynamics, enhancing overall diagnostic capability

Transcranial Doppler Ultrasound Market Dynamics

Driver

Rising Prevalence of Cerebrovascular Disorders and Non-Invasive Diagnostics

- The increasing incidence of stroke, sickle cell disease, and other cerebrovascular disorders, combined with a preference for non-invasive monitoring techniques, is a key driver for the growing adoption of transcranial Doppler ultrasound systems

- For instance, in March 2025, Natus Medical launched a portable TCD device specifically designed for stroke risk assessment and sickle cell monitoring in children, highlighting innovations targeting high-demand clinical applications

- As healthcare providers focus on early detection and continuous monitoring, TCD systems offer advantages such as real-time cerebral blood flow tracking, micro-emboli detection, and automated reporting, which improve patient outcomes

- Furthermore, the rising awareness of neurological disorders and increasing investments in advanced diagnostic equipment are making TCD devices an integral tool in modern hospitals and diagnostic centers

- The ease of use, bedside application, and ability to integrate with hospital monitoring networks are key factors propelling TCD adoption in both developed and emerging regions

- The growing demand for portable and AI-enabled TCD devices is also driven by the need for point-of-care diagnostics in emergency care, ICU, and outpatient settings

- For instance, governments and healthcare organizations in Asia-Pacific are investing in stroke management programs, providing subsidies for advanced TCD systems in regional hospitals, further boosting market growth

- Increasing research collaborations between medical device companies and universities for the development of AI-powered neuroimaging solutions is expanding the scope of TCD applications, creating opportunities for advanced diagnostics and clinical trials

Restraint/Challenge

High Equipment Cost and Limited Skilled Operators

- The relatively high cost of advanced transcranial Doppler ultrasound systems compared to conventional imaging methods is a significant barrier, limiting adoption in price-sensitive healthcare facilities

- For instance, portable AI-enabled TCD devices from companies such as Natus Medical can cost multiple times more than standard Doppler systems, making them less accessible for smaller clinics or developing regions

- Another challenge is the shortage of trained operators capable of accurately performing TCD examinations and interpreting results, which can affect reliability and consistency of clinical outcomes

- Addressing these challenges requires investment in operator training programs, user-friendly device interfaces, and cost-effective solutions that balance advanced features with affordability

- While portable and AI-enabled TCD devices improve workflow and diagnostic accuracy, the combination of equipment cost and skill requirements continues to constrain wider market penetration

- Overcoming these barriers through targeted training, financing options, and simplified user interfaces will be crucial for sustained market growth and broader adoption

- For instance, inconsistent reimbursement policies for advanced TCD diagnostics across countries limit hospital adoption, as many facilities struggle to justify equipment costs without standardized insurance coverage

- In addition, device maintenance requirements and calibration needs for high-precision TCD systems can pose operational challenges, especially in smaller or rural healthcare centers, slowing market expansion

Transcranial Doppler Ultrasound Market Scope

The market is segmented on the basis of equipment type, end-user, application, display mode, and mode type.

- By Equipment Type

On the basis of equipment type, the market is segmented into imaging and non-imaging transcranial Doppler systems. The non-imaging segment dominated the market with the largest revenue share of 55.3% in 2025, driven by its established use in routine cerebrovascular monitoring and ease of operation in hospital and diagnostic settings. Non-imaging TCD systems are widely adopted for stroke risk assessment, micro-emboli detection, and continuous bedside monitoring due to their cost-effectiveness and portability. Hospitals often prefer non-imaging systems because they allow for rapid assessments without requiring extensive operator training. Furthermore, these systems are compatible with various monitoring accessories and can be integrated with hospital networks for real-time data reporting. The non-imaging segment also benefits from ongoing advancements in automated waveform analysis and AI-based interpretation, enhancing clinical efficiency.

The imaging segment is expected to witness the fastest growth rate of 18.9% from 2026 to 2033, fueled by rising adoption in neurosurgery, neurocritical care, and research applications. Imaging TCD systems provide detailed visualization of cerebral blood vessels and hemodynamic flow, which is crucial for precise diagnosis and preoperative planning. Increasing use in advanced hospital setups and academic research centers is boosting demand, as imaging systems enable simultaneous anatomical and functional assessment. Technological developments such as high-resolution imaging and AI-assisted vessel tracking further enhance diagnostic capabilities, making these systems increasingly attractive for specialized applications.

