Global Uremia Treatment Market

Market Size in USD Billion

USD

6.85 Billion

USD

10.83 Billion

2024

2032

USD

6.85 Billion

USD

10.83 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.85 Billion | |

| USD 10.83 Billion | |

| % | |

|

Uremia Treatment Market Size

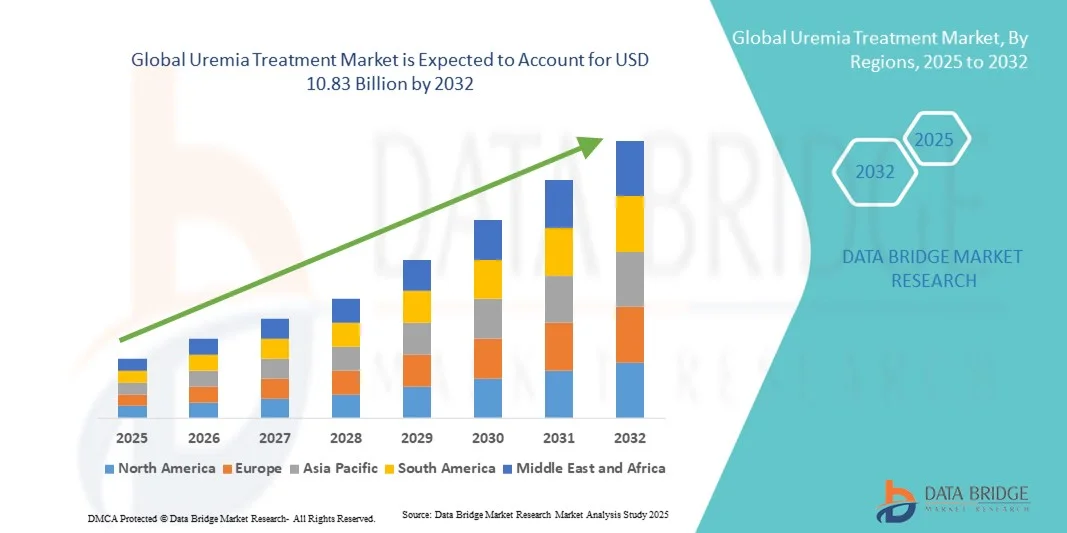

- The global uremia treatment market size was valued at USD 6.85 billion in 2024 and is expected to reach USD 10.83 billion by 2032, at a CAGR of 5.90% during the forecast period

- The market growth is largely driven by the rising prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), which significantly increase the risk of uremia, thereby boosting the demand for effective treatment options

- Furthermore, ongoing advancements in dialysis technologies, improved therapeutic approaches, and increasing awareness regarding early diagnosis and management of renal disorders are accelerating the adoption of uremia treatment solutions, thereby significantly enhancing the market’s expansion

Uremia Treatment Market Analysis

- Uremia treatment, encompassing dialysis, pharmacological therapy, and renal replacement strategies, plays a critical role in managing toxin accumulation caused by kidney failure, thereby preventing severe complications in patients with chronic kidney disease (CKD) and end-stage renal disease (ESRD)

- The escalating demand for uremia treatment is primarily driven by the rising global burden of CKD, increasing geriatric population, and growing awareness regarding advanced renal care and early diagnosis of kidney dysfunction

- North America dominated the uremia treatment market with the largest revenue share of 40% in 2024, supported by well-established healthcare infrastructure, high disease prevalence, and the presence of major dialysis service providers and pharmaceutical companies driving innovation in uremia management

- Asia-Pacific is expected to be the fastest-growing region in the uremia treatment market during the forecast period due to improving healthcare access, rising investments in dialysis centers, and growing government initiatives aimed at combating renal disorders

- The hemodialysis segment dominated the uremia treatment market with a market share of 46.5% in 2024, driven by its widespread availability, proven efficacy, and increasing utilization among ESRD patients globally

Report Scope and Uremia Treatment Market Segmentation

|

Attributes |

Uremia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Uremia Treatment Market Trends

Technological Advancements in Dialysis and Regenerative Therapies

- A significant and accelerating trend in the global uremia treatment market is the integration of advanced dialysis technologies and regenerative medicine approaches aimed at improving toxin removal efficiency and patient outcomes. This evolution is redefining standards in renal care management worldwide

- For instance, Baxter International introduced portable and connected peritoneal dialysis systems that enable real-time monitoring and better patient compliance, highlighting the shift toward digital and patient-centric dialysis solutions

- AI integration in dialysis equipment enables personalized treatment adjustments based on patient data analytics, improving precision and reducing complications. For instance, Outset Medical’s Tablo Hemodialysis System uses AI algorithms to optimize dialysis cycles and predict maintenance needs. Furthermore, remote monitoring capabilities allow clinicians to track treatment adherence and make timely interventions

- This trend toward smarter, connected, and patient-focused treatment systems is fundamentally reshaping expectations for kidney disease management. Consequently, companies such as Medtronic and Baxter are focusing on AI-driven dialysis solutions with enhanced connectivity and patient engagement features

- The demand for technologically advanced and data-driven uremia treatments is growing rapidly across both hospital and home-care settings, as healthcare providers increasingly prioritize improved clinical outcomes and personalized therapy approaches

Uremia Treatment Market Dynamics

Driver

Rising Prevalence of Chronic Kidney Disease and Advancements in Dialysis Technology

- The increasing global incidence of chronic kidney disease (CKD) and end-stage renal disease (ESRD), coupled with ongoing improvements in dialysis techniques and therapeutic approaches, is a major driver for the uremia treatment market’s expansion

- For instance, in March 2024, Fresenius Medical Care launched an advanced home hemodialysis platform in Europe designed to improve patient convenience and treatment outcomes, reinforcing the role of innovation in market growth

- As the aging population and lifestyle-related disorders such as diabetes and hypertension continue to rise, the demand for effective uremia management solutions has surged, highlighting the importance of efficient renal replacement therapies

- Furthermore, the growing integration of digital technologies, including connected dialysis machines and AI-powered treatment monitoring systems, is transforming patient management and enabling remote oversight by clinicians

- The shift toward home-based dialysis and personalized treatment plans, supported by portable and easy-to-use devices, is significantly enhancing patient comfort and adherence, driving adoption across both developed and emerging markets

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Developing Regions

- The substantial cost associated with long-term dialysis and uremia management, coupled with limited healthcare infrastructure in low-income regions, poses a major challenge to widespread treatment accessibility

- For instance, patients in developing countries often face financial strain due to recurring dialysis expenses and the unavailability of subsidized healthcare programs, restricting consistent access to life-saving treatments

- Addressing these challenges through cost-effective technologies, affordable dialysis solutions, and public-private healthcare partnerships is essential to ensure broader treatment coverage and equity. Companies such as Baxter and Fresenius are focusing on manufacturing low-cost dialysis equipment to enhance affordability

- In addition, the shortage of skilled nephrologists and specialized renal care centers in certain regions further limits the effective management of uremia, particularly in rural and underserved areas

- While international organizations and governments are increasing efforts to expand renal healthcare infrastructure, the pace of improvement remains gradual, creating disparities in treatment accessibility and quality across different geographies

- Overcoming these barriers through healthcare policy reforms, expanded insurance coverage, and innovative financing models will be crucial for ensuring sustainable growth of the global uremia treatment market

Uremia Treatment Market Scope

The market is segmented on the basis of treatment type, drug type, mode of administration, distribution channel, and end user.

- By Treatment Type

On the basis of treatment type, the uremia treatment market is segmented into hemodialysis and peritoneal dialysis. The hemodialysis segment dominated the market with the largest revenue share of 46.5% in 2024, primarily due to its strong clinical effectiveness and widespread availability in hospitals and dialysis centers worldwide. It remains the preferred therapy for patients with end-stage renal disease (ESRD) because it effectively removes toxins and excess fluids from the blood. The segment benefits from technological advancements such as automated machines, biocompatible membranes, and real-time patient monitoring systems that improve treatment efficiency. In addition, favorable reimbursement policies and the presence of leading service providers such as Fresenius Medical Care and DaVita have further strengthened its dominance. The increasing global prevalence of CKD and growing healthcare expenditure are also contributing to sustained segmental growth.

The peritoneal dialysis segment is projected to witness the fastest growth rate during the forecast period, driven by its convenience and suitability for home-based treatment. It allows patients greater autonomy and flexibility, reducing the need for frequent hospital visits. Advancements in automated peritoneal dialysis (APD) systems and portable devices are making treatment simpler and safer for patients. Moreover, supportive government initiatives encouraging home healthcare and patient-centric care models are fueling adoption. The rising geriatric population, which prefers less invasive and more comfortable therapies, also contributes to segment growth. Increasing healthcare investments in developing countries are expanding peritoneal dialysis accessibility globally.