- By End-User

On the basis of end-user, the market is segmented into hospitals, diagnostic centers, and others. The hospitals segment dominated the market with a share of 60.1% in 2025, owing to high adoption of TCD systems for continuous monitoring in stroke units, ICUs, and neurology departments. Hospitals prefer TCD for its non-invasive nature and ability to provide real-time cerebral blood flow measurements, which is critical for patient management. The integration of TCD systems with hospital information systems and electronic health records allows clinicians to monitor trends over time and improve patient outcomes. Moreover, hospitals benefit from portable and standalone systems for bedside use, enhancing workflow efficiency. The segment is further supported by government and private hospital investments in advanced neurodiagnostic equipment.

The diagnostic centers segment is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, driven by increasing outpatient monitoring and preventive neurovascular screening programs. Diagnostic centers are increasingly adopting TCD for sickle cell disease management, stroke risk assessment, and routine cerebrovascular health evaluations. The rising trend of point-of-care diagnostics and specialized neurological testing in outpatient settings is fueling demand. Portable and easy-to-use devices make it feasible for centers with limited staff to perform multiple assessments efficiently. In addition, partnerships with research institutions for clinical trials and neurological studies further encourage adoption in diagnostic centers.

- By Application

On the basis of application, the market is segmented into sickle cell disease, acute ischemic stroke, intracranial steno-occlusive disease, and micro-emboli detection. The acute ischemic stroke segment dominated the market with a share of 42.8% in 2025, owing to the high prevalence of stroke and the critical role of TCD in early diagnosis and monitoring of cerebral blood flow. Hospitals and emergency care units rely on TCD for rapid, bedside assessment of cerebral hemodynamics in acute cases. The non-invasive nature and real-time data output allow timely interventions, reducing the risk of permanent neurological damage. Integration with AI-assisted analysis improves detection of occlusions, stenosis, and perfusion deficits. Stroke protocols increasingly include TCD monitoring as part of standardized care, further boosting its adoption.

The sickle cell disease segment is expected to witness the fastest growth rate of 19.3% from 2026 to 2033, driven by rising awareness and screening programs for children at risk of cerebrovascular complications. TCD is recommended as a routine monitoring tool for pediatric sickle cell patients to detect elevated stroke risk early. Increasing government initiatives and NGO-led healthcare programs in regions such as Africa and Asia-Pacific are expanding access to TCD screening. Technological improvements in portable devices and automated analysis make regular monitoring more feasible and efficient. Research and clinical trials on sickle cell-related neurovascular complications are also contributing to market growth in this segment.

- By Display Mode

On the basis of display mode, the market is segmented into B-mode and M-mode. The M-mode segment dominated the market with a share of 51.4% in 2025, as it is widely used for continuous monitoring of cerebral blood flow velocities and detection of micro-emboli events. M-mode TCD allows precise measurement of flow dynamics over time, making it essential in stroke and neurocritical care. Clinicians rely on M-mode for its real-time waveform visualization, enabling timely intervention during acute cerebrovascular events. The segment benefits from advancements in digital signal processing and AI-assisted waveform interpretation, enhancing accuracy and clinical decision-making. Continuous monitoring capabilities also make M-mode devices popular in ICU and intraoperative environments.

The B-mode segment is expected to witness the fastest CAGR of 16.7% from 2026 to 2033, driven by increasing adoption in diagnostic and research applications where anatomical visualization of cerebral vessels is required. B-mode provides structural imaging alongside blood flow assessment, enabling comprehensive evaluation of neurovascular health. High-resolution B-mode systems are gaining traction in specialized hospitals and academic research centers. The combination of anatomical and functional data allows for improved diagnostic confidence. Technological developments such as 3D visualization and AI-assisted vessel tracking further enhance the utility of B-mode systems.

- By Mode Type

On the basis of mode type, the market is segmented into portable and standalone systems. The standalone segment dominated the market with a share of 54.6% in 2025, due to widespread deployment in hospitals and large diagnostic centers requiring high-performance and feature-rich devices. Standalone TCD systems provide comprehensive functionality, including advanced waveform analysis, multi-parameter monitoring, and integration with hospital networks. Hospitals prefer standalone units for their reliability, accuracy, and capacity to handle multiple simultaneous patients. The segment benefits from ongoing investments in neurocritical care and research facilities. Compatibility with multiple transducers and accessories further enhances their adoption.

The portable segment is expected to witness the fastest growth rate of 20.1% from 2026 to 2033, fueled by increasing demand for point-of-care diagnostics, bedside monitoring, and emergency stroke management. Portable TCD systems are lightweight, battery-operated, and easy to transport, making them ideal for use in ICUs, outpatient clinics, and remote healthcare facilities. Rising adoption of telemedicine and home healthcare services also supports portable TCD growth. Technological advancements such as AI-assisted analysis and wireless connectivity make portable devices increasingly capable and reliable.

Transcranial Doppler Ultrasound Market Regional Analysis

- North America dominated the market with the largest revenue share of 41.7% in 2025, supported by advanced healthcare infrastructure, high adoption of neuroimaging technologies, and the presence of major market players offering both portable and standalone systems

- Healthcare providers in the region prioritize non-invasive, real-time monitoring solutions for cerebrovascular disorders, making TCD systems a key diagnostic and monitoring tool in stroke units, ICUs, and neurology departments

- This widespread adoption is further supported by significant investments in research and development, strong presence of key market players offering portable and AI-enabled TCD devices, and high awareness among clinicians about early detection of stroke and sickle cell complications, establishing transcranial Doppler ultrasound as a preferred solution in both hospital and diagnostic settings

U.S. Transcranial Doppler Ultrasound Market Insight

The U.S. transcranial Doppler ultrasound market captured the largest revenue share of 79% in 2025 within North America, driven by advanced healthcare infrastructure and the widespread adoption of non-invasive neuroimaging technologies. Hospitals and diagnostic centers increasingly rely on TCD systems for stroke assessment, sickle cell disease monitoring, and cerebrovascular disorder management. The rising demand for portable and AI-enabled TCD devices, along with integration into hospital monitoring networks, further supports market growth. In addition, increasing investments in stroke prevention programs and clinical research are encouraging adoption across both pediatric and adult care. The strong presence of key market players offering innovative solutions reinforces the market's expansion.

Europe Transcranial Doppler Ultrasound Market Insight

The Europe TCD market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing prevalence of stroke, intracranial steno-occlusive disorders, and rising awareness of early diagnosis. Stringent healthcare regulations and growing hospital investments in advanced neurodiagnostic tools are fostering adoption. European diagnostic centers and hospitals are leveraging TCD systems for acute stroke management and micro-emboli detection. The region’s technological advancements in AI-assisted monitoring and emphasis on preventive healthcare further boost market growth. Integration of TCD systems with electronic health records and hospital networks enhances operational efficiency and clinical decision-making.

U.K. Transcranial Doppler Ultrasound Market Insight

The U.K. TCD market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing home and hospital-based neurodiagnostic programs and rising awareness of cerebrovascular health. Hospitals and outpatient clinics are adopting TCD systems for stroke risk assessment and sickle cell disease monitoring. Government initiatives promoting early detection and preventive care support the market expansion. The country’s advanced healthcare infrastructure and research collaborations with universities and medical device companies are fueling innovation. The demand for portable, AI-enabled TCD devices in both urban and semi-urban hospitals is expected to continue stimulating growth.

Germany Transcranial Doppler Ultrasound Market Insight

The Germany TCD market is expected to expand at a considerable CAGR during the forecast period, fueled by rising awareness of cerebrovascular disorders and increasing demand for advanced diagnostic solutions. Hospitals prioritize non-invasive, real-time monitoring of cerebral blood flow for stroke and aneurysm management. Germany’s emphasis on innovation, technology integration, and precision healthcare promotes the adoption of both portable and standalone TCD systems. The integration of TCD devices with hospital monitoring networks and electronic health records supports clinical efficiency. Growing investments in preventive and neurocritical care further encourage market adoption.