- By Drug Type

On the basis of drug type, the market is segmented into potassium-sparing diuretics, angiotensin-converting enzyme (ACE) inhibitors, angiotensin-receptor blockers (ARBs), beta blockers, NSAIDs, oral anticoagulants or antiplatelets, and others. The ACE inhibitors segment dominated the market in 2024, owing to their critical role in lowering blood pressure, reducing proteinuria, and slowing the progression of kidney damage in uremia patients. These drugs are widely used as first-line therapy in chronic kidney disease management due to their dual cardiovascular and renal protective benefits. The segment’s dominance is supported by the availability of a wide range of ACE inhibitors and their inclusion in standard nephrology treatment guidelines. Furthermore, continuous research into new formulations with improved renal safety profiles is enhancing their clinical adoption. Increasing awareness among healthcare providers regarding early intervention for hypertension and uremic complications further drives demand. The rising global prevalence of hypertension and diabetes is also fueling segment growth.

The angiotensin-receptor blockers (ARBs) segment is expected to witness the fastest growth rate during the forecast period due to their better tolerability and lower incidence of side effects compared to ACE inhibitors. ARBs are often prescribed to patients who cannot tolerate ACE inhibitors, making them an important alternative therapy. The growing focus on combination treatments using ARBs and other antihypertensive drugs enhances their therapeutic scope. Increasing availability of generic ARBs and strong clinical evidence supporting their renal protective effects are expanding their use. Moreover, rising patient preference for long-term oral therapies with minimal adverse reactions supports segment acceleration. The segment also benefits from growing healthcare access and medication affordability in emerging markets.

- By Mode of Administration

On the basis of mode of administration, the market is segmented into injectable, oral, and others. The injectable segment dominated the uremia treatment market in 2024, driven by the extensive use of injectable erythropoiesis-stimulating agents (ESAs), anticoagulants, and other dialysis-related medications. Injectable drugs provide faster action and are essential for managing anemia and clotting disorders in patients undergoing dialysis. Their usage is highly preferred in hospital and clinical settings under medical supervision, ensuring accurate dosage and patient safety. The growing demand for parenteral therapies and the introduction of biosimilar injectables are strengthening this segment’s presence. Moreover, manufacturers are developing advanced formulations that offer sustained release and improved patient outcomes. The prevalence of severe uremic cases requiring immediate medical intervention further supports the dominance of injectable treatments.

The oral segment is projected to exhibit the fastest CAGR during the forecast period due to the increasing demand for convenient, long-term treatment options. Oral medications such as ACE inhibitors, ARBs, phosphate binders, and beta-blockers play a crucial role in managing CKD-related uremia outside hospital settings. The shift toward outpatient and homecare management is encouraging patients to adopt oral therapies that ensure better adherence and quality of life. Rising pharmaceutical R&D investments in renal-safe oral formulations are expanding therapeutic availability. The growing accessibility of oral drugs through retail and online pharmacies also supports this segment’s rapid growth. In addition, patient education programs promoting early-stage medication management are contributing to increased oral therapy adoption.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the market in 2024, supported by their role as the primary point of access for critical dialysis drugs and emergency renal treatments. Hospitals are key centers for diagnosing and managing uremia, especially in advanced cases requiring intensive care. The segment benefits from direct collaboration between nephrologists and pharmacists, ensuring appropriate drug administration and continuous monitoring. In addition, hospitals maintain ready stock of essential injectables and dialysis-related supplies, ensuring uninterrupted patient care. Rising hospital-based dialysis procedures and government support for specialized renal centers are reinforcing segment dominance. The growing number of multi-specialty hospitals equipped with advanced nephrology units further strengthens the hospital pharmacy network.

The online pharmacies segment is anticipated to record the fastest growth rate over the forecast period due to increasing digitalization of healthcare and rising consumer preference for convenience. Online platforms enable easy access to chronic kidney disease medications, home delivery options, and competitive pricing advantages. The surge in telehealth consultations and e-prescriptions has boosted the adoption of online pharmacies among uremia patients. Governments in emerging economies are also supporting digital pharmacy regulations, improving accessibility and trust. Moreover, online channels offer subscription-based medicine delivery, ensuring continuity of long-term treatments. Growing internet penetration and smartphone usage are accelerating the segment’s global expansion.