Asia-Pacific Transcranial Doppler Ultrasound Market Insight

The Asia-Pacific TCD market is poised to grow at the fastest CAGR of 22% during the forecast period of 2026 to 2033, driven by rising incidence of stroke, sickle cell disease, and intracranial steno-occlusive disorders across the region. Expanding healthcare infrastructure, urbanization, and increasing government initiatives for stroke and neurovascular care are key growth drivers. Countries such as China, Japan, and India are witnessing a growing preference for portable and AI-assisted TCD systems to improve patient monitoring and clinical workflow. Furthermore, the availability of cost-effective systems and domestic manufacturing capabilities is increasing accessibility to a broader consumer base. Rising awareness of preventive healthcare and early diagnosis further accelerates market growth.

Japan Transcranial Doppler Ultrasound Market Insight

The Japan TCD market is gaining momentum due to the country’s advanced healthcare infrastructure, high geriatric population, and focus on early detection of cerebrovascular disorders. Hospitals and diagnostic centers are increasingly adopting TCD systems for stroke assessment, sickle cell monitoring, and micro-emboli detection. Integration with AI-assisted analysis and hospital monitoring systems is enhancing workflow efficiency. The Japanese market emphasizes accuracy, reliability, and ease of use, promoting adoption of both portable and standalone devices. Growing awareness of preventive neurological care and government initiatives further stimulate market growth.

India Transcranial Doppler Ultrasound Market Insight

The India TCD market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to increasing prevalence of stroke and sickle cell disease, along with rapid expansion of healthcare facilities. Hospitals and diagnostic centers are increasingly adopting TCD systems for early detection and monitoring of cerebrovascular disorders. The push towards smart hospitals, government initiatives for stroke prevention, and the availability of affordable, portable TCD devices are key factors propelling market growth. Strong domestic manufacturing capabilities and rising awareness among clinicians and patients further drive adoption. The growing focus on preventive healthcare and point-of-care diagnostics is expected to sustain market expansion in India.

Transcranial Doppler Ultrasound Market Share

The Transcranial Doppler Ultrasound industry is primarily led by well-established companies, including:

- NeuraSignal (U.S.)

- Rimed Ltd. (Israel)

- Viasonix Ltd. (Israel)

- Natus Medical Incorporated (U.S.)

- Compumedics Limited (Australia)

- DWL Elektronische Systeme GmbH (Germany)

- GE Healthcare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Mindray Medical International Limited (China)

- ATYS Medical (France)

- EDAN Instruments, Inc. (China)

- EB Neuro S.p.A (Italy)

- Neurolite AG (Switzerland)

- Konica Minolta, Inc. (Japan)

- Shenzhen Delica Medical Equipment Co., Ltd. (China)

- Spencer Technologies (U.S.)

- Probo Medical (Germany)

- Fujifilm SonoSite, Inc. (U.S.)

- Medtronic (Ireland)

- NIHON KOHDEN CORPORATION (Japan)

What are the Recent Developments in Global Transcranial Doppler Ultrasound Market?

- In June 2025, a feature article detailed how TCD ultrasound is transforming PFO detection and stroke prevention, emphasizing its higher sensitivity than traditional echocardiography and the increasing role of automated systems such as NG2 in improving clinical stroke workflows

- In March 2025, NeuraSignal Inc. was highlighted as Canada’s only licensed Transcranial Doppler (TCD) manufacturer cleared by Health Canada, underscoring regulatory progress and expanded access to advanced robotic TCD systems across Canadian healthcare facilities

- In February 2025, NeuraSignal announced that a study on its robot‑assisted Transcranial Doppler (raTCD) technology for detecting right‑to‑left shunts (RLS) and patent foramen ovale (PFO) was accepted for presentation at the International Stroke Conference (ISC) 2025, demonstrating superior detection performance compared with traditional methods and supporting integration into stroke care workflows

- In October 2023, NeuraSignal’s NovaGuide Intelligent Ultrasound system showed significantly improved performance in detecting stroke‑associated heart defects (RLS) compared with standard care, with BUBL clinical trial data supporting enhanced diagnostic accuracy using robot‑assisted TCD

- In February 2023, NovaSignal donated its NovaGuide 2 Intelligent Ultrasound (robot‑assisted TCD) to The Jacobs Institute to advance stroke and vascular research, enabling continuous neuromonitoring for improved procedural safety and neurovascular outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.