- By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market in 2024, accounting for the largest revenue share due to the high concentration of dialysis facilities and advanced renal care infrastructure. Hospitals provide comprehensive treatment for both acute and chronic uremia cases, including emergency interventions and complex dialysis sessions. The availability of specialized nephrologists, trained staff, and high-end dialysis systems ensures optimal patient outcomes. In addition, hospitals benefit from reimbursement programs that cover dialysis and uremia-related treatments. The segment’s growth is supported by the expansion of public and private hospital networks, particularly in North America and Europe. Increasing hospital admissions due to rising CKD prevalence continues to sustain strong demand for in-hospital treatment services.

The homecare segment is projected to grow at the fastest rate during the forecast period, driven by increasing patient preference for comfort, flexibility, and reduced treatment costs. Technological advancements in portable dialysis devices and home-based monitoring systems are enabling patients to safely manage treatment from home. The growing trend toward personalized care and self-managed therapies is fostering market expansion. Moreover, healthcare providers are offering structured home dialysis training programs, enhancing patient confidence and safety. Government initiatives promoting home healthcare reimbursement further encourage adoption. As awareness about home-based renal care improves, the homecare segment is expected to play a pivotal role in reshaping the future landscape of uremia management globally.

Uremia Treatment Market Regional Analysis

- North America dominated the uremia treatment market with the largest revenue share of 40% in 2024, supported by well-established healthcare infrastructure, high disease prevalence, and the presence of major dialysis service providers and pharmaceutical companies driving innovation in uremia management

- Patients in the region benefit from well-established healthcare infrastructure, broad availability of hemodialysis and peritoneal dialysis centers, and the presence of leading players such as Baxter International and Fresenius Medical Care offering innovative renal care solutions

- This widespread adoption is further supported by favorable reimbursement frameworks, high healthcare expenditure, and a growing focus on home-based dialysis and personalized renal therapies, establishing North America as a key hub for advanced uremia management and treatment innovation

U.S. Uremia Treatment Market Insight

The U.S. uremia treatment market captured the largest revenue share of 82% in 2024 within North America, driven by the high incidence of chronic kidney disease (CKD), lifestyle-related disorders such as diabetes and hypertension, and the widespread availability of advanced dialysis infrastructure. Patients are increasingly opting for home-based hemodialysis and peritoneal dialysis, supported by strong reimbursement coverage and healthcare innovation. The presence of major players such as Baxter, DaVita, and Fresenius Medical Care continues to strengthen the U.S. market. Moreover, the integration of AI-powered dialysis monitoring systems and remote patient management solutions is propelling the adoption of next-generation uremia therapies across the country.

Europe Uremia Treatment Market Insight

The Europe uremia treatment market is projected to grow at a significant CAGR throughout the forecast period, primarily fueled by the increasing prevalence of renal disorders, supportive government initiatives, and technological advancements in dialysis treatment. Countries such as Germany, France, and the U.K. are witnessing rising adoption of home-based and automated dialysis systems. The region’s strong focus on improving healthcare accessibility and implementing cost-effective renal care programs is further driving market expansion. Growing collaborations between research institutions and pharmaceutical firms to develop innovative therapeutics are also shaping the European market landscape.

U.K. Uremia Treatment Market Insight

The U.K. uremia treatment market is anticipated to expand at a noteworthy CAGR during the forecast period, supported by the National Health Service’s (NHS) emphasis on early diagnosis and improved CKD management. Rising cases of hypertension and diabetes are contributing to the growing patient pool requiring dialysis and pharmacological intervention. In addition, the adoption of portable dialysis machines and telehealth solutions is facilitating home-based care. Increasing awareness of kidney health, along with the integration of digital tools for patient monitoring, is expected to sustain long-term market growth in the U.K.

Germany Uremia Treatment Market Insight

The Germany uremia treatment market is expected to grow at a substantial CAGR during the forecast period, driven by advanced healthcare infrastructure, a strong network of dialysis centers, and robust investment in biomedical innovation. German healthcare providers emphasize the use of high-efficiency dialysis membranes and biocompatible materials, ensuring improved patient safety and treatment outcomes. The nation’s focus on sustainability in medical device production and its adoption of AI-integrated dialysis systems are reinforcing market expansion. In addition, ongoing collaborations between public institutions and private dialysis service providers are enhancing accessibility to advanced renal care.

Asia-Pacific Uremia Treatment Market Insight

The Asia-Pacific uremia treatment market is poised to record the fastest CAGR of 25% during the forecast period of 2025 to 2032, driven by the growing burden of CKD, expanding healthcare infrastructure, and rising awareness about renal health in countries such as China, Japan, and India. The region’s rapid technological advancements in dialysis systems and increasing government initiatives promoting kidney health programs are supporting market growth. Furthermore, the emergence of local dialysis equipment manufacturers and the adoption of cost-effective treatment solutions are improving accessibility for a broader patient base. The increasing investment by global healthcare companies in Asia-Pacific further boosts regional market expansion.

Japan Uremia Treatment Market Insight

The Japan uremia treatment market is gaining momentum due to its aging population, advanced healthcare system, and early adoption of innovative dialysis technologies. The country places a strong emphasis on home-based and automated dialysis, ensuring convenience and continuity of care for elderly patients. The integration of IoT and AI-enabled dialysis devices for continuous monitoring is also transforming treatment practices. In addition, the Japanese government’s initiatives to support renal disease prevention and early intervention are further driving market demand. The presence of domestic innovators and partnerships with global firms are accelerating technological adoption in Japan.

India Uremia Treatment Market Insight

The India uremia treatment market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to the rising prevalence of kidney disorders, growing healthcare expenditure, and the government’s focus on expanding dialysis coverage under national health schemes. India’s growing network of dialysis centers and the entry of affordable domestic device manufacturers are making treatment more accessible. The increasing awareness of CKD management and improved healthcare infrastructure in Tier 2 and Tier 3 cities are boosting adoption rates. Moreover, the rise of public-private partnerships and telehealth-based renal care services is helping bridge the treatment gap, propelling India’s leadership within the regional uremia treatment market.

Uremia Treatment Market Share

The Uremia Treatment industry is primarily led by well-established companies, including:

- Fresenius Medical Care (Germany)

- Baxter (U.S.)

- DaVita Inc. (U.S.)

- B. Braun SE (Germany)

- NIPRO (Japan)

- Toray Industries, Inc. (Japan)

- Asahi Kasei Medical Co., Ltd. (Japan)

- Outset Medical (U.S.)

- Quanta Dialysis Technologies Inc (U.K.)

- Vifor Pharma (Switzerland)

- Amgen Inc. (U.S.)

- Cara Therapeutics (U.S.)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Medtronic (Ireland)

- Terumo Corporation (Japan)

- Fresenius Kabi AG (Germany)

- Johnson & Johnson Services, Inc. (U.S.)

- Sanofi (France)

- Novartis AG (Switzerland)

What are the Recent Developments in Global Uremia Treatment Market?

- In March 2024, U.S. surgical teams performed one of the first gene-edited pig-to-human kidney xenotransplants in a living recipient a high-profile milestone demonstrating that genetically modified porcine kidneys can function in humans and jump-started regulatory and industry momentum toward clinical xenotransplant trials to address organ shortages. The story was widely covered by major outlets and scientific journals

- In March 2024, the FDA approved vadadustat tablets for treatment of anemia due to chronic kidney disease in adults on dialysis a second oral HIF-PHI to reach the U.S. market. The approval followed large phase 3 data and marked further expansion of oral anemia therapies for dialysis patients, with regulatory attention on cardiovascular and thrombotic safety signals

- In June 2023, AWAK Technologies launched a pre-pivotal clinical trial in partnership with Singapore General Hospital to test its wearable peritoneal dialysis device (AWAK PD / later Viva Kompact). The trial built on first-in-human work and represents a concrete clinical advance toward a wearable, sorbent-based PD system that could let patients do dialysis “on the go.”

- In February 2023, the FDA approved daprodustat the first oral hypoxia-inducible factor prolyl hydroxylase inhibitor (HIF-PHI) approved in the U.S. for treatment of anemia in adults on dialysis. This approval added an oral alternative to injectable ESAs for dialysis-dependent patients, shifting anemia-management options in CKD care

- In August 2021, the U.S. Food and Drug Administration approved KORSUVA® (difesuch asfalin) injection the first therapy specifically approved to treat moderate-to-severe pruritus (itching) associated with chronic kidney disease in adults undergoing hemodialysis. The approval introduced the first targeted pharmacologic option for a common, debilitating uremic symptom and was followed by market launches in the US, Canada and other territories

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